XYLD - My Income Portfolio And Return Of Capital

2023-04-26 16:29:14 ET

Summary

- Eighteen of the twenty-six titles in my total portfolio are CEFs, whose distributions may consist of income, capital gain or return of capital.

- In this article, I decided to examine the components of their distributions for early 2023, so as to understand whether and how much is return of capital.

- Indeed, CEF managers’ reliance on return of capital has always been suspicious to me, even though it has little tax implication for me as an Italian.

- However, its most worrying aspect is that it lowers the quality of distributions, threatening their sustainability in the long term.

I Love My Dog

Cat Stevens released a song with this title on his first album (1967). At the time I was a child, I didn’t listen to Cat Stevens, and dogs scared me. A few years later, however, I bought my first Cat Stevens LP, “Tea for the Tillerman,” at a music cash & carry on the other side of Florence, where the records were all in bulk in huge boxes and you had to rummage through the entire store to find what you were looking for, assuming it was there.

So, I began to love Cat Stevens songs, all while I continued to dislike dogs, and this aversion lasted throughout my youth and for many more years until the day I met my wife, who loves dogs. Today I adore them too, especially Cesare, the Lagotto Romagnolo who joined the family a year ago. This Italian breed is a typical water dog of small-medium size that has been specially bred to find truffles on all kinds of terrain. Cesare is six years old, was given to us by some friends and has become an irreplaceable presence in our house because of his sweetness, friendliness, surrender and family participation (even if he occasionally takes out some chickens).

But even nicer is when I take him out for a kind of “meditative walk,” during which he shows all his ability to live in the present moment, guided only by his sense of smell. The trails he sniffs establish a direct relationship with reality, filtered through his nose, dragging both of us inside a life lived always in real time. I envy him because Cesare is able to do what I am only rarely able to, which is to live the “here and now,” combined with the extraordinary ability to let go of emotions and tensions by simply “shaking off.”

The “Here and Now” of Financial Markets

The energy disposed of, the situation overcome, Cesare gets rid of an emotion with that one movement: nothing more, nothing less. And then it is time to start again and discover something new. What an enviable reset! If only I, too, could find the strength to live the financial markets in the moment, without burdening my mind with tensions, emotions, expectations, hopes, disappointments...

No one can even imagine what the markets will do a week from now, a day from now, or even ten minutes from now. They will fluctuate and their fluctuation will be a sum of individual moments that will reverberate in the moods of us investors. Cesare can shake himself from time to time; I can’t do that. On the contrary, emotions add up inside me, not cancelling each other out, and their sum burdens my state of mind, upsets my serenity, and undermines my lucidity just when I need it most. All that happening during the time when I should be making conscious decisions to safeguard a portfolio threatened by specters such as inflation, recession or even stagflation.

Lately, however, I have been trying to shake myself off as well, and my mind has thus given birth to the decision to stop buying CEFs for my main portfolio (Cupolone), as I had imagined doing in past months. I decided to give myself time to see how the situation evolves, and to reflect on it in light of the consideration I will give in this article to one of the most controversial aspects of CEFs, namely the return of capital ('ROC'). Return of capital occurs when investors receive a portion of their original investment that is not considered income or capital gain.

Return of Capital, the “Stone Guest”

As in Aleksander Puškin’s famous tragedy, written in 1830 and titled The Stone Guest , return of capital is an unseen and disturbing presence, known to all but named by no one out of fear. In truth, CEF managers’ reliance on return of capital has always made me suspicious, even though theory says that it reduces an investor’s adjusted cost basis and has tax implications that many investors, especially if American, know (and exploit) better than I do, such as deferring some of the shareholder’s tax liability.

As for me, being Italian, once a year I receive from my bank a string of small refunds simply called “foreign dividend”, not subject to taxation, which should represent undue taxes related to returns of capital from my CEFs. I say should because no one has ever been able to explain this to me, being refunds coming directly from the corresponding bank in the US.

For a more in-depth discussion on this topic, I refer to an interesting article by Steven Bavaria entitled “ Return Of Capital For Dummies .” However, I have decided to examine one by one the components of the distribution of the eighteen CEFs in my total portfolio for early 2023, availing myself of the very up-to-date data provided on the CefConnect website, which I reproduce below.

My CEFs’ Return of Capital

As you may know, my investments are divided into three different income portfolios: Cupolone, my primary CEF portfolio; Giotto, comprised of ETFs that adopt a covered-call strategy; and Masaccio, my “tactical” portfolio. I summarize for brevity’s sake the total composition of my overall portfolio, in which there are precisely 18 CEFs, 5 ETFs, 2 stocks and 1 ETN, dividing the securities into Closed-End Funds and Other Income Vehicles:

Closed-End Funds

- BlackRock Science and Technology Trust ( BST )

- Calamos Dynamic Convertible and Income ( CCD )

- Calamos Global Total Return ( CGO )

- Eaton Vance Enhanced Equity Income II ( EOS )

- Eaton Vance Tax-Adv. Global Dividend Opportunities ( ETO )

- Eaton Vance Tax-Adv. Dividend Income ( EVT )

- Guggenheim Strategic Opportunities ( GOF )

- John Hancock Tax-Adv. Dividend Income ( HTD )

- PIMCO Corporate & Income Strategy ( PCN )

