PWR - MYR Group: Driving The Energy Transition

2023-06-26 13:33:15 ET

Summary

- MYR Group is a holding company of electrical and industrial contractors with 13 subsidiaries, some over 100 years old.

- MYR Group is a great way to play the energy transition, which will unfold over the next decade.

- MYR Group's strong management team, pristine balance sheet, and history of successful M&A can all drive outperformance.

Investment Thesis

MYR Group's ( MYRG ) position as a key enabler of the energy transition through its work on transmission & distribution infrastructure, data center expansion, and green energy installation should allow it to take advantage of fiscal tailwinds. By combining the billions of dollars in infrastructure investments with a strong management team, a history of successful M&A, and an impeccable balance sheet, I believe MYR Group will make for a good long-term investment.

Background and History

MYR Group is a company with a storied history. It is a holding company of electrical and industrial contractors and consists of 13 subsidiaries. Some of these subsidiaries are over 100 years old with the oldest, L. E. Myers, in business since 1891. These subsidiaries work independently and funnel money back to the holding company to reinvest back into the business. This decentralized business model has helped MYR Group outperform the market since 2016.

Over its history, MYR Group has fluctuated as a public and a private company. It went public in its current incarnation in 2008, but its earnings growth was erratic and somewhat stagnant between 2010 and 2017. Accordingly, its share price lagged the market during that time period. However, its revenue had grown at a CAGR of about 7.8% between 2010 and 2017 from $631 million to $1.037 billion, meaning that the company was growing, but not creating value.

In 2016, Engine Capital, which owned 4.6% of the company at the time sent a letter to the board requesting a sale or recapitalization of the company to create more shareholder value. As a result of the letter , Engine Capital appointed 2 board members and a new CEO soon took over, Rick Swartz, who is also the current CEO. Since the start of 2017, MYR Group has had impressive financial performance with revenue growth accelerating to grow at a CAGR of 17.8% between 2017 and 2023, EPS growing at a CAGR of 27.18%, and share price performance that has outperformed the S&P 500.

With Rick Swartz as CEO, MYR Group has pursued a strategy of share repurchases, M&A, and investments in organic growth, all of which I believe can continue to drive the share price higher and help MYRG outperform the market over the medium to long term.

