EPRT - My Top 5 REIT Holdings Revealed

2024-01-04 07:00:00 ET

Summary

- 2023 did not play out as expected, with predictions of a recession being proven wrong.

- Analysts' predictions for the performance of value stocks, including REITs, were also inaccurate.

- Despite the unpredictability of the market, certain REITs, such as Realty Income, Digital Realty Trust, American Tower, VICI Properties, and Agree Realty, are still recommended as good long-term investments.

If I said it once, I said it a dozen times in December alone…

2023 did not play out as expected.

Right about this time last year, I published an article titled, “ My Top REIT Picks for 2023 .” There, I quoted a Nasdaq article that happened to be one of the more optimistic pieces at the time:

“In our view, 2023 will be a year of important ‘transitions.’ We believe the first transition will be away from a bear market to a potential bull.

“History suggests attractive forward returns for stocks after the type of drawdowns we witnessed in 2022, but the timing of the market boom is unclear and the process will be bumpy, in our view. Longer-term, returns for balanced stock and bond portfolios look attractive to us again, with valuations more reasonable and bond yields above long-term inflation expectations.

But even then, as I noted, that assessment did “come with some caveats”:

“We believe the next two major transitions involve an evolution of investors’ concerns: away from inflation and towards recession, as well as away from pandemic-related disruptions towards geopolitical ones.”

Most everyone else, meanwhile – myself included, I must admit – were just calling for a recession.

It was the only logical conclusion to come to considering the inflationary conditions consumers were experiencing.

Looking back, I obviously have to acknowledge my error in how the economy played out. But as for there being any other “logical conclusion to come to”?

That one, I stand by.

The Year of the Recession That Didn’t Happen

Here’s another thing I keep saying…

2023 just goes to show you how nobody has a crystal ball. Which, incidentally, another part of “My Top REIT Picks for 2023” illustrates:

“Some say we’re in for a recession in the first half of the year. Some say we’re in for a recession in the second half. Some say we’re already in a recession and that won’t change for a while. And some say we’ll avoid a recession altogether.”

But, “Nobody’s throwing parties of anticipation about picking up profits left and right like gold nuggets on the ground.”

Clearly, the no-recession crowd won out. Even then, though, I can’t say I remember a single one of those opinions that got it even close to completely right.

I’m not saying that to insult anyone. Remember I already admitted – and will continue to admit – that I was far from perfect in my predictions.

There were too many national and global factors involved, from apparent consumer mindsets to political priorities to international conflicts. There always are to some degree or another.

That degree is minimal or at least manageable in some years. Maybe even most, allowing analysts like me to call the shots fairly well.

We (hopefully) look at the current data from multiple angles… (hopefully) try to set our own egos aside… (hopefully) consider historical trends and outliers…

And come to our conclusions for everyone to comment on and criticize at will.

Our track records usually result from our levels of experience, education, and willingness to continue being educated.

But, again, those track records are never perfect. And sometimes our calls are very far off.

The Year of the Value Stock That Didn’t Happen

Take the Nasdaq piece I previously quoted. While it perfectly pegged those “geopolitical” disruptions, clearly a recession never happened.

Moreover, it predicted:

“… the end of ‘growth’ stock dominance and an increased focus on consistent cash flow, dividend, and coupon generators – what RiverFront calls the ‘P.A.T.T.Y.’ (Pay Attention to the Yield) theme. Under these circumstances, we see modest upside for stocks and bonds in our base case scenario, with preferences for consistent cash flow generators, cyclicals, smaller-cap companies, and traditional ‘value’ plays like energy and financials.”

So when I commented in turn how, “Since REITs are ‘traditional value plays’ as well, that analysis ultimately bodes well for the sector”…

It made for two wrong analyses instead of one.

Speaking of wrong, I also had to write how:

“2022 was a tough year for real estate investment trust ("REIT") investors. A very tough year, in fact. This is the first time in over a decade that my top picks lost money.

“I’m always happy to show you the proof of my stock-market wins. But I have to be just as honest about the losses.”

As I already stated, solid analysts tend to have strong track records. Just not perfect ones.

That’s why analysts and readers alike need to hope for the best but plan for the worst. Which brings me to one final point before I address how 2023 went.

It’s another quote from yesteryear’s article, and it immediately followed my agreement with Nasdaq’s assessment:

“But even if that isn’t the case [that value stocks are the biggest winners of 2023], I believe the companies below are worth buying and holding onto for the long-term.

Realty Income Corporation ( O )

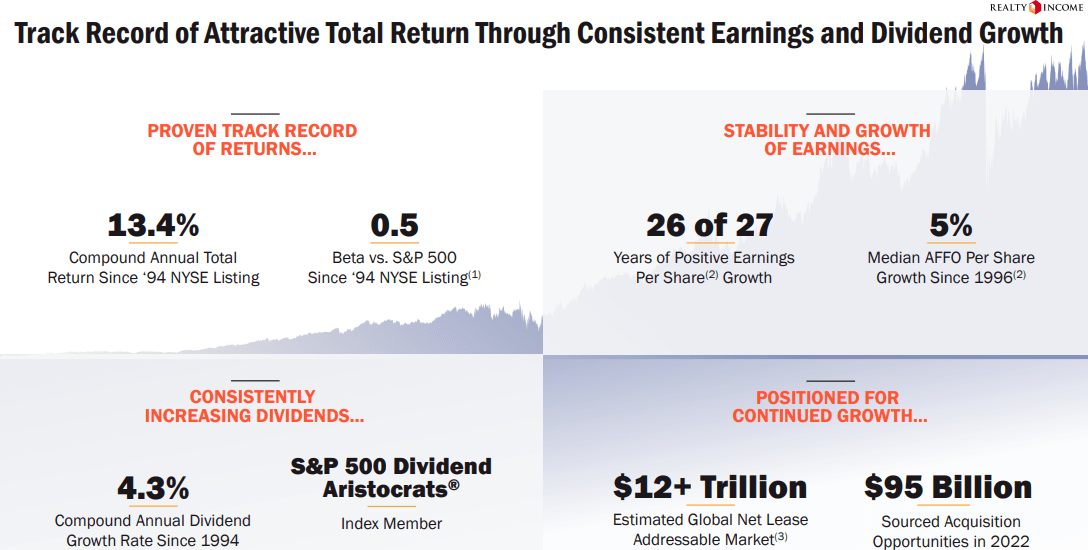

As many of my followers know, Realty Income is my largest holding as I view this as the ultimate “Sleep Well At Night” stock, or “SWAN” for short. The triple-net real estate investment trust (“REIT”) has been operating since 1969 and has been publicly traded since 1994.