- PIMCO Dynamic Income ( PDI )

- John Hancock Premium Dividend ( PDT )

- PIMCO Corporate & Income Opportunity ( PTY )

- Cohen & Steers Quality Income Realty ( RQI )

- Royce Value Trust ( RVT )

- Special Opportunities Fund ( SPE )

- Cohen & Steers Infrastructure ( UTF )

- Reaves Utility Income Fund ( UTG )

- XAI Octagon Floating Rate & Alternative Income Term Trust ( XFLT )

Other Income Vehicles

- Ares Capital ( ARCC )

- Crescent Capital ( CCAP )

- JPMorgan Equity Premium Income ( JEPI )

- JPMorgan Nasdaq Equity Premium Income ( JEPQ )

- Global X Nasdaq 100 Covered Call ( QYLD )

- Global X Russell 2000 Covered Call ( RYLD )

- Credit Suisse X Links Crude Oil Shares Covered Call ETN ( USOI )

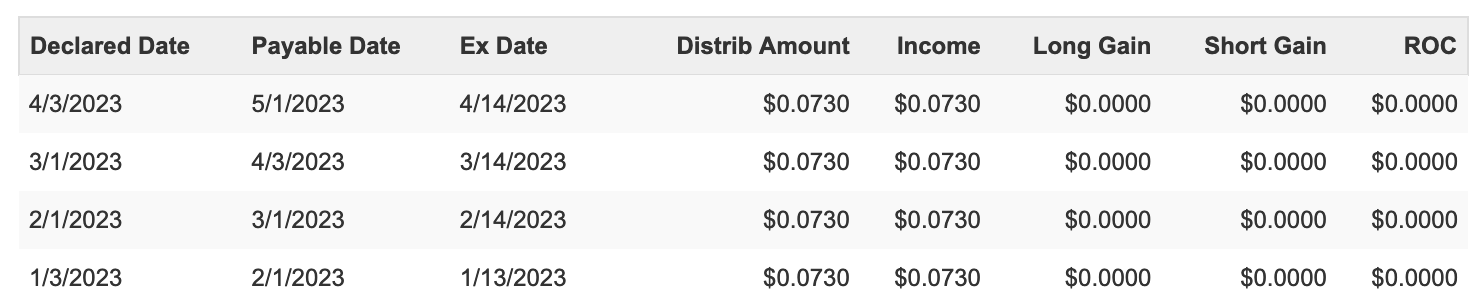

- Global X S&P 500 Covered Call ( XYLD )

Stocks, ETFs and ETNs pay a variable dividend that does not include return of capital, so the “problem” is confined to the 18 CEFs. For this reason, the analysis will not cover the 8 titles that I have grouped under “Other Income Vehicles.”

On the origin of the distributions of CEFs often comes the criticism from those who dislike this investment instrument, which I have found over the years to be very divisive, between rabid supporters and bitter enemies. I would like to place myself somewhere in the middle, appreciating its innumerable merits but equally recognizing its undeniable weaknesses. In any case, I know what I am getting and what I am giving up, and in this awareness, I believe I am in good company, since collectively, the 18 CEFs in my portfolio capitalize to over twenty billion dollars.

Some of them show positive NAV performance since launch, despite 2022 being the markets’ black year (and this, despite all the cautiously optimistic forecasts made by major investors for Italy’s largest financial newspaper at the end of 2021). BST, ETO, EVT, HTD, PDT, RVT, UTF, and UTG have indeed created value over time for their shareholders, even though some of them have repeatedly resorted to return of capital in the first months of the year for their distributions.

But let’s look in detail at the distributions of all my CEFs for these early months of 2023.

