MYRG - MYR Group: Solid Fundamentals And Great Growth Trajectory

2023-05-24 08:58:13 ET

Summary

- MYR Group posted yet another solid quarterly results.

- They have a solid growth potential, and their fundamentals are solid.

- But I think the valuation is on the higher side.

- I assign a hold rating on MYRG stock.

MYR Group ( MYRG ) offers electrical construction services in North America. They operate in two segments, commercial and industrial and transmission, and distribution. In the commercial and industrial segment, they offer a range of services like installation and repair of commercial wiring; and signalization for hospitals, hotels, clean energy projects, processing facilities, and management systems. In the transmission and distribution segment, they provide a range of services on substation facilities and electric transmission, like engineering, construction, and maintenance services. MYRG recently announced yet another solid Q1 FY23 result. In this report, I will analyze its quarterly results and discuss its future growth potential. I think its valuation is a little high. Hence I assign a hold rating on MYRG.

Financial Analysis

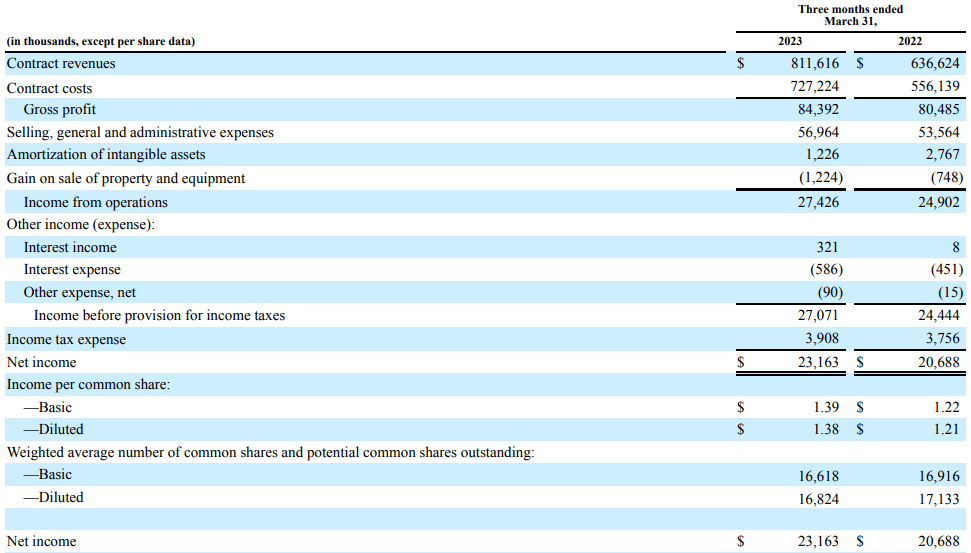

MYRG recently posted its Q1 FY23 results . The revenues for Q1 FY23 were $811.6 million, a rise of 27.5% compared to Q1 FY22. I believe the major reason behind the surge was increased revenue from its transmission and distribution (T&D) and commercial and industrial (C&I) segments. The revenues from the T&D segment rose by 22% in Q1 FY23 compared to Q1 FY22. I believe increased revenues from distribution projects and transmission projects, especially from clean energy, were the main reason behind the rise in revenues in the T&D segment. On the other hand, the revenues from the C&I segment rose by 35% in Q1 FY23 compared to Q1 FY22. Their revenues increased in some geographical areas like Western Canada, Colorado, New York, and California due to several projects awarded to them, and I think this led to an increase in revenues from the C&I segment.

{kind=link}

The gross margin for Q1 FY23 was 10.4% which was 12.6% in Q1 FY22. I believe higher costs due to inflation and supply chain disruptions were responsible for the decline. But I think the decline in gross margins is not much of an issue because the challenges like supply chain issues and inflation are diminishing, and I think it won't affect them much in the upcoming quarters. The net income for Q1 FY23 was $23.1 million, a rise of 12% compared to Q1 FY22. Apart from the decline in gross margins, everything went well for the company. Their financial performance was solid this quarter; their revenues and net income grew well.

