PAI - NAD And PAI: Choosing Quality

2023-03-20 17:47:39 ET

Summary

- NAD is a leveraged municipal bond fund emphasizing higher credit quality.

- PAI is a non-leveraged fund focused on investment-grade corporate bonds.

- Both funds are trading at significant discounts to their net asset values, presenting a potential opportunity.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on March 19th, 2023.

With a recent uptick in volatility in the market, investors could be looking more toward safety and quality. Nuveen Quality Municipal Income Fund ( NAD ) and Western Asset Investment Grade Income Fund ( PAI ) could be potential options in that space.

NAD is a municipal-focused bond fund but is highly leveraged, which increases risks. On the other hand, PAI invests in corporate bonds that might not be as safe or as high up on the credit quality scale, but it's balanced out by being a non-leveraged fund. Non-leveraged closed-end funds are rare, with most CEFs often incorporating leverage.

Both are trading at sizeable discounts, deeper than their longer-term averages, which could present a potential opportunity to consider either fund. With anything, there are pros and cons, so I hope to outline those in this article. Despite being funds with different fixed-income focuses, they actually have several broader similarities with the current environment.

The Basics

NAD

- 1-Year Z-score: -1.32

- Discount: -11.67%

- Distribution Yield: 4.12%

- Expense Ratio: 0.98%

- Leverage: 38.99%

- Managed Assets: $2.99 billion

- Structure: Perpetual

NAD's investment objective is "to provide current income exempt from regular federal income tax and to enhance portfolio value." They'll attempt to achieve this through investing "in municipal securities that are exempt from federal income taxes. The Fund uses leverage. By investment policy, the Fund may invest up to 35% of its managed assets in municipal securities rated at the time of investment BBB and below or judged by the manager to be of comparable quality."

The fund incorporates leverage while attempting to achieve its objectives. Similar to most muni funds, it's in a rather elevated amount. That increases the upside but also the downside when things are going wrong. It also means a higher expense ratio; the total comes to 2.62% when including leverage expenses. The fund's leverage is through variable-rate debt, meaning costs will rise as interest rates rise.

NAD Capital Structure (Nuveen)

PAI

- 1-Year Z-score: -1.29

- Discount: -8.03%

- Distribution Yield: 4.77%

- Expense Ratio: 0.77%

- Leverage: N/A

- Managed Assets: $120.58 million

- Structure: Perpetual

PAI's investment objective is "a high level of current income, along with capital appreciation." To achieve this, the fund "provides a portfolio of primarily investment grade debt, including government securities, bank debt, commercial paper, and cash/cash equivalents." They "emphasize team management and extensive credit research expertise to identify attractively priced securities."

Unlike NAD and most other closed-end funds, PAI is non-leveraged. That allows the fund's expense ratio to seem quite low, and they appear not to gouge a hefty management fee too. That's despite the fund being quite small. In fact, the 0.77% is similar to the average actively managed ETF expense ratio.

Performance And Discounts

Both funds have had substantial losses in the last year due to rising interest rates. So at first glance, they wouldn't look safe at all.

That might be true if one still expects the Fed to raise interest rates aggressively going forward. Given the latest bank failures and inflation continuing to trend lower (while admittedly still too elevated,) I suspect we are much closer to the end than the beginning of interest rate hikes.

It wasn't these funds simply dropping while everything else was fine; it was because investment-grade bonds and even munis lost ground in the last year. Below we can see a comparison of iShares iBoxx $ Investment Grade Corp Bond ETF ( LQD ) and iShares National Muni Bond ETF ( MUB ).

Ycharts

MUB actually performed quite well on a relative basis. NAD detracted from this barometer for munis significantly, which could be for several factors. Both have higher relative expense ratios compared to these ETFs. Additionally, portfolio positioning and NAD carrying a sizeable amount of leverage would have seen the losses amplified.

However, I believe this reflects yet another point on why NAD and PAI are actually more similar than they might first appear. At least in the last year, they almost synced up perfectly in their performance. The big difference was on a total share price basis, where NAD experienced the larger losses to a material degree.

