TD:CC - My Dividend Growth Portfolio March Update: Still Accumulating Cash

2023-04-10 03:17:06 ET

Summary

- The portfolio remains at record high levels of cash holdings, which is fine for the first time in a long time, cash is providing a decent return.

- Income growth is projected at 7.9% for the year, up from last month. This was primarily due to including an estimated return on cash.

- The Intel position has been completely disposed of and replacement positions purchased.

It's hard to believe we already have one quarter in the books for the year. Against my expectations, the markets are incredibly strong right now. It appeared they might fold when SVB collapsed, but they have shown some resiliency and bounced back hard. There is a significant amount of optimism right now.

While there are some pockets of bargains, there aren't many great ones. Many of the best ones result from the banking system's problems. On a comparative basis, the deals look even less appealing when compared to the (mostly) risk-free return on cash. In the preceding several years, holding cash as a dividend growth investor didn't make much sense. Putting the money back to work in more dividend growth stocks grew the income immediately versus hanging on to it indefinitely, waiting for prices to come down at zero interest. Today, an investor can afford to be patient with cash yielding better than most dividend growth stocks, even after a year or two of increases. True, prices may never be better than they are today over the next year or so; however, there isn't a lot of downside to being patient.

Portfolio Goals

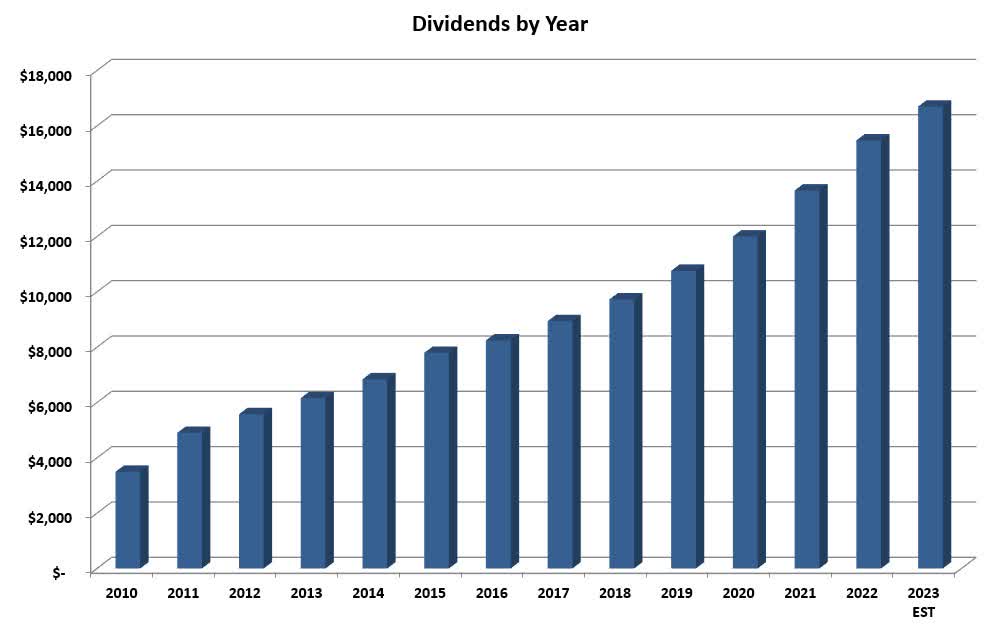

The portfolio goals are simple: Grow the income by 10% annually with dividends reinvested and 7% annually without reinvesting. This goal allows my income to double approximately every seven years while reinvesting and every ten years after I begin withdrawing the dividends. It's important to know that this portfolio has been closed to new capital since 2016. The graph below shows the steady progress of income growth.

{kind=link}

Portfolio Guidelines

I use guidelines to achieve my goals rather than rules. Rules imply something hard and fast, whereas guidelines are flexible but give a general direction to follow. I keep these simple, as I have found that complexity adds time without any real benefit. These have evolved over the years, the most recent being the addition of selling covered calls in certain circumstances.

- Invest in companies from the Champions and Contenders list with at least 15 years of dividend growth.

- Look for companies with a 3% starting yield and the potential to maintain a 7% dividend growth for decades. The growth is critical as it's impossible to continue growing income at 7% without reinvesting unless companies raise distributions by at least that amount.

