ICE - Nasdaq: A Structurally Growing Exchange Facing A Temporary Slowdown

2023-05-15 17:04:48 ET

Summary

- Nasdaq has an attractive business model offering strong barriers to entry, high profitability, limited capital investments and recurring revenue streams.

- While transaction-related revenues are exposed mostly to the least attractive categories, Nasdaq has built a significant non-transaction business within different attractive categories.

- Following very strong years, trading volume could normalize, reducing the growth trajectory of the business.

- Valuations are not stretched and reflect at least partially lower earning growth for the coming years.

In general, financial exchanges are amongst the most attractive business models. They are highly profitable local monopolies with whom it is almost impossible to compete. In addition, they have defensive, asset-light and highly scalable business models. However, exchanges' core transactional businesses are mature with limited growth opportunities, which leads exchanges to move away from cyclical volume-related revenue to a more stable, higher growth recurring revenue stream.

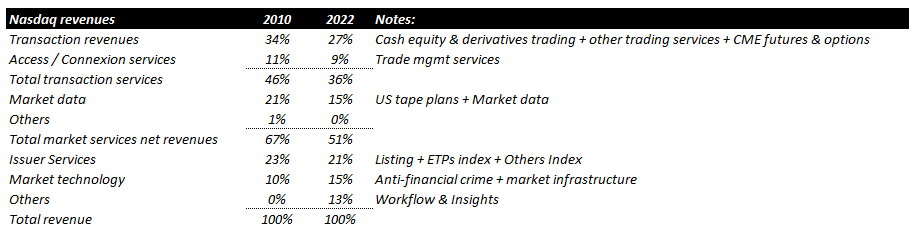

Nasdaq ( NDAQ ) is no different! The company has reduced its exposure to the competitive cash equity and equity option businesses from 34% in 2010 to 27% in 2022 despite transaction-based revenues being most likely at a cyclical peak (more about that later).

(Source: Company annual reports and author) (Source: 2022 annual report and author)

{kind=link}

{kind=link}

Nasdaq is one of the exchanges with the lowest exposure to transaction-based revenues.

(Source: Companies' annual reports and author)

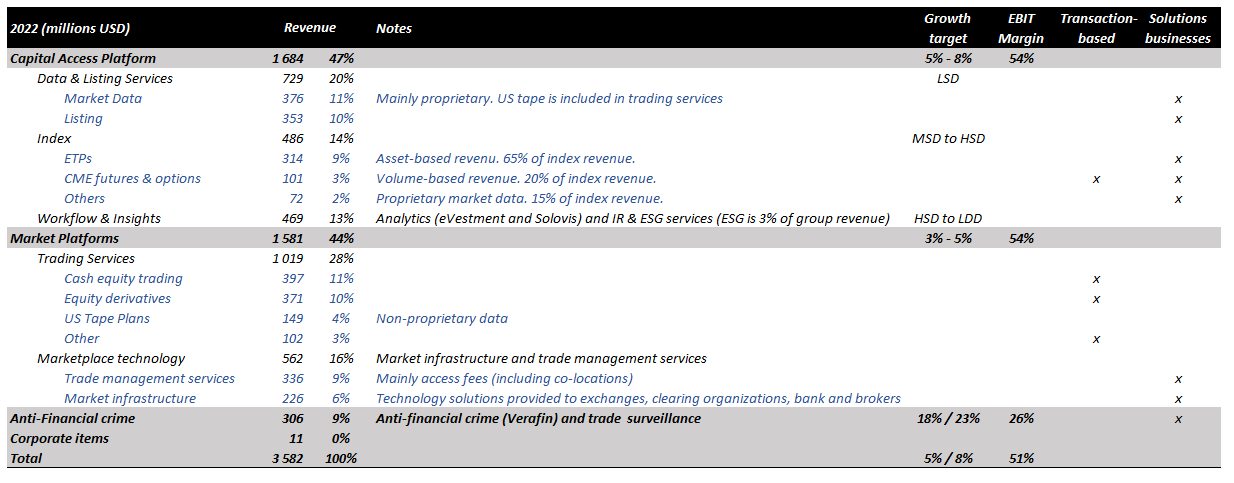

Transaction-related business (27% of revenues)

