QYLD - My Income Portfolio - Keep It Simple Sweetheart

2023-04-03 11:59:27 ET

Summary

- The world seeks complexity, but simplicity often trumps complexity.

- For my investment goals, I have made the choice to focus mainly on CEFs and ETFs, carefully weighing their merits and drawbacks.

- Those of us who invest in these income vehicles are smart enough to know what we are getting and what we are giving up.

- After many years, I am still convinced that the merits outweigh the drawbacks.

Caravaggio's Revolution

In the heart of Rome, a stone's throw from Piazza Navona, stands the church of Sant'Agostino, a place where in the early seventeenth century art history turned over a new leaf. Indeed, inside it is preserved a painting by Caravaggio, generally known as the Madonna of the Pilgrims , in which the painter depicted a man and a woman, elderly and poor, kneeling before the Virgin.

The figure of Mary, in the clothes of a commoner at the door of a ramshackle house, is striking, but the centerpiece of the narrative is the bare feet of the two pilgrims, in the foreground, with which Caravaggio simply wanted to tell us that Our Lady looks with special affection upon the humblest and poorest among her faithful, far from the ideal of "virtuous beauty" of seventeenth-century aesthetics.

Once again it is the genius next door , a scoundrel in his early thirties and full of problems with the law, who changes the course of history. On those dirty and dusty feet, indeed, would walk the history of art in the centuries to come. A simple and disruptive message, as that embodied many years later by Raskol'nikov and Sònja in Dostoevsky's Crime and Punishment , the murderer and the prostitute reunited in the Gospel reading.

Keep It Simple, Sweetheart

The world seeks complexity, but simplicity often trumps complexity, just as the simple figures of two kneeling old people painted by Caravaggio swept away a century and a half of Renaissance pageantry in one fell swoop. Similarly, many of us are convinced that financial markets are complex: in fact, almost all savers think that common-sense investing requires knowledge inaccessible to those who are not experts in the field.

A few months ago, I wrote an article dedicated to Irene , a neighbor of mine who would like to learn to take her first steps independently in the world of investing. I suggested that she follow a strategy based on three simple steps: identify quality securities, buy them at the lowest possible price and keep them for the long term. An almost trivial formula, yet each step presents increasingly difficult challenges, and on these difficulties the whole game is played.

Fifty articles ago I was taking my first steps here on Seeking Alpha, strong in certain convictions that have nevertheless faded over time as I compared my ideas with those of the people who commented on my articles. If ever there is an enriching moment in the knowledge process, it is the exchange of ideas with those who have different experiences and ways of seeing. This happened to me as well, and I am glad to have had that opportunity, which certainly made me a more knowledgeable investor.

It is because of this greater awareness that I would like to clarify a few simple points, which I consider fundamental in my approach to the world of investments, particularly CEFs and ETFs.

High Income Vehicles

Those of us who invest in high income vehicles are smart enough to know what we are getting and what we are giving up. We are not trying to beat the market, just wanting to live off our dividends and distributions" (From RetiredinIndy's comment on my last article).

Ten years ago, I first entered the American market, driven by the need to find a source of income complementary to that from my publishing job, which unfortunately did not provide me with the desired continuity.

I initially turned to the world of ETFs, and only later discovered the existence of CEFs, which immediately caught my attention. At the time they were freely purchasable for a European, but today they must have KID (Key Information Document) in order to purchase them, otherwise you can only buy them if you are classified as a professional investor. I am, but my qualification is reviewed every year according to some parameters that I will not dwell on.

So, in 2014 I built my first portfolio with a mixture of ETFs, a few CEFs and some individual stocks. For a few years my portfolio was an "open construction site," until, in 2018, I resolved to build one based entirely on a handful of CEFs that I considered quality at the time. Some survived even in subsequent portfolio revisions, while others were lost along the way.

But my goal was always to create a source of income for myself through high-dividend instruments, selected initially based on Morningstar ratings and a financial risk assessment tool supplied by Nasdaq, called RiskGrades (no longer in existence today). I believed in my strategy, which for over a year I strenuously defended, even on these pages, and then gradually abandoned in favor of other evaluation criteria based mainly on NAV performance .

For the past year it has not been easy to identify CEFs and ETFs with positive NAV performance, given the collapses in almost every sector of the market, and my portfolio also suffers right now from an overall loss of around 7%, which has occurred entirely in the past month, with the heavy developments on the banking front.

