NC - NACCO Industries: Significant Upside But Shares Could Become Cheaper

2023-07-18 17:30:16 ET

Summary

- NACCO Industries, Inc. has been given a "Hold" rating due to a benign outlook for energy mineral prices and a growth-oriented business strategy, despite a year-over-year decline in earnings and sales in Q1 2023.

- The company's coal mining, North American mining and mineral management segments are expected to continue providing solid financial foundations, despite some temporary adverse factors.

- Despite expected lower profitability in 2023, NACCO's solid financial position should support the payment of dividends and the company's growth and diversification plans.

A Hold Rating for NACCO Industries, Inc.

This analysis essentially confirms the "Hold" recommendation for shares of the stock in Cleveland, Ohio-based resource company NACCO Industries, Inc. ( NC ) provided in the previous article . The rating was based on analysts' benign outlook for energy mineral prices and a growth-oriented business strategy but with an eye on the ongoing energy transition. The recommendation was not higher than Hold as the stock price was on track to become more attractive despite the catalysts in place. In fact, investors had an opportunity to take advantage of a lower share price after the first-quarter 2023 results showed a year-over-year decline in earnings and sales. However, shares of NACCO Industries have been recovering since early June and are now more in line with the long-term trend.

Those catalysts are still in place, essentially providing a solid financial foundation that helps the company to continue its growth while diversifying the business so it can better respond to the energy transition. This bodes well for the future of NACCO Industries and investors who hold a position in the stock can take advantage of growth opportunities presented by the volatility of the natural resources market. I believe the stock can generate higher returns than many other players in the oil and gas industry specifically, because it is not involved in the production and exploration of those commodities and therefore does not incur the costs of a pure mining company. Shares tend to take this trait into account when trading in my opinion.

Again, this analysis does not result in a higher recommendation rating than Hold, as shares may still become more attractive in the period ahead, as lower commodity prices than the summer 2022 surge are still expected to put some downward pressure on stock prices.

How NACCO Industries Is Performing in the Energy Sector

NACCO Industries operates in the industry through three segments: Coal Mining, North American Mining and Mineral Management.

Coal mining contributes more than 30% to the company's overall profitability, North American mining about 20% and the mineral management division a little less than 50%.

Coal mining currently includes open-pit coal mining techniques, and NACCO supplies the commodity to power generation companies and activated carbon producers under long-term contracts. NACCO serves customers throughout North Dakota, Texas, Mississippi and Louisiana as well as within the Navajo Nation Indian Reservation of northwestern New Mexico.

Activated carbon is required in the performance of a variety of techniques including the purification of liquids such as municipal drinking water and others. To name a few, it is also used in metallurgy for gangue processing during the extraction of precious metals and to control pollutants during industrial processes. This technology is also used to eliminate odors or purify ingredients in the processed food and beverage industry.

NACCO supplied 6.91 million tons of coal in the first quarter of 2023 , trending in a negative way from 7.05 million in the same quarter of 2022, due to the closure of supply operations at a Texas branch serving a power plant until it was dismantled by the owner in March 2023.

Year-over-year, the coal mining segment saw operating income and Adjusted EBITDA decrease 95.7% and 60%, respectively to $313,000 and $4.6 million in the first quarter of 2023. These decreases, while significant, were due to temporary factors. These include costs to set up and search for efficiencies in a new mining area, unusual weather conditions affecting mining, and a $2.4 million write-down of inventories to net realizable value, probably because of lower demand for electricity for industrial use, mainly due to the slowdown in production activities .

There may be a lower need for energy for industrial use as manufacturing companies are currently struggling with a lack of orders and a marked contraction in input buying. This trend affects not only NACCO, it must be noted, but other operators in the industry as well.

Some of these factors are expected to affect the company's profitability for the remainder of 2023 as inefficiency in the new mining area may continue for a few more months. But once efficiency is restored, this should more than offset higher depreciation effects in 2023 and a little beyond due to capital expenditures to develop the new mining area.

