QYLD - My Income Portfolio: A Stairway To Heaven

Summary

- As in Led Zeppelin’s famous song, for me, investments in high-dividend securities represent a kind of stairway to heaven.

- Indeed, their steady flow of money relieves psychological pressure during times of market uncertainty and helps me experience them with greater peace of mind.

- During February, I made some purchases on weakness, increasing my positions in various names: CCAP, RQI and UTF.

- I also have on the horizon the inclusion of ORCC in my portfolio, a specialty finance company focused on lending to U.S. middle-market companies.

Brunelleschi's Dome

By whichever way one arrives, Florence announces itself from afar with the unmistakable outline of its cathedral dome, built by Filippo Brunelleschi between 1420 and 1436 and which Florentines call the "Cupolone" (a nickname from which I was inspired for my main portfolio). A symbol of Florence and the Renaissance, its mighty mass soars over the roofs of houses with red brick and white ribs projecting it skyward.

Brunelleschi's admirable innovation was to erect its vault without the use of supporting armatures. In fact, it is formed by two distinct domes: an inner one, more than two meters thick, consisting of large arches made of ashlars arranged in a "herringbone" pattern; and an outer roofing dome covered with terracotta tiles and punctuated by eight white marble ribs.

Between the two domes runs a path of narrow, dark corridors, initially designed to allow workers to build and maintain the structure, and later opened to the public so that they could climb up to the large lantern at its top. My parents took me to climb the 463 steps and explore the dome from the inside as a child, sparking my imagination.

The first part of the ascent is indeed comfortable and smooth, but as one ascends, the steps become steeper and the radius of curvature of the outer dome makes the walk increasingly difficult, until the final steep and narrow ramp that leads to the open air. At its base, fearful, I stopped, and had to postpone the "conquest" of the summit until my later youth.

Stairway to Heaven

Led Zeppelin released this celebrated suite in 1971, but it wasn't until a few years later that it became part of my personal hit parade, and I have been listening to it ever since, losing myself in the magical atmosphere created by the initial guitar arpeggio and the sound of the sweet flute. I like to compare the ascent of Brunelleschi's dome to Led Zeppelin's "stairway to heaven": a path that likewise progresses from quiet and smooth to increasingly tight and pressing, until it explodes with the breathtaking view of Florence from above.

Everyone has their own, personal stairway to heaven. Ever since I started investing in the U.S. financial market, I have always thought of investing in high-dividend securities as a kind of stairway to heaven, after so many years of ups and downs in my job. A stairway to climb step by step, thanks to the dividends that began to arrive regularly and created that "virtuous circle" that I would reluctantly give up (as well as providing a "parachute" during market crashes).

The Secret to Riches

The secret to riches is the same as the secret to comedy: timing. (Max Skinner from the movie A Good Year ).

While trying to remain as faithful as possible to my habit of not increasing the cost-basis price of my holdings, at the end of February I made some purchases on weakness, increasing my positions in two Cohen & Steers funds: Quality Income Realty ( RQI ) and Infrastructure ( UTF ). Their load price moved up, but only by a small percentage.

Also, a small buy of CCAP, whose subsequent rebound from the lows made me very happy, despite its tax inefficiency for me as an Italian.

I also lightened, on an uptick, my positions in BlackRock Science And Technology Trust ( BST ) and Royce Value Trust ( RVT ), rebalancing the weights of their respective portfolios and creating additional liquidity to increase my positions in two Eaton Vance funds that interest me: Tax-Adv. Global Dividend Opps ( ETO ) and Tax-Adv. Dividend Income ( EVT ), as well as John Hancock Tax-Adv. Dividend Income ( HTD ) and, again, Cohen & Steers Infrastructure ( UTF ).

The latter four are all CEFs that I have been following for some time, waiting for the profitable moment (assuming it comes) to mediate their prices upward as little as possible. As I have said in previous articles, I never follow the trend of the market and always try to buy in the downside moments so as not to find myself "caught off guard" at the next crash. I know how nerve-wracking it is to wait for the rise from the lows during panic phases, which is why I never buy my names in moments of market mania. Today, we are still seeing attractive prices when projected over the long term and compared to the highs of the last three years, so I decided here and there to make a few targeted purchases without waiting any longer.

Then maybe the market will correct and I will regret not having waited… but that's part of the game.