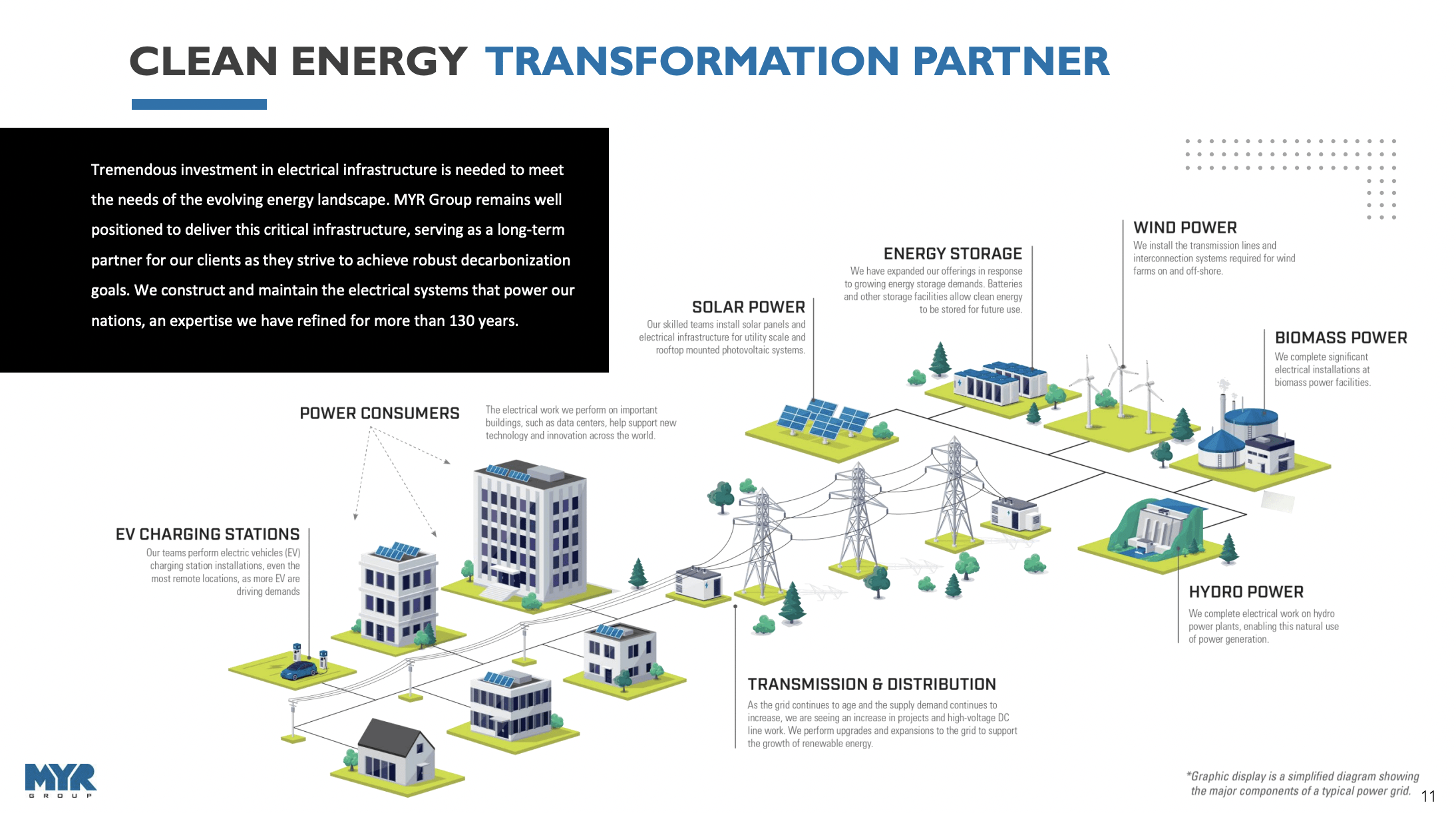

Shares outstanding have gone down 20% since 2016 and acquisitions such as Western Pacific Enterprises in 2016, Huen Electric in 2018, and Powerline Plus companies in 2022 have expanded MYR Group's scope and driven strong shareholder value creation. MYR Group now has a wider range of construction capabilities and is well-positioned for the future. Their abilities are summarized in the graphic below and range from traditional transmission & distribution construction to solar energy installations and data center buildout.

MYRG Capabilities (MYRG Investor Presentation)

{kind=link}

MYR Group is also riding significant fiscal tailwinds as the Bipartisan Infrastructure and Jobs act and the Inflation Reduction Act (IRA) will provide over $1 trillion in capital for the green energy transformation. Alternative Asset Managers have also been vocal about the vast need for capital and the opportunities for capital deployment in the space .