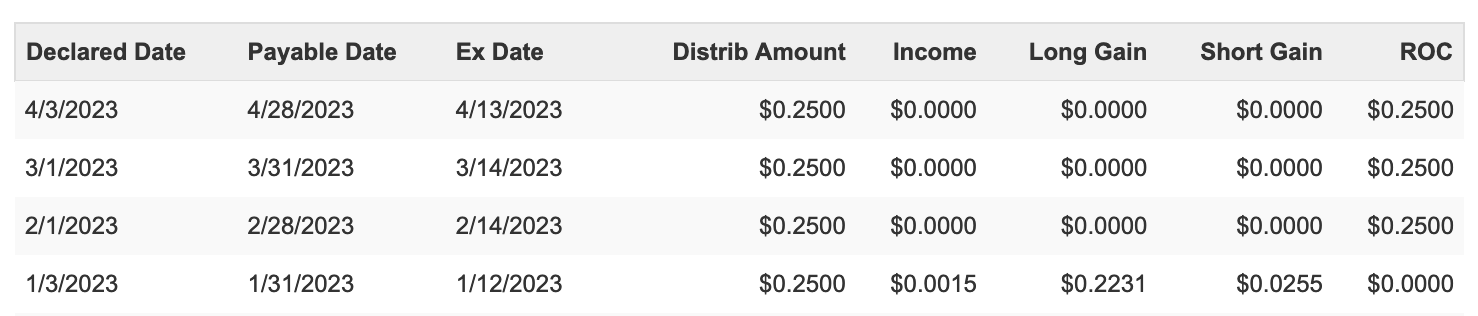

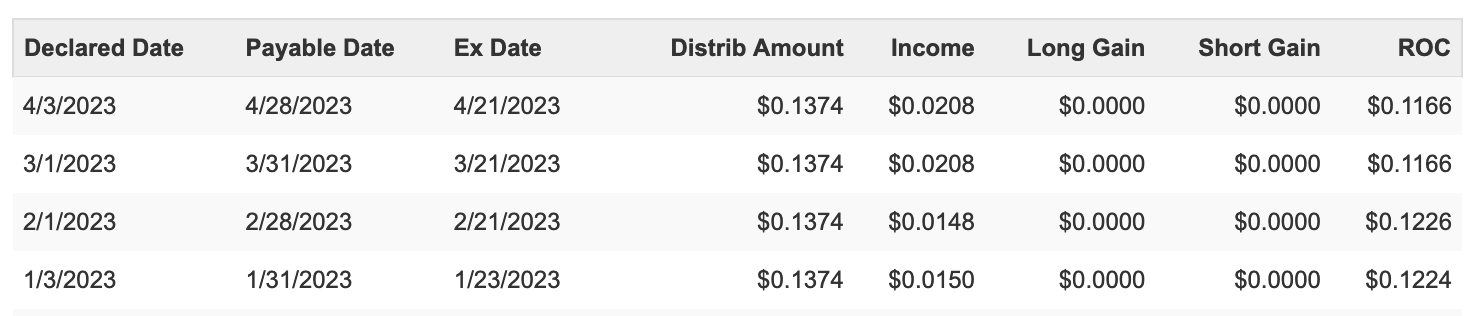

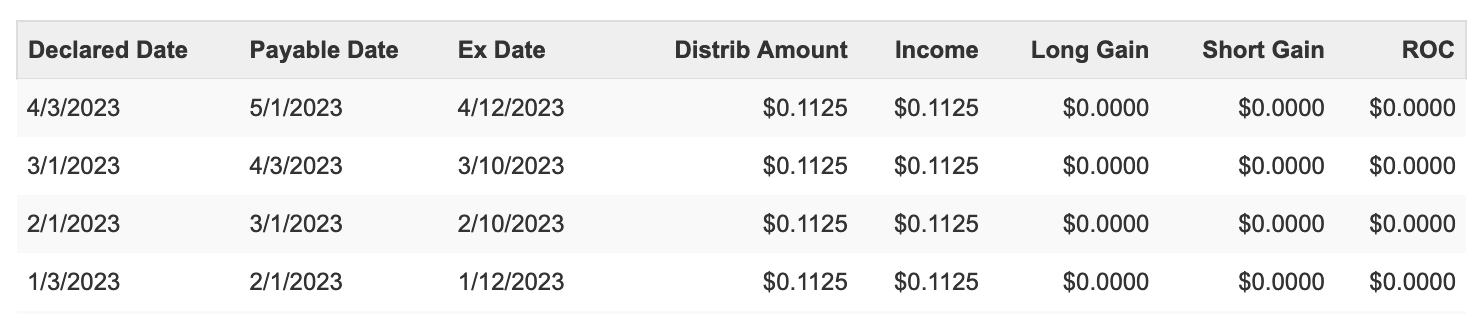

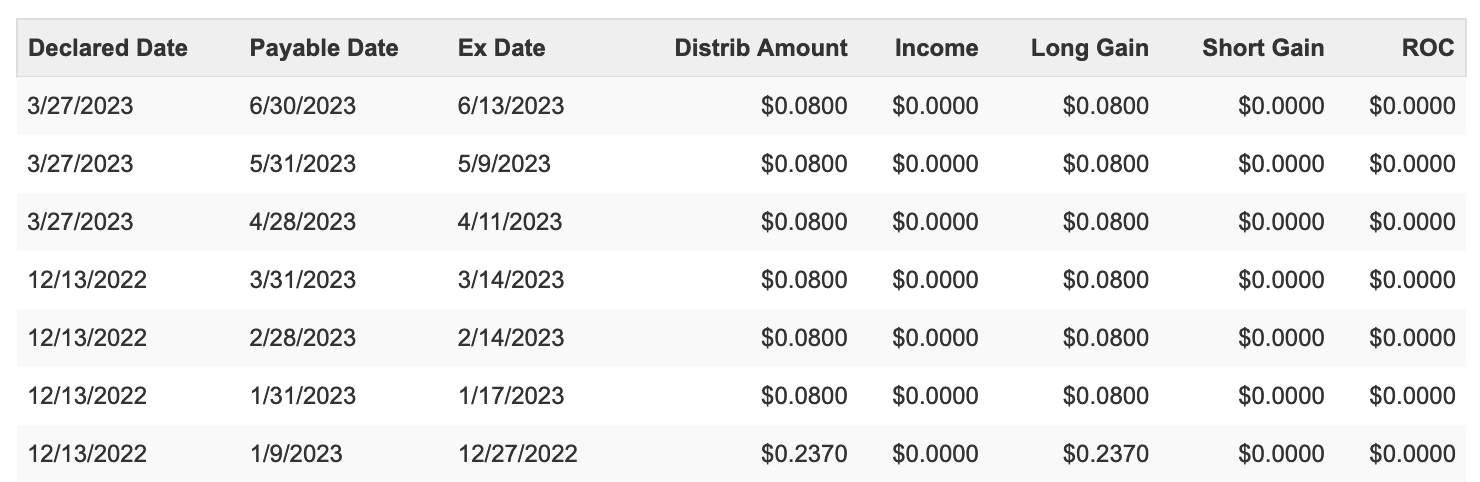

BST

{kind=link}

The last three distributions consisted exclusively of return of capital while the one in January was predominantly based on long-term capital gains.

