BBSEY - My Top 3 Insurance Stocks For A Financial Rebound

Summary

- Inflation hit a YoY high in June, as CPI prices surged to 9.1%. Companies like insurance carriers are increasing premiums, following suit after the largest annual increase in over 40 years.

- Insurance is highly profitable and often low-volatility, given its diversified income streams that can produce long-term returns while serving as a potential hedge against inflation.

- Although equities generally perform poorly in rising rate environments, insurance tends to generate revenue streams through underwriting fees and investments in both up and down markets.

- Everyone needs insurance, and insurance is part of the financial sector, which we believe stands to benefit from a financial rebound. Seeking Alpha’s Grading System shows you why the three stock picks are strong buys. All possess excellent Factor Grades and strong fundamentals, are very profitable and have outperformed the S&P 500 this year.

Why Invest in Financial Stocks?

The market selloff means there will eventually be a rebound, and with earnings season underway, we’re seeing some recovery, and I believe that financials will be among the sectors. Financials tend to benefit when interest rates increase. For instance, banks make more on net interest income as they can charge higher loan rates to borrowers. They can also make money on deposits because, typically, those yields that banks pay clients and consumers for holding cash tend to significantly lag yields on loans and the bond market. Therefore, they're able to make a much larger profit. However, one negating impact this year is sharply rising yields that have caused consumers and businesses to stop demanding or limiting their need for credit. So while financials should be making more interest income due to the increased cost of capital, demand has fallen given the surging rates, which has hindered the bank’s ability to create a profit by increasing the number of loans that they issue and credit they originate. However, where banks and other financials may not reap as many benefits, insurance is one industry that stands to benefit in a rallying or bear market.

Insurance Rates Surging Like Inflation

Traditionally, insurance companies tend to benefit when interest rates rise, investing primarily in more conservative debt investments and bonds. As their interest rates rise, they can produce a greater level of income. However, as interest rates this year have risen so sharply, the offsetting return due to the lost principal value of those bonds has made it a difficult environment. So while insurance companies tend to benefit during rising interest rate environments, the pace and magnitude at which yields have gone parabolic and sharply increased have likely created an offsetting effect. But they can still offer excellent returns and have diversified offerings.

Insurance is a recession-resistant industry with great return potential

Insurance is a recession-resilient financial because regardless of the environment, individuals and businesses must maintain auto and homeowners insurance coverage, life insurance, etc., which secures long-term returns for insurers with minimal downside.

In the current environment, insurance companies will likely benefit as rates and replacement costs of goods, materials, and labor increase. I’ve written about it before, but as replacement costs rise, if the insured forgets to update their policies, insurance companies will not cover the total value of a claim but rather benefit from old policies that did not include upgrades or appreciated values.

Insurance premiums paid are also unique to financials because these premiums can be invested. When receiving large sums of money that are accumulated in an up market, these invested premiums can generate a significant cash flow and be great for a company in covering any potential claims, expenses, etc. But there is also an opportunity cost. In a down market, as we’ve seen, investment portfolios can also take a hit. Given most insurance companies tend to invest in more conservative investments, as I outlined above, portfolios generally use longer duration bonds to match the portfolio's duration with future expected cash flows from claim payouts, it’s crucial to consider this potential risk. Because insurance companies typically produce high levels of profits each year from varied income on policies they underwrite, consider three top insurance stocks rated quant strong buys.

Investing in Insurance Companies

My three stock picks are Top Financial Stocks with a market capitalization above $1B and in the insurance industry. Despite a sharp sell-off for many stocks this year, insurance companies offer an inflation hedge, as we’re seeing them increase premiums as costs abound. The insurance industry has tailwinds that allow companies to navigate the uncertain environment while growing their portfolios through diversification and making money by charging insureds premiums for coverage, whether they use or never use their service. Whether premiums are used or not, an added bonus is they can invest premiums to generate more profits for their bottom line. This unique business model is why I have selected three top-ranked insurance stocks for your portfolio.