Over its history as a publicly traded company, Realty Income has achieved positive growth in its adjusted funds from operations (“AFFO”) on a per share basis for 26 out of the last 27 years and has delivered a 5% median AFFO per share growth since 1996.

On top of that, the S&P 500 company is a Dividend Aristocrat, having increased its dividend for 29 consecutive years and delivering a 4.3% compound annual dividend growth rate since 1994.

{kind=link}

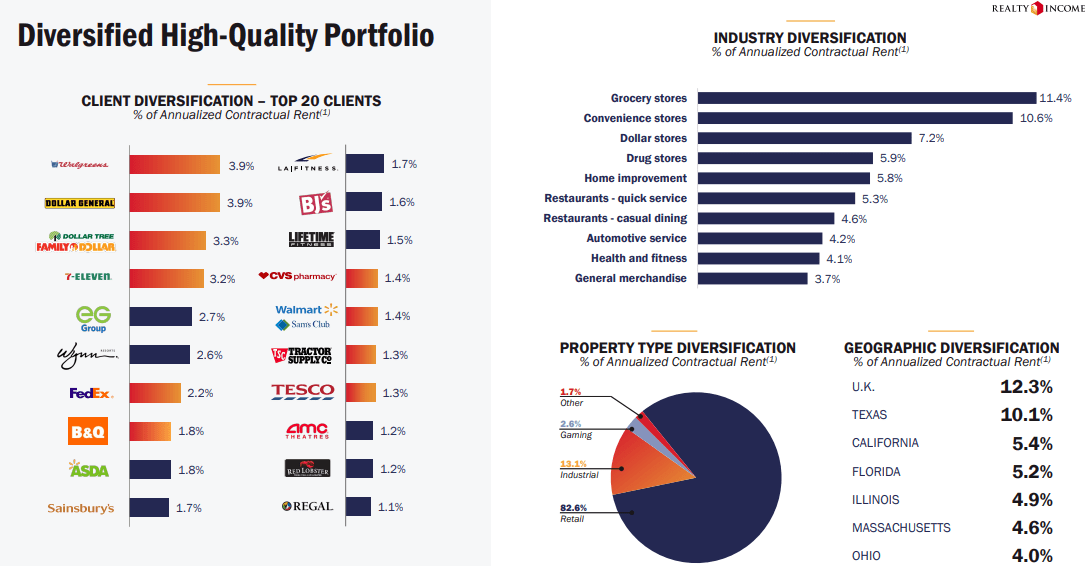

Realty Income specializes in the acquisition, ownership, and management of net leased commercial properties with a 262.6 million SF portfolio comprised of 13,282 commercial properties located across all 50 states, the U.K., Spain, Italy, and Ireland.

Their properties are leased to approximately 1,324 tenants operating in 85 separate industries including defensive retail sectors such as grocery and convenience stores, home improvement, drug stores, dollar stores and quick service restaurants.

O’s top tenants include well established businesses including Walgreens, Dollar Tree, 7-Eleven, FedEx, and Wynn Resorts and their portfolio is composed of retail, industrial, and gaming properties.

Commercial retail properties represent approximately 82.6% of their portfolio, while industrial and gaming properties make up approximately 13.1% and 2.6%, respectively.