It is worth remembering that the dent of lower profitability was also due to lower thermal coal shipments because of the halt in supply to the decommissioned power generator in Texas. But this has been known for over a year and the stock price has since shown both lows and highs.

In 2023, capital expenditures for mine development and equipment replacement are expected to be approximately $12 million. Coal development spending is likely to fall significantly thereafter, prompting the company to focus more on growth by diversifying its business and potentially adding more weight to the energy transition metal such as lithium in its portfolio of operations. Because of this, the company can also have more cash to pay dividends, which will also help to keep the stock price up.

In short, as one can understand, this analysis assumes that the coal business is far from obsolete and will continue to provide cash flow for many years to come.

Although coal is considered one of the largest emitters of atmospheric CO2 among fossil fuels, its use for energy production is not likely to disappear any time soon, and from time-to-time uncertain prospects may make it necessary to resort to the raw material as other forms become too expensive in response to geopolitical tensions. In addition, there are entire communities in the US that depend on the possibility to extract the raw material through the exploitation of the existing mineral deposits. Therefore, for social and political reasons, it is not feasible for the time being to dispense with this raw material and replace it with other, cleaner forms.

The North American Mining segment includes the provision of value-added contract mining and other related services to miners of aggregate for the construction industry and to miners of lithium and other minerals. This segment also provides contract mining services to independent mine and quarry operators in Florida, Texas, Arkansas and Indiana.

Year-over-year, operating income and Adjusted EBITDA for the North American mining segment decreased 34.7% and 1%, respectively to $830,000 and $2.7 million in the first quarter of 2023. While the decline in operating income is expected to continue as Caddo Creek reclamation activities in Texas are no longer taking place as completed last year, adjusted EBITDA should instead benefit from higher depreciation and amortization costs as the company has historically invested significant capital to growth initiatives of the North American mining segment.

Among the various initiatives that are part of this segment, the one that stands out is where NACCO is taking an interest in the lithium business, one of the key metals for the energy transition program, through an exclusive contract for a lithium project in northern Nevada owned by Lithium Americas Corp (LAC). Lithium Americas is a Canadian explorer for lithium resources in the US and Argentina and the company that will process and sell the alkali metal which is a key element in the battery and electric energy accumulators of electric vehicles, photovoltaic technology for solar panels and many other devices.

This lithium project is called the Thacker Pass Project and is expected to produce lithium by 2026. Lithium Nevada will pay NACCO Industries an administrative fee per ton of lithium shipped under a 20-year agreement .

Furthermore, Lithium Americas Corp. will reimburse all costs incurred in building the facility and pay NACCO Industries a construction fee, providing NACCO Industries with a modest revenue stream over the two years through 2026.

The Minerals Management segment leases its royalties and mineral interests to third-party exploration, production and mining companies, which can then explore, develop, produce and sell energy minerals.

Year-over-year, first-quarter 2023 operating income and Adjusted EBITDA for the Minerals Management segment decreased 48% and 43.8%, respectively to $6 million and $6.9 million as prices for oil and natural gas fell back to pre-crisis levels. Raw material volumes were also lower due to the natural decline in production from the existing wells. However, the company continuously engages in investment activities aimed at renewing the activities belonging to the Minerals Management segment. With that in mind, the company expects to spend around $21 million in 2023, or about 30% of total CapEx.

Although Lower Commodity Prices, Dividends and Business Growth/Diversification Plans Continue

Even if the company's profitability in 2023 will be lower than in the previous year, mainly because this year's business activities will not be able to rely on the raw material prices observed last year due to the energy crisis in Europe, the company still expects a positive cash flow after CapEx of $72 million.

As such, NACCO Industries, Inc. shareholders should have no problem receiving its quarterly dividend of $0.22 per share going forward. This was recently paid out on June 15th and, at the time of writing, translated into a dividend yield [FWD] of 2.52% (vs. S&P 500's yield of 1.52% ). The company has been paying dividends quite consistently for 36 years and increasing them for 9 years, and in the meantime, the profitability of operations has fluctuated due to the volatile price of the commodities covered.

The dividend should be paid out without any problems also due to the very solid financial position, which allows the company to make further progress in the following long-term steps.