1. Unum Group ( UNM )

-

Market Capitalization: $8.72B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 10/24): 6 out of 660

-

Quant Industry Ranking (as of 10/24): 1 out of 22

Life and health insurance company Unum Group, together with its subsidiaries, helps investors protect their finances and financial future, offering disability and life insurance policies, supplemental and voluntary products including dental and vision, and group pensions. Operating in the U.S., UK, and Poland, Unum sells its benefits products primarily to employers for the benefit of employees.

{kind=link}

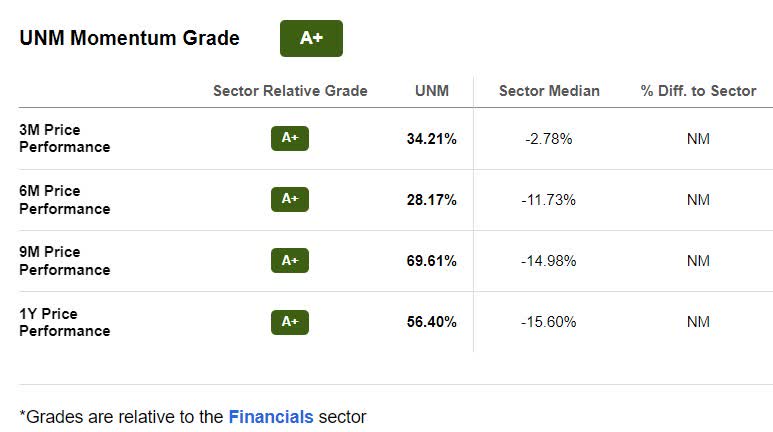

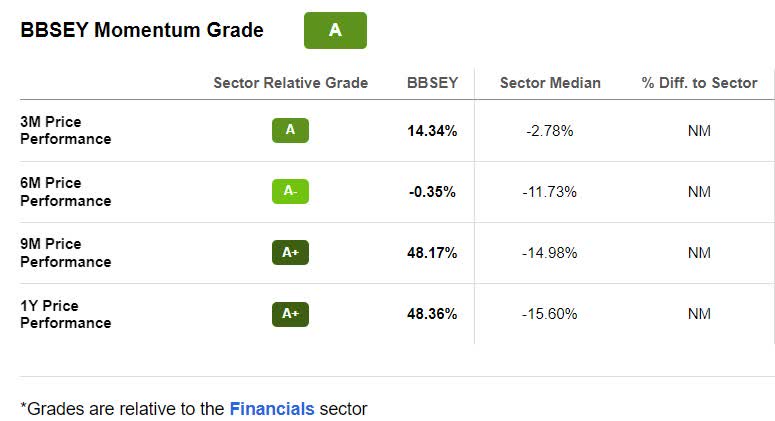

Strongly bullish, UNM has been on an uptrend since the pandemic and continues to showcase stellar momentum while trading at a discount.

Unum Valuation & Momentum

Unum Group is the quintessential value investment, trading at an attractive discount to its sector peers and offering an overall valuation grade of B-. Looking at the underlying metrics, Unum’s forward P/E ratio of 7.44x is a -28.76%, and a forward PEG of 0.49x is a -55.93% difference to the sector.

{kind=link}

Year-to-date, UNM has experienced a nearly 75% price increase. Over the last year, it's +60%. As evidenced in the A+ momentum grades above, UNM outperforms its sector peers quarterly and has continued its bullish momentum since 2020, with many analysts calling the stock overbought, as investors are actively purchasing shares, driving its price higher. With its impressive earnings and ‘above-market, secure, – not stretched’ dividend yield, Unum stock lifted its full-year operating income guidance after Q2 earnings beat Wall Street consensus expectations.

Unum Growth & Profitability

As many companies see inflation eating away at profits which subsequently puts dividends at risk of being cut, insurance companies tend to have more stable earnings. Recurring premiums and investing them in up and down markets until a benefit has to be paid allows them to generate additional income, helping to weather potential dividend cuts. As a result of strong financials and liquidity that remains above Unum’s targeted levels of $1.2B and leverage below 25%, this capital strength has allowed a return of capital to shareholders through dividends and share repurchases. In addition to a forward dividend yield of 3.03%, UNM’s dividend scorecard below looks very attractive, offering a solid dividend safety grade and 22 years of consecutive dividend payments.

