NAC - NAC: Betting On A Fed Pivot

2023-11-20 17:04:06 ET

Summary

- The Nuveen California Quality Municipal Income Fund is a closed-end fund trading at a discount to net asset values of around 13.88%.

- The NAC fund focuses on municipal securities in California, which are typically not taxed like regular income in California or by the federal government.

- The fund has a high leverage ratio and interest rate risk, but activist funds on the shareholder record may help narrow the discount to net asset value.

The Nuveen California Quality Municipal Income Fund ( NAC ) is a $1.5 billion closed-end fund, or CEF, trading at a discount to net asset values of around 13.88%. The fund focuses on municipal securities in California. These are typically not taxed like regular income in California or by the federal government. I could be mistaken here; I'm neither a tax specialist nor a U.S. citizen.

For what it is worth, this fund picks loans that are considered fairly safe, as judged by well-known financial rating agencies like Moody's and Standard & Poor's. The loans it chooses usually have a long time before they need to be paid back - on average, about 21 years. One risk it introduces is duration or interest rate sensitivity.

I've taken a snapshot of the portfolio of Morningstar to give you a glimpse of the kinds of debt of various Californian institutions the fund owns.

Top holdings NAC (Morningstar)

These generally have very solid credit ratings.

credit quality NAC (Morningstar)

For some perspective, the highest discount among U.S. traded and U.S.-focused municipal bond funds is 15.34%. There is one trading at a premium of 2.8%. On average, the discount is 11.67%. The average discount of all closed-end funds (that trade at a discount) is 11.45%.

In my opinion, this is a very steep discount for a closed-end bond fund. Municipal bond funds rarely (if ever) traded at such discounts a few years back. However, several interest rate hikes wreaked havoc even in treasury markets. This is a leveraged fund with a current effective leverage ratio of 43%. The fund has a lot of interest rate risk (leverage-adjusted duration of 16.49). It didn't fare too well since the end of '21, but given the leverage, it is a miracle it didn't do worse.

I imagine investors who owned this, believing they held a stable fixed-income vehicle, were quite surprised at the volatility and speed of the decline in price and net asset value.

As people started throwing in the towel, this was further exacerbated. Without as many buyers ready to step in, the discount to net asset value had to widen to attract sufficient arbitrageurs to start propping it back up.

In this case, there are now several activist funds on the shareholder record (I found it through Saba Capital's 13-f) but at least Logan Stone Capital and RiverNorth Capital are closed-end fund specialists, if not activists.

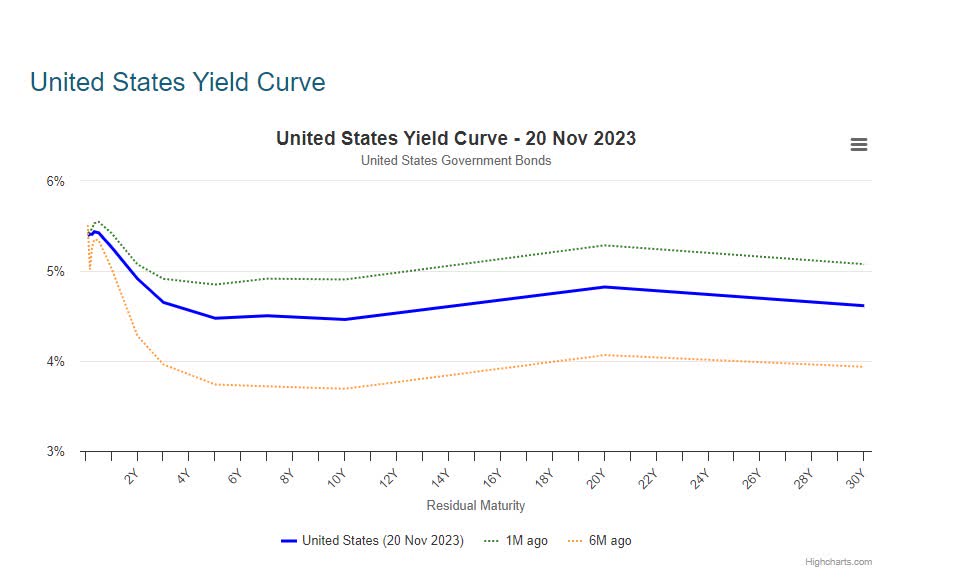

That's great because the fund is already raising its distribution, which is now ~5.04%. That's not fantastic, given where treasuries are:

US yield curve (worldgovernmentbonds.com)

{kind=link}

At 20 years of duration (slightly further out), these currently yield 5.4%.

Some careful monitoring of the leverage employed would be great, too. Often it makes sense to borrow short and invest in the long end, as this fund is essentially doing. With this flat yield curve, it doesn't make much sense to run 40% leverage. I get that if they buy newly issued bonds, these will trade at a premium to what they're borrowing at. However, the annualized leverage cost of 4.53% isn't covered by the average portfolio coupon of 4.15%. Note that it is covered by the market distribution rate, which you could view as a better proxy for what the fund's "cash flow" really is because they have several zero coupon bonds as well, and these benefit from relentless upward gravity towards par but never yield.

A last remark about the leverage being used, the fund is using Variable Rate Preferred or VRP and Variable Rate Remarketed Preferred or VRRPs, and both have floating rates. These move up with interest rates. Having said that, this effect should be reflected in the leverage-adjusted duration statistic the fund publishes and which I cited earlier.

With this fund, I see a big bet that rates will reverse back down or the curve will invert. Then they're dancing around that, picking excellent municipal bonds. But if rates on the long end rise over the coming year, this fund is in a world of pain again; if they come down (as in the last week or two), the fund should do very well.

This fund could be interesting if you want to make a long-duration bet. If you believe in a recession or long rates being too high, you get a levered bond portfolio at a discount to net asset value. That's not a bet I want to make, and if I add this fund to my portfolio, I'd likely hedge the duration risk by shorting TLT against it or a yield or 30-year bond future. I'd be mainly interested to profit from the discount to net asset value narrowing.

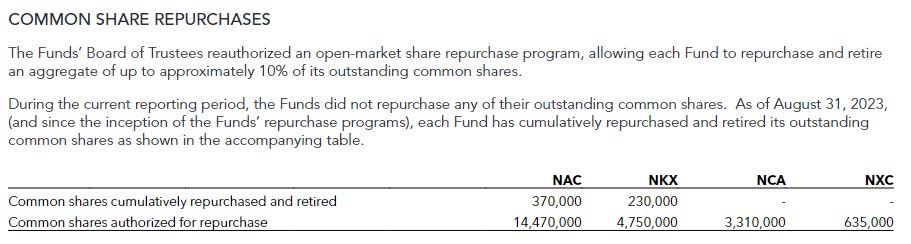

For that to happen, it would be great to see a tender offer or liquidation so investors could get some of their money back. The fund does have authorization to do buybacks in place, but it only bought back a negligible amount of shares:

{kind=link}

It is time to step up purchases aggressively. I don't know what newly issued California muni bonds yield... But by buying back their shares at a 13.8% discount, they're picking up a 16% return immediately while picking up a ~5% yielding diversified package of securities that trade slightly below par themselves.

Conclusion

Nuveen California Quality Municipal Income Fund could work well for investors looking for a long-duration bet. It has floating rate leverage; it trades at a significant discount to the net asset value. Muni funds don't often trade at these discounts. The presence of Saba and other closed-end fund specialists will help to increase the odds the fund will work to narrow the discount to net asset value and not get too complacent about its leverage position. This significantly ups the odds of a more robust buyback effort or a future tender offer.

For further details see:

NAC: Betting On A Fed Pivot