Nasdaq's transaction-based business is mainly composed of US and Nordic cash equities and US equity options (multiple-listed options and proprietary single-exchange-listed options such as Nasdaq 100 index options). The trading business is highly cash generative and very profitable with strong incremental margins. In addition, it provides stability during periods of increasing market volatility because revenues are strongly correlated to trading volume (it increases during market stress) as pricing is on a per share basis (versus pricing on a national value in Europe). Unfortunately, trading volume for these product categories is cyclical, offers limited structural growth opportunities and is highly competitive.

The cash equity business is highly competitive because equities can be traded on different exchanges, dark pools and alternative trading venues. Besides, on-exchange trading is losing market share and is facing higher regulatory scrutiny.

{kind=link}

The equity options business faces a lower level of competition than the cash equity business, as the market is much more concentrated. This higher level of concentration is the direct result of higher barriers to entry. Indeed, options clearing must be conducted through an exchange, thus preventing the competition from alternative trading venues. The equity index option business is even more attractive as it does not face competition due to the use of proprietary indices (eventually exclusive rights) such as the Nasdaq 100 index. As a result, these options are traded on a single exchange, which gives exchange operators some pricing power.

{kind=link}

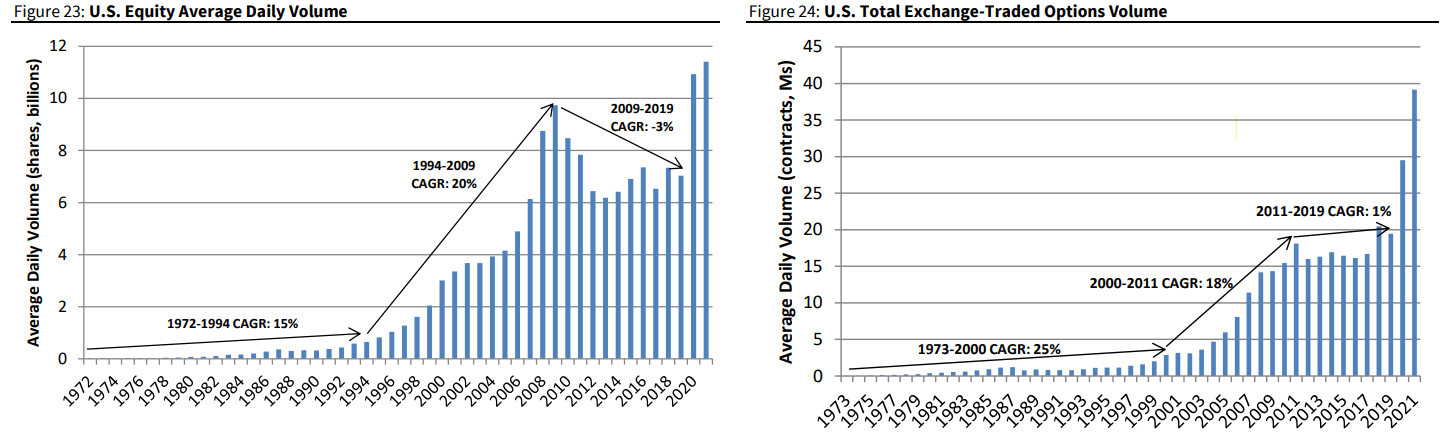

Trading volume is currently at elevated levels. Indeed, cash equities and equity options strongly benefited from the surge in retail trading following the pandemic due to people's free time, the proliferation of commission-free brokerage accounts and innovation (trading apps, etc.). We believe that trading volume could normalize over the coming quarters, pressuring transaction-related revenues.