{kind=link}

Despite the current bear market, the favorable economics of insurance is also why the industry is considered recession-resilient and why Warren Buffett’s Berkshire Hathaway holds a substantial stake in insurance. Insurance sales volumes tend to increase during economic growth and inflation. Although we’re in a period of contraction, insurance is unlikely to become obsolete because it's a service everyone needs. Where higher claims were paid during the height of the pandemic, as vaccine distribution and COVID concerns are becoming less frequent, insurance companies like Unum are experiencing positive earnings.

“The decline in mortality also produced a more normal result for long-term care block as benefits experience more closely aligned with pre-pandemic levels of experience, especially for claimant mortality. Second, we saw an exceptionally favorable performance in our Unum US group disability line with a strong acceleration in premium growth and historically low benefit ratio,” said Steve Zabel, Unum CFO .

Second-quarter earnings beat top-and bottom-line results with an EPS of $1.91, beating by $0.69, and revenue of $3.05B, beating by $49.17M. Strong financial performance was due to improvements in the U.S. disability line that saw one of its lowest benefits ratios on record at 66.4%. Unum’s Colonial Life unit also recorded its lowest benefits ratio of 47.6% for the quarter.

{kind=link}

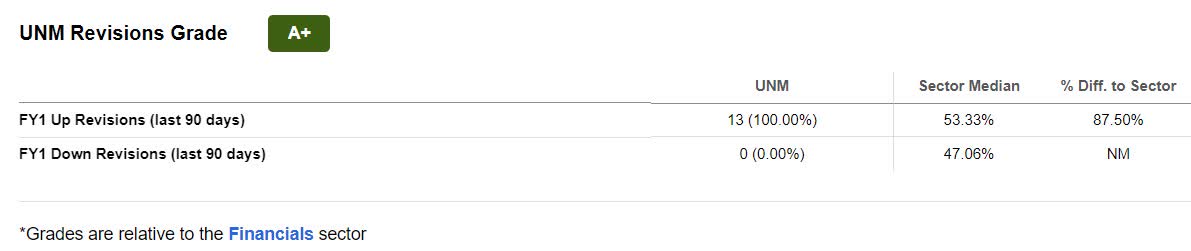

Like many businesses that have had to pass costs onto consumers, the tailwinds of increasing interest rates and costs have resulted in year-over-year growth in premium income of 3.5% for Unum’s core business units. With tremendous momentum and a favorable outlook, it’s no surprise that 13 analysts have given upward revisions in the last 90 days. As Rick McKenney, Unum Group President & CEO said during the same Q2 Earnings Call:

“I'm very pleased with our performance in the second quarter and the flexibility it creates for us as we move forward. risks from the pandemic are still very real, and there is growing concern over the direction of economic growth. However, I believe it's a testament to the strength of our business that we are in such a favorable position today from an earnings and capital perspective after navigating through the pandemic over the last two years.”

Unum Group’s fundamentals and its Strong Buy quant rating indicate it could be a good consideration for a portfolio in addition to the next stock pick.

2. Reinsurance Group of America, Inc. ( RGA )

-

Market Capitalization: $9.34B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 10/24): 7 out of 660

-

Quant Industry Ranking (as of 10/24): 1 out of 6

Reinsurance Group of America is one of the biggest global life and health insurance companies, offering life and health reinsurance, living benefits reinsurance, group reinsurance, financial solutions, and more. With approximately $3.5T of life reinsurance in force and $92.2B AUM as of December 31, 2021, as rated by Seeking Alpha’s quant ratings, RGA is a Strong Buy to watch.

Insurance companies themselves want to protect and insulate themselves against major claims, which is the benefit of reinsurance. RGA offers a way to minimize insurance companies’ other insurance liabilities to be paid. Especially in an inflationary environment recovering from the pandemic, RGA can capitalize on increasing net premiums from other life insurance providers that took a hit during the height of COVID. Major claims, unforeseen circumstances, and deaths from COVID and non-COVID cases have prompted insurers to try and guard against future losses. RGA stands to gain, which is why I’ve selected it as my next stock pick.