What might be even more interesting to note is that it isn't only the last year that these funds have synced up in performance. Here's a look at the last decade of performance between these funds.

Ycharts

It is nearly identical, yet one is a muni bond, and one is invested in corporate bonds. In terms of tax benefits, NAD would clearly win out due to the portion of the distribution that is tax-free, but we'll discuss that more in the distributions section.

Before the Fed was raising interest rates, I was putting a particular focus on screening for senior loan funds:

- Closed-End Funds: Senior Loan Funds Q1 2022 Update

- Closed-End Funds: Senior Loan Funds Q4 2021 Update

- Closed-End Funds: Senior Loan Funds Q3 2021 Update

- Closed-End Funds: Senior Loan Funds Revisited (posted April 1st, 2021.)

- Income Lab Ideas: Senior Loan Funds (posted January 3rd, 2021.)

Going forward, a recession could see the Fed cutting interest rates which would cause a rally in the underlying bond holdings. While that isn't a guarantee, even a pause from the Fed raising interest rates should see these funds stabilize going forward. Additionally, being higher quality bonds should bode well in terms of defaults and bankruptcy impacts being fairly limited relative to high-yield or junk bonds.

For the reasons above, I think adding a bit of higher-quality debt could make some sense as a bit of a hedge. I keep most of my portfolio invested in CEFs I'd look to hold forever. However, I snuck some extra senior loan funds in as a bit of a hedge last year. It worked out mostly as Invesco Senior Income ( VVR ), and BlackRock Floating Rate Income Strategies ( FRA ) improved significantly in 2022.

I have sold VVR at this point but continue to hold FRA due to a sizeable discount. Unfortunately, at this point, it looks like it could be turning into a mistake to hang on to FRA. Had one shifted from senior loan funds to higher-quality bonds, they would have experienced a smaller decline in the last couple of weeks.

Ycharts

But this highlights why trying to time markets, including trying to utilize hedges, is incredibly difficult. At least, I'm not smart enough. Perhaps it's better I can admit that than try to pretend the contrary is true; thus, why I'm always putting a heavy emphasis on discounts (relative and absolute) and being diversified. Up until just a couple of weeks ago, the discussion was centered around interest rates going higher than we originally expected. Now there is talk of one more 25 basis point hike and pause or even cuts. Yet, inflation remains elevated. So we can see how quickly the environment can change. Should the Fed need to reverse course and raise higher than expected again, higher-quality debt will suffer again.

Anyway, back to NAD and PAI. In terms of their discounts, any discount narrowing that these funds could experience could help make the fund's total share price performance outpace the underlying portfolio. Both of these funds are trading at discounts wider than the average in the last decade. PAI, in particular, looks interesting as the fund has experienced trading at premium levels throughout the years.

Ycharts

Good News, Bad News On Distributions

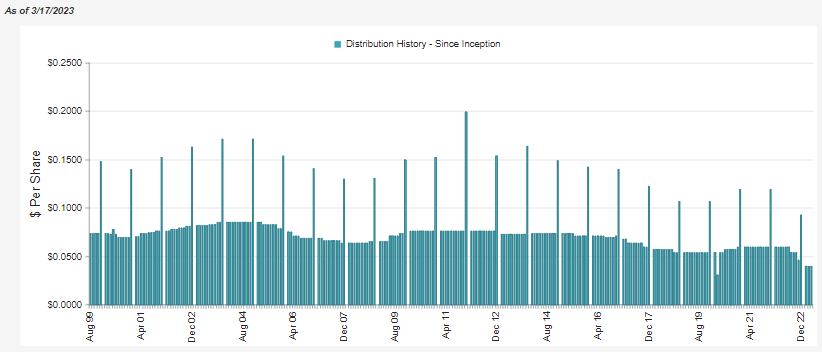

With the fund's distributions, there is some good and bad news. Some of the good news is that PAI is covering its distribution according to its last report. Since the fund isn't leveraged, they shouldn't be experiencing any squeezing of the spread between their borrowings and what their underlying portfolio is earning. All else being equal, coverage should remain strong going forward unless we start seeing defaults.

{kind=link}

For this reason, I expect the fund's current distribution to continue at the current level.