The solid financial position will allow NACCO Industries to capitalize on growth opportunities that are considered strong across the minerals management segment as well as mitigation resources in North America.

The company's objective is to build a high-quality, high-return, diversified portfolio of oil and gas minerals and royalty interests in the United States.

But that's not all: NACCO Industries is also striving to become a leading provider of waterway and wetland mitigation services in the US Southeast, a business that is growing given the importance of green issues on the US political agenda.

Focusing on the environmental sustainability of economic activity, NACCO Industries is developing this project, called the Thacker Pass Project, which will provide multi-year contract mining services to lithium miners in northern Nevada. Lithium is a key metal for the energy transition.

Additionally, NACCO Industries' strong balance sheet helps support its projects to increase the efficiency of its coal mining segment, and ongoing projects are expected to make a significant contribution to lowering the cost per ton of coal delivered, beginning in 2024.

The Balance Sheet Is Solid

The financial condition of NACCO Industries appeared strong as of the end of the first quarter of 2023, as the balance sheet had $109.64 million in cash on hand or approximately $14.6 per share, while the debt amounted to $20.4 million.

In addition, the company had the possibility to use a $150 million revolving credit facility, of which it had $117 million remaining to draw.

The latest quarter's debt to 12-month EBITDA ratio is 1.36x, which means that it will take a year and 4 months for the current EBITDA level to pay off all outstanding debt. While the ideal debt-to-EBITDA ratio is not the same for every company as it varies by industry, I believe that a score below 3 generally means the company has a strong credit history, allowing access to additional loan capital if necessary.

NACCO's balance sheet also includes an interest coverage ratio of 6.05, which is calculated as a 12-month operating income of $12.7 million divided by a 12-month interest expense of $2.1 million. This suggests that the company has no trouble paying its financial obligations stemming from its outstanding debt, as investors typically find a figure of at least 1.5x to be ideal.

Finally, the balance sheet has an Altman Z score of 3.32x (scroll down this webpage to the Risk section), indicating safe zones and little chance of bankruptcy within the next few years in my view.

The Altman Z-Score measures the likelihood that a company will face bankruptcy problems, depending on the value it takes on. If the value is less than or equal to 1.8, the balance sheet is in distress zones, which means a high probability of bankruptcy within a few years. When the ratio is between 1.8 and 3, the balance sheet is in a gray area, which still implies a risk of bankruptcy, albeit moderate. While a score of 3 or higher means that the risk of financial insolvency is extremely low or non-existent.

Thus, the decline in the company's profitability is mainly due to raw materials returning to pre-energy crisis levels, so this should not be a cause for concern for investors. Also because it affects every company that is active in the natural resource industry.

Instead, a solid financial position should allow NACCO to confidently pursue projects to expand and diversify its business.

Profitability and cash flow generation depend on commodity price volatility, and it cannot be ruled out that they will peak again, as was the case during the strong recovery from the pandemic crisis or the surge in prices during the energy crisis in Europe. It must be taken into account that due to the much more turbulent international geopolitical environment, the markets can re-purpose almost everything nowadays, and even more frequently than before, which nevertheless represents an opportunity for investors in commodities such as natural resources.

So, the lower earnings recorded in the first quarter of 2023 don't get NACCO into trouble in my view, but the company will continue to be a vehicle for investors who want to participate in the volatility of the fossil fuel markets.

The Valuation of NACCO's Stock

Having rebounded from earnings results for the first quarter of 2023, the stock price is now more in line with the long-term trend but could still be negatively impacted by headwinds from coal, crude oil and natural gas trading significantly lower than a year ago.

This analysis assumes that whenever the stock price forms interesting entry points, this is an opportunity to add to the position.

