PAXS - My Views On Asset Allocation: Shifting From Equities To Credit Cash And Gold

2023-10-16 16:50:15 ET

Summary

- I suggest shifting investment focus from equities to credit-based securities due to hints of higher interest rates for longer than expected.

- Clearbridge Investments warns of rising uncertainty and market volatility, supporting the suggestion to move away from traditional equity investing.

- I recommend allocating a portion of the portfolio to cash and gold as a defensive measure against potential economic downturns.

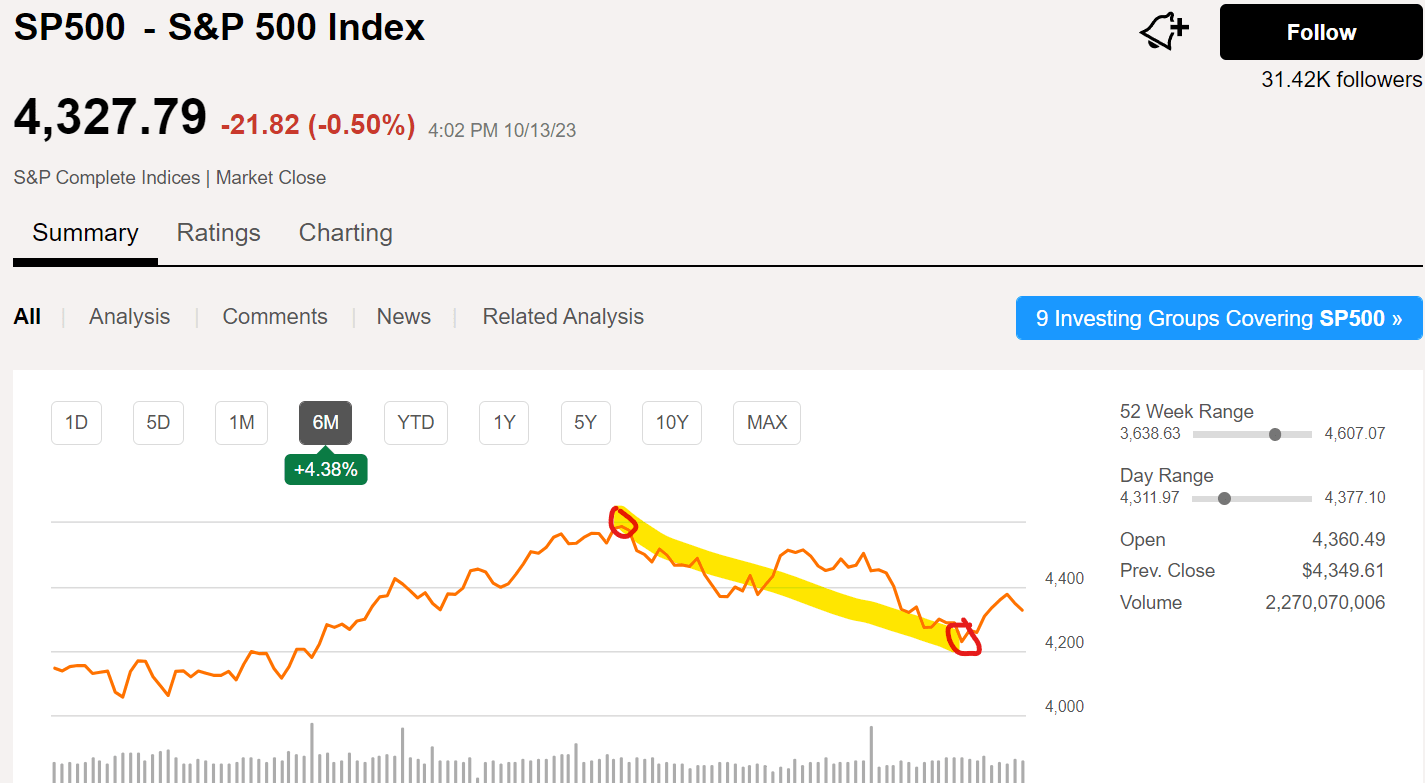

As I begin to invest my pension payout over the past several weeks, taking advantage of lower prices after the downdraft in the major indexes from the beginning of August through the end of September (see chart below), I have been analyzing macroeconomic conditions and reading a lot about what we have to look forward to in 2024 and beyond. Some of what I have been reading gives me cause for concern, yet also confirms my approach to investing for income.