{kind=link}

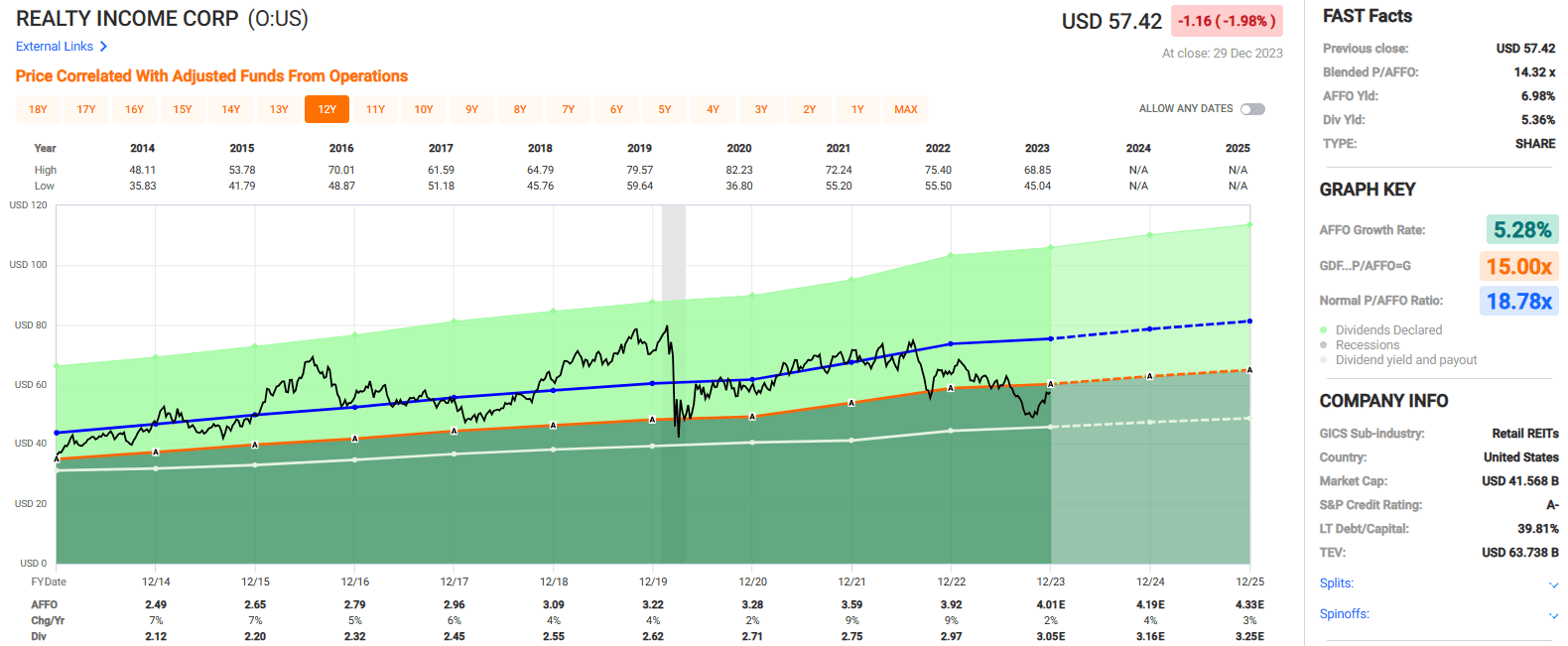

Realty Income stock price fell -10.00% in 2023. Keep in mind that the chart below shows the stock’s price return and does not factor in dividends or include total return figures.

At its low point in 2023 (10/30/23), the stock was down as much as 27.55% but rebounded significantly, gaining 24.23% from the beginning of November until year-end 2023.

Many of the factors driving REIT prices over the last several years have been macroeconomic in nature (interest rates / inflation) and not necessarily company-specific.

While highly leveraged REITs have generally suffered more than REITs with low leverage, the entire REIT sector seems to have been more influenced by the 10-Year Treasury (US10Y) than the fundamental performance of any particular REIT.

While this can be discouraging for shareholders who have seen O’s earnings rise, but stock price fall, it can also create opportunities for investors that are able to ignore the noise and to buy a piece of the company while it is trading at a discount to what its fundamentals would dictate.

{kind=link}

Realty Income has delivered an average AFFO growth rate of 5.28% and an average dividend of growth rate of 3.92% over the last 10 years. The stock pays a 5.36% dividend yield that is well covered with a 2023 AFFO payout ratio of 76.08% and trades at a P/AFFO of 14.32x, compared to its 10-year average AFFO multiple of 18.78x.

We rate Realty Income a Buy.

{kind=link}

Digital Realty Trust, Inc. ( DLR )

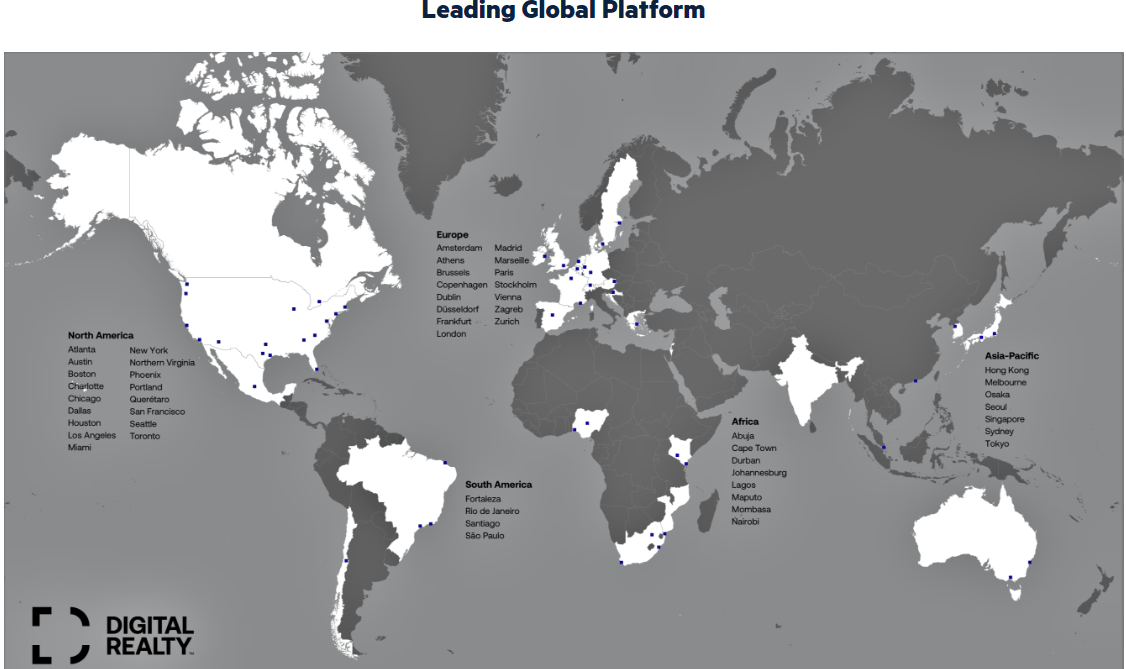

Digital Realty is a data center REIT that supports and works with leading enterprises around the globe to provide data center, interconnection, and colocation services. DLR has a global platform with more than 300 data centers located in over 50 metros across 25 countries and on 6 continents.

Digital Realty provides technology solutions to a variety of customers, providing enterprise colocation and even dedicated server halls for hyperscale customers.

DLR’s tenants include many of the world's top companies such as Amazon, Google Cloud, IBM, Oracle, Nvidia, and Microsoft Azure, and in total, DLR receives almost 50% of its annualized recurring revenue (“ARR”) from its top 20 customers.

Based on ARR, the majority of DLR’s customers provide cloud services, representing 36% of ARR, followed by network and content providers at 17% and 15%, respectively. Digital Realty has approximately 5,000 global customers, and 49% of their customer base is investment grade or equivalent.

{kind=link}

Unlike many REITs in 2023, DLR enjoyed the tailwinds from the advanced developments made in artificial intelligence (“A.I”) over the course of the last year.

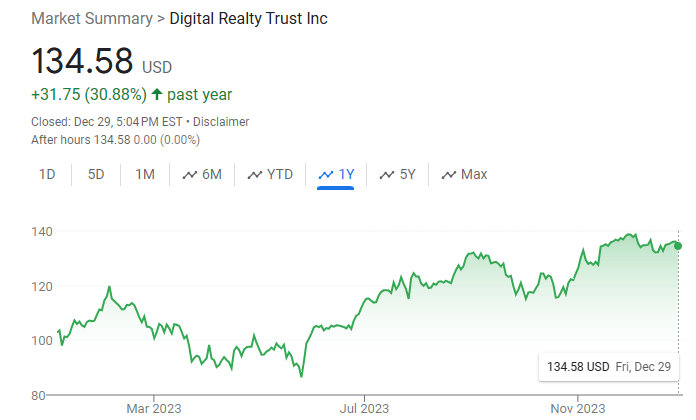

At its low point in 2023, DLR’s stock’s price fell around 16.56% from the beginning of 2023 to May 24, when the stock was trading at $86.49 per share.

