MYTE - MYT Netherlands: Pressure On Profitability Continues

2023-10-10 08:25:43 ET

Summary

- The company's revenue increased by 16.5% YoY, while the operating loss (% of revenue) reached 1.1%.

- A decrease in gross profit margin due to investments in prices and a decrease in economies of scale continues to have a negative impact on operating profitability.

- My recommendation is Hold because I expect margin pressure to continue in the coming quarters while I don't see additional growth catalysts.

Introduction

Shares of MYT Netherlands (MYTE) have fallen 64% YTD. Despite the fact that the company continues to show GMV growth across all geographies, and the company's shares are priced relatively inexpensively based on multiples, I believe that this is still not the best time to open long positions. In my article, I would like to analyze current financial trends and share my expectations about future financial results.

Investment thesis

While revenue growth continues to be in positive territory amid consumer pressure from macro headwinds, I believe the company will not be able to demonstrate meaningful improvement in operating margins in the coming quarters that could act as a catalyst/driver for the stock. First, I don't think we'll see support for unit economics from increased economies of scale because management expects, in my personal opinion, modest revenue growth. Secondly, the effect from the launch of a new distribution center will only be in the second half of 2024 (fiscal).

Company overview

MYT Netherlands is the parent company of Mytheresa Group, which operates an e-commerce platform for selling items in the luxury segment (shoes, bags, accessories). The company's platform features brands such as Gucci, Loro Piana, Prada, etc. The company delivers to more than 130 countries.

4Q 2023 (fiscal) earnings review

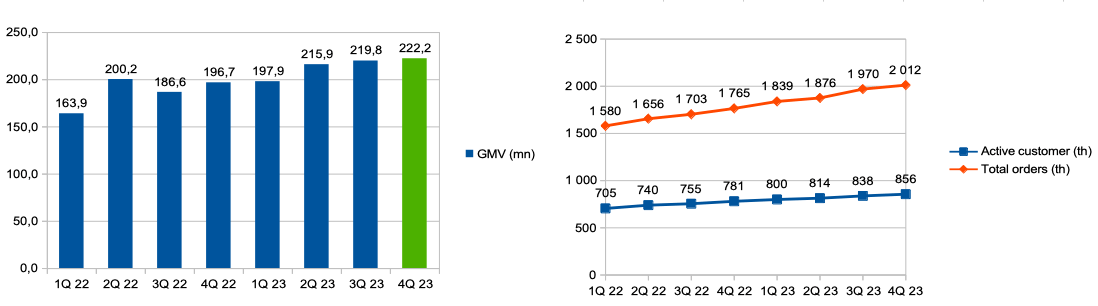

The company's GMV (gross merchandise value) increased by 13% YoY due to an increase in the number of orders by 14% YoY and the number of active customers by 9.6% YoY, while the average order value showed an increase of 4.5% YoY.

GMV and active customer & orders (Company's information)

{kind=link}

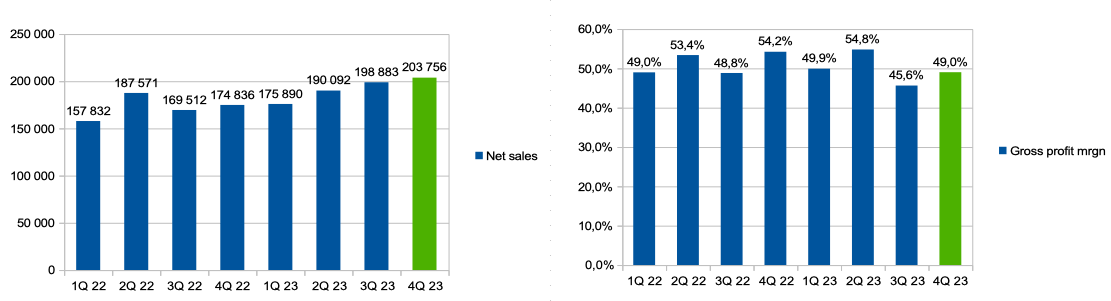

Thus, the company's revenue increased by 16.5% YoY. Gross profit margin decreased from 54.2% in the 4th quarter of 2022 (fiscal) to 49% in the 4th quarter of 2023 (fiscal) due to investments in prices.