However, my idea is always to invest in CEFs. I have spent years studying and delving into their merits and drawbacks, focusing my attention exclusively on these investment instruments (later expanded to the world of covered call ETFs). As I have discovered from the many comments to my articles, there are many of us who share the same interest, aware of "what we are getting and what we are giving up" in using them.

Single Stocks

I have always approached individual stocks little (and poorly) because I do not have enough knowledge to successfully venture into their research and selection. Of course, I thank all the people who suggest individual stocks to complete (in their view) my portfolio by increasing its diversification. But I prefer to maintain and cultivate my narrow circle of competence based on CEFs and ETFs, although lately I have been timidly opening up to the world of BDCs. As far as I am concerned, however, I remain focused on CEFs and ETFs, the financial instruments I delude myself that I know best… or to whose whims I am more accustomed.

In this regard, I take this opportunity to express my amazement at cases like those of SVB or Credit Suisse, two banks that fell like a house of cards in a matter of days, leaving behind a pile of rubble. Each time I wonder how can this be possible, but evidently it is, and this reinforces my conviction to invest in funds or ETFs, leaving the selection of individual stocks, with all the risks involved, to others more astute than me.

Incidentally, according to reports in Italy's largest financial newspaper, not one economist they interviewed in early 2023 about possible market performance during the year even hinted at a banking crisis. Not a single one. This speaks volumes about the value of forecasts and suggests that the easiest thing to do is to invest in what you think you more or less know, with a long-term horizon. The rest is just idle talk, or presumptuous opinions not worth listening to.

Italian Income Tax Code

The Italian income tax code classifies financial incomes into two categories: "capital incomes" ( redditi di capitale ) and "other incomes" ( redditi diversi ):

- "Capital incomes" include interests, dividends, and other incomes derived from the mere possession of financial assets (for instance, CEFs and ETFs). These incomes are always taxed, that is, they cannot be offset by any past losses;

- "Other incomes" include capital gains and losses derived from the disposal of financial assets, as well as income from derivatives (like ETNs). These incomes are always taxed net of financial losses and expenses, that is, they can be offset by any past losses.

Taxation of CEFs and ETFs

American CEFs and ETFs are non-tax-harmonized instruments on whose dividends we Italians are subject to a withholding tax of 15% in America and 26% in Italy, for a total amount of 41%. In this case, however, the Italian-American treaty to avoid double taxation provides that the 15% withheld in America is returned to us by our government. On capital gains, on the other hand, we have only the Italian withholding tax of 26%, because they take place in Italy.

The accumulation of all sums (dividends plus capital gains) from non-tax-harmonized instruments has to be taken to the tax return: according to the income bracket reached, also adding income from work, the taxable amount is calculated using the rate due. If the tax is less than what has been withheld, we can ask for a refund of the excess amount, otherwise we have to pay the difference. Personally, I have always been reimbursed for taxes withheld in excess, which is why I consider investing in CEFs and ETFs to be very tax-efficient for me, because no tax benefit has ever been lost, since everything gets recalculated and offset in my tax return.

Taxation of Single Stocks

Unlike CEFs and ETFs, individual stocks (including BDCs) are instead tax-harmonized and their dividends are subject to a variable final tax in America and 26% on the remaining 85% (so called "net frontier") in Italy. In the case of BDCs, 15% is withheld in America and 26% (on 85%) is withheld in Italy, for an overall tax of 37.1% that does not have to be brought to the tax return, as dividends from CEFs and ETFs do. So, tax is withheld, and that's it.

In addition, some stocks are subject to American withholding taxes even higher than 15%, as for example in the case of AllianceBernstein (AB). For a foreigner, in fact, the US tax rate on AB is 37%: added to this is the 26% Italian tax on 63% (the "net frontier"), which brings the total levy on its dividend to 53.38%. On a Canadian stock such as Global Dividend Growth Split Corp. Class A (GDV:CA) [GDV.TO], which I sold last summer, the total withholding is 44.5%. Since it is not possible to offset these withholdings on our tax return, the convenience from a tax point of view is nil.

To sum up, as you can imagine, these tax considerations lead me to favor the purchase of CEFs and ETFs, although recently I have again included in my portfolio two very interesting BDCs ([[ARCC]] and [[CCAP]]), mainly for the reason I will discuss here below. As for ORCC, on the other hand, I have decided not to build any position, and indeed have liquidated the few stocks I owned, preferring to increase ARCC and CCAP a bit and limit my exposure to the world of BDCs to these two stocks only for now.