From that point until the end of 2023, DLR’s stock price increased by 55.60%, giving the stock a total 2023 price return of +30.88%.

The proliferation of A.I. is expected to increase enterprise computing demands, which will benefit DLR by increasing the demand for its server rack space contained within its data centers.

{kind=link}

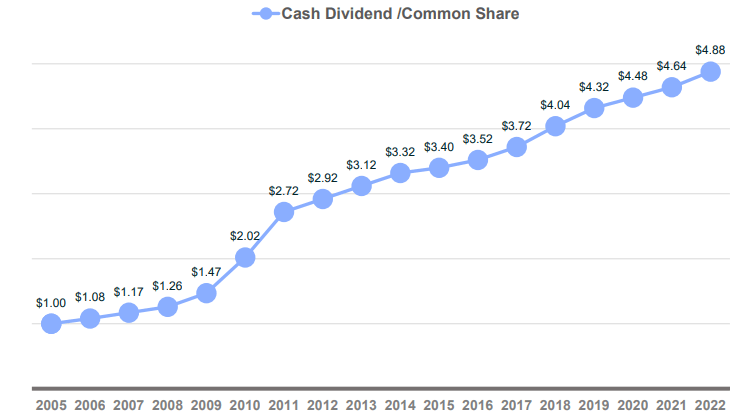

Digital Realty went public in 2004, and since 2005 they have increased their dividend each year up until 2022. Analysts expect the dividend to remain unchanged in 2023 from the rate paid in 2022, at $4.88 per share.

Additionally, analysts project moderate AFFO growth of 3% in the coming year and AFFO growth of 7% in 2025.

{kind=link}

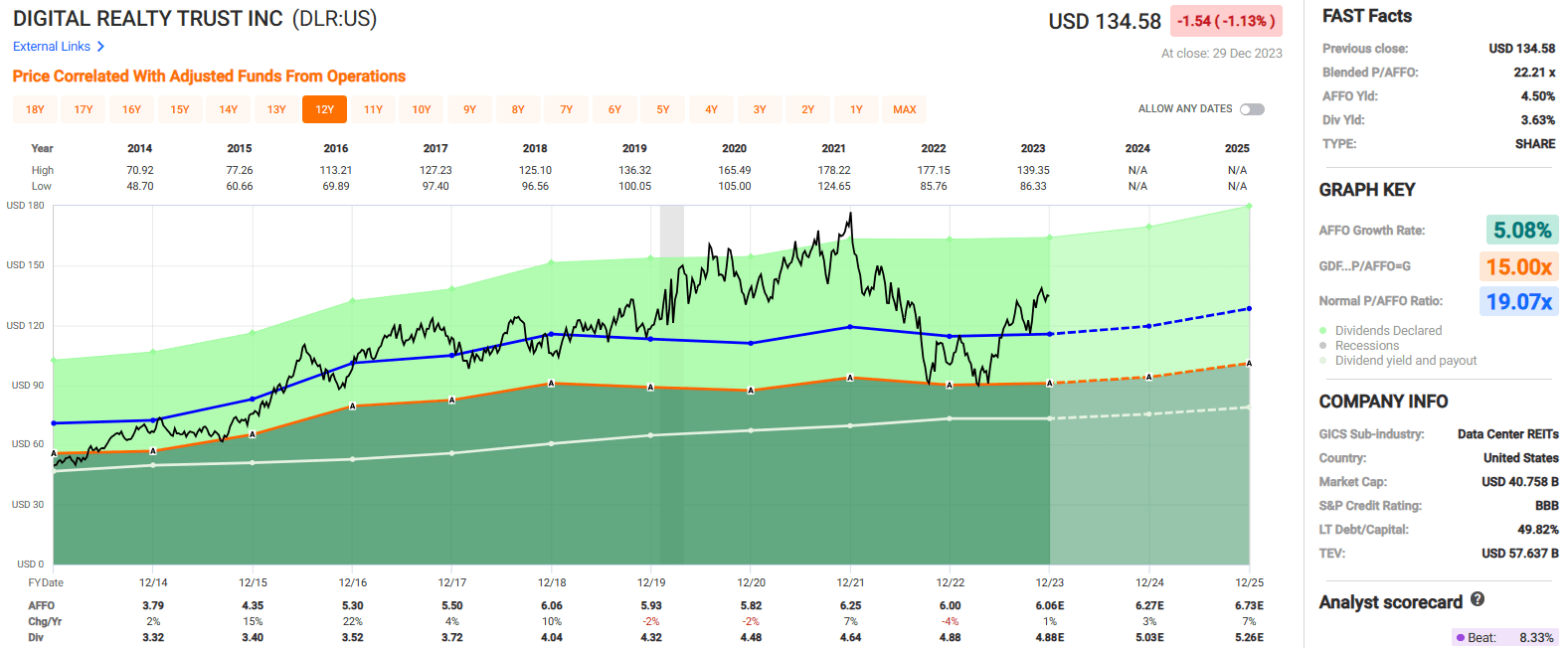

Over the last 10 years DLR has had an average AFFO growth rate of 5.08% and an average dividend growth rate of 5.11%.

The stock pays a 3.63% dividend yield that is well covered, with a 2023 expected AFFO payout ratio of 80.52% and trades at a P/AFFO of 22.21x, compared to its 10-year average AFFO multiple of 19.07x.