Revenue and gross profit margin (Company's information)

{kind=link}

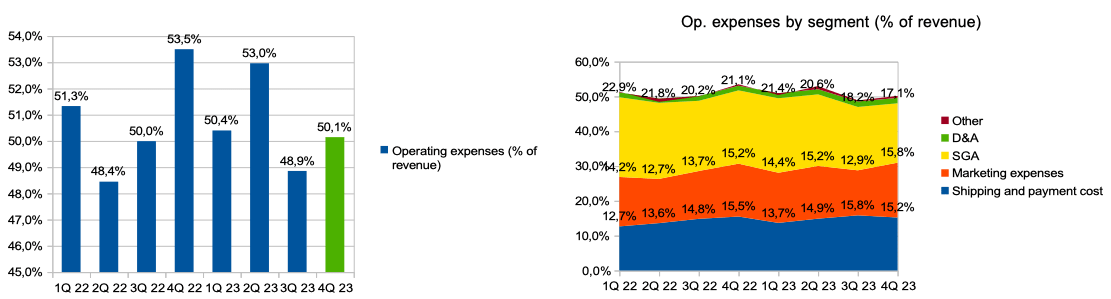

Operating expenses (% of revenue) decreased from 53.5% in the 4th quarter of 2022 (fiscal) to 50.1% in the 4th quarter of 2023 (fiscal). The greatest contribution to the reduction in operating expenses was made by expenses for SGA, which decreased (% of revenue) from 21.1% to 17.1%.

Op. expenses (% of revenue) and op. expenses by segment (% of revenue) (Company's information)

{kind=link}

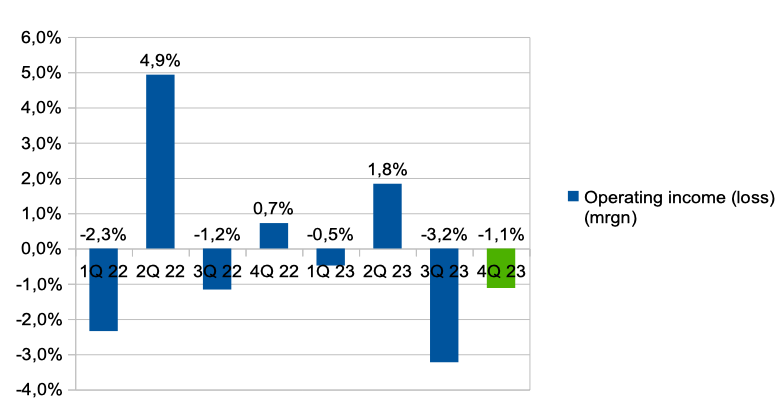

Thus, the operating loss (% of revenue) reached 1.1%, while in the 4th quarter of 2022 (fiscal) the company demonstrated a positive operating margin of 0.7%.

Operating income (loss) margin (Company's information)

{kind=link}

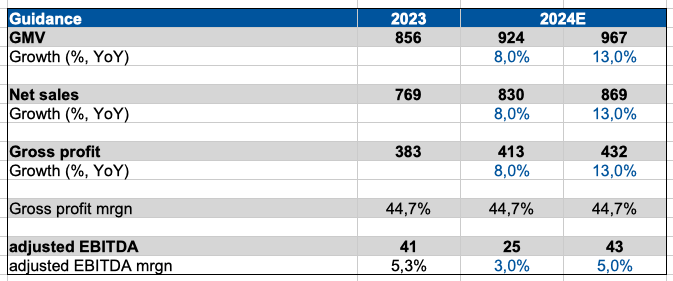

In addition, the company provided guidance for 2024 (fiscal). Thus, management expects that the growth rate of GMV and revenue will be about 8%-13%, while the adjusted EBITDA margin may decrease to 3%-5%. You can see the details in the graph below.

Guidance 2024 (fiscal) (Company's information)

{kind=link}

My expectations

Although the company operates in the luxury segment, where consumers are less sensitive to price changes, the company's management expects that the revenue growth rate in 2024 (fiscal) will be about 8%-13%, which in my personal opinion is a rather modest growth rate, especially in conditions of high inflation.