The So Called "Other Incomes"

According to Italian income tax code, gains derived from the disposal of tax-harmonized securities (like U.S. stocks) and derivatives (like [[USOI]]) generate so called "other incomes" ( redditi diversi ), the only ones that can allow us to be offset using prior losses. So if one day I sell ARCC or CCAP at a gain, I will pay 26% tax if I have no prior losses. Otherwise, I will offset with those losses. REITs behave the same way, as do ETNs, whose dividends are also considered "other income" in Italy and therefore can be offset using past losses. This is the reason why I put USOI back into my portfolio, so that I could offset its dividends with previous losses, month after month.

The recent tax reform promoted by the current Meloni government seems destined to revolutionize Italian taxation in this field by uniting all these sources under the heading of "financial income," with the possibility of offsetting all gains and losses, no longer distinguishing between "capital incomes" and "other incomes." This would certainly be a significant step toward simplification of the Italian tax system in this field, but this is a story yet to be written.

My Overall Portfolio's Yield

As you may know, my investments are divided into three different income portfolios: Cupolone, my primary CEF portfolio; Giotto, comprised of ETFs that adopt a covered-call strategy; and Masaccio, my "tactical" portfolio. This is the complete list of the 26 titles that make up my three portfolios:

Cupolone

- BlackRock Science and Technology Trust ( BST )

- Calamos Dynamic Convertible and Income ( CCD )

- Calamos Global Total Return ( CGO )

- Eaton Vance Enhanced Equity Income Fund II ( EOS )

- Eaton Vance Tax-Adv. Global Dividend Opps ( ETO )

- Eaton Vance Tax-Adv. Dividend Income ( EVT )

- Guggenheim Strategic Opps ( GOF )

- John Hancock Tax-Adv. Dividend Income ( HTD )

- PIMCO Corporate&Income Strategy ( PCN )

- PIMCO Dynamic Income ( PDI )

- John Hancock Premium Dividend ( PDT )

- PIMCO Corporate&Income Opportunity Fund ( PTY )

- Cohen&Steers Quality Income Realty ( RQI )

- Special Opportunities Fund ( SPE )

- Cohen&Steers Infrastructure ( UTF )

- Reaves Utility Income Trust ( UTG )

Giotto

- JPMorgan Equity Premium Income ( JEPI )

- JPMorgan Nasdaq Equity Premium Income ( JEPQ )

- Global X Nasdaq 100 Covered Call ( QYLD )

- Global X Russell 2000 Covered Call ( RYLD )

- Global X S&P 500 Covered Call ( XYLD )

Masaccio

- Ares Capital Corp ((ARCC))

- Crescent Capital ((CCAP))

- Royce Value Trust ( RVT )

- Credit Suisse X Links Crude Oil Shares Covered Call ETN ( USOI )

- XAI Octagon FR & Alt Income Term Trust ( XFLT )