Brookings Institute

Peer Analysis

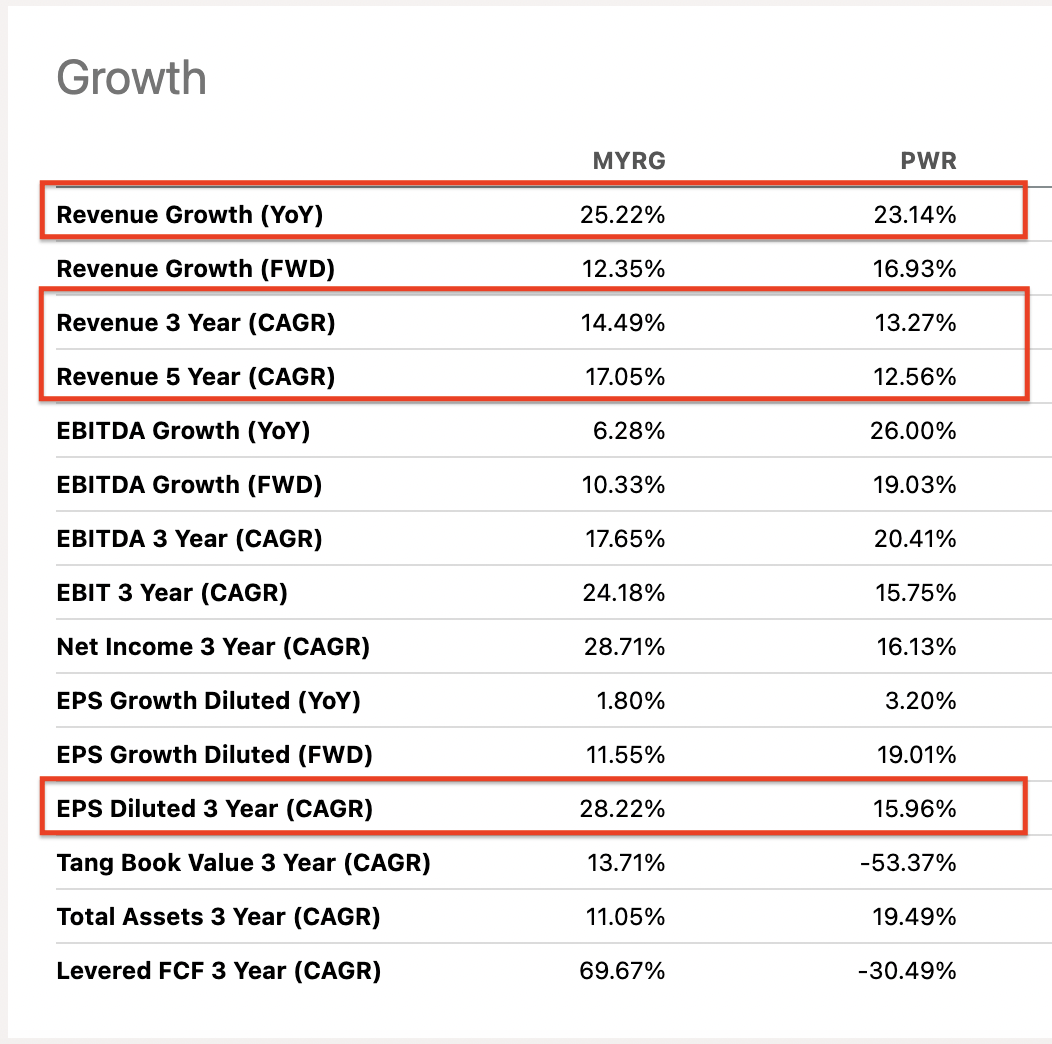

MYR Group is the little brother of the energy transition. The big brother is Quanta Services ( PWR ), which ranks at the #1 electrical contractor holding company with over 3x as much revenue as MYR Group. A comparison of the two is shown below with both having similar revenue growth over the past year, but MYR Group does have better 3-year revenue growth and EPS growth. MYR Group also has a stronger balance sheet than Quanta Services as Quanta has $4.08 billion in long-term debt while MYR Group has close to zero long-term debt.

MYRG v. PWR Growth (Seeking Alpha)

{kind=link}

In fact, this may have something to do with incentives as MYR Group management is incentivized on ROIC, which uses net income as an input, thus prioritizing the generation of net income. Free cash flow conversion is also better for MYR Group.