{kind=link}

Non-transaction business (73% of revenues)

The solution business, comprised of the capital access platforms and anti-financial crime segments and the marketplace technology business in the market platforms segment, does not rely on transaction volume to generate revenues. Despite facing more competition (no monopoly position), the solution business offers attractive features such as more stable recurring revenues, proprietary products enjoying pricing power and decent growth prospects.

While a portion of the solution business such as the listing and index businesses remain subject to market conditions, most of the solution businesses are much more resilient and relatively immune to market conditions. Unlike transaction-based businesses that rely on trading volume to grow, the growth of solution business is driven by structural growth drivers that should enable the solution segment to grow organically by 7%-10% over the coming three to five years. The workflow and insights (13% of sales) and market data (15% of sales) businesses should benefit from the growing demand for data, including ESG data (currently accounting for <3% of sales), the proliferation of quantitative and high-frequency strategies, and the need for digital solutions. The index business (14% of sales) will keep benefiting from the shift from active to passive investments, the brand power behind Nasdaq indexes, and the increasing need for data (risk management, reporting, analytics, etc.). The anti-financial crime business will benefit from the demand of financial institutions for better risk management solutions due to the stricter regulatory environment and the proliferation of transaction/payment methods.

More specifically, the anti-financial crime business is expected to grow by 18%-23% over the coming years. In addition to benefiting from the structural growth drivers previously mentioned, the business should benefit from cross-selling opportunities following the Verafin acquisition. Indeed, the legacy market and trade surveillance offerings were mainly sold to tier 1 financial institutions whereas Verafin, with its fraud detection and anti-money laundering solutions, serves mainly smaller financial institutions (The anti-financial crime segment signed its first global tier 1 client in April). Analytics solutions could expand internationally, as they are much more present in the US than in international markets. Besides, Nasdaq could flex its pricing power over the coming years, given it did limit price increases over the past years in order to build its customer base.

Per management, overall revenue growth is expected to be around 5%-8%. We think that management expectations for the market platform are probably overly optimistic (given our thoughts that trading volume is at a cyclical high level). Within that context, we think revenue will grow around 5%, which is at the lower-end of the company guidance.

(Source: Nasdaq investor presentations and author)

{kind=link}

Operating margin should remain relatively stable as lower-margin businesses (Anti-financial crime, analytics) will outgrow the high-margin trading business, especially considering that it can face cyclical headwinds from lower trading volume.

(Source: Nasdaq investor presentations and author)