RGA Valuation & Momentum

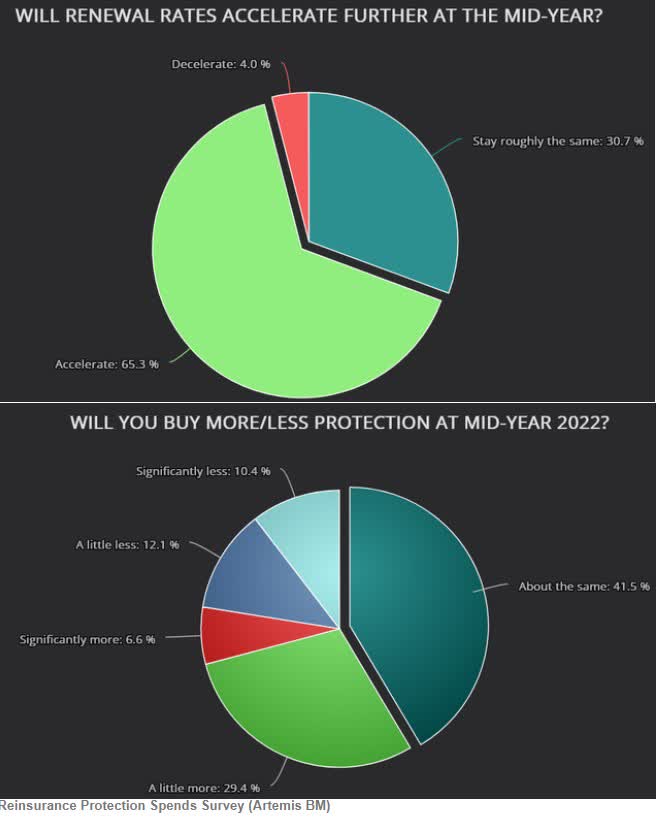

Despite RGA being considered relatively overvalued, it may be worth paying a small premium, given its strong operating momentum and projected growth. Interest rate hikes could boost RGA’s income from its financial solutions division while also capturing a large share of business from other insurance carriers wanting to minimize the brunt of losses. According to an Artemis survey , most respondents indicate they would buy more protection in 2022 and that renewal rates are likely to accelerate.

{kind=link}

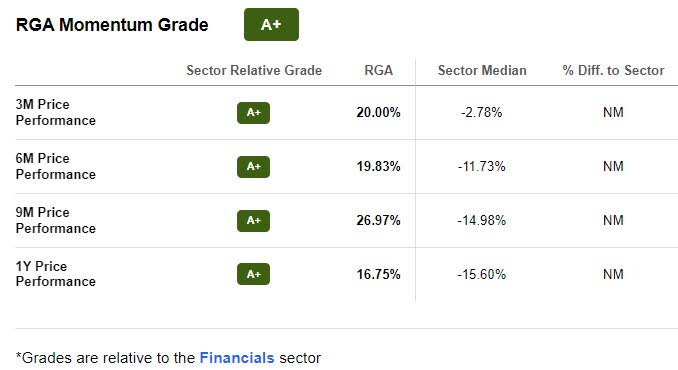

As we look at the company as a whole and its A+ momentum grade, the stock is already on a bullish trend. The level at which the stock is reading has many analysts calling it overbought, driving its share price higher.

{kind=link}

Year-to-date, the stock is +26%, and over the last year, it’s +16.75%. Its quarterly price performance shows that RGA significantly outperforms its sector median peers. With the stock primed for growth and its latest earnings beating expectations, let’s dive into more numbers.

RGA Growth & Profitability

Favorable tailwinds benefit RGA, as evidenced by its record level of earnings per share. Although revenue of $3.89B missed by $148.68M, second quarter results showcased an EPS of $5.78 that beat by $3.02, resulting in it raising its dividend by nearly 10%.

"COVID-19 claim costs came down substantially this quarter, and our underlying non-COVID-19 mortality was favorable in many markets," said Anna Manning, RGA CEO .