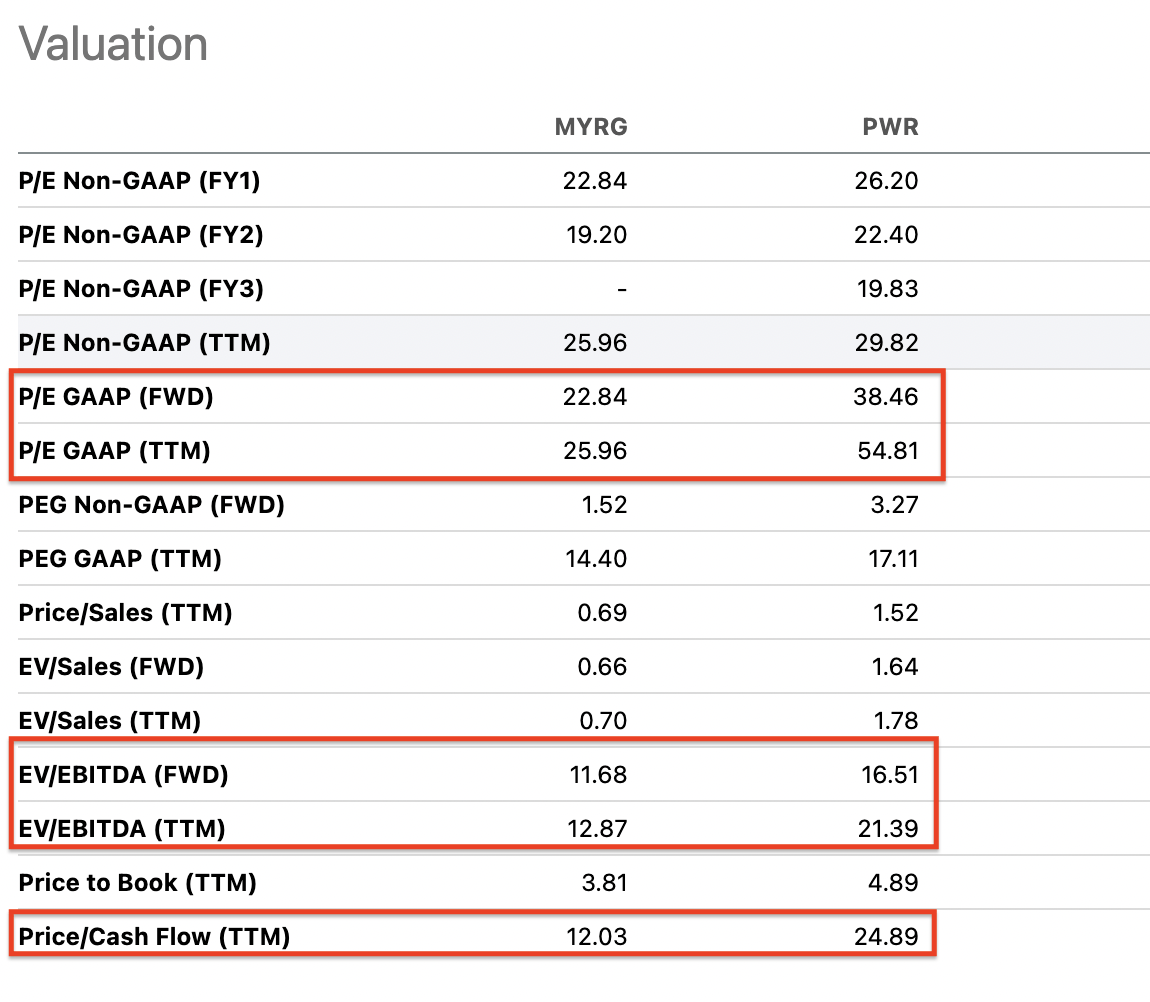

Yet despite these similarities in growth and profitability, MYR Group trades at half the valuation of Quanta Services on a GAAP P/E, EV/EBITDA, and Price/Cash flow basis, as showcased below.

MYRG v. PWR Valuation (Seeking Alpha)

{kind=link}

This may be due to the fact that MYR Group's expected future revenue and EPS growth is much less than Quanta Services. Analysts expect MYR Group to grow revenue 12.35% and EPS 11.55% while Quanta Services is expected to grow revenue at 16.93% and EPS at 19.01%.

I believe this discrepancy in expectations between two similar businesses is unwarranted given MYR Group's history of similar revenue growth, the fiscal tailwinds, and the strong management in place at MYR Group.