{kind=link}

Some bad news is that NAD is not covering its distribution. Rising leverage costs should continue to see the fund's spread between what it costs to borrow and what the underlying portfolio can earn being squeezed. This report is for the fiscal year-end 2022, which ends in October. So we would have seen rates rise even further since then.

NAD Annual Report (Nuveen)

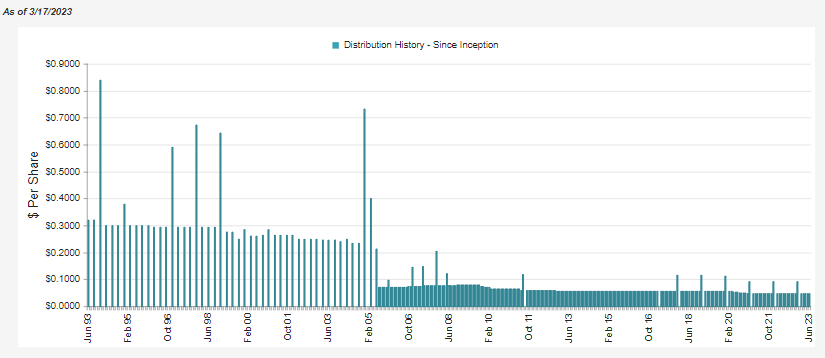

For this reason, we've already seen the fund cutting its distribution several times in material amounts. We are now at an all-time low in monthly distributions for the fund.

{kind=link}

Some good news here is that if rates stabilize or are cut going forward, these costs will start to reverse. With cuts already taking place, the amount being paid out going forward is also already reduced relative to that last report.

Additionally, the most significant benefit of NAD is the tax-free status of the fund's distributions. Thanks to being invested in municipal bonds, the overwhelming majority of the distribution is tax-exempt income.

Depending on your state, some of the distribution will be tax-free for the state too. Though it's a national muni fund, that won't be a benefit to everyone, and for those it is, it can be a relatively small amount.

{kind=link}

Still, this means the higher your income bracket, the larger the taxable equivalent yield. So the 4.12% distribution rate currently isn't necessarily reflective of your net distribution yield. In fact, that could mean that the distribution yield for NAD is over PAI's at 4.77%. PAI is giving you good old-fashioned ordinary income that is taxed at the highest rates.

{kind=link}

However, this brings up the next point of more "bad" news or at least not beneficial. Right now, risk-free U.S. Treasuries are yielding above both of these levels. Again, with NAD, the taxable equivalent yield could still eclipse Treasuries. For PAI, though, the main benefit would appear to come from the fund's discount and having the active management of Western Asset.

Portfolio Exposure

NAD

For NAD, they are heaviest in A or higher rated debt. They carry some below investment-grade munis, but it is very limited.

NAD Credit Quality (Nuveen)

The portfolio is spread out amongst several different states, meaning no overly significant weighting in any particular state. That type of diversification can help the fund if different regions of the U.S. experience different depths in a possible recession.

NAD Top State Exposure (Nuveen)

In addition to this, the fund carries 1232 holdings. The largest weighting for the top position is tied with four different positions representing 0.7% of the fund's portfolio.

{kind=link}

The average leverage-adjusted effective duration of the portfolio is 14.18 years. That's really no surprise when considering muni bonds are issued with long maturities. For NAD, the effective maturity is 18.21 years. That's why we've seen the portfolio perform so weakly, as interest rates were rising rapidly.

However, another benefit here is that besides the fund's discount, the fund's average bond price as a percentage of par comes to $92.98.

PAI

PAI is invested the most in BBB rated debt, but single A also represents a healthy chunk of the portfolio.

PAI Portfolio Credit Quality (Western Assets)

As mentioned before, while that might mean on the surface that PAI could be considered riskier, that would be ignoring the high amount of leverage NAD utilizes. As we saw above, the actual results of the funds were nearly identical, excluding tax considerations.