We rate Digital Realty Trust a Buy (very close to a Hold)

{kind=link}

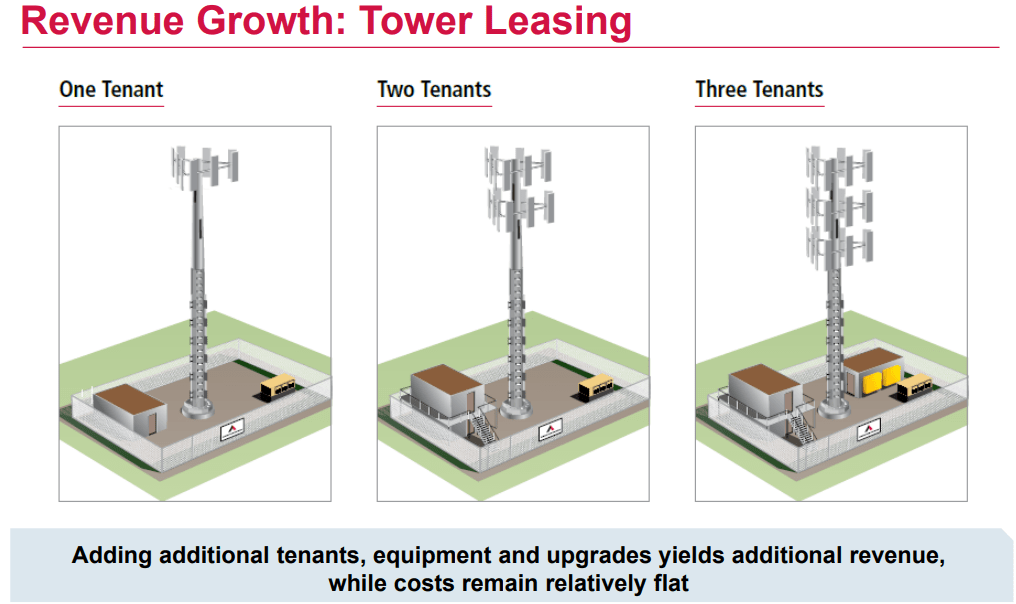

American Tower Corporation ( AMT )

AMT was founded in 1995 and has become one of the largest global REITs specializing in the development, ownership, and operation of broadcast and wireless communications real estate.

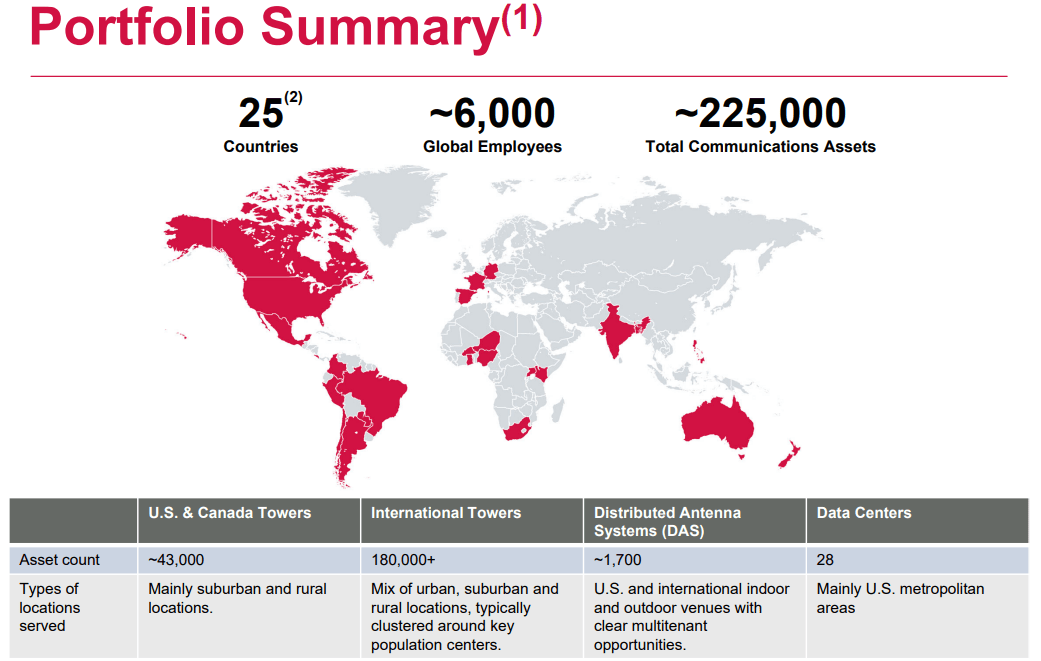

American Tower is a cell tower REIT with a market cap of almost $101.0 billion and a portfolio comprised of almost 225,000 multitenant communication sites located across 25 countries and on 6 continents.

AMT has approximately 43,000 U.S. and Canada Towers, more than 180,000 international towers, and around 1,700 distributed antenna systems.

In addition to their cell towers, AMT has a portfolio of 28 highly interconnected data centers located in the U.S.

{kind=link}

American Tower’s communication sites serve a variety of customers including government agencies, multinational telecommunication companies, broadband and media providers, and mobile network operators.

Essentially, AMT’s cell towers are used by agencies and enterprises that need to reach customers through wireless communications technologies.

Core to AMT’s business model is colocation, or neutral hosting, allowing the cell tower REIT to host multiple carriers on a single tower. This reduces infrastructure cost and increases profitability, as additional tenants generate additional revenue with very little incremental expenses added.