MYR Group Valuation

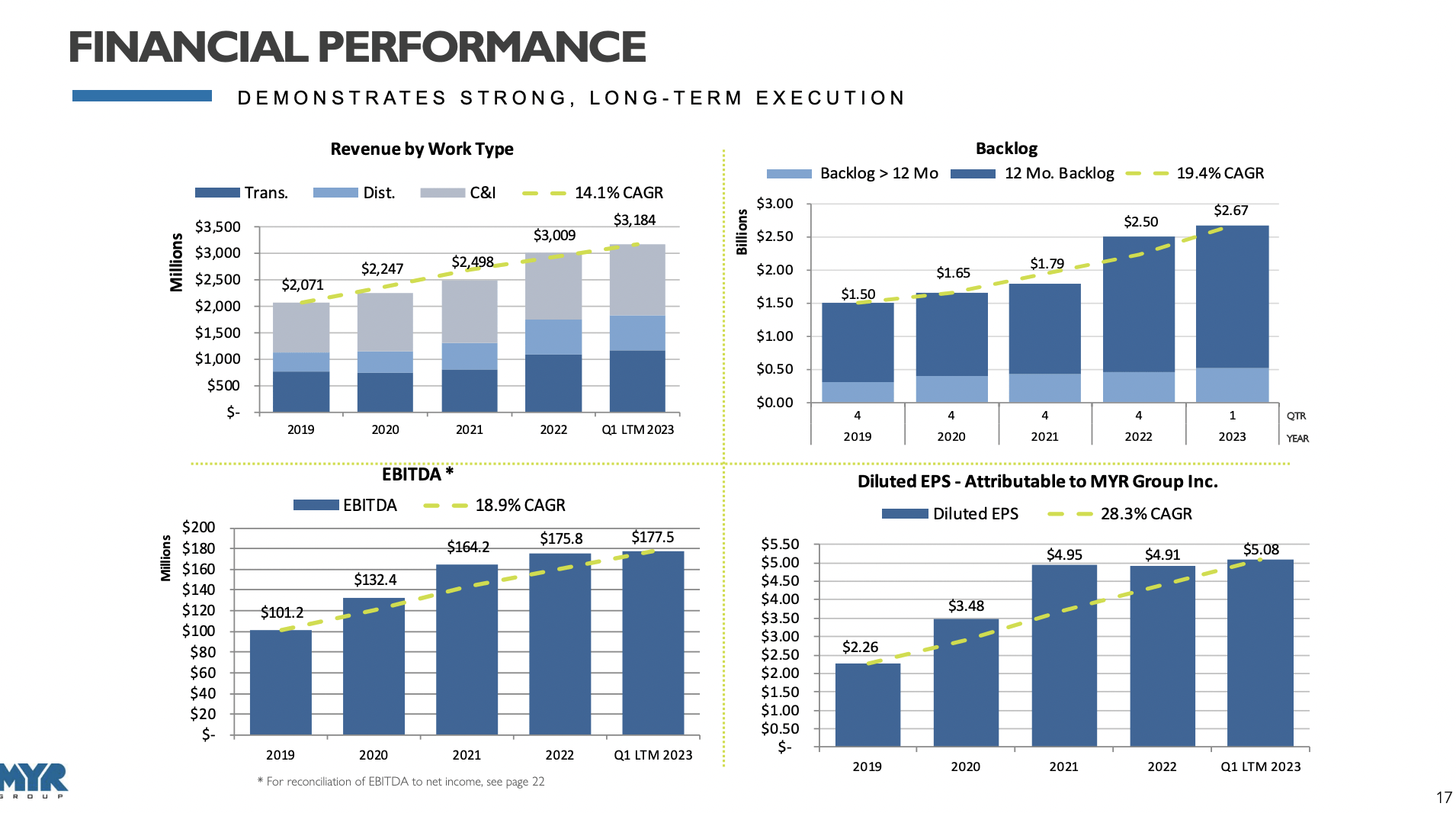

I believe MYR Group can grow EPS at a strong 15% CAGR over the next 7 years, which is slower than their past 3 years in which EPS grew at an astounding 28% rate. There are a few reasons I believe my estimate is conservative. MYR Group has grown its backlog at a CAGR of 19.4% over the past 3 years, which is a good proxy for future revenue growth as backlog converts into revenue.