- Replace (or sell covered calls against) significantly overvalued positions if the opportunity exists to reduce risk and increase income. In practice, this usually means higher quality at a higher yield.

- I want to see flat to mild payout ratio creep. A payout ratio growing from 30% to 35% over ten years is acceptable. One that has gone from 30% to 60% is not. I want companies to grow the dividend with earnings, not by increasing the payout ratio.

- Unless it is well-diversified across industries, no single sector should account for more than 20% of the income. This burned me in 2016 when several energy companies cut dividends.

Again, these are just guidelines and are flexible to accommodate what makes sense to achieve my overall goals. I follow a few other items but don't see them as integral to my investing. Instead, these tend to be more personal preferences. They include avoiding foreign companies because I don't enjoy accounting for the taxes and FX rates causing fluctuating dividends.

How am I doing so far in 2023?

Income is projected to be up 7.9% for the year, still below the 8% projection at the start of the year but well up from last month. The primary driver of change was adding a conservative estimate on interest from cash. I am holding cash in SWVXX with a 7-day yield of 4.68%.

The 7.9% growth projection is still below my goal of 10% annual income growth, but as I wrote about in the 2023 Look-Ahead , a down year wasn't unexpected, although not a given. The low growth estimate is due to the Intel ( INTC ) cut and Blackstone ( BX ) reduction. I am presently projecting a conservative $4.00 total dividend for Blackstone.

Typically, the projected income growth is low at the beginning of the year and ramps up as the year progresses. This ramping process generally is due to two factors. Firstly, I tend to keep my dividend increase projections conservative at the start of the year. And the second is the income grows as dividends are reinvested. This second effect will be less extreme this year due to projecting some interest from cash.

While the goals of this portfolio are strictly income-based, many readers are interested in the overall performance. Year to date, the portfolio is up by 3.6%, significantly trailing the S&P 500. However, given the massive outperformance last year, this isn't surprising. Since the start of 2017, the portfolio has returned 118%, significantly beating the S&P 500 over the same period, although there have been stretches of underperformance.

March's Dividend Increases

Sadly, there were no dividend increases in March.

April's Expected Increases

This month only brings three expected increases. One of these is particularly significant as Ameriprise ( AMP ) is the largest holding in the portfolio.

Ameriprise

At 6.7% of the portfolio, Ameriprise is the single largest holding. However, it accounts for a disproportionately small amount of income at just 3.5%. The company has an 18-year dividend growth streak, with 5 and 3-year growth rates of over 8%. Last year's increase was in the double digits at just over 10%.

So far, 2023 hasn't been fruitful for increases from asset managers. The meager increases shouldn't have surprised anyone, asset manager performance is directly tied to the market. However, Ameriprise bucked the trend last year, and everything points to a double-digit increase this year. While another 10%+ increase is possible, I'm projecting closer to the five-year average at 8%.

Apple ( AAPL )

Last year after Apple's stingy increase, I debated if it still belonged in the portfolio. At the time, it was the largest position in the portfolio. When the price of Apple seemed well ahead of the market at the end of August, I took the opportunity to reduce my position size. Today the company makes up 3.9% of the portfolio and is still one of the ten most significant positions, and accounts for 0.7% of the income.

Apple has an 11-year dividend growth streak, but the growth rate is steadily falling as the company focuses on buybacks over dividends. The 5-year growth rate is over 8%; however, last year's was 4.5%. While the company could give a more significant raise this year, it will likely continue focusing on buybacks. Another one-cent quarterly raise is probable, which equates to 4.3%.

Johnson & Johnson ( JNJ )

This Dividend King is the poster child for dividend growth investing. Johnson & Johnson has 60 years of dividend growth and 10, 5, and 3-year growth rates, all around 6%. This is impressive dividend growth consistency for such a long-time dividend grower. It will be interesting to see what the company does for a raise this year with the upcoming split.