{kind=link}

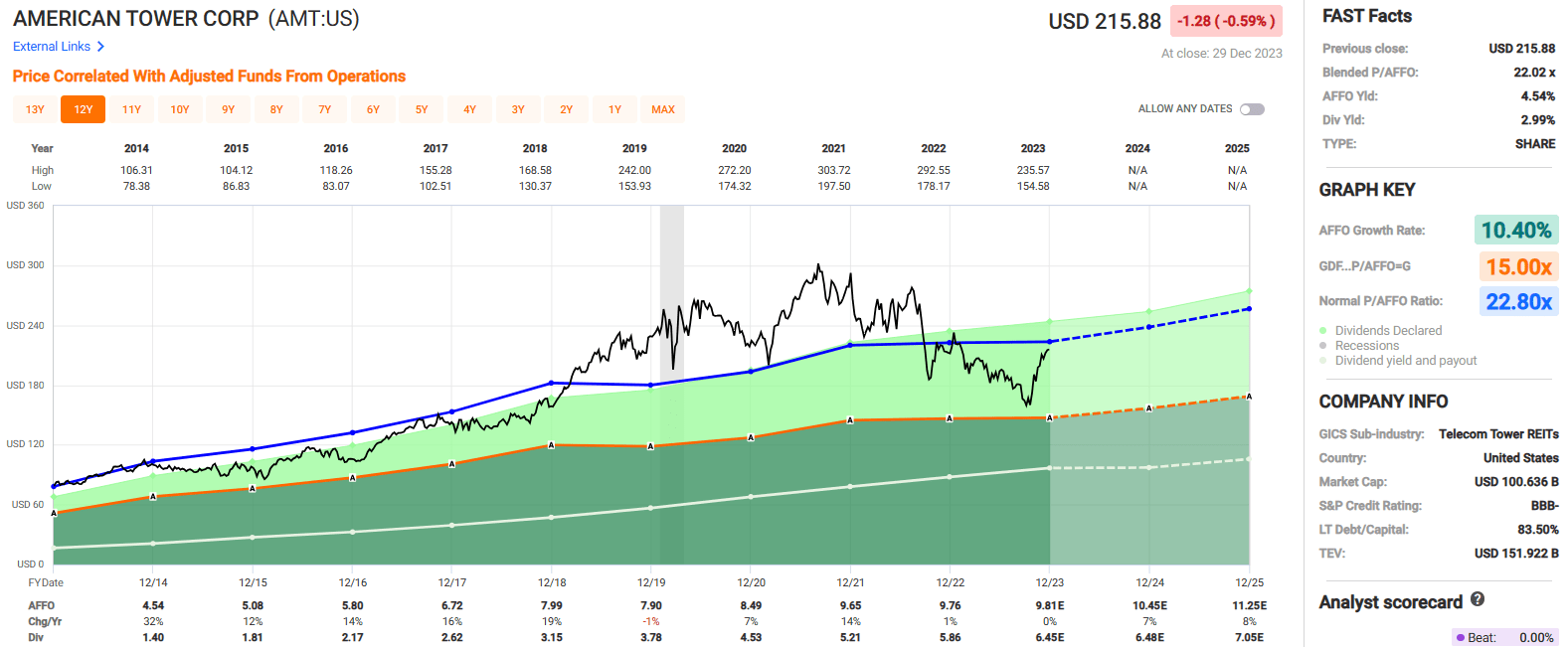

AMT’s price return was relatively flat in 2023, with a total price return of less than a percent. However, keep in mind that this does not factor in dividends paid, so in reality AMT returned closer to 3%-4% during the year, inclusive of dividends.

From January to the beginning of October, AMT’s stock price was down roughly -26%, but then rebounded from October to the end of 2023, gaining approximately 36% over the last several months.

AMT, like all other REITs, benefited from the Fed’s more dovish stance on interest rate projections for 2024. This just goes to show how much impact the 10-year TRSY yield had on REITs over the last several years and the disconnect between market prices and fundamental values.

Or, put another way, no business fundamentals caused the 36% rally we’ve enjoyed since October, but instead market factors such as the yield on bonds drove the rally. The same can be said for the stock price’s decline earlier in the year.

{kind=link}

Now, that’s not to say that AMT doesn’t face any business challenges; in fact, their AFFO growth slowed to 1% in 2022 and is expected to increase by less than 1% in 2023.

However, this looks to be a short-term aberration, as AMT has delivered an average AFFO growth rate of 10.40% over the last 10 years and analysts expect AFFO growth per share of 7% in 2024 and 8% in 2025.

AMT has excellent growth rates. In addition to its strong AFFO growth, AMT has delivered an average dividend growth rate of 20.53% since 2014.

Currently AMT pays a 2.99% dividend yield that is very secure, with a 2023 expected AFFO payout ratio of approximately 65% and the stock trades at a P/AFFO of 22.02x, compared to its 10-year average AFFO multiple of 22.80x.

We rate American Tower a Buy (getting close to a Hold)

{kind=link}

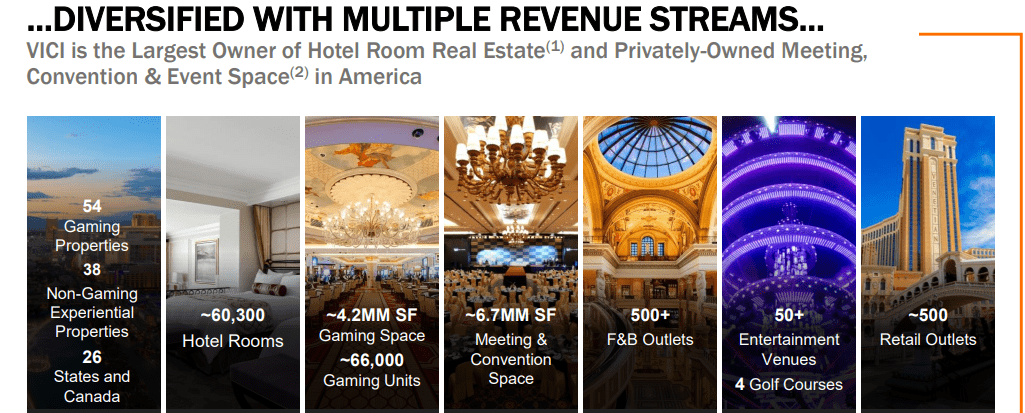

VICI Properties Inc. ( VICI )

VICI is a gaming REIT that invests in experiential real estate, with a 127 million SF portfolio that is comprised of 93 experiential assets, including 54 gaming properties and 39 non-gaming experiential properties.

Their non-gaming properties primarily consist of family entertainment centers (bowling alleys) that VICI recently acquired in a sale-leaseback (“SLB”) with Bowlero ( BOWL ). These are located across 17 states.

VICI’s 54 gaming facilities include multiple iconic trophy properties along the Las Vegas Strip such as Caesars Palace, Excalibur, Harrah’s Las Vegas, The Mirage, and The Venetian Resort.

In total, their gaming properties contain around 4.2 million SF of gaming space and approximately 66,000 gaming units.

Additionally, their gaming properties include roughly 60,000 hotel rooms, around 500 retail outlets, and more than 500 nightclubs, sportsbooks, bars, and restaurants.

