TRS - Myers Industries Deserves Upside Despite Recent Weakness

2023-05-17 06:32:34 ET

Summary

- Myers Industries has experienced weak financial results in recent months, but the company's long-term prospects remain positive.

- The company's management expects sales growth and earnings per share to improve throughout the rest of the year.

- Despite short-term challenges, Myers Industries' low share price and favorable outlook make it an attractive investment opportunity for long-term investors.

Sometimes, patience is required in order for an investment prospect to pay off. This is especially true when the company you're acquiring stock in is experiencing some weakness from a fundamental perspective. A good example of one firm that I was bullish on and still am bullish on that has underperformed over the past few months is Myers Industries ( MYE ), an enterprise that's engaged in the production of durable plastic reusable containers, pallets, small parts bins, and more. The company also engages in the distribution of tools, equipment, and supplies, mostly centered around the automotive market. As a value-oriented investor, I place a great deal of value on how cheap a stock is. But during uncertain economic times and with a company that is experiencing some weakness on both its top and bottom lines, you cannot expect every value-oriented prospect to move higher just when you buy it. Despite the weaknesses that Myers Industries has demonstrated as of late, I would make the argument that the firm still does offer some upside from here. Because of this, I've decided to keep it rated the 'buy' I had it rated previously.

Assessing recent weakness

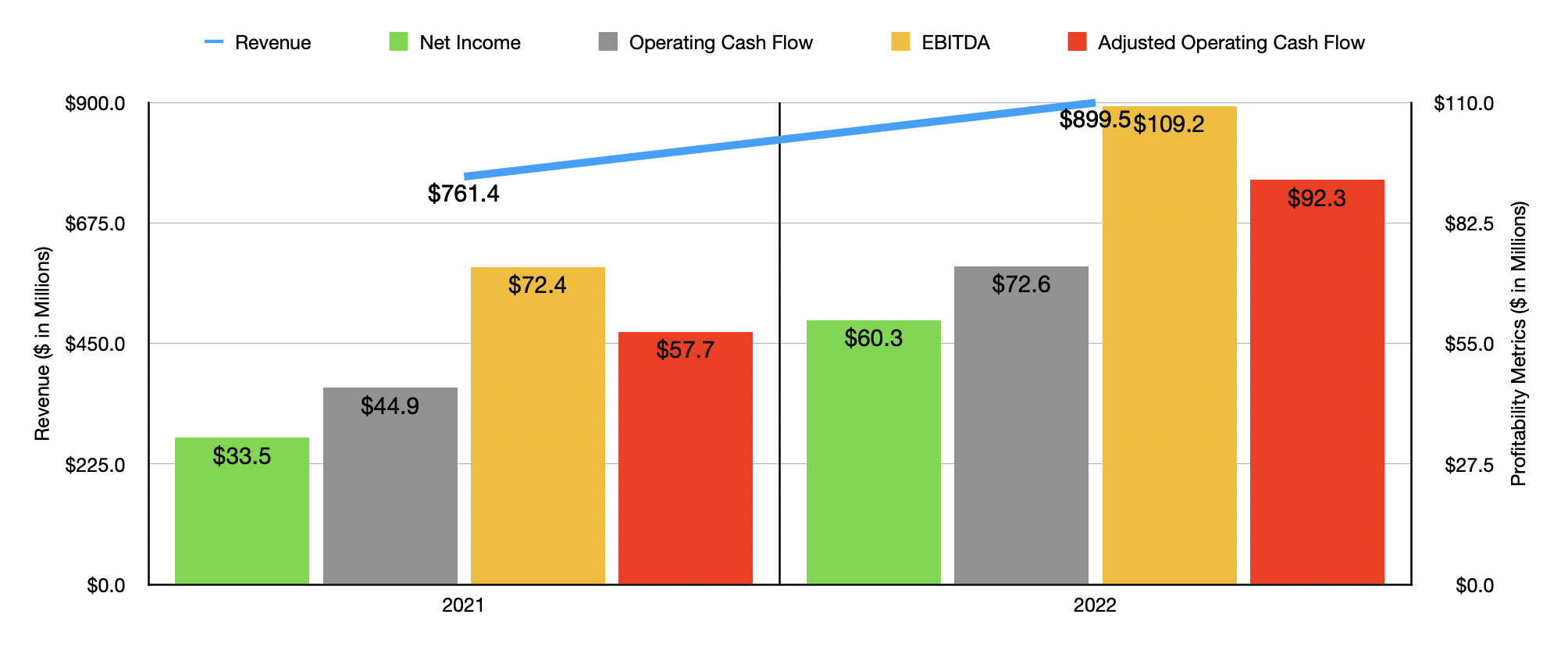

Back when I last wrote about Myers Industries in late October of last year, the company only had financial data covering through the third quarter of its 2022 fiscal year. Fast forward to today, and we now have financial results covering through the first quarter of the 2023 fiscal year. Late last year, the results posted by management were quite bullish. Consider data for 2022 in its entirety. Sales for the year came in at $899.5 million. That represented an increase of 18.1% over the $761.4 million the company generated one year earlier. Bottom line results for the firm were also up. Net income, for instance, had grown from $33.5 million to $60.3 million. Operating cash flow jumped from $44.9 million to $72.6 million. If we adjust for changes in working capital, we would have seen the metric increase from $57.7 million to $92.3 million. And finally, EBITDA for the firm grew from $72.4 million to $109.2 million.