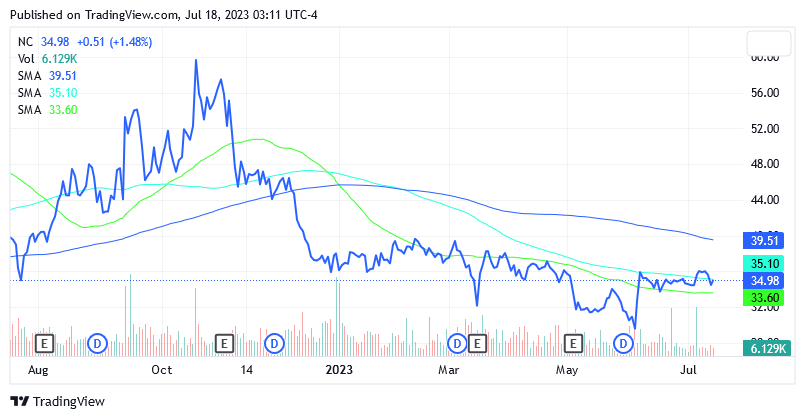

Shares of NACCO Industries, Inc. traded at $34.98 apiece as of this writing giving it a market cap of $258.89 million. Shares are trading significantly below the middle point of $45.44 of the 52-week range of $29.37 to $61.51.

{kind=link}

Shares are also trading slightly above the 50-day simple moving average value of $33.60, almost on par with the 100-day simple moving average value of $35.10 and significantly below the 200-day simple moving average value of $39.51.

Also, NACCO Industries, Inc. stock does not appear expensive compared to its peer group on a price-to-book basis.

In fact, NACCO Industries has a price-book ratio [PB] of 0.60x, vs. Ur-Energy Inc. (URG)'s PB of 2.72x, Hallador Energy Company (HNRG)'s PB of 1.22x, Uranium Royalty Corp. (UROY)'s PB of 1.59x, Fission Uranium Corp. (FCUUF)'s PB of 1.03x and enCore Energy Corp. (EU)'s PB of 1.43x.

NACCO Industries shares could get even cheaper and as such offer an opportunity to gain greater exposure to the price increases analysts at Trading Economics are seeing in coal, crude oil and natural gas prices.

Analogous to what happened after the Federal Reserve hiked interest rates by 25 basis points to the range of 5% to 5.25% on May 3, and in my opinion largely causing shares of NACCO Industries to fall more than 15% and hit an intraday low of $29.37 on June 5, another strong downtrend may follow the next interest rate decision scheduled for July 26.

Source: Seeking Alpha

Rate traders are pointing to a 97.3% chance that the Federal Reserve will hike interest rates by 25 basis points to 5.25-5.5% from the July 26 meeting, which will likely lead to bearish sentiment across US-listed stocks including NACCO, as higher borrowing costs are seen as a threat by investors, suggesting the economy could slip into recession, which could spell bad times for businesses.

The risk that NACCO shares could be affected by the bearish sentiment is not very high, but it is significant as suggested by the 24-month beta of 0.62x which means NACCO will fall as US-listed stocks trade lower but less intensely.

However, analysts at Trading Economics predict that natural gas, crude oil, and coal will finish higher a year from now, meaning that if NACCO becomes significantly cheaper after the July 26 Fed hike, it has greater potential for a strong upside with higher commodities.

As of this writing, analysts at Trading Economics forecast that in 12 months' time, natural gas will trade at $3.26 from the current $2.56 per Metric Million British Thermal Unit. They forecast that crude oil will trade at $84.82 per barrel from the current price of $74.28, and that coal will trade at $150.44 per metric ton from the current price of $131.10 per MT.

Conclusion

This article reiterates a Hold rating on NACCO Industries, Inc.

The stock represents a commodity company that is pursuing a growth/diversification strategy of its business thanks to prudent management and a solid financial position. The stock offers a solid solution to benefit from the volatility in commodities in my view.

Profitability and cash flow have declined recently as energy commodity prices have fallen from their highs during the energy crisis. This is normal for a company whose business is exposed to the volatility of these markets and indeed affects every company in the industry.

Shares of NACCO could get cheaper after the Fed's interest rate decision scheduled for July 26, adding upside potential as I believe fossil fuels to trade higher in the coming months.

For further details see:

NACCO Industries: Significant Upside, But Shares Could Become Cheaper