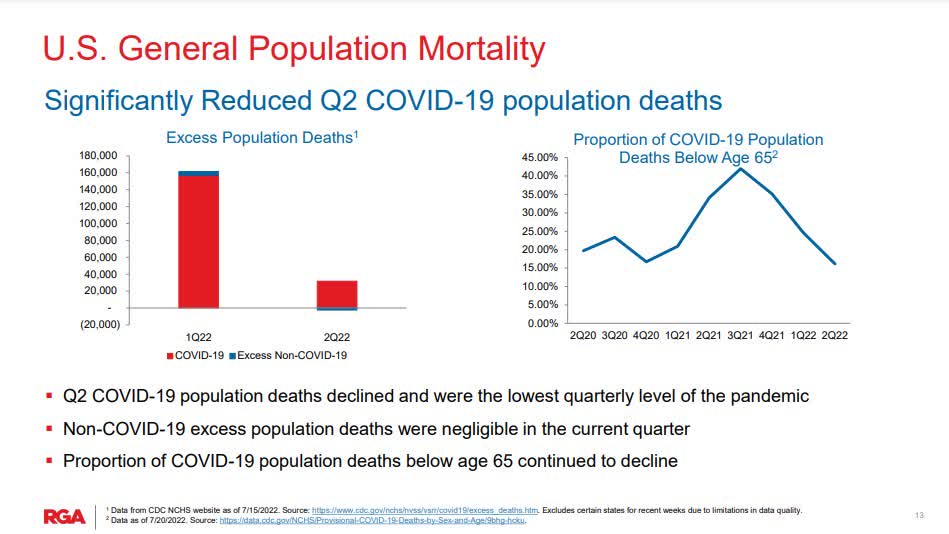

With vaccine distribution and higher population immunity, YTD COVID-19 claims have declined, reducing RGA’s claim costs.

U.S. General Population Mortality Stats (RGA 22Q2 Investor Presentation)

{kind=link}

RGA’s premium growth increased by 4.3% since Q1, and it continues to diversify its holdings and investment strategy to balance and manage risk and return cycles. Strong balance sheets and cash flow have allowed RGA to continue to return excess capital to shareholders through dividends and share repurchases. Although the company has a modest 2.26% forward dividend yield, its dividend safety is an A+, and RGA has paid its shareholders a consistent dividend for 12 years.

{kind=link}

With new product and strategic initiatives in the pipeline, favorable underwriting, and interest rate hikes to boost investment income, RGA’s global business offers potential upside and an attractive outlook. Consider this quant-rated strong buy stock for a portfolio, along with my next pick.

3. BB Seguridade Participações S.A. ( BBSEY )

-

Market Capitalization: $10.98B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 10/24): 5 out of 660

-

Quant Industry Ranking (as of 10/24): 1 out of 9

Headquartered in Brazil, BB Seguridade Participações S.A. ( BBSEY ) operates in two segments, Insurance, and Brokerage. A multi-line insurance carrier and a subsidiary of Brazil’s largest bank, Banco do Brasil S.A. ( BDORY ), BBSEY offers a basket of options that includes investing in pensions, bonds, reinsurance, and dental insurance.