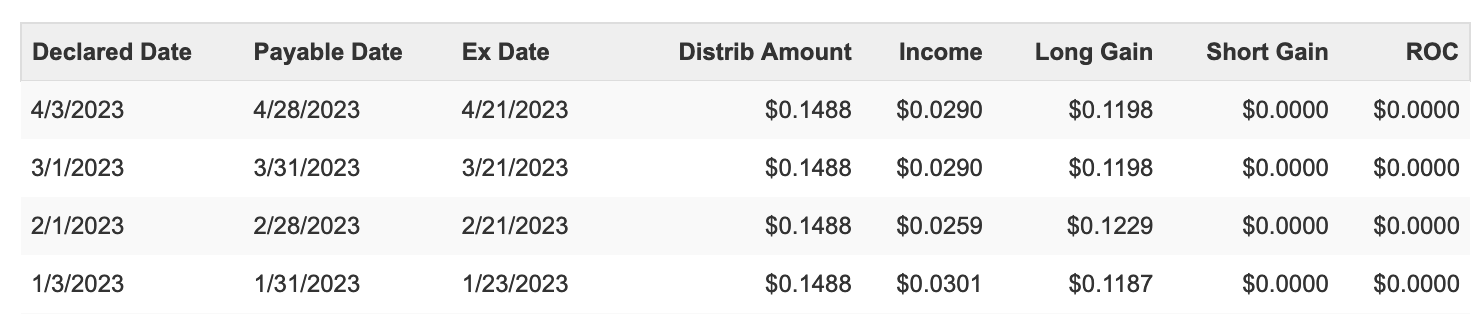

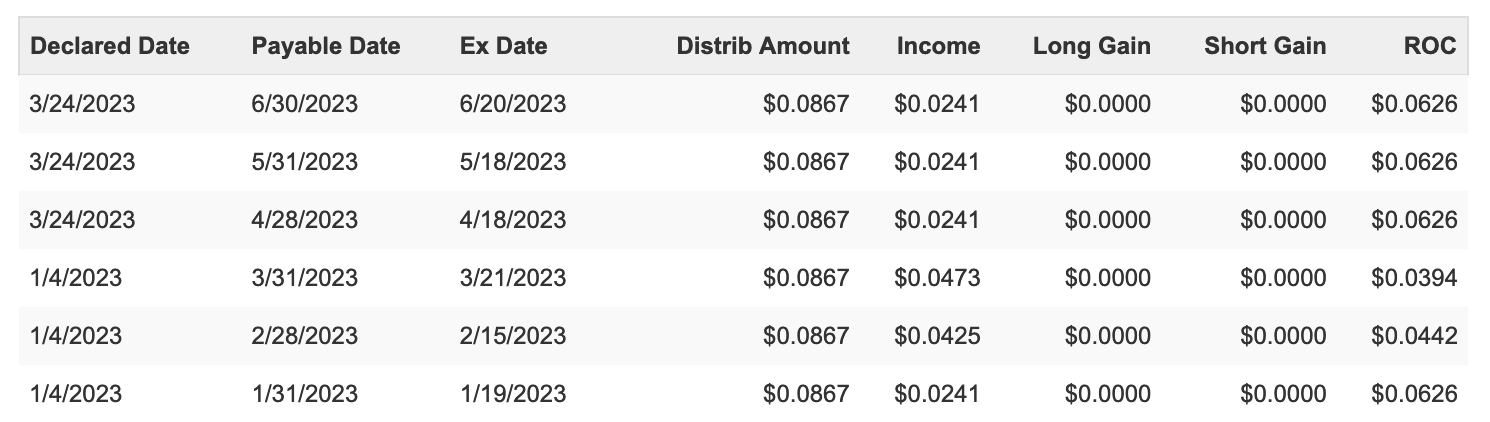

CCD

{kind=link}

Return of capital for April distribution, while the previous ones consisted almost exclusively of long-term and short-term capital gains.