{kind=link}

What I am reading lately, (some of which is negatively slanted in part due to the recent conflict in Israel adding to general fears and uncertainty beyond the lingering war in Ukraine), are hints of higher interest rates for longer and potentially much longer than many are expecting, or at least hoping for, and that we need to buckle down as investors and prepare for the long-term payoff. One way to do that is to shift your thinking from an investment return that is based on capturing capital gains from stock appreciation to one that is an income-based approach from credit holdings such as fixed income, senior loans, CLOs, bonds, etc.

For many investors, both those who are more experienced as well as younger investors, this is a difficult transition to make when one is accustomed to seeing overall portfolio values rise. But if you consider the points made in a recent memo from Howard Marks of Oaktree Capital regarding the sea change that he is witnessing after 30 years of investing, he suggests a move away from equities and into credit. This line of thinking makes a lot of sense to me and confirms my approach to investing that is modeled after Steven Bavaria's strategy . I call my approach my Income Compounder portfolio.

From the recent memo written by Howard Marks of Oaktree Capital, his concluding remarks summarize the gist of his thoughts:

This isn't a song I've sung often over the course of my career. This is the first sea change I've remarked on and one of the few calls I've made for substantially increasing investment in credit. But the bottom line I keep going back to is that credit investors can access returns today that:

- are highly competitive versus the historical returns on equities,

- exceed many investors' required returns or actuarial assumptions, and

- are much less uncertain than equity returns.

Unless there are serious holes in my logic, I believe significant reallocation of capital toward credit is warranted.

Further support of this suggestion to move away from traditional equity investing in growth and value stocks to a more fixed income or credit-based defensive posture is a series of articles from Clearbridge Investments, a Franklin Templeton company. In their publications, they warn of a pending rise in uncertainty and market volatility for a variety of reasons including higher rates for longer, and potentially much longer than many are expecting.

From Clearbridge Investments on Asset Allocation: Allocation Views | Franklin Templeton

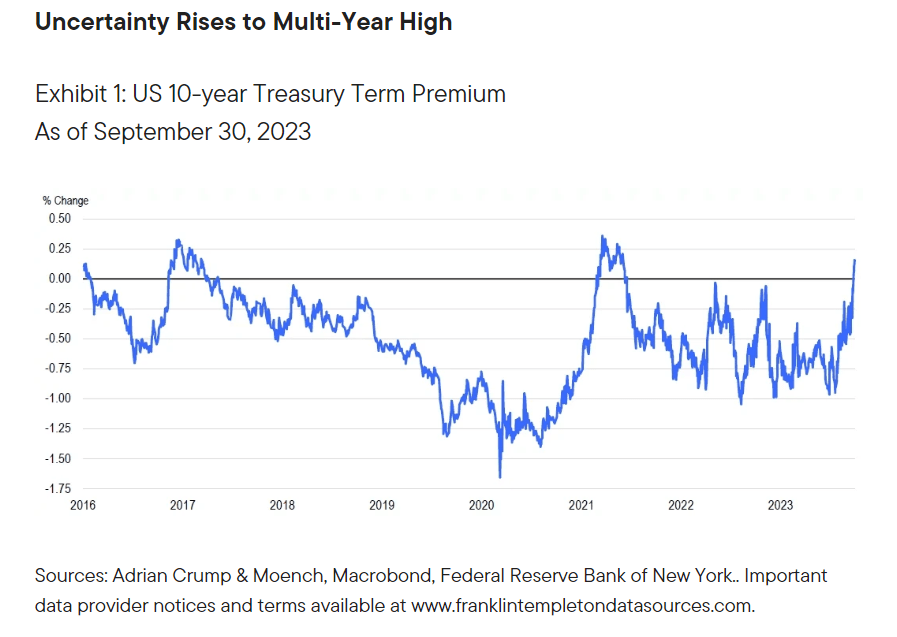

The US Federal Reserve held rates unchanged but hinted at one last hike still to come this year. Perhaps more tellingly, the Fed "dot plot" led financial markets to accept that rates would stay "higher for longer" or perhaps even "higher forever." This led to an ongoing rise in the so-called "term premium," or the return over anticipated short-term rates required to compensate for the uncertainty of holding longer-dated bonds (see Exhibit 1).