{kind=link}

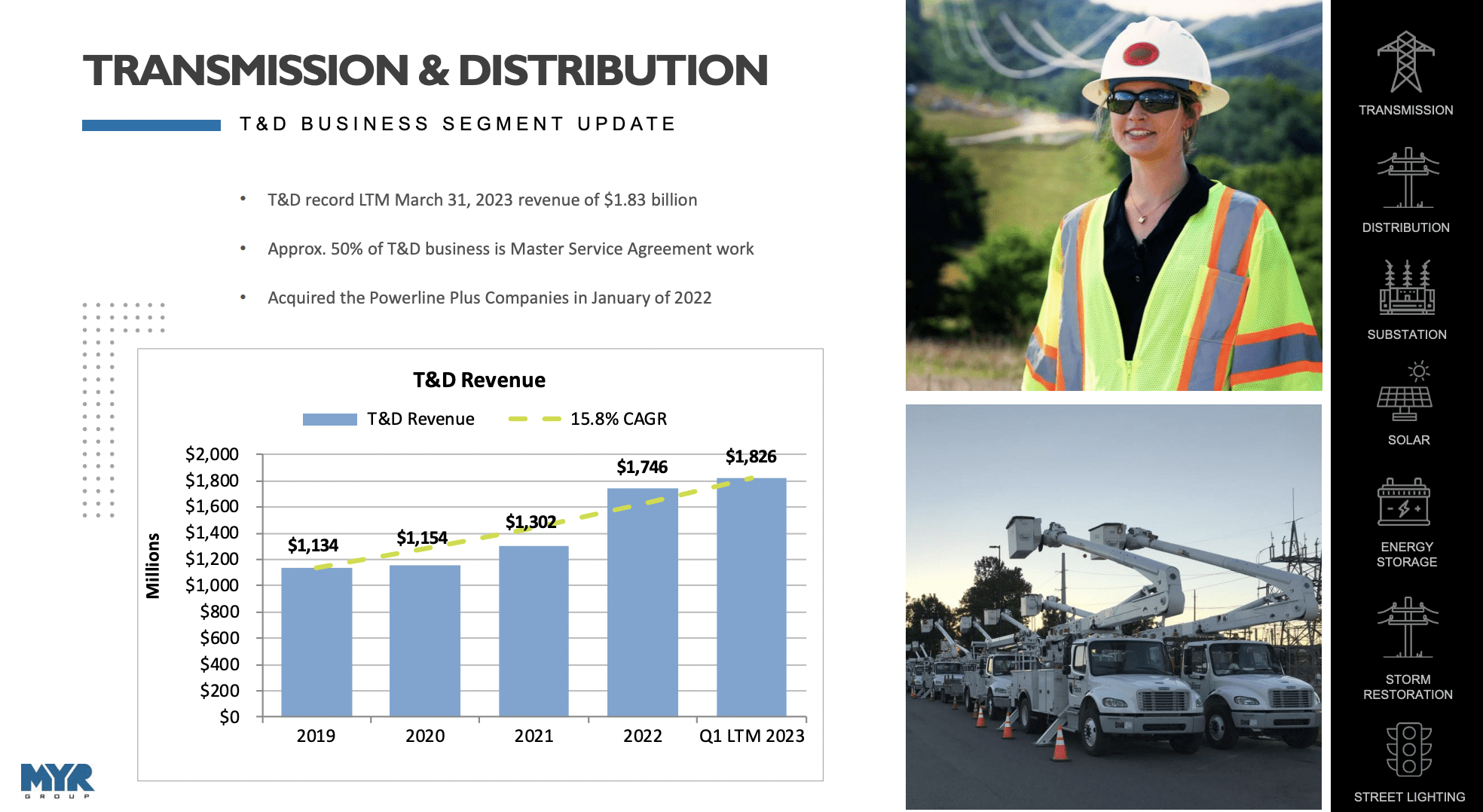

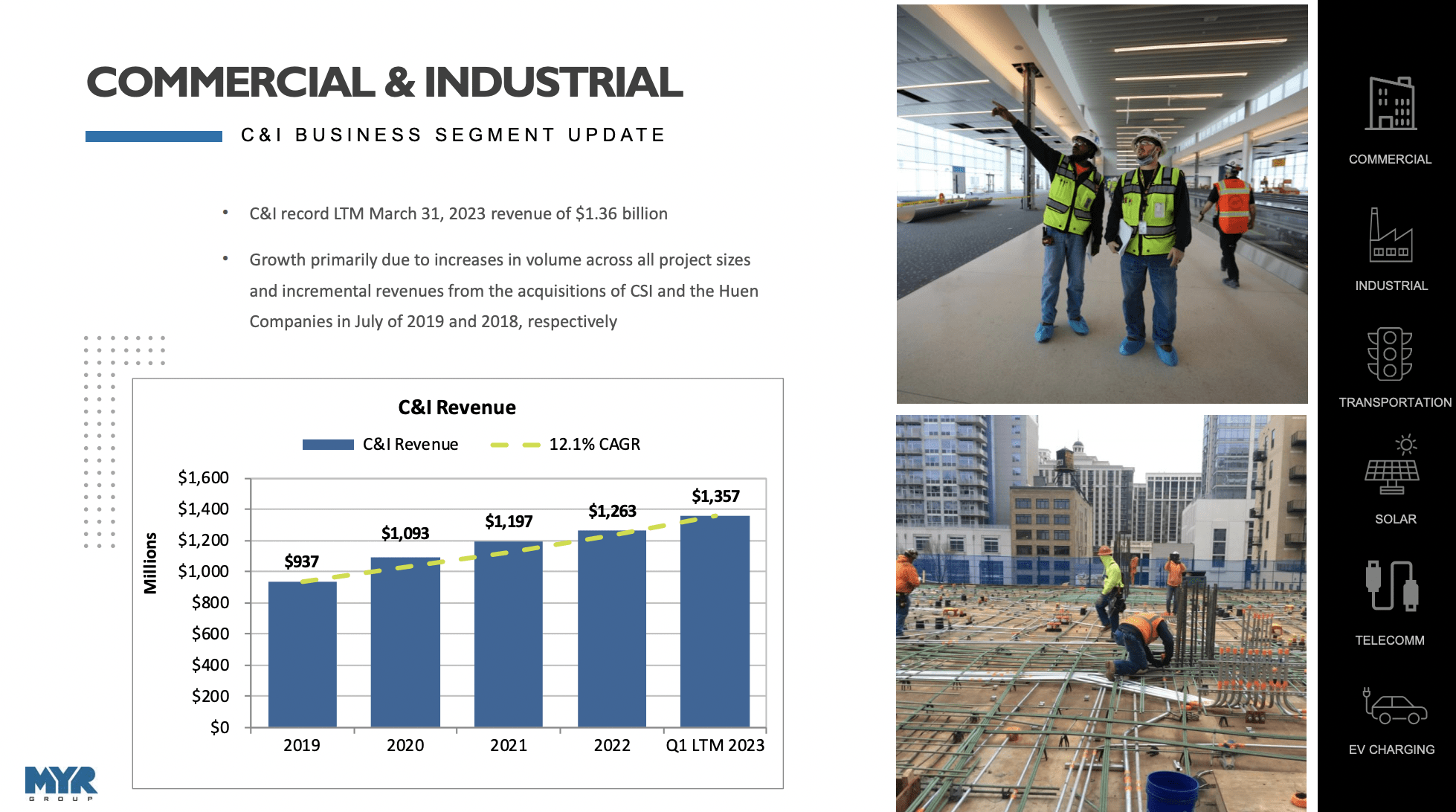

Additionally, as MYR Group continues to grow, its 2 operating segments: Commercial & Industrial (C&I) and Transmission & Distribution (T&D) are shifting in their importance where T&D is growing faster than C&I. This is margin accretive as T&D operating margins are between 6% and 8%, while C&I margins are just 2-5%. This means EPS can get a lift from margin expansion as T&D outpaces C&I. The two images below show the growth in both C&I and T&D, highlighting how T&D is growing faster.