Technical Analysis

{kind=link}

MYRG is trading at the $133.6 level. Above is the monthly chart of the company. It is on an uptrend and has risen more than 45% since January 2023, thanks to the terrific results posted by them in the last two quarters. But the stock has risen significantly in the last four months, and generally, when a stock rises so fast, there is a high chance that we might see profit booking in the stock, and due to this, we might see a slight correction in the stock. Hence I would advise not to invest at such a high price. In February, the stock broke out of its then-all-time high of $120, and when a stock gives a breakout, it returns to test the breakout level. So, in my opinion, when the stock comes back to test the level of $120, that will be the best time to invest. So I think one should wait for the right opportunity to buy the stock.

Should One Invest In MYRG?

By the end of Q1 FY23, their T&D and C&I segments had a backlog of $1.28 billion and $1.39 billion, respectively, which makes it a total of $2.67 billion which is 11% higher than Q1 FY22. Their record backlog is a positive sign. In addition, their free cash flow increased by 157% to $18 million in Q1 FY23 compared to Q1 FY22. Their long-term debt has also reduced to $20.4 million, which was $35.4 million in Q1 FY22. This indicates how strong their balance sheet is. After having a terrific FY22, they are off to a solid start; they performed well in Q1 FY23, and maintaining the solid growth rate throughout FY23 will be challenging. But I believe some factors will help them in FY23. The Solar Energy Industries Association has released an insight report that states a 41% growth in solar installations in 2023. So I think solar installation projects and the clean energy market will be a key revenue drivers for them in 2023. In addition, their diversified business makes them immune from certain market failures.

They have a strong balance sheet, solid business, and solid future growth potential. So, I believe every pullback and correction will be a great investment opportunity. So MYRG should be on your radar because it can provide solid long-term gains.

Talking about its valuations. MYRG has a PEG ((FWD)) ratio of 1.55x compared to the sector ratio of 1.54x and has an EV / EBIT ((FWD)) ratio of 16.94x compared to the sector ratio of 14.74x. So after looking at both ratios, I think the valuation is a little on the higher side.

{kind=link}

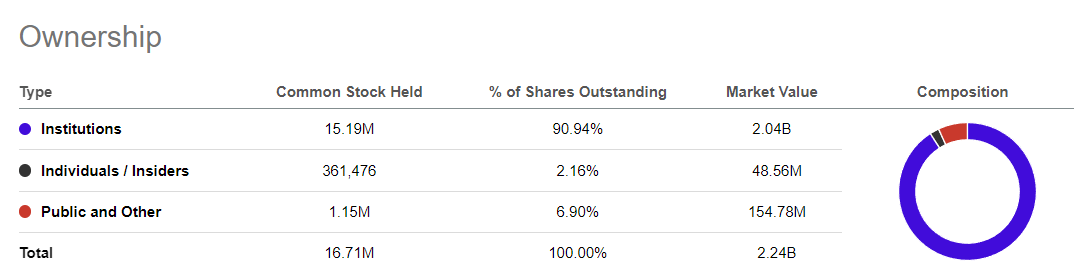

The fact that institutions own 90.9% of the shares of MYRG is an encouraging sign, and I believe that this might be the cause of the company's share price swings becoming less volatile. In addition, the management has announced a new $75 million share buyback, another positive sign showing the management's confidence in their company.

Risk

Although the clients' industries' spending habits generally determine their revenues, the T&D segment, in particular, might be vulnerable to seasonal swings in sales and operations results. These changes, which can greatly impact the company's gross margins, are determined by the weather, the length of the day, client spending habits, the available system outages from utilities, and holidays. Because work undertaken during these times may be constrained and more expensive to finish, their profitability may decline throughout the winter and during severe weather. Additionally, during the summer, when consumer demand for power is at its highest, their T&D customers frequently cannot withdraw their T&D lines from service, which delays the need for maintenance and repair services. Additionally, their work is done in various environments, such as sites that may have been exposed to dangerous and harsh conditions, difficult site conditions, and large urban centers where delivery of materials and labor availability may be impacted. The seasonality of its operation has an impact on its working capital requirements as well.

Bottom Line

It performed well in Q1 FY23, and its balance sheet looks strong; looking at its diverse business, I believe it might continue to perform well financially throughout FY23. I believe every pullback in the stock will be a great buying opportunity. But I think the valuation is a little high at the moment, and the share price is near its all-time high. I expect there might be profit booking in the stock, so we might see a correction in the stock. Hence I would advise waiting for the correction, buying the dips, and holding the stock for the long term. I assign a hold rating on MYRG.

For further details see:

MYR Group: Solid Fundamentals And Great Growth Trajectory