My Overall Portfolio's Weights

As you may know, my investments are divided into three different income portfolios: the above mentioned Cupolone, my primary CEF portfolio; Giotto, comprised of ETFs that adopt a covered-call strategy; and Masaccio, my "tactical" portfolio.

In speaking of the holdings in the Giotto portfolio, I take this opportunity to point out an interesting article by Jason Zweig, entitled "Why Investors Are Piling Into Funds That Promise Not to Beat the Stock Market," in the Wall Street Journal on Feb. 10, devoted entirely to ETFs that follow a covered-call strategy.

This is the complete list of the 26 titles that make up my three portfolios today:

Cupolone

- BlackRock Science And Technology Trust ( BST )

- Calamos Dynamic Convertible and Income ( CCD )

- Calamos Global Total Return ( CGO )

- Eaton Vance Enhanced Equity Income II ( EOS )

- Eaton Vance Tax-Adv. Global Dividend Opps ( ETO )

- Eaton Vance Tax-Adv. Dividend Income ( EVT )

- Guggenheim Strategic Opp ( GOF )

- John Hancock Tax-Adv. Dividend Income ( HTD )

- Pimco Corporate & Income Strategy ( PCN )

- Pimco Dynamic Income ( PDI )

- John Hancock Premium Dividend ( PDT )

- Pimco Corporate & Income Opportunities ( PTY )

- Cohen & Steers Quality Income Realty ( RQI )

- Special Opportunities Fund ( SPE )

- Cohen & Steers Infrastructure ( UTF )

- Reaves Utility Income Trust ( UTG )

Giotto

- JPMorgan Equity Premium Income ( JEPI )

- JPMorgan Nasdaq Equity Premium Income ( JEPQ )

- Global X Nasdaq 100 Covered Call ( QYLD )

- Global X Russell 2000 Covered Call ( RYLD )

- Global X S&P 500 Covered Call ( XYLD )

Masaccio

- Ares Capital Corp ( ARCC )

- Crescent Capital ( CCAP )

- Royce Value Trust ( RVT )

- Credit Suisse X Links Crude Oil Shares Covered Call ETN ( USOI )

- XAI Octagon FR & Alt Income Term Trust ( XFLT )

