NDAQ - Nasdaq: 4 Reasons To Buy This Otherwise Overvalued Company

2023-07-13 16:20:49 ET

Summary

- Nasdaq gets a buy rating today.

- Positives: competitive dividend yield and growth, solid financial footing, share price trending below moving averages, anti-financial crimes business segment shows growth potential.

- Headwinds: the company is currently extremely overvalued based on its P/E ratio.

- The risk of acquiring software firm Adenza is offset by long-term value potential for Nasdaq.

Research Brief

After having covered a few other exchange operators in the last quarter, I am kicking off Q3 by covering Nasdaq ( NDAQ ), bringing together the key sectors I write about which are technology/data and financials.

The company is scheduled to announce its Q2 earnings results next Wednesday, July 19th, so ahead of that call the goal is to see if this stock is a buy, sell, or hold right now.

Notable items about this company from their website are: they introduced the first electronic stock market in 1971 and today have 4K+ company listings, almost 40 offices globally, and the iconic MarketSite location in Times Square in NYC with its well-publicized opening bell ceremonies, a location I have walked past many times in years past during my New York days.

From its company profile, its business segments are very diversified across market platforms, capital access platforms, and anti-financial crime.

Our Rating Methodology

Our goal is to find value buying opportunities for stocks in the financial & tech sectors, for companies that otherwise have strong financial fundamentals.

We individually rate 5 categories: share price trend, valuation, dividends, financial condition of company, macro factors affecting company.

If we recommend a stock on at least 4 of the 5 categories it gets a buy rating, 3 out of 5 is a hold rating, and less than that is a sell rating.

Share Price Presents Buying Opportunity

First, let's look at the stock price for Nasdaq before market open on Thursday, July 13th, which is $50.

Nasdaq - price at market open July 13 (StreetSmartEdge trading platform)

The above chart I made in a trading platform to compare the price vs the 50-day simple moving average (blue line) and 200 day simple moving average (red line). Since the death cross formation in March, the stock has been unable to break out past its 200-day SMA resistance line lately.

In my hypothetical portfolio strategy simulation, I am looking for a buying range below both the 200 day and below or around the 50-day SMA, which is highlighted in yellow ($49 - $54 buying range), and holding the stock for a timeframe of 1 year, selling it at a 10% capital gain, which would put the exit price target range at $54 to $59. While holding, I want to earn dividends and sell covered call options, which generate premiums.

Since this stock is currently trading around $50, I would recommend it as a value buy in line with my portfolio strategy above. *Please note the above is a hypothetical scenario, and your own may be to hold longer.

Extreme Overvaluation is Concerning

Next, let's dive deeper into some valuation metrics, using data from Seeking Alpha . In my analysis, I use GAAP-based forward P/E ratio and forward P/B ratio, comparing to the sector median as a benchmark.

Unfortunately, I am not impressed with the valuations on this stock. Its P/E is at 20.78, over 121% higher than its sector average and earning it a grade of "D-" from Seeking Alpha. The P/B is equally concerning, being at 3.68, putting it over 277% higher than its sector median.

By comparison to two other exchange operators, CME Group ( CME ) has a P/E of 21.10 and a P/B of 2.38, while Intercontinental Exchange ( ICE ) has a P/E of 25.01 and a P/B of 2.72.

So, while these two peers have a higher P/E, they have a somewhat more attractive P/B ratio than Nasdaq.

In the category of valuation, therefore, I do not recommend this stock.

Dividends Competitive vs Peers and 5 Year Growth

Now, let's discuss what kind of dividend yield a dividend-oriented investor can get on this stock. In my test portfolio, I am looking for stocks with a competitive dividend yield vs its peers, dividend growth and reliable quarterly payouts. Does Nasdaq fit that profile?

Using Seeking Alpha data , the dividend yield is 1.76% as of July 13th, with a payment of $0.22 and no immediate upcoming ex-date.

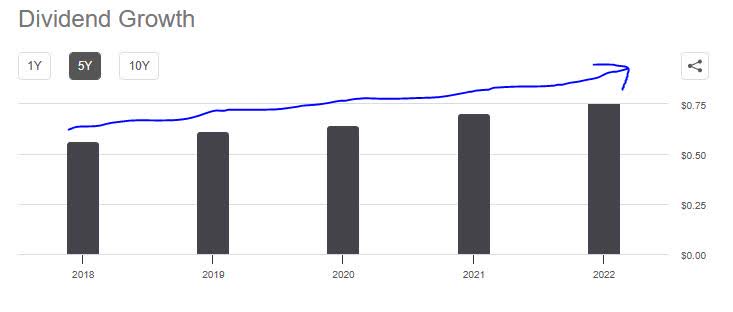

I like their 5-year dividend growth, which is positive:

{kind=link}

For instance, they went from an annual dividend of $0.57 in 2018 to $0.78 in 2022, a 37% increase in 5 years. Also, their quarterly payouts have been steady and uninterrupted, looking at historical data going back to 2013.