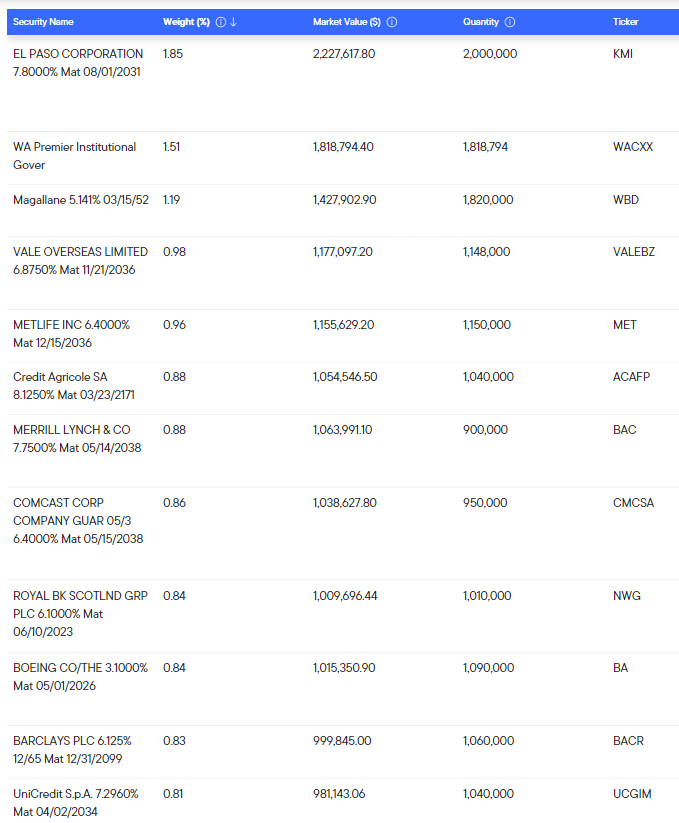

The largest sector for PAI is banking, followed by energy.

PAI Sector Exposure (Western Assets)

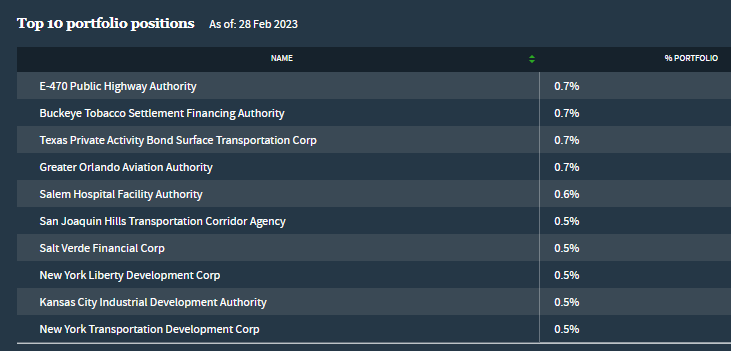

Banking is certainly not something one might want to see now. However, none of the largest banking sector holdings are related to the banks currently struggling. The top ten exposure represent larger weightings relative to NAV, but the fund still carries a sizeable number of holdings at 429.

{kind=link}

The weighted average life of the fund is 12.34 years, with the effective duration coming down to 7.32 years. This is quite incredible, given the nearly identical total NAV return performance in the last year amidst the rapidly rising interest rates. All else being equal, NAD should have fallen significantly further if interest rate risks were the only factor in bond prices.

Conclusion

Overall, historical performance isn't pretty, with a particularly large hit in the last year due to significantly rising interest rates. However, it's about what performance could be going forward. Sticking with higher-quality holdings heading into a potential recession could be beneficial.

Additionally, the Fed is probably much nearer to the end of raising rates than the beginning. The pressures of those increases should be letting off now. This is particularly true with the bank failures as of late. If the Fed cuts rates during a potential recession, the underlying portfolios on these funds could rise and produce capital gains for these funds. At the very least, these funds should stabilize if we see a pause in rate hikes.

The yields on these funds are only merely competitive with the risk-free U.S. Treasuries. That could be seen as a negative, but at the same time, you can pick these funds up at discounts. For NAD, you are also looking at mostly tax-free distributions, which means the taxable equivalent yield could materially exceed that of U.S. Treasuries. The higher your tax bracket, the higher the benefit.

For further details see:

NAD And PAI: Choosing Quality