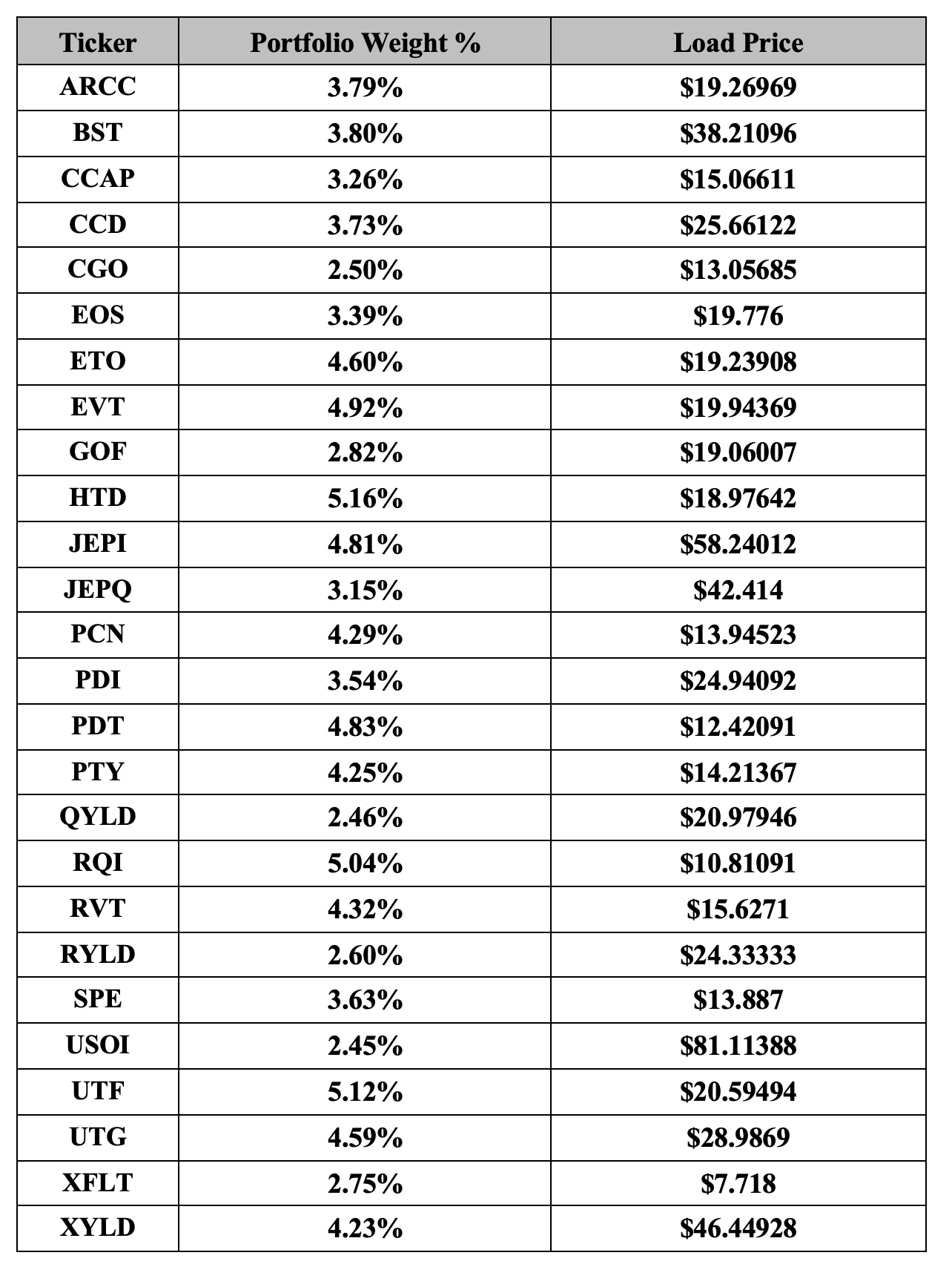

And these are the current weights of all the holdings in my portfolios, with their relative load prices:

{kind=link}

Note: The weight of each security is shown based on the current market price.

As can be easily verified by comparing the load prices of my holdings against their current market prices, the portfolio as a whole is making a loss, albeit a modest one, and partly offset by the rise of the dollar against the euro. This does not frighten me, as I consider myself a dividend investor looking at the long term, only marginally interested in additional possible capital gains at times when my stocks reach new highs and I decide to lighten their positions, as I have been doing for years now. But that's another story and I'll reevaluate over time, if the right conditions are met.