{kind=link}

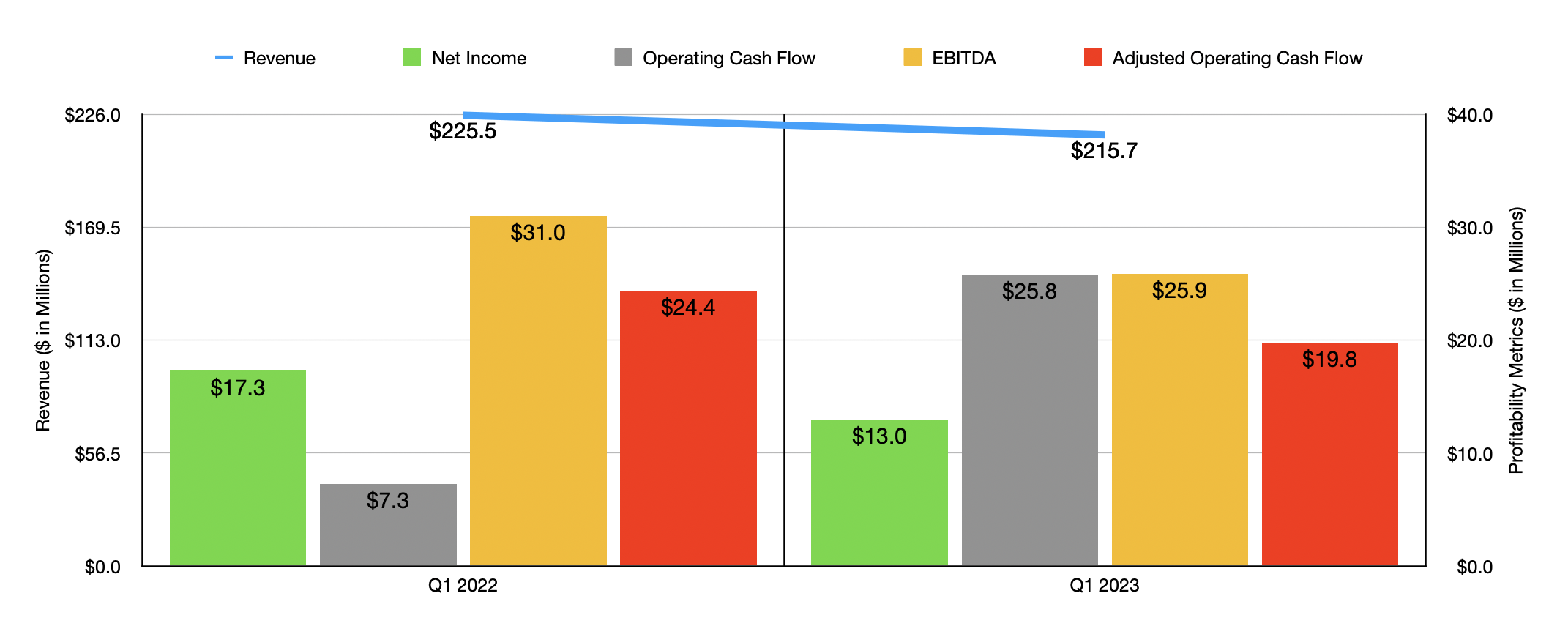

Given this robust performance from 2021 to 2022, it wouldn't be odd to bet that 2023 would shape up to be another great year for the company. But in some respects, strong performance has been elusive. In fact, for the first quarter of 2023 , revenue for the company actually came in weaker than it had been one year earlier. Sales of $215.7 million were below the $225.5 million reported for the first quarter of 2022. This decrease of 4.3% came about even though the company saw strength in the food and beverage market. Unfortunately, the consumer, vehicle, and parts of the industrial market, all suffered. Lower shipment volumes and a change in product mix negatively impacted the company to the tune of $25.4 million. The company's prior acquisition of Mohawk only helped offset this by about $2.5 million.

{kind=link}

The decline in revenue for the company also brought with it a worsening of its profitability. Net income, for instance, fell from $17.3 million to $13 million. Obviously, the decrease in revenue negatively impacted the company. But the firm also saw pain from a margin perspective. Its gross profit margin, for instance, did increase from 31.9% to 32.9%. However, selling, general, and administrative costs jumped from 21.3% of sales to 24.1%. These were largely due to acquisition activities, as well as higher salaries and benefits. For the most part, the weakness on the company's bottom line hurt the company's other profitability metrics as well. Although operating cash flow jumped from $7.3 million to $25.8 million, the adjusted figure for this, which removes changes in working capital, fell from $24.4 million to $19.8 million. Meanwhile, EBITDA for the company declined from $31 million to $25.9 million.

Despite these rather rocky results during the first quarter of the year, management believes that the rest of the year should show signs of improvement. For 2023 as a whole, sales growth should be in the low to mid-single digit range. Earnings per share, meanwhile, should be between $1.50 and $1.80. At the midpoint, that would imply net income of $60.7 million. If we assume that other profitability metrics will rise at the same rate that it should, we should anticipate adjusted operating cash flow of $92.9 million and EBITDA of $109.9 million. These numbers are only marginally better than what we've seen in 2022, which would imply a rebound from the weakness the company experienced during the first quarter.