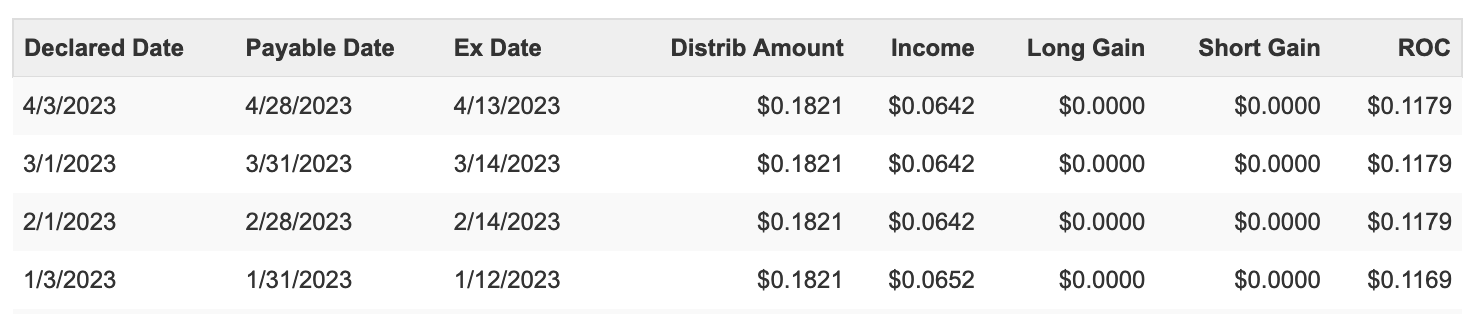

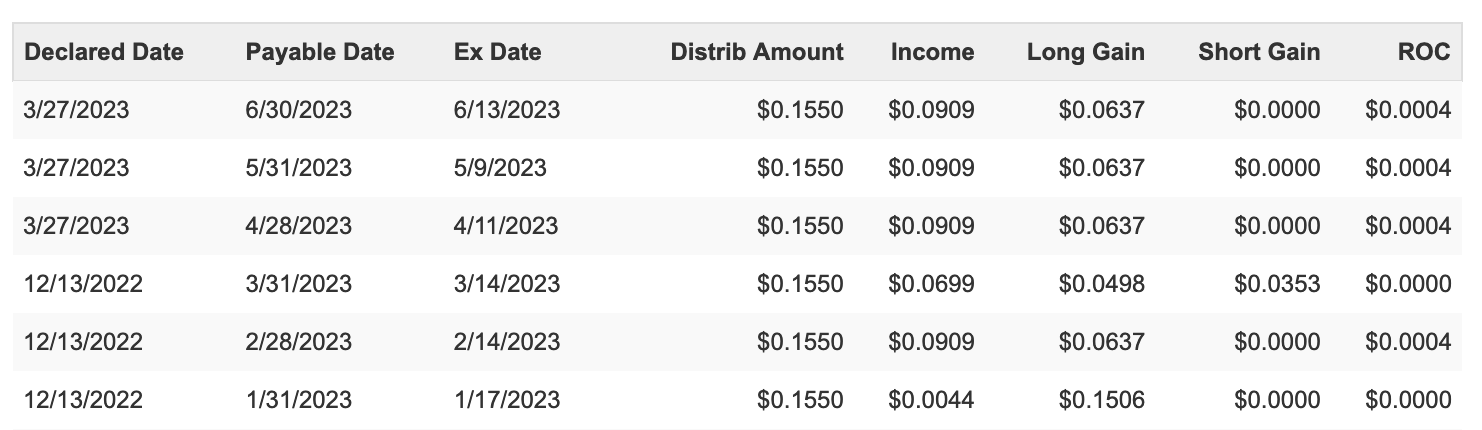

CGO

{kind=link}

After three months of return of capital, April saw long and short-term capital gains.