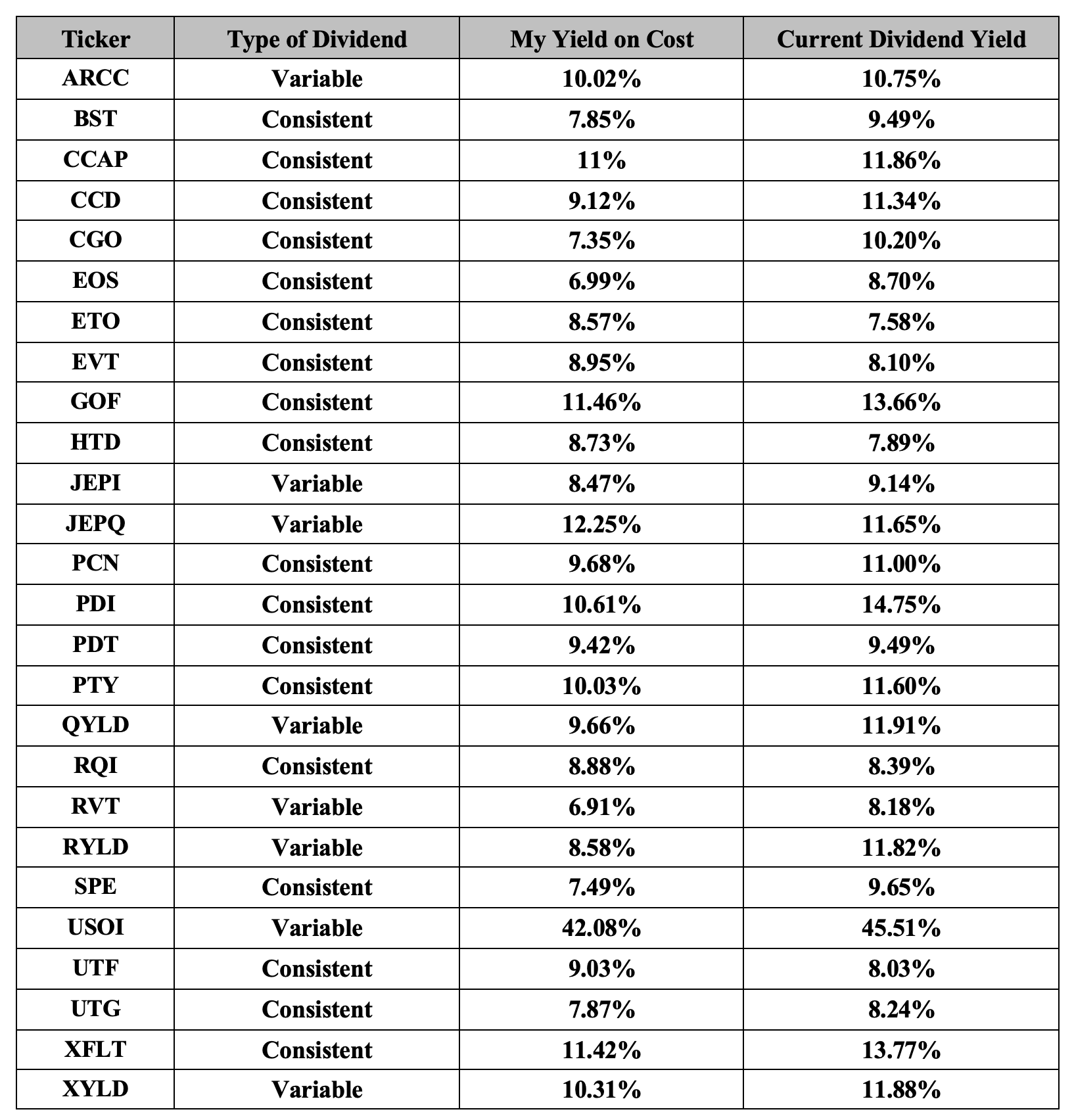

Here below are the yields on cost of all the titles in my portfolios, compared to the current dividend yield. The first column reports the type of dividend, which in some cases is constant over time while in others is variable, that is, it can change from month to month.

{kind=link}

Note: All my yields on cost refer to the last paid or announced distribution/dividend.

As can be easily verified by comparing my yields on cost to the current dividend yields, I could have done more and certainly better. Some CEFs, bought in 2020 (during the covid crisis) at lower prices than today, show higher yields than they offer today, but my overall portfolio yields much less than it would if it were built today, although I continue to be very satisfied with the result.

Indeed, the total yield (including dividends paid and announced) reaches 9.90% this month, thanks in part to the robust contribution of USOI, without which it would instead be around 9%. No one is able to buy at the lows, and even I have to make do, so to speak: I have been buying as the market fell, averaging down my load prices, and since "any crisis always lasts longer than your savings," my liquidity today is about to run out while the light at the end of the tunnel is still far away.

This does not frighten me, as I consider myself a dividend investor looking at the long term. And the constant flow of money in the form of distributions/dividends helps to lighten the darkness, even if in some cases we are talking about double-digit returns at current market prices, the sustainability of which over time raises more than a few reasonable doubts.

Bedtime Thought

A 13th century English scholastic philosopher and theologian, the Franciscan friar William of Ockham, put forward the idea that simpler solutions are more likely to be correct than complex ones. This problem-solving principle, known today as "Ockham's Razor," basically states that instead of searching for supplementary hypotheses to solve a problem, one should select the solution with the least complexity.

As far as I am concerned, the simplest investment solutions to meet my needs are CEFs and ETFs. Indeed, in both of these types of instruments, I identified many years ago a stable source of income that I can increase by reinvesting dividends and that helps me to face the market downturns more calmly while keeping the bar straight on my long-term goals.

Those who adopt a dividend-based financial strategy by investing in high income vehicles know that they have to hold on. The alternative for us is not the 3.5% offered by ETFs such as SCHD, although with a largely positive NAV performance since inception. Those of us who adopt a dividend strategy want more income month after month, willing to pay a price for our choices, and knowing that at times like the present, when negative sentiment prevails in the markets, the biggest mistake we can make is to panic like there is no tomorrow.

The price to pay? A robust belly ache from volatility.

For further details see:

My Income Portfolio - Keep It Simple, Sweetheart