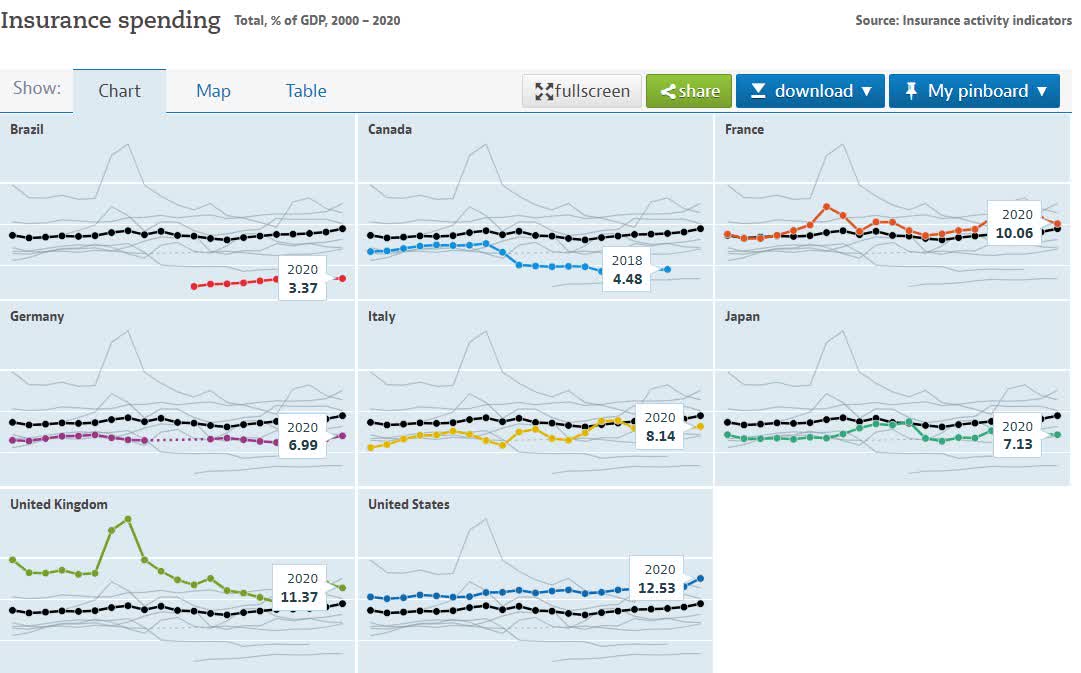

As a leading insurance company in Brazil, BBSEY is one to watch. From a global perspective, Brazil is an under-penetrated insurance market as showcased below in the OECD charts for various nations’ insurance spending by the total percentage of GDP. Not only does this indicate there is a solid opportunity for growth in Brazil’s emerging marketplace, but as Ravi Parikh wrote :

“The opening of Brazilian insurance market in the 1990s, allowing foreign capital and players, has helped in improving the financial literacy amongst the urban population and helps them educate regarding the needs for life insurance products.”

{kind=link}

BBSEY Stock Valuation & Momentum

From a valuation standpoint, BBSEY comes at a discount. Possessing an overall B+ valuation grade that includes a forward PEG of 0.49x compared to the sector median of 1.10, a -55.39% difference to the sector, and a forward EV/EBIT of 8.66x, a -24.46% difference to the sector, BBSEY is undervalued. In addition, the stock has bullish momentum.

{kind=link}

Despite BBSEY ending down more than 5% Monday following news of Brazil’s central bank upgrading economic forecast from 2.71% to 2.76% and market analysts lowering inflation forecasts from 5.62% to 5.6%, the stock has been on a longer-term uptrend, rising above the 200-day moving average and significantly outperforming the S&P 500. Quarterly, BBSEY has outperformed its sector peers and continues to improve gradually. With insurance premiums on the rise and lower loss ratios as highlighted in Q2 earnings, BBSEY’s Strong Buy quant rating highlights the stock’s growth and profitability.

BBSEY Growth & Profitability

On a year-over-year basis, BBSEY experienced a premium growth of 23%, with a big contribution coming from rural insurance, which grew by 42% YoY. Home insurance increased 27% from the previous quarter, and pensions experienced a 346% YoY increase in net income.

BBSEY Profitability Grade (Seeking Alpha Premium)

EPS of $0.13 beat by $0.02, and revenue of $335.71M beat by more than 61%, for a total of $42.88M. As BBSEY Chief Executive Officer Ullisses Assis stated during the Q2 Earnings Call:

“We have had a strong collection of pension plans. So, in the second quarter, we had almost BRL12 billion (USD 2.26B) in contributions and a very strong growth in premium bonds. We are again leaders in terms of collection, 27% higher than the same quarter last year. All of this will enable us to pay out BRL2.1 billion (~ USD 400M), which is a payout ratio of 80%, as we had announced before.”