{kind=link}

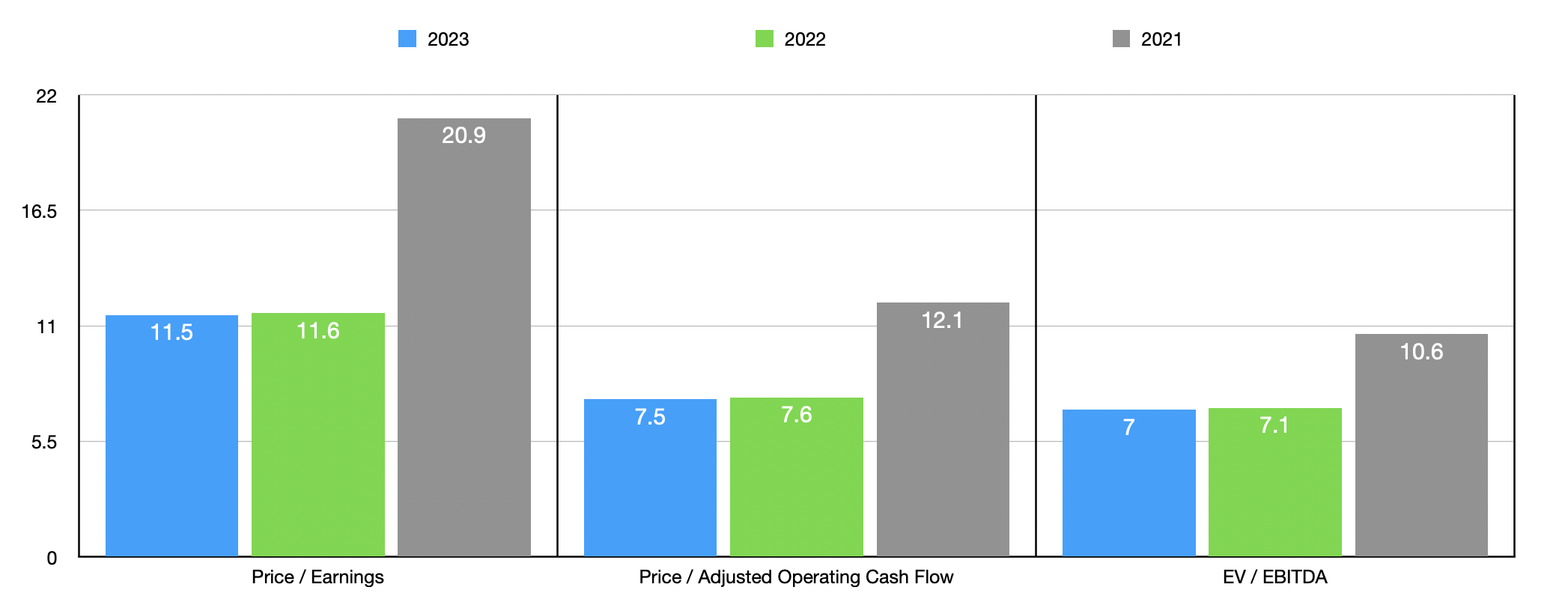

If these numbers come to fruition, the company would be trading at a forward price to earnings multiple of 11.5. The forward price to adjusted operating cash flow multiple would be even lower at 7.5. And the forward EV to EBITDA multiple for the company would come in at only 7. As you can see in the chart above, this pricing is almost identical to what we get if we use data from the 2022 fiscal year. As part of my analysis, as I do with many other companies I write about, I decided to compare Myers Industries to five similar enterprises. On a price to earnings basis, three of the five companies were cheaper than our prospect. When it comes to the other valuation approaches, however, the picture changes for the better. On a price to operating cash flow basis, as an example, only one of the five companies was cheaper than Myers Industries. And when it comes to the EV to EBITDA approach, I found that two of the five firms were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Myers Industries |

| 11.6 |

| 7.6 |

| 7.1 |

| TriMas ( TRS ) |

| 18.6 |

| 13.9 |

| 9.8 |

| O-I Glass ( OI ) |

| 4.8 |

| 98.2 |

| 4.8 |

| Greif ( GEF ) |

| 8.1 |

| 5.5 |

| 6.6 |

| Ardagh Metal Packaging ( AMBP ) |

| 5.5 |

| 14.8 |

| 9.1 |

| Silgan Holdings ( SLGN ) |

| 16.1 |

| 13.7 |

| 10.5 |

Takeaway

I acknowledge that the picture for shareholders, from a fundamental perspective and a share price perspective, has not been particularly exciting when it comes to Myers Industries. Given uncertain economic conditions, I can understand why investors might view this as a sign to move on. This sentiment has definitely been reflected in the company's share price. Since I last wrote about the firm late last year, shares are down 4.1% at a time when the broader market is up 5.9%. But for those focused on the long haul, the low share price of the company and management's favorable outlook for the year, makes me believe that some upside is still available from this point.

For further details see:

Myers Industries Deserves Upside Despite Recent Weakness