To top it off, VICI owns 4 championship golf courses and over 30 acres of developable land adjacent to the Las Vegas Strip.

{kind=link}

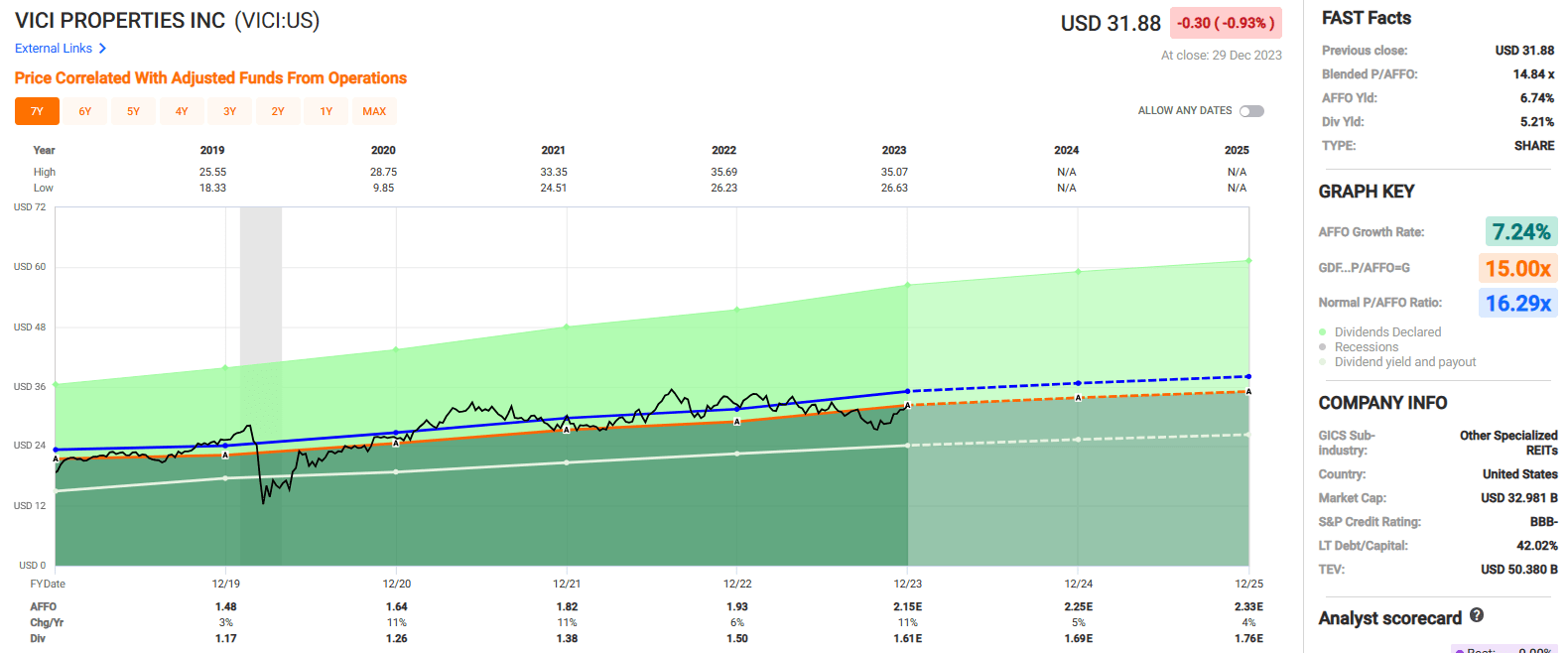

VICI’s stock price was essential flat on the year, gaining less than a percent in 2023.

At its low point on October 30 th , VICI stock price was down by approximately 14% on the year. However, from October 30 th to the end of 2023 the stock price rallied by +17.29%.

Other than Digital Realty Trust, you might notice a pattern in the price action for the REITs discussed.

Once the Federal Reserve indicated it was likely done tightening in 2024, most REITs rebounded in lock-step, providing further evidence that much of the suffering in “REIT-dom” had more to do with interest rates, instead of failing business models or other fundamental issues.

{kind=link}

Since 2019, VICI has had an average AFFO growth rate of 7.24% and an average dividend growth rate of 10.80%.

Over the next several years, analysts forecast AFFO growth below VICI’s historical average, with projections for AFFO per share to increase by 5% in 2024 and by 4% in 2025.

While these growth projections are under VICI’s average, it is still solid growth for a net lease REIT and should provide more than enough coverage for its dividend.

Currently VICI pays a 5.21% dividend yield that is well covered with an expected 2023 AFFO payout ratio of approximately 75%. The stock trades at a P/AFFO of 14.84x, compared to its normal AFFO multiple of 16.29x.

We rate VICI Properties a Buy.

{kind=link}

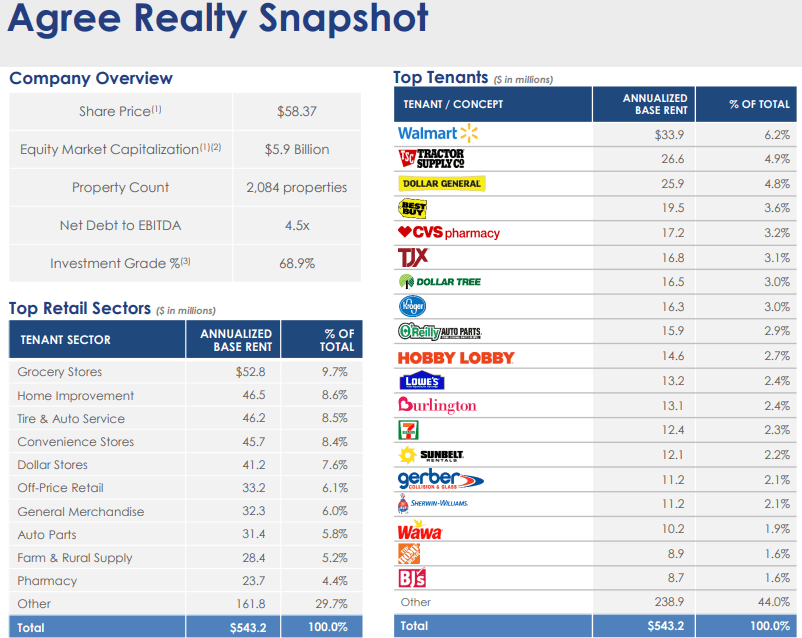

Agree Realty Corporation ( ADC )

Agree Realty is a net lease REIT that specializes in the acquisition, ownership, and management of commercial real estate that is net leased to leading retailers in defensive industries that are resistant to ecommerce and recession.