By comparison, CME Group's dividend yield is slightly higher at 2.43%, and the yield for Intercontinental Exchange is lower at 1.46%.

This puts Nasdaq's dividend yield in the middle of the two, and combined with steady payouts and a 5-year dividend growth makes it competitive vs peers in the dividend category.

So, in this category, I recommend this stock.

A Company with Solid Financial Metrics

First off, this company's free cash flow has been consistently positive, as the below chart from its Q1 presentation reveals:

{kind=link}

Second, another sign of financial strength is share repurchases and dividend distributions. As the chart below shows, Q1 saw a growth in both, which is a positive sign that this company is able to return capital back to shareholders:

Nasdaq - share repurchases & dividends paid (Nasdaq - Q1 presentation)

Third, let's talk about profitability improvement year over year. From the company's income statement , we see considerable YoY improvement in both net income and earnings per share, as the table below shows:

{kind=link}

So, the company thus far heading towards Q2 results has proven profitability growth, has returned capital back to shareholders, and has shown positive cash flow. I think the trend will continue in the next earnings call.

Thus, I recommend this stock in the category of the company's financial condition.

A Macro Trend in Tackling Financial Crime Helps this Company

There is a larger macro factor that could play well for this company, and that is the increased trend of financial crimes risk as the financial sector continues to depend more on technology, along with the need to mitigate that risk.

A June 10th analysis by analyst Welbeck Ash Research summed it up well:

Increased resources to commit crimes require an equally improved defense, which Nasdaq is offering with its AFC(Anti-Financial Crimes) segment.

To deep dive further, from a forward-looking perspective, I think this should bode well for Nasdaq.

Consider the following from a June 30th article in The Asset magazine:

Most companies globally anticipate an increase in financial crime risks in the next 12 months, with cyber security and data breaches expected to be the primary drivers, followed by financial pressures on organizations, according to a recent report.

Though many people many know of Nasdaq as a financial exchange, they actually have an entire business segment dedicated to tackling financial crimes as well.

In fact, take a look at the numbers for Nasdaq's AFC business segment for Q1, which showed an 18% organic revenue growth, driving $84MM in quarterly revenue for the company:

Nasdaq - AFC business segment (Nasdaq - Q1 presentation)

The company in its presentation commented that "revenues increased due to demand from Tier 2 banks for our FRAML solutions, particularly payments fraud."

So, I would recommend this stock in this category on the basis of the growing macro trend towards tackling financial crimes is correlated to the growth in this company's anti-financial crimes segment, which helps diversify its revenue stream beyond its other business segments, and revenue diversification is always a good thing in my opinion.

Rating Score

Today, this stock won in 4 of my 5 rating categories, so it gets a buy rating. My rating is in line with the Wall Street consensus, but is more bullish than both the consensus from the SA quant system and SA analysts which gave it a hold rating, as seen below:

ratings consensus (Seeking Alpha)

Risks to our Ratings Outlook

A risk to my bullish outlook on this stock that I could identify would be the company's recent acquisition of financial software firm Adenza, which I have seen other analysts already identify as an overly costly and debt-burdensome deal.

Consider what Seeking Alpha analyst Felix Fung had to say on this topic in his July 13th analysis :

While the combination with Adenza should be accretive in the long run, the price tag and leverage are two major concerns in the near term. The market also seems pessimistic about the deal as the company's share price has declined over 10% since the announcement of the deal.

In order to fund the acquisition, Nasdaq will also have to take on $5.9 billion in debt. Considering the current interest rates, the debt will likely have to be issued at a pretty high rate.

While that is definitely a valid risk concern, I personally think that the Street has already priced it in by now and this specific risk should not drive the share price down further from here, and from a forward-looking view in a year's time this acquisition will prove its value in my opinion.

In the larger picture, Nasdaq President of Market Platforms Tal Cohen set a positive tone in describing this long-term vision:

The addition of Adenza accelerates Nasdaq’s journey to advance the world’s economies through market modernization, and represents a major leap forward in our ability to serve our clients’ biggest and most complex problems.

Analysis Wrap Up

In closing, I reiterate my buy rating on this stock, which is in line with the Wall Street consensus rating.

Positives include competitive dividend yield and growth, solid financial condition of the company, a diversified portfolio of business segments that include anti-financial crime which will benefit from the macro trend of increased risk of financial & payment fraud, and a stock price trading in a buying territory based on my chart.

A headwind is that the company is currently seeing extremely high valuations, which kept it from getting a "strong buy" rating today.

The risk of acquiring software firm Adenza comes with added debt, but in the long term I believe it will drive value for the combined company, so should mitigate the short-term risk.

I continue to keep the exchange operators like Nasdaq, CME Group, and Intercontinental Exchange on my watchlist as they have an interesting & diversified business model that has proven resilient, but also they have been able to adapt well to the current data-driven environment and have harnessed the power of data as a service, since there is value in data itself.

For further details see:

Nasdaq: 4 Reasons To Buy This Otherwise Overvalued Company