I think we most likely see a dividend raise in the 4-5% range. However, the company has maintained a payout ratio in the low 40% range for years. When the company splits, it won't be able to support both the payout ratio and the dividend, and one will need to change. We will likely see the JNJ dividend drop post-split, similar to when Abbott Labs ( ABT ) split or when Altria ( MO ) split. I believe the total dividend paid will be the same when combined between JNJ and Kenvue (KVUE), but I think the company will take a conservative stance toward this year's increase. A delayed announcement is within the realm of possibilities.

Sales In March

As reported last month , the dividend cut by Intel led me to dispose of the position. The process was finished in March. I don't automatically sell on a dividend cut, as I like to evaluate each situation on its merit. However, Intel had been on my review list for quite a while. The company's constant failures in execution caused me to lose faith. The company has plenty of potential, as the company generates mountains of cash, but there are investments better suited to my portfolio now.

Purchases in February

I make two kinds of purchases. The first is replacement purchases for companies that have been sold, and the second is regular reinvestment of dividends. With replacement purchases, the goal is to increase income, income growth potential, and portfolio quality. Unfortunately, hitting all three is rare, so I usually settle for two out of three. When it comes to regular purchases, my focus is more on bargain prices in companies that meet the portfolio's goals.

Replacement Purchases

The proceeds from the sale of Intel have been fully reinvested. Unfortunately, given the high yield of Intel at the time of the cut, I could not replace the income lost. The combination of companies I selected replaced only 59% of the pre-cut income. However, the replacements will provide superior dividend growth in the long run. These were all additions to existing positions. The table below shows the number of shares added with the Intel proceeds.

| Company |

| Shares |

| CME Group ( CME ) |

| 2 |

| Realty Income ( O ) |

| 4 |

| Enterprise Products Partners ( EPD ) |

| 34 |

| Home Depot ( HD ) |

| 2 |

| CVS ( CVS ) |

| 12 |

| PepsiCo ( PEP ) |

| 2 |

| Blackstone Group |

| 2 |

| Prudential Financial ( PRU ) |

| 2 |

Regular Purchase

At times last month, some good buys existed, although not necessarily the ones I wanted to add. Unfortunately, this portfolio doesn't hold any bank stocks, although I considered starting a position last month. Instead, I decided to add to holdings in my other portfolios. I made more purchases last month than the previous couple, and the cash balance remains at historic highs. Below are the additions and the average price paid for the month.

- Visa ( V ), 1 share, $217.47

- CME Group, 3 shares, $180.10

- Prudential, 1 Share, $78.77

- Home Depot, 1 share, $282.00

- CVS, 2 shares, $150.69

What Else am I watching?

The big story last month was the bank failures, which led to significant price drops in banks. But the damage wasn't limited to the banks, as everything touching the financial sector was seemingly affected. While the insurance companies I watch have yet to reach the bargain level I sought, many other financial companies did.

I added significantly to my U.S. Bank ( USB ) and Toronto-Dominion Bank ( TD ) positions. I also started a position in Charles Schwab ( SCHW ) but quickly closed it for a 15% gain-I would have loved to have held it for the long term, but sometimes in extreme uncertainty, I will take a quick profit on the chance things get worse. I was tempted by some of the smaller, harder-hit regional banks; the risk-reward looked (and still looks) good.