{kind=link}

They go on to clarify the impacts of this increasing uncertainty on the financial markets:

Even as inflation is likely to ease through the end of this year, it seems less certain that the Fed will rush to cut rates before the impact of slower growth is felt, as it will be these forces that cement the return to target levels of inflation. Only in select emerging economies are we now starting to see a moderation in monetary policy, which may help to support these markets. Overall, this sees our policy theme remain quite a negative driver for financial markets, even as it has evolved to downplay the likelihood of any further rate hikes while emphasizing "Policy to Remain Restrictive" even as we move into 2024.

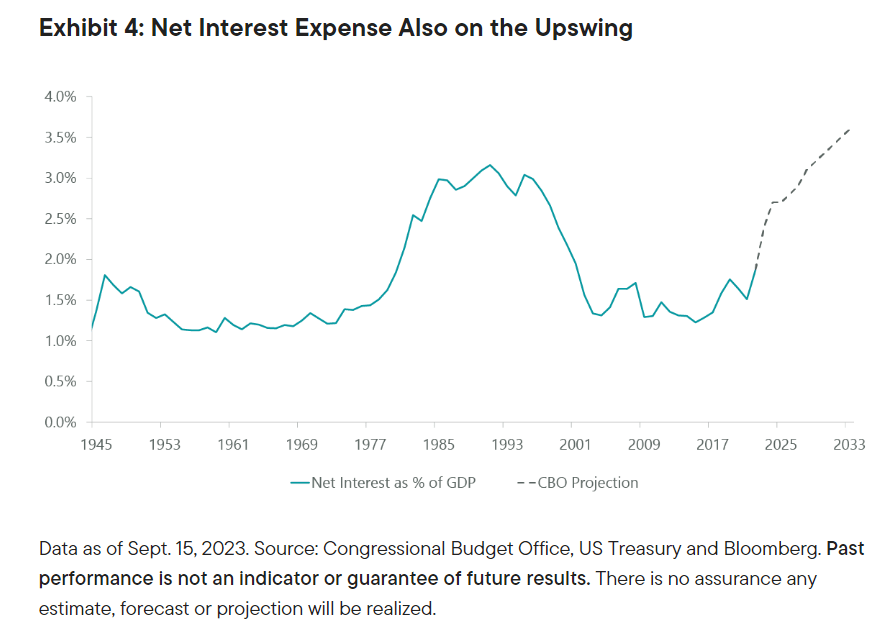

And then to add to those concerns over higher interest rates, we have ongoing concerns with US government spending, rising deficits, downgraded credit ratings, and general anxiety regarding interest payments on US debt. In this article from Clearbridge, those fears are elucidated:

Further, historically the 10-year Treasury has peaked right around when the Fed has completed their hiking cycle, meaning longer-term yields may stabilize in the coming months. Looking ahead, it appears that almost all Note and Bond maturities will be rolled over at higher yields, which should continue to put upward pressure on interest costs over the next several years.

{kind=link}

That scenario would tend to raise the term premium even higher as discussed above. This is put into context by the article to further explain the potential negative impact on equities:

If the term premium moves higher in the coming years, it could have important ramifications for financial markets, with higher Treasury yields having a significant impact on corporate credit, currencies, and equities. The most direct impact to equities would likely be in terms of higher interest expense, resulting in lower operating margins. Currently, this does not pose much of a concern due to many companies' large cash balances and little debt, but could prove challenging for smaller capitalization companies.

We… believe defensive leadership could outperform in the near term with long-term interest rates stabilizing or declining in the coming months. This view is based upon the notion that long-term rates have historically dropped following the conclusion of a Fed tightening cycle regardless of economic outcome. Longer-term, however, the trend in Federal deficits and term premiums leads us to believe investors would be well suited to prepare for the possibility of a regime change.

There is that reference to "regime change" again (or "sea change" according to Marks). These comments and my own observations and understanding of credit spreads, inflationary pressures, and ongoing fears of a coming recession confirm my belief that now is a good time to be overweight fixed income, credit-based securities, cash, and a small allotment to gold.