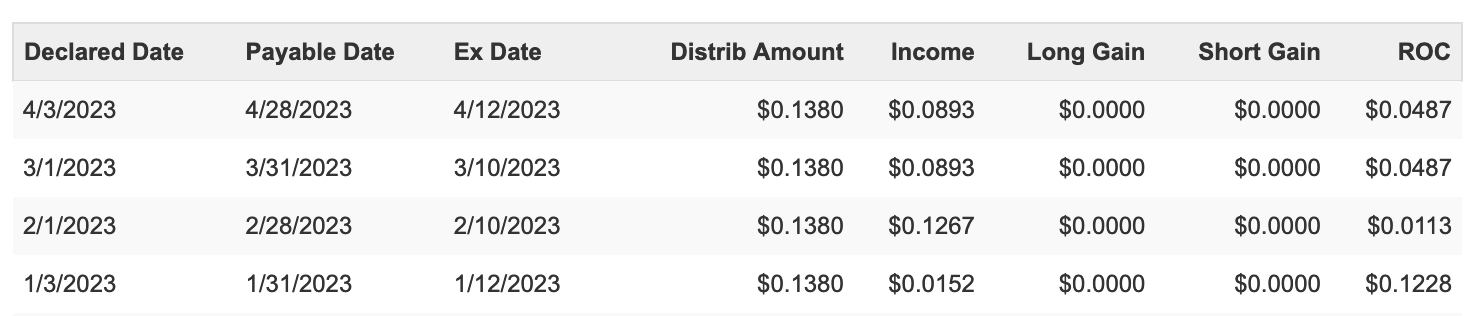

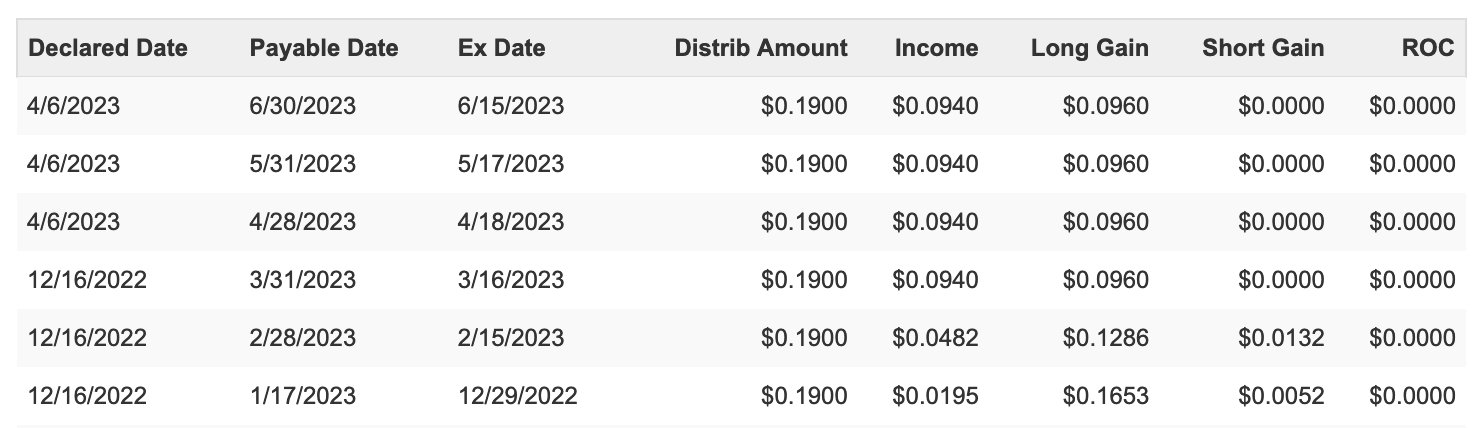

EOS

{kind=link}

The last four distributions consisted exclusively of long-term capital gains.

ETO

{kind=link}

A small percentage of income and the rest a return of capital for the last four distributions.

EVT

{kind=link}

A small percentage of income and the rest being long-term capital gains for the last four distributions.

GOF

{kind=link}

About one-third income and the rest a return of capital for the last four distributions.

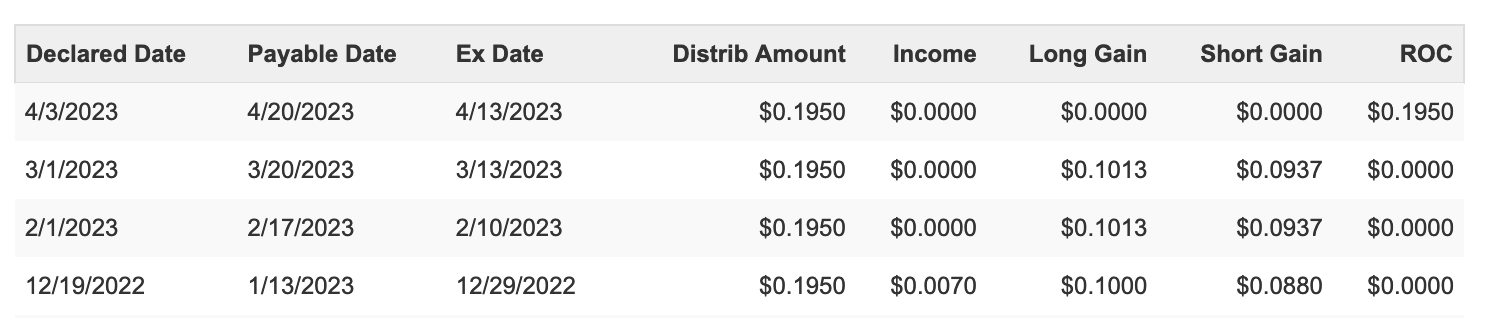

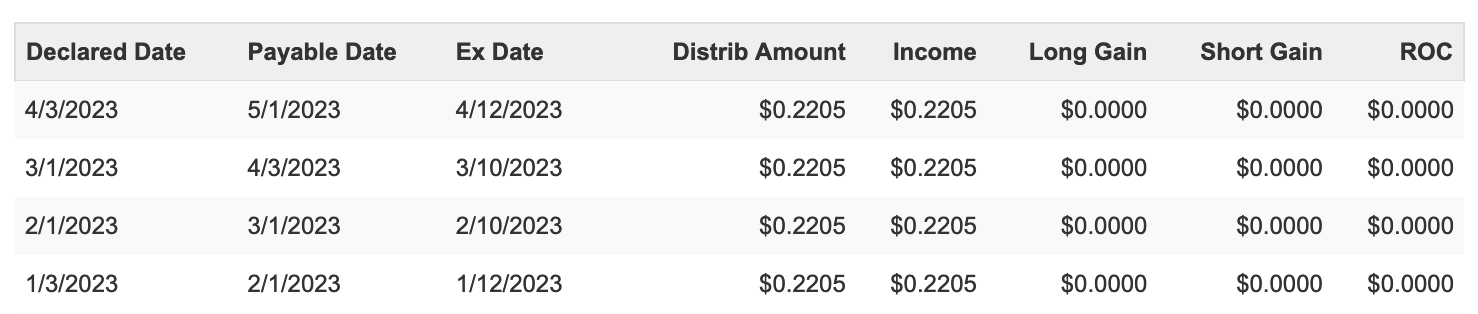

HTD

{kind=link}

A predominance of income supplemented by return of capital for the last three distributions, while January’s was almost entirely return of capital.

PCN

{kind=link}

All distributions were generated from income.

PDI

{kind=link}

All distributions were generated from income.

PDT

{kind=link}

All four distributions were based on varying percentages of income and return of capital.

PTY

{kind=link}

All distributions were generated from income.

RQI

{kind=link}

All distributions were generated from long-term capital gains.