ADC prides itself on the quality of its tenants and receives approximately 69% of their annualized base rent (“ABR”) from investment-grade tenants. I would say that the quality of ADC’s tenants, and by extension, the properties they own, is one feature that really stands out with ADC. Some of their top tenants include Walmart, Tractor Supply, Dollar General, Best Buy, CVS, and Kroger.

ADC’s top retail sectors include grocery stores, which make up 9.7% of Agree Realty’s ABR, followed by home improvement and auto service, which make up 8.6% and 8.5% respectively.

At the end of the third quarter, ADC’s portfolio consisted of 2,084 commercial properties totaling roughly 43.2 million SF of gross leasable area across 49 states. Their portfolio was 99.7% leased and had a weighted average lease term of 8.6 years.

{kind=link}

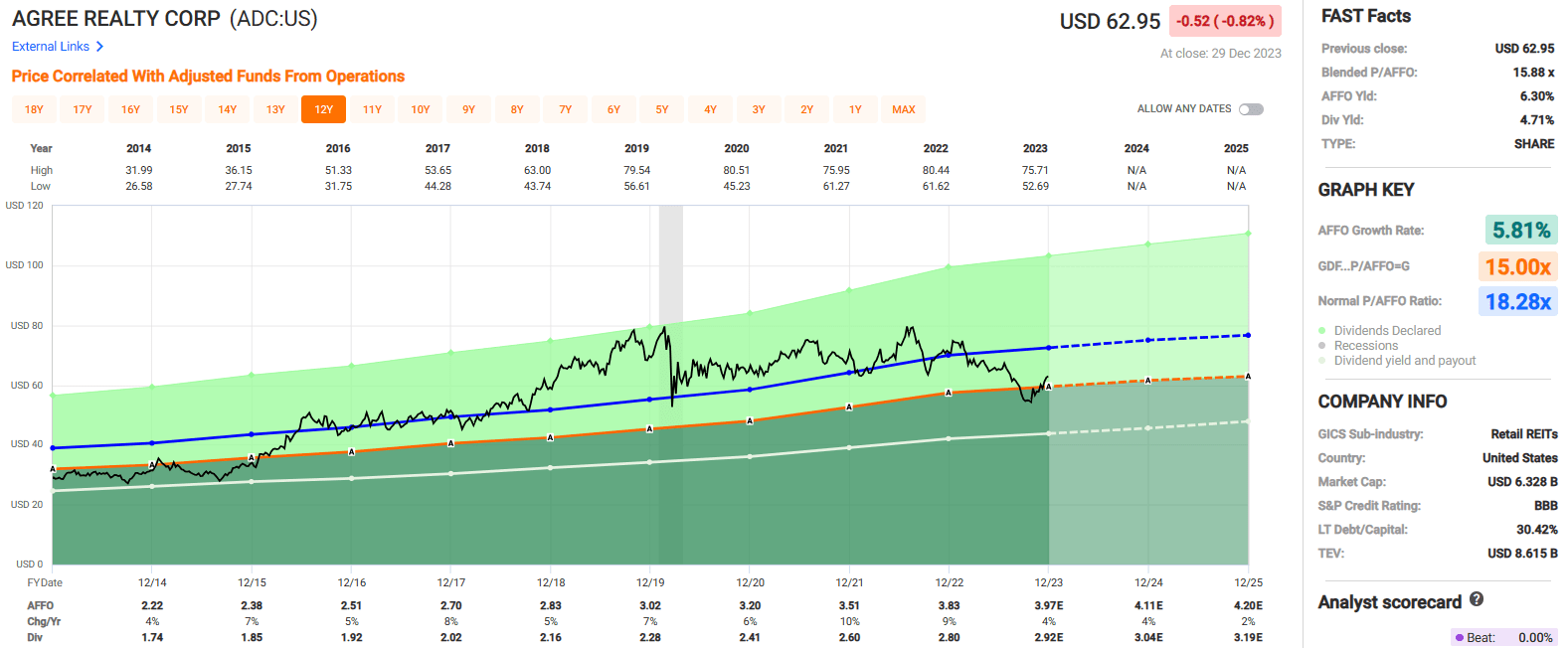

Over the course of 2023, ADC’s stock price fell by -10.81%, in line with several of its net-lease peers. You’ll notice the same pattern in its price chart below, with the stock declining steadily up until the end of October, with ADC down -23.62% YTD as of October 12 th .

From that point until year-end, ADC stock price rallied +16.77%, again showing how much interest rates and the Federal Reserve impact the market’s sentiment on REITs.

{kind=link}

Since 2014, Agree Realty has had an average AFFO growth rate of 5.81% and an average dividend growth rate of 6.15%. Analysts expect AFFO to increase by 4% in 2024 and then by 2% the following year.

ADC pays a 4.71% dividend yield that is well covered with a 2023 AFFO payout ratio of 73.55% and currently trades at a P/AFFO of 15.88x, compared to its average AFFO multiple of 18.28x.

We rate Agree Realty a Buy.

{kind=link}

In Closing

The above-referenced REITs now make up close to 30% of my portfolio, with Realty Income being the largest holding (at ~10%).

I'm perfectly content with these positions, which I expect to generate ~20% returns over the next 12 months.

I bought all of these in 2023, and I'm thrilled to see the success of Digital Realty, that is one of my top-performing REITs in 2023. I'm also happy that I was able to pounce on American Tower, which has returned ~15%.

As you can see, I'm overweight net lease REITs with core positions in Realty Income, Agree Realty, and VICI Properties. I also own Essential Properties Realty Trust ( EPRT ).

I hope you enjoyed this article, and I wish you the very best in 2024.

For further details see:

My Top 5 REIT Holdings Revealed