NC - NACCO Industries: A Low Valuation That Seems Justified

2023-06-29 09:44:25 ET

Summary

- NACCO Industries faces severe difficulties in maintaining margins due to increased costs and operational inefficiencies at its mines.

- The outlook for coal is disappointing, with prices expected to fall by 3% YoY, affecting NC's earnings potential.

- Investors should consider other coal companies like Alpha Metallurgical Resources for better exposure to the industry.

Investment Summary

The last report from NACCO Industries (NC) showed them experiencing severe difficulties to maintain a strong level of margins. The impact the Mississippi Lignite Mine Company had on the results was significant as the cost per ton sold went up drastically. This was attributable to costs incurred to establish a new mine area. Operational inefficiencies hurt the results as NC had an operating profit of $1.8 million for Q1 2023 compared to $14.9 million in Q1 2022.

The outlook doesn't look incredibly well either as the Falkirk Mine is effectively generating lower earnings as a result of the transition of Coal Creek Station power plant to the new Rainbow Energy plant. These lower earnings are expected to persist between May 2022 and May 2024. Because of these uncertainties regarding earnings, I think it will result in a lower multiple for the company for the foreseeable future, or until they post a major beat resulting in a catalyst for the share price. The significant decrease in coal earnings for 2023 I think constitutes NC being a sell rating right now. There are better coal plays out there, and unfortunately, NC doesn't seem to be one right now.

Disappointing Outlook For Coal

The company had some notes on the outlook for coal in the last report. The coal deliveries are expected to decrease at a modest rate compared to 2022 levels. The ceased deliveries from Sabine, one of the mines is a reason for this negative outlook.

As if the deliveries decrease wasn't enough to harm the outlook, the operating profits, and Segment Adjusted EBITDA are also expected to post a severe decline compared to 2022 numbers. This anticipation also accounts for a $14 million termination payment from a former Falkirks customer.

Industry Challenges (Investor Presentation)

The price of coal doesn't seem that positive either as 2024 expectations are that it will fall by 3% YoY. This would further hurt the earnings potential of NC. Now it is true that we are still heavily relying on coal to fuel our societies. I don't find it very likely we see a significant decline from the 10.8% of energy consumption that comes from coal. We are indeed moving into renewables , but I think the shift won't be fast enough, and if there is a decrease I think it's more likely to come from LNG instead as that is rising at a decent rate.

Quarterly Result

Taking a look at the last report, some notable issues helped ensure that NC would post a disappointing result. The cost of sales was significantly higher as a result of issues at various mines that we discussed above here. Revenues decreased by around 10% YoY and the cost of sales grew by 17.9%. That sort of movement doesn't work out and it brings significant risk for investors as the company is unable to maintain consistency.

Income Statement (Q1 Report)

Besides those issues, it seems that cuts weren't taken across other parts, the selling, general and administrative expenses were largely unchanged on a YoY basis. What I find interesting is the minerals management segment which saw a significant decline of nearly 25%, going from $12.7 million to $8.2 million. The segment makes its revenues from royalties collected by lessees that are selling natural gas, oil, natural gas liquids, and coal which are extracted by third parties. The changing and lower prices of all these commodities were the reason for the decrease, and without any significant catalyst in sight it seems unlikely we will see the same numbers as in Q1 2022 I think.

All in all, the last quarterly report seemed riddled with disappointment as a result of volatile commodity prices and difficulties in maintaining earnings as they are transitioning some mines. I think this negative will unfortunately persist with NC and the multiple will remain suppressed.

Risks

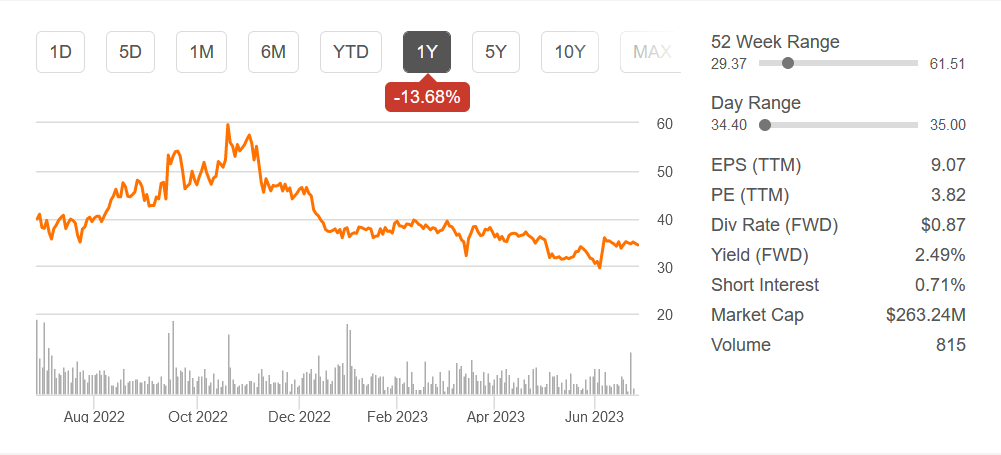

As for risk when looking at NC I think the most prominent one is what has been highlighted in the last report, volatility of prices and cost of sales. That commodity prices shift in price is nothing new and something that investors accept. But when it comes at the same time as the cost of sales rises for a mining company you end up with a very bad quarter. Unfortunately for NC shareholders, this has also resulted in some share dilution over the last few years. Something which has further depressed additional appreciation a position could have potentially made. The stock price is down 1.38% in the last 5 years and hasn't been helped with a yearly dilution of around 1.36%.

Valuation & Wrap Up

As I have mentioned throughout this article, NC had a very bad last quarter as the cost of sales took hold of the results and the share price has had a difficult 2023 so far. I think that coal is here to stay for some time, but investing in NC to get exposure to it seems like one of the worse ways to do so. Instead, I think investors are far better off with a company like Alpha Metallurgical Resources Inc (AMR). The company boasts a lower FWD p/e than NC at just 3.2 . I think the pessimism surrounding coal companies are a big factor in this low multiple. But that means we as investors have a strong opportunity to get in a very attractive price. As far as other measurements go, the company seems likely to post negative cash flows in the coming quarters, as operations are struggling. This means NC is trading at a negative p/fcf, introducing risk to investors. As for the sector, it's valued above where NC is currently, at 8.9 on a forward basis. The FWD valuation is up compared to the TTM valuation, which plays into my thesis that the sector will face some challenges going forward regarding earnings, as 2022 was an exceptional year. Despite NC being valued under the sector, I think the glaring operational issues they have experienced are cause for a lower multiple, and shouldn't be viewed as a value play as a result.

{kind=link}

What you get with AMR as opposed to NC is a company that is doing impressive buybacks and also distributes a decent dividend at around 1% yield. But the main attraction is the buybacks. AMR has announced a $1 billion buyback plan, which would be close to 50% of the entire market cap. This presents strong value potential for shareholders and I view AMR as a better investment than NC right now. To reiterate my rating for NC, I think they are a sell here.

For further details see:

NACCO Industries: A Low Valuation That Seems Justified