Why Cash is Good Now

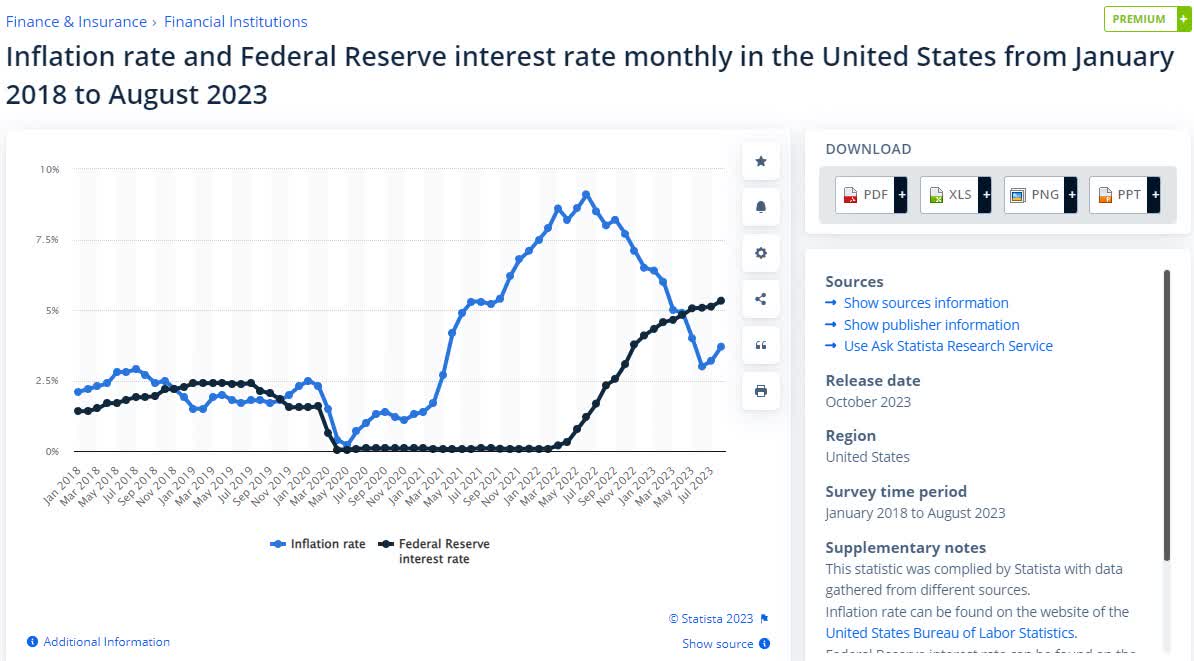

Last year when interest rates were still low and inflation was rising, as seen in this chart from Statista, the hot safe, cash alternative was I Bonds from the US Treasury. Now that interest rates have gone up and long-term Treasuries are approaching 5%, there are many other safe cash alternatives that pay interest rates of 5% and above.

{kind=link}

I currently have about 25% of my total investment portfolio saved in several of those cash alternatives such as ETFs that hold Treasuries, money market funds, Treasury bonds, and bank savings accounts. The rest is invested in fixed income such as high-yield bond funds, CEFs and other credit securities such as CLO funds, BDCs, and REITs - both common and preferred shares.

About half of my overall cash allotment is in funds that hold government bonds and short-term investments like iShares 0-3 Month Treasury Bond ETF (SGOV), currently yielding 4.75%; and WisdomTree Floating Rate Treasury Fund (USFR), now yielding 5.3%, as well as in a money market account with Fidelity (SPAXX, yielding 4.98%). Half of the cash investments are split about evenly between the two Treasury funds with the other half in SPAXX, so that I can use those funds for buying new securities when the opportunities arise. I also hold a much smaller amount of cash in an online savings account with UFB Direct, part of Axos Financial ( AX ) which pays up to 5.25%.

I also still hold a small amount of I Bonds but do not intend to allocate more to them unless the pegged inflation rate that will be announced for I Bonds starting November 1, amounts to more than 5% annualized, which is possible .

That would be an increase from the current 4.3% interest on I bond purchases made through Oct. 31. But it's less than the 6.89% rate offered on I bonds bought between November 2022 through April 2023.