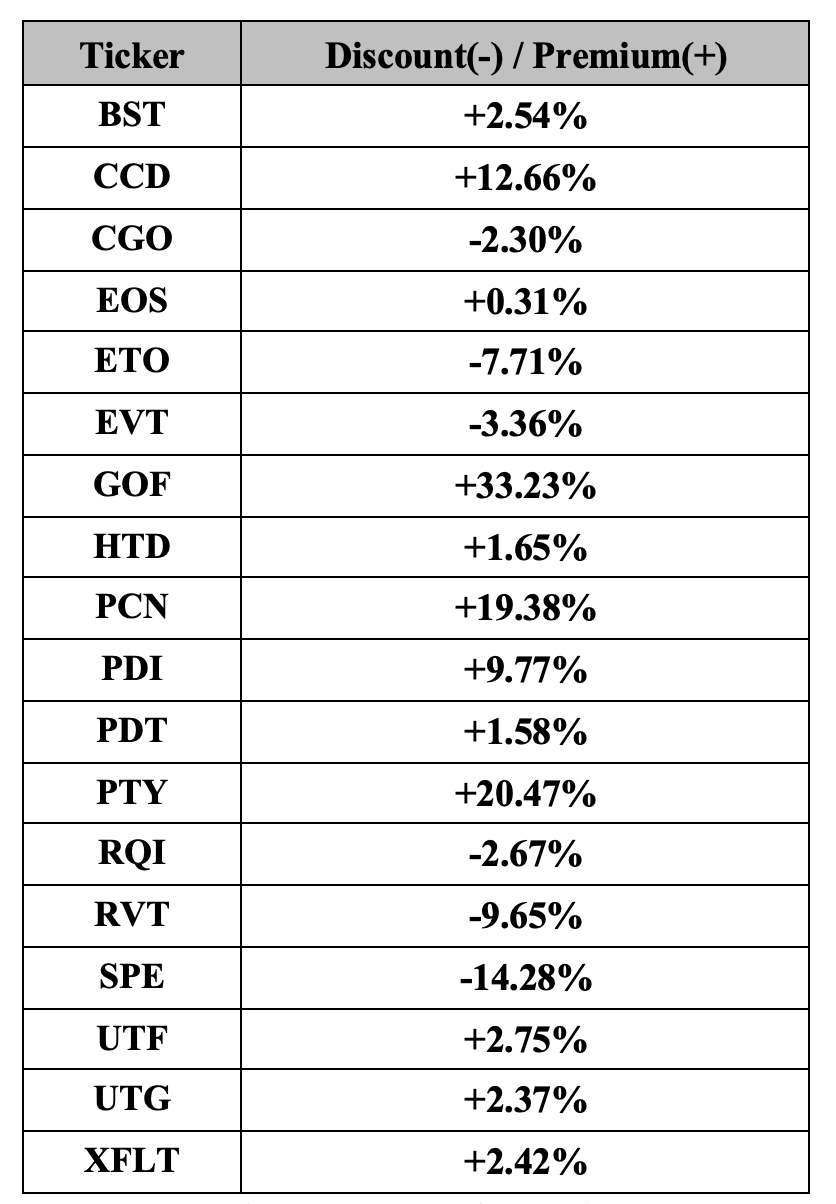

Discounts/Premiums of my CEFs

Before increasing already open positions, I always take a look at the relationship between the market price of the securities I am interested in and their NAV. The table below shows discounts and premiums for each CEF in my portfolio, with results that, in some cases, appear puzzling. As can be seen, the four fixed-income funds (GOF, PCN, PDI, and PTY) currently price at a premium to NAV that reaches and even exceeds double digits, peaking at 33+ percent for GOF. As far as I know, fixed debt and inflation are not friends, but evidently the market is chasing the yields of these funds, and this fact is driving up their premiums.

I take this opportunity to point out that all four of these funds were purchased by me at discount in the spring of 2020, and their positions have never been increased since. Let's say that on fixed debt I keep the engine idle and now I'm focusing more on equity funds, in the prospect of a future rise in the market (for the possible capital gains I mentioned above.)

As for the other CEFs, apart from CCD which has a double-digit premium, six quote at a discount while seven have a premium slightly above par. Here is a list of all 18 CEFs in my overall portfolio, showing their respective discounts or premiums (data as of Mar. 01, 2023):

{kind=link}

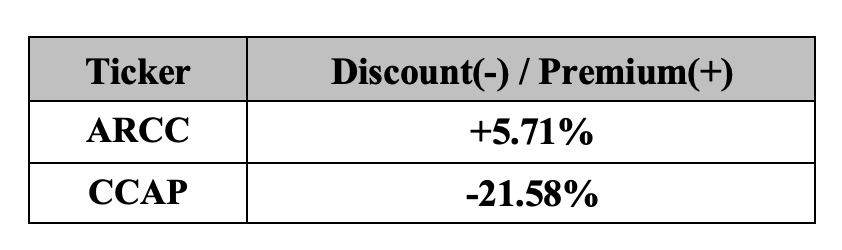

These 18 CEFs are also joined by the two BDCs, of which CCAP quotes at a steep discount to NAV while ARCC shows a premium of more than 5 percent (updated data as of 12/31/2022), as can be seen in the table below:

{kind=link}

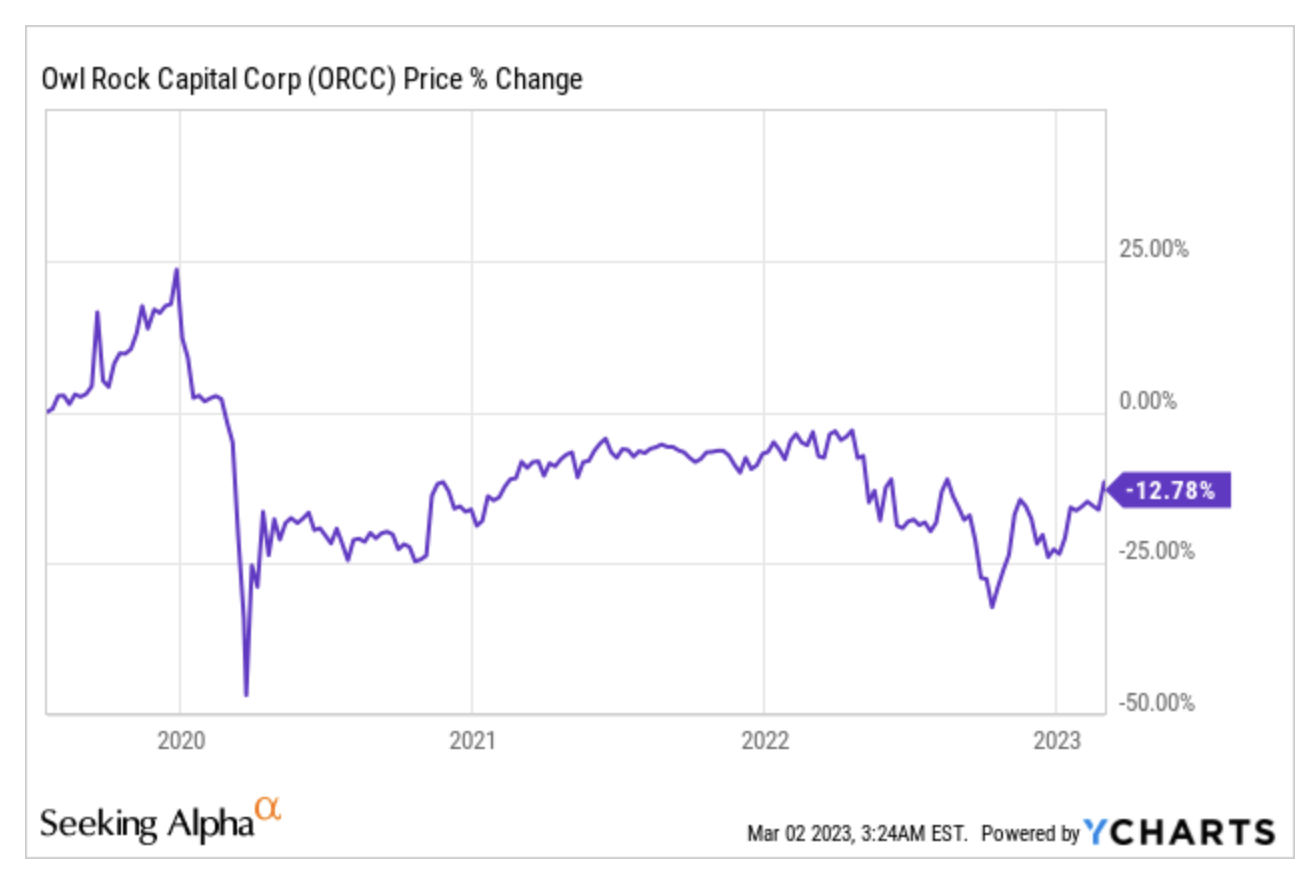

ORCC, a New Entry

Lately, I have been entertaining the idea of adding another BDC to the Masaccio portfolio, namely ORCC, a specialty finance company focused on the top of the capital structure (71% First Lien Senior Secured, 14% Second Lien Senior Secured), whose debt investments are 98% floating rate.

The performance of the stock is negative compared to launch, as can be seen from the chart below, with a sudden collapse in early 2020 (the start of the pandemic), a slow and gradual recovery until the outbreak of the war in Ukraine, but a comforting hold in the last year, although amid numerous ups and downs.

ORCC is a stock launched in 2018, capitalizing over $5 billion, trading at a 9.34 percent discount to NAV (updated data as of 12/31/2022), and offering a yield at the current price of around 9.5 percent on a quarterly basis.

For now, I have only put a little toe in this pond because, as always, I like to assess the performance of my holdings "from the inside": I will see over time whether and how much to increase my position.

{kind=link}

Bedtime Thought

Indeed, we cannot dwell enough on the merits of dividend-based financial strategies, whose steady flow is self-sustaining, relieving psychological pressure and helping to face the market downturns more calmly. The market at the moment lacks directionality amid concerns about continuing high levels of inflation and fears about future restrictive monetary policy moves that could result in a recession.

During the uncertainty, I continue to find meaning in the line of increasing the portfolio by buying on weakness or in downturns, and keeping the bar straight on my long-term goals. To do this, the wisest thing for me is to ignore the "noise" that accompanies us in these phases and that could lead us to rash moves in the wake of emotion.

"There's a lady who's sure all that glitters is gold and she's buying a stairway to heaven..." sang Robert Plant. As for me, I don't think all that glitters is gold, but even I, in my own way, am trying to buy my stairway to heaven. And so far, it's working.

For further details see:

My Income Portfolio: A Stairway To Heaven