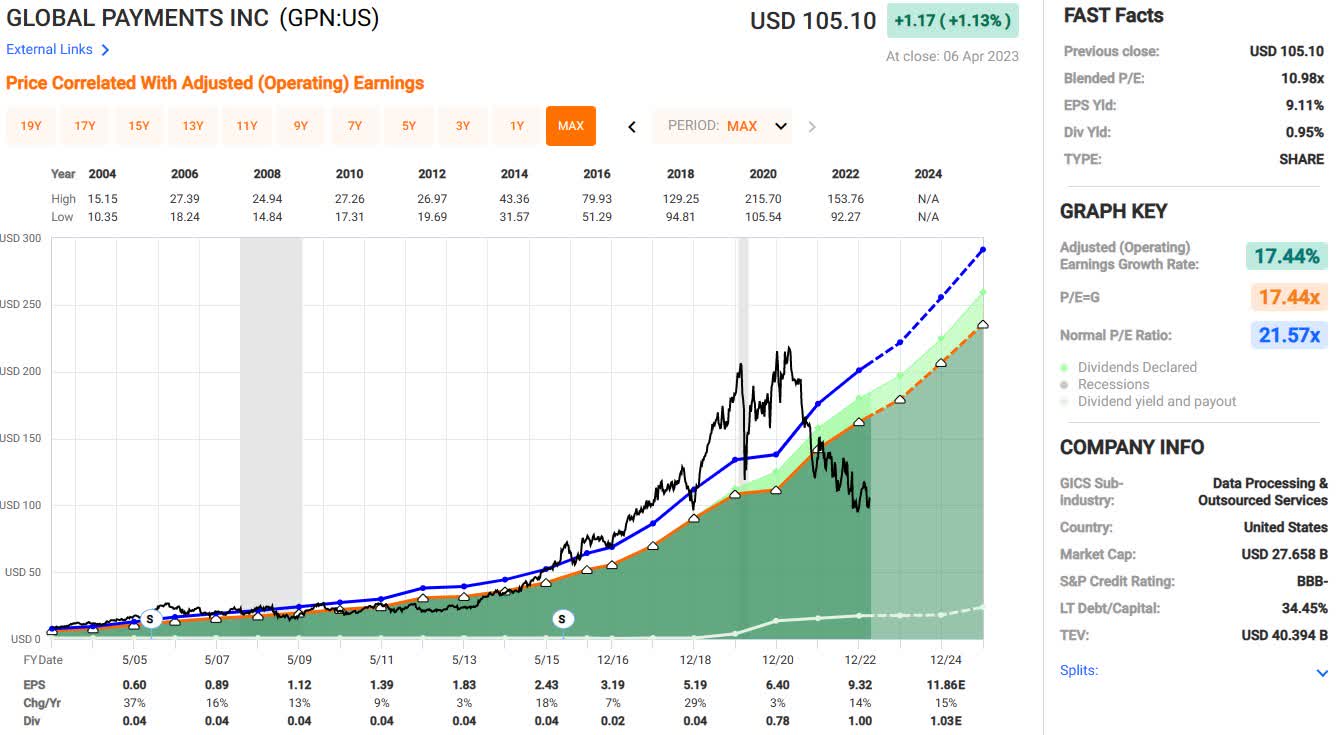

Payment companies were also hit hard and offered some fantastic bargains. Fidelity National Information Services ( FIS ) and Global Payments ( GPN ) were already beaten down and are available at historically high yields. The fast graph below shows the consistent growth of GPN, and earnings are expected to be in the double digits for the foreseeable future.

{kind=link}

While banks occupy many of the top spots in my bargain watch list, retailers maintain high positions. Williams-Sonoma ( WSM ) last month announced a 15% dividend increase and now yields over 3%. WSM joins my other favorite retailers, Home Depot, Lowe's ( LOW ), Tractor Supply Co ( TSCO ), and Best Buy ( BBY ), as significant bargains, although these could see better buy points in a recession.

Nexstar ( NXST ) continues to be a massive bargain based on historical yields. Others in the communication world also remain bargains. Comcast ( CMCSA ) continues to hang out near historically high yields, as does Verizon ( VZ ) for those looking for a high-yield option.

I am still watching to see if Automatic Data Processing ( ADP ) falls to a 2.5% yield. It seems to want to but can't quite get there, kind of like waiting for Home Depot to hit that 3% yield mark. A 2.5% yield on ADP is only my first buy point, and I'm passing over other high-quality stocks that are better bargains to take ADP at that point. However, I have been looking to expand my ADP position and am willing to reach a little.

Finally, as I have for the last several months, I continue to make small daily purchases of Schwab U.S. Dividend Equity ETF ( SCHD ). The ETF is appealing when there are a lot of "just ok" buys but not many extreme bargains. The yield is near its top historical end, and the dividend growth has a strong track record.

Final Thoughts

With a decent yield on cash, there is no reason to rush into buying anything. Unless we see a significant drop in the market, my cash pile will continue to outpace reinvestments. I'm ok with that, as there seems to be a disconnect between the safe yields and the market.

This report came out a little later than usual, so I hope readers still find it useful. Thanks for reading, and happy investing!

For further details see:

My Dividend Growth Portfolio March Update: Still Accumulating Cash