{kind=link}

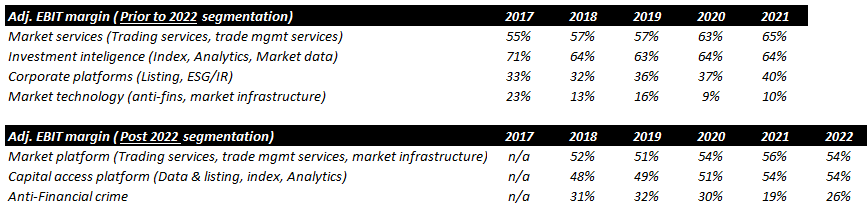

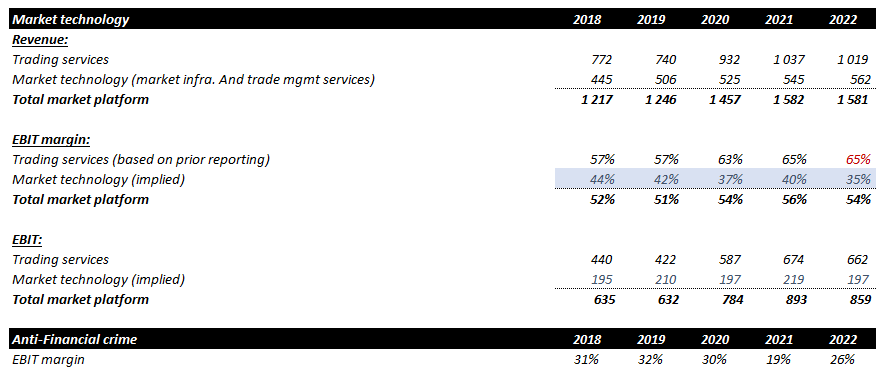

The market infrastructure and anti-financial crime businesses have room for margin expansion given that the company made significant investments in order to develop SaaS solutions and grow customer base, which depressed margins. As a result, we estimate that the operating margin of the market technology business (included in the total market platform segment) decreased from 44% in 2018 to 35% in 2022. At the same time, trading services' operating margin increased from 57% in 2018 to approximately 65% in 2022 thanks to the surge in trading activity, enabling the segment's operating margin to improve. The anti-financial crime business had a 31% operating margin in 2018 and declined to 26% in 2022 following the 2021 Verafin acquisition.

(Source: Nasdaq investor presentations and author)

{kind=link}

The company guides for a 4%-7% increase in operating expenses, which is roughly similar to our 5% revenue growth expectation at the midpoint. As a result, EPS should grow at a mid-single digit growth rate.

A strong outperformer

This business transition towards higher growth and more stable software and analytics businesses allowed Nasdaq to significantly outperform its peer group and the broad US equity index over the last three, five and 10 years. However, this trend has reversed since the beginning of the year. Nasdaq's share price performance is in negative territory and lags its peer group.

(Source: Bloomberg)

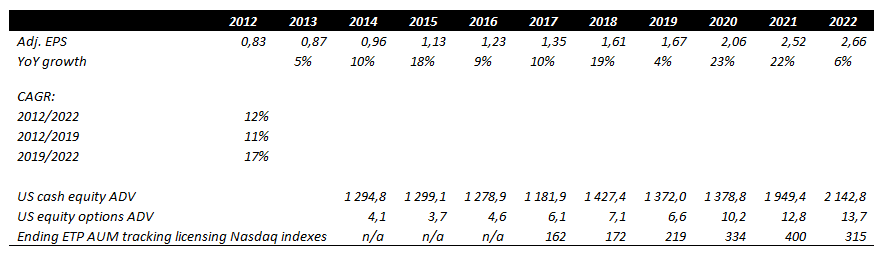

We believe that the recent underperformance comes from a lower earnings growth profile, following outsized EPS growth in 2020 and 2021 resulting from a surge in trading activity (cash equity and equity options) and very elevated equity valuations, especially for technology-related companies (representative of the Nasdaq index), boosting listing fees and ETP-linked revenues. Besides, 2023 consensus revenues are expected to grow at only 3% (assuming stable trading revenues), below the 5%-8% mid-term company guidance. Lower revenue growth comes from the extension of the sales cycle in several businesses such as Verafin, IR and analytics, lower AUM and IPO fees due to lower investor interest for tech-related stocks in a higher interest rate environment. Finally, a normalization of trading volume could further reduce revenue growth, with a risk of negative revenue growth. Consensus expects operating costs to grow ~5%, implying negative operating leverage and only 2% EPS growth for 2023.

(Source: Company annual reports)

{kind=link}

Valuation

As a result, Nasdaq's valuations are slightly lower than peers despite having a much larger non-transactional business, which is more resilient and requires higher valuation multiples.

(Source: Bloomberg)

Conclusion

Even though the transaction-related business is skewed towards the less attractive categories (cash equity and multi-listed options), Nasdaq successfully leverages its brand, data, and client base to build an attractive non-transaction business, that provides growth opportunities, visibility, and resilience. As a result, a significant portion of revenues comes from attractive businesses. From a valuation perspective, we think that current valuations are not stretched and reflect, at least partially, the short-term headwinds and lower earnings growth. We prefer to wait for an eventual pushback in trading revenues and/or more attractive valuations in order to potentially build a position.

For further details see:

Nasdaq: A Structurally Growing Exchange Facing A Temporary Slowdown