The Case for Gold

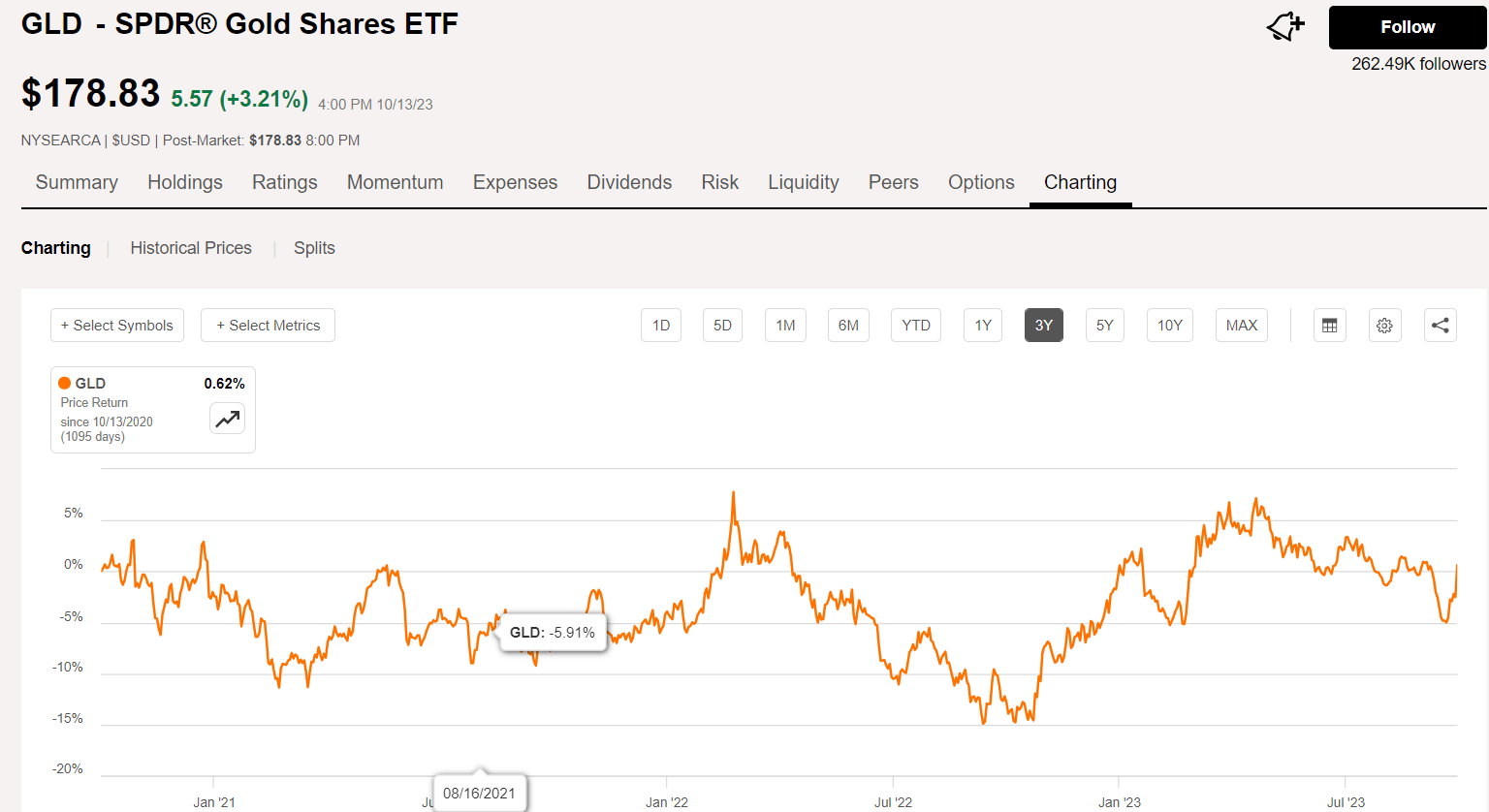

I have never been a big fan of gold, or anything close to a "gold bug", however, I do believe there is a time and a place for a small allocation of gold in one's long-term investment portfolio. Over the past 3 years, the price of Gold, as represented by SPDR Gold Shares ETF ( GLD ) has remained somewhat stable, trending around $1,900/oz with essentially less than 1% return on an investment made 3 years ago.

{kind=link}

However, that may have all changed about a week ago when Hamas attacked Israel and kicked off a new war. The price of gold started rising as investors suddenly sought " safe haven " assets. Combined with the belief that US interest rates may have now peaked, or soon will, Gold has become a more desirable asset, and the price has responded by moving back up above $1,900/oz. Gold mining stocks are the most likely to benefit from the combination of higher gold prices, moderating inflation, and pressure on the US Dollar and the Fed to reduce rates soon.