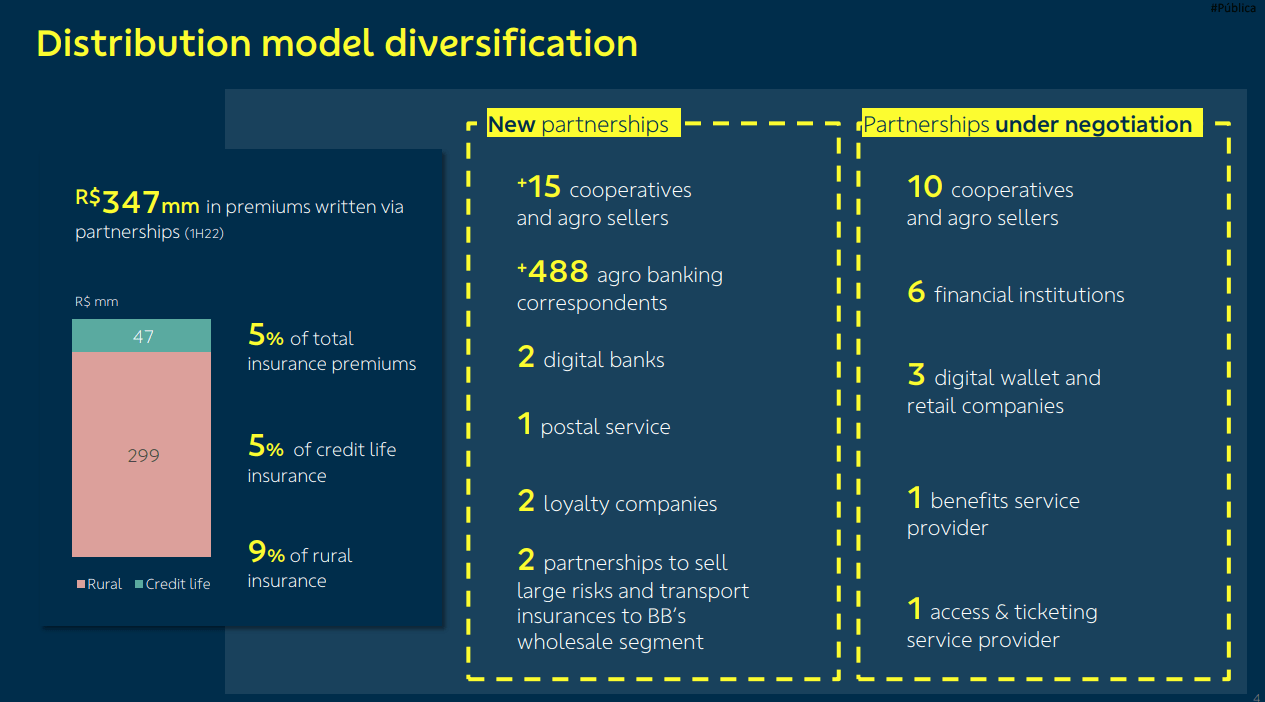

With a 6.91% forward dividend yield and solid financial performance, the company has paid four years of consecutive dividends. Although its dividend scorecard is not very attractive, BBSEY is capitalizing on rising prices to increase its net income growth through premium collection. Despite market volatility and the major indexes down, BBSEY has taken steps to continue diversifying its portfolio, adding new partnerships while ranking in the dough with current customers and increasing premiums.

BBSEY Premium Diversification Model (BBSEY 2Q22 Earnings Presentation)

{kind=link}

To reiterate, insurance stocks can be a profitable business model and inflationary hedge and, therefore, unlikely to become obsolete. People and businesses need insurance ; therefore, investing in the right companies that offer value and growth in an industry of this caliber can prove beneficial. Consider the three stocks mentioned above because a financial rebound could be on the horizon.

A financial rebound may be on its way, and insurance stocks may benefit.

The markets are volatile, and many investors hope for a financial rebound as portfolios have experienced substantial losses. Focusing on investments that can perform well when markets fall or rise is important, especially in the current environment, which makes the insurance industry attractive.

Insurance companies generate revenue by collecting premium income, investing premiums that are not paid out as claims, and in several ways that include non-insurance operations. UNM, RGA, and BBSEY are rated Strong Buys by Seeking Alpha’s quant ratings, offering excellent fundamentals as measured by our Factor Grades that score each stock’s characteristics from A to F on a sector-relative basis. Not only are UNM and BBSEY trading at a discount, but investors also get increased exposure to financials in the insurance industry as a potential inflationary hedge. RGA’s valuation is a bit more expensive than the sector, but all three stock picks have solid growth and profitability to help shield from declines in income caused by the Fed tightening. Check out the Grades on your stocks by Creating A Screen . Our investment research tools help to ensure you are furnished with the best resources to make informed investment decisions.

For further details see:

My Top 3 Insurance Stocks For A Financial Rebound