However, I would like to draw attention to the company's ability to demonstrate improved financial performance. I believe operating profit will continue to be under pressure in the coming quarters due to the following factors. Firstly, based on management guidance , we can conclude that the gross profit margin level will continue to be at a stable level. I believe this is due to the need to continue to invest in prices in the face of high inventory levels in the industry.

Our focus remains on growing the absolute gross profit figure and for fiscal year '24 we expect gross profit to also grow 8% to 13% in line with top line growth.

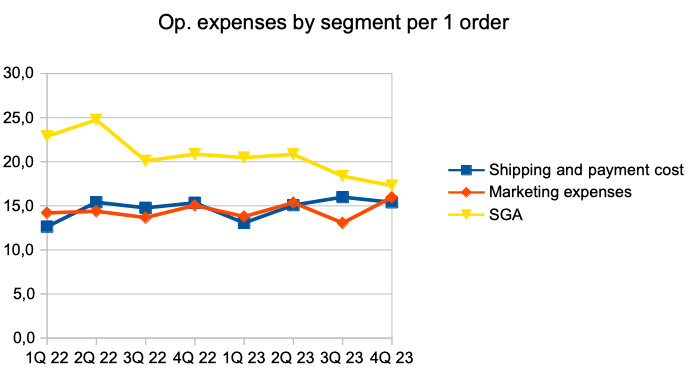

Secondly, low growth rates do not allow the leverage effect to be used in view of the growth in business scale, because a high part of operating expenses (rent, salaries, logistics) is fixed. So, if we look at the dynamics of the main operating expenses per order, we will see that the company is making improvements in the SGA expenses segment, while shipping and marketing expenses continue to be at a stable level.

Op. expenses by segment per 1 order (Company's information)

{kind=link}

Separately, I would like to note that the company recently launched a new distribution center, which should help reduce and optimize logistics costs, but the effect of the launch will be realized no earlier than in the second half of 2024 (fiscal).

Already in the second half of fiscal year 2024, we should see the positive impact of the new facility on our business. All the milestones mentioned will further increase the high cost variability in our business model.

Risks

Margin: rising operating costs due to high inflation and declining economies of scale may put pressure on the operating profitability of the business.

Competition: increased competition may lead to the need for additional investments in prices and increased marketing costs, which can contribute to a decrease in both the company's revenue and market share, as well as profitability levels.

FX: unfavourable changes in foreign exchange rates may result in additional negative pressure on revenue in euro terms.

Valuation

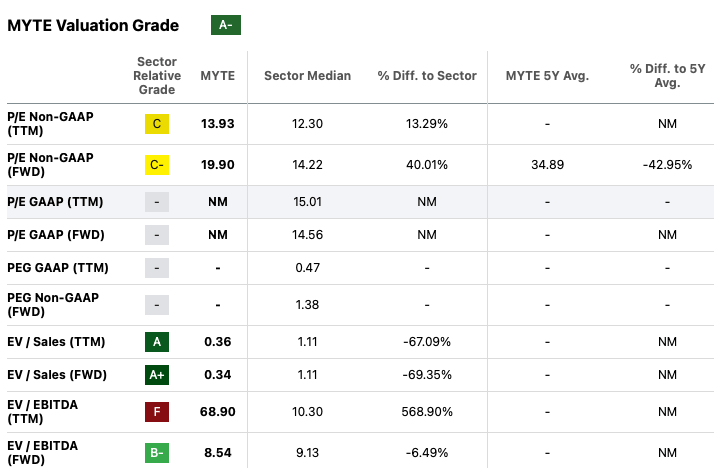

Valuation Grade is A- In accordance with the EV/Sales ((FWD)) and EV/EBITDA ((FWD)) multiples, the company is trading at 0.34x and 8.5x, which implies a discount to the sector median of about 70% and 6. 5% accordingly. I believe that investors should not decide to buy shares based solely on relatively low valuations based on multiples, as the stock price may continue to be under pressure in the absence of growth catalysts. Additionally, I think the company deserves a discount to its valuation given its relatively low revenue growth and business size.

{kind=link}

Conclusion

Thus, at the moment my recommendation is hold. I expect revenue growth to continue to be modest in the coming quarters, while I don't see the potential for meaningful improvement in business margins. I would be happy to change my recommendation to buy if I see signs of faster revenue growth and improved unit economics.

For further details see:

MYT Netherlands: Pressure On Profitability Continues