RVT

{kind=link}

The only quarterly distribution with small percentage of income and the rest a combination of capital gains and return of capital (with predominance of the latter item).

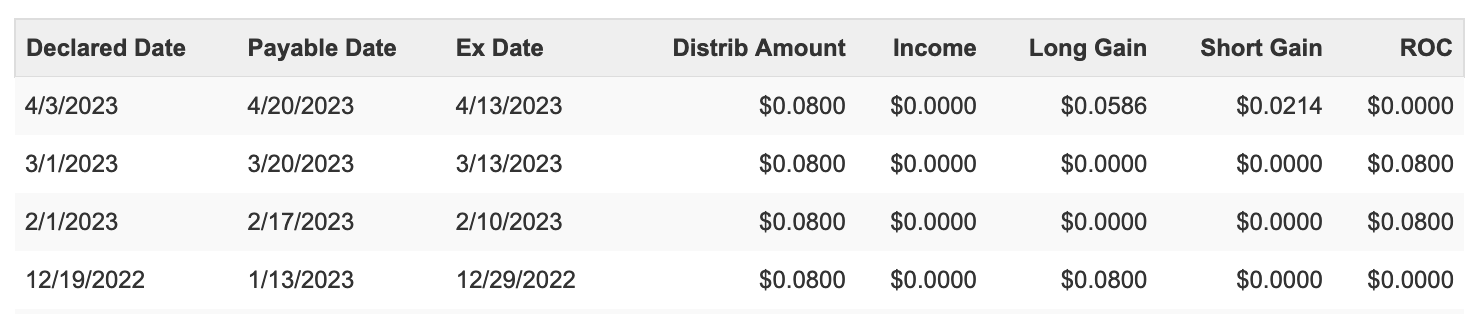

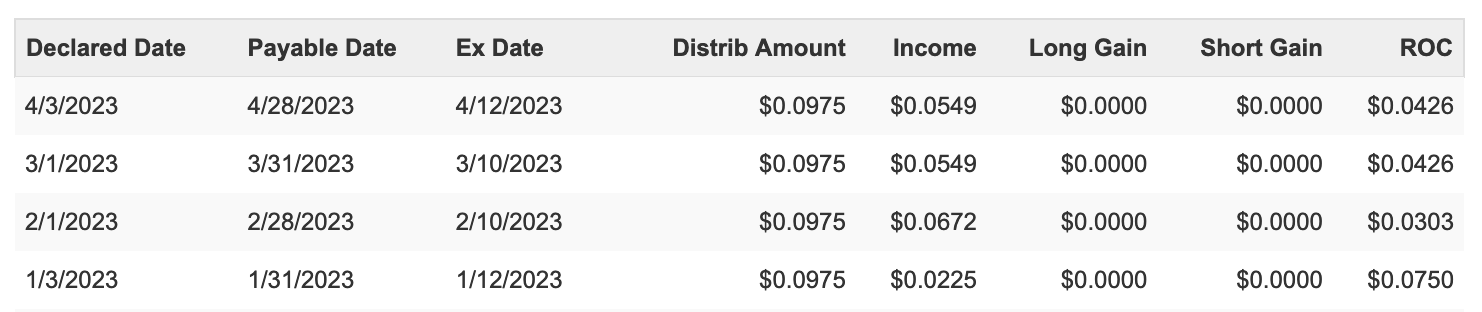

SPE

{kind=link}

All past and already stated next distributions are based on varying percentages of income and return of capital (with greater prevalence of the latter item).

UTF

{kind=link}

All past and already stated next distributions are based on varying percentages of long-term income and capital gains, with a very small reliance on return of capital.