{kind=link}

{kind=link}

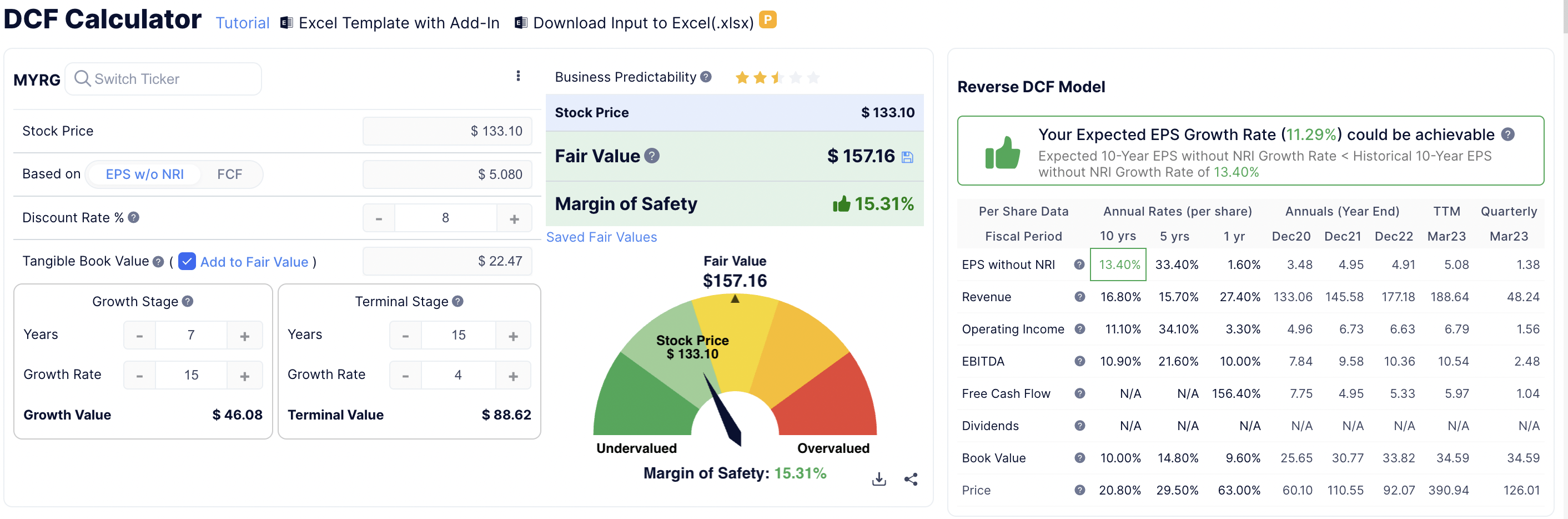

Due to their strong moat and history with some of their subsidiaries in operation for over 100 years, I believe they can continue to grow EPS at a terminal rate of 4% over 15 years. The energy transition will take over a decade to complete and their operations should grow above GDP. At the time of writing this makes MYR Group undervalued by about 15.3%.

{kind=link}

For the DCF calculation, I use EPS as the primary metric for valuation. This is because it accurately represents the profit MYR Group is generating. I added book value to the calculation because MYR Group has substantial investments in fixed assets and those should be included as part of the value. My assumptions assume a slowing in EPS growth compared to the past 3 years as the business scales and it becomes more difficult to grow on a higher base of EPS/revenue. My terminal rate assumes a rate slightly higher than GDP, which can be driven by maintenance work and accretive buybacks. In fact, half of MYR Group's T&D revenue is through Master Service Agreements, which represent long-term maintenance agreements and provide a recurring source of revenue.

Risks

I will now discuss a few key risks to my thesis that MYR Group would make for a good long-term investment. I recognize that MYR Group is currently trading at an expensive P/E with a TTM P/E of 26. This is a sizable premium to the broader market, to small/mid-caps in general, and to MYR Group's history. This means MYR Group has to execute and grow revenue/EPS at high rates to sustain such a valuation. Any slowdowns or erosions in their competitive position would hurt MYR Group's value and stock price.

MYR Group relies on unionized workers at its many subsidiaries and labor disputes could result in loss of revenue and impaired EPS growth, which would affect my thesis.

A slowdown in data center expansion, a pause in funding for grid renewal and roadblocks in fiscal spending for green energy could also result in a slowdown in growth for MYR Group.

MYR Group could also underperform its peer Quanta Services if Quanta Services grows revenue and EPS at higher rates than MYR Group.

Conclusion

MYR Group represents an ideal way to invest in the energy transition as they are key drivers of enhancing green energy usage and renewing the electric grid. They have a long operating history and a strong financial position to take advantage of the billions of dollars in government spending in these key areas. I believe MYRG can continue to grow revenue and EPS at strong above-average rates over the medium to long-term. And while MYR Group's stock is not cheap, their long-term growth trajectory seems well-worth the premium that their stock trades at.

For further details see:

MYR Group: Driving The Energy Transition