The Van Eck Gold Miners ETF ( GDX ) is one way to invest in gold mining stocks without trying to pick the best one or two miners to buy. A recent article from my fellow SA analyst outlines the reasons why GDX is a Strong Buy now, and I agree with his conclusion. I started a small position of about 2.5% of my portfolio with shares of GDX.

On the other hand, if interest rates do remain higher for longer, then gold miners will not advance as quickly and may even struggle to remain profitable due to rising input costs, and especially if the price of gold stalls again. For that reason, I would not invest a large portion of my retirement savings in gold but look to DCA into a bigger position of perhaps 5% of my total holdings over the next few months.

I posed the question to my Bing AI search engine "Is Gold a good investment now"? One of the responses was this recent news story (complete with ads for Gold sellers) from CBS News Money Watch with the title: "Is gold investing right for you? Here's how to decide."

Precious metals, like gold and silver, are also worth considering as an addition to your portfolio. Gold is popular among investors because it's considered a safe-haven asset, which means it tends to retain its value or even appreciate during times of economic uncertainty or market volatility. It also has a long history of being used as a store of value and a hedge against inflation. But gold prices can fluctuate in the short term, and it typically takes longer to see large returns on this investment.

As usual, it all comes down to your investment horizon (mine is more than 10 years), risk tolerance, objectives for investing (e.g., growth vs income), and cost. In my case, I am primarily focused on income but a small position in Gold in my portfolio could help offset some loss of value in other holdings such as equities if we do get into a full-fledged recession in the next year or two. And I believe that based on technical factors along with the current macro environment, gold is due to rise in price above $2,200 by 2024. Other SA analysts agree with me, including Avi Gilburt, who recently wrote about his expectations for gold prices:

So, I will reiterate my near-term expectations. I am looking for gold to rally to the $2,428 region as my next big target over the coming several years. Yet, if we see very strong extensions, it could even take us to the $2,700 region.

In summary, for me this is a tactical allocation to gold in the form of shares of GDX, and I am anticipating that my investment at today's cost should return more than 10% per year over the next year or two. I also bought a few shares of Barrick Gold ( GOLD ) in my taxable growth-oriented portfolio.

Concluding Remarks

Although the emphasis in this article is on cash, gold, and a sea change adjustment away from equities in my long-term investment portfolio, I do remain invested in equities (stocks, both common and preferred shares) and CEFs that hold equities including the Cornerstone funds, CLM and CRF. Like the name implies, they represent cornerstone holdings in my Income Compounder portfolio with a very high-yield income stream that is made even better with reinvestment at NAV. I also hold other stocks including 7 different BDCs in my portfolio currently. Most recently, I have been taking advantage of reduced prices for several REIT Preferred shares, including those offered by CMT, PMT, and TRTX, including the C shares (TRTX.PR.C) which offer a relatively "safe" yield of 11%.

The majority of my income investments consist of CEFs that hold high-yield bonds, CLOs, senior secured loans, and other credit and fixed income instruments including some private credit and alternative assets. For example, I hold a full position in Simplify Volatility Premium ETF (SVOL), which currently yields 17% and has been holding up quite well despite the recent rise in the VIX.

I also loaded up over the past couple of months on Floating Rate senior secured loans including AFT, BGT, JFR, PHD, and VVR. Most of those funds have recently increased the distribution and all of them yield in excess of 11% and benefit from rising rates yet still trade at a discount to NAV.

One last point that I want to mention is that when I say I am "shifting" my asset allocation, that mostly refers to new money being invested. I am not selling anything (other than ZTR, which I wrote about here ). I typically reinvest in those funds that offer DRIP at a discount such as CLM/CRF, the Pimco funds such as PAXS (you can read more about that fund here ), GOF, OPP, OXLC, ECC, and a few other funds that offer up to 5% discount for reinvesting.

My income stream continues to grow as I reinvest my monthly distributions in whatever asset offers the best value at the time. Lately, that has included mostly cash and gold as I have explained herein. Now I will be watching the markets to see whether things turn south again. With Q3 earnings season starting up, I believe that the market direction will become clearer over the next several weeks. We may be in for a soft landing, or we may be headed towards recession. Either way, I will be prepared.

For further details see:

My Views On Asset Allocation: Shifting From Equities To Credit, Cash, And Gold