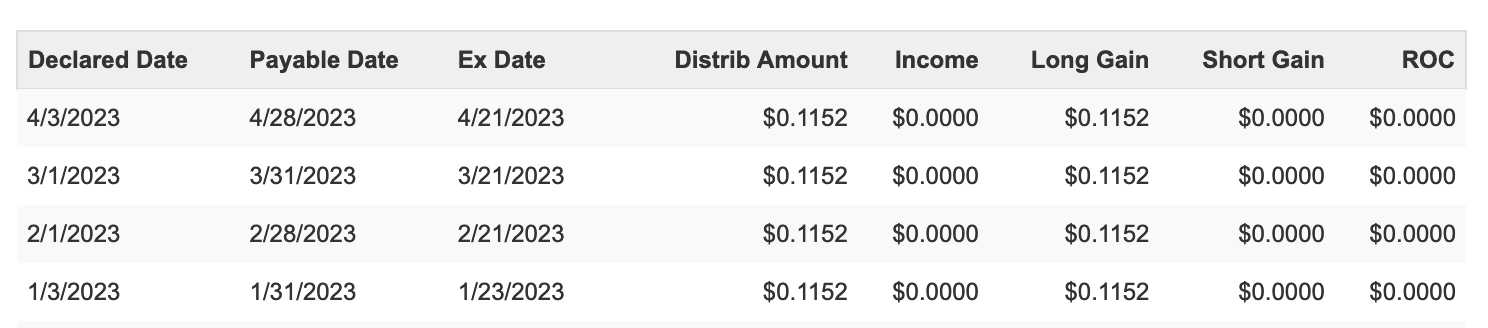

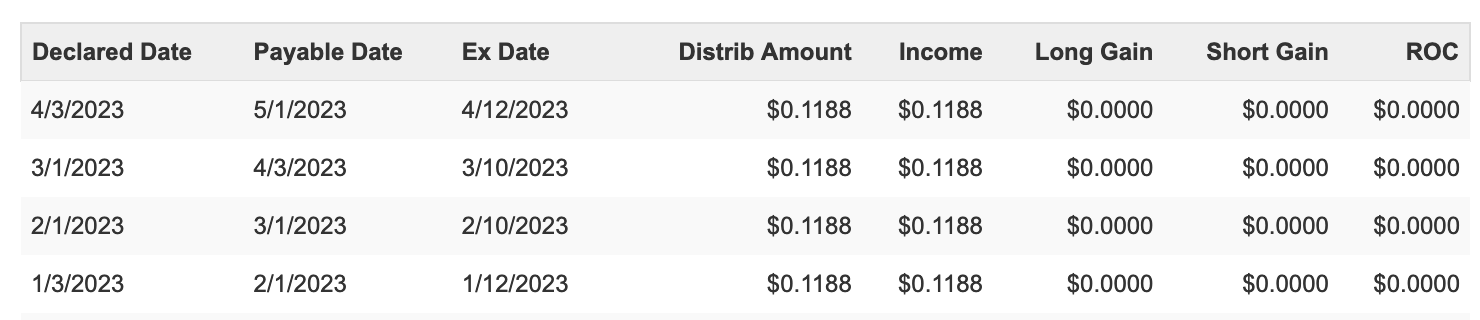

UTG

{kind=link}

All past and already stated next distributions are based on varying percentages of income and return of capital.

XFLT

{kind=link}

All distributions were generated from income.

Summing Up

As we have seen, in many cases the continuity of distributions has been ensured by a mixture of long-term and short-term capital gains combined with a form of payment classified as a return of capital, although I am not aware of what kind (whether destructive or constructive). It cannot be denied that the combination of these two elements, which mainly affects equity funds, may raise some concerns about the sustainability of their distributions in the coming months, should the economic situation deteriorate.

At present, out of 26 stocks in the portfolio, there are 9 that have resorted to return of capital (ignoring the insignificant percentage for UTF), even though their NAV performance remains largely in positive territory since launch. Obviously, the return of capital for these CEFs does not excite me, not least because they represent about one third of my assets. But the news is not such as to lose sleep over, since for now the remaining two-thirds of the portfolio seem likely to continue their march, despite the negative performance of many NAVs (a fact, however, not unusual these days).

What About USOI?

After another shake off, like Cesare, during April I decided to significantly reduce my position in USOI, taking advantage of its quotation around $83 and getting a gain in dollars but a loss in the euro equivalent, due to the negative change in the dollar/euro exchange rate. I am aware that ETNs are a minefield, but they are the only securities whose “coupons” –I want to remind here– generate so called “other incomes” ( redditi diversi ) , the only ones that can allow me to offset them, month after month, using prior losses.

On the other hand, USOI has been the only one among the many ETNs I have had over time that offered me a positive performance: that is why I have decided to keep aside the cash generated by its lightening, waiting for news regarding its future. In the meantime, I am considering possible alternatives, again among ETNs, to continue to benefit from the tax advantage offered to me by these securities, while being aware of the risks associated with this type of instruments.

The “Burst of the Chariot”

In Florence’s Cathedral Square, on Easter morning, the traditional auspicious ceremony called “Burst of the Chariot” ( Scoppio del Carro ) is renewed. A pole is erected in front of the cathedral’s high altar, connected by a steel cable to the Chariot (a wagon of fireworks called Brindellone because it is tall and wobbly), set up in the outdoor space between the cathedral and the baptistery.

On the steel cable is a rocket in the shape of a dove (the so-called “Columbine”): during mass, the archbishop lights the Columbine and it sets off, hissing quickly along the cable, travelling down the entire nave, through the cathedral’s central doorway and hitting the Chariot, lighting the spectacular fireworks on it, to the delight of the thousands of people attending the event each year.

If the race goes off without a hitch and the Columbine makes it all the way by lighting up the Chariot and coming back without stopping, tradition has it that the upcoming harvest season will be favorable and abundant. This year has made a perfect flight, so agricultural expectations are decidedly positive, while thick clouds seem to be gathering on the horizon in the financial markets. Cesare would shake it off and get by, living by the day as his wont.

I can’t but try to cling to Paul Samuelson’s line when he said that “the stock market has predicted nine of the past five recessions.” If finance were an exact science there would be no trading books because the market players would all be moving in the same direction, instead a recent WSJ report on the top stock-fund managers reveals that only 27 of 1,257 were able to rise at all in the past 12 months, or just over 2 percent (by the way, where are the Customers’ Yachts...?).

This is an “amateurish” percentage that speaks volumes about the randomness of markets and the forecasts of their performance on which we investors make our decisions, to the point that as many as 98 percent of the top stock-fund managers have failed to hit growth targets in the past year. To my knowledge, forecasting market performance based on the flight of the Columbine is perhaps risky, but I think it could be introduced as an alternative criterion. It may not be more reliable than that of many fund managers, but it is likely not necessarily less so either.

For further details see:

My Income Portfolio And Return Of Capital