NDAQ - Nasdaq: That's Still A 'No' From Me

Summary

- I've reviewed the company Nasdaq a few times at this point, and while the company has outperformed over the past few months, it's still a bit expensive.

- I'm reviewing the company and looking at where things might go for 2023.

- The current 2023E does not paint a pretty picture for investors - even if the company is beyond safe. I believe there are better alternatives out there and here is why.

Dear readers/followers,

When it comes to Nasdaq (NDAQ), I prefer to look at the longer-term performance of the stock. My initial article on the company was written in October, and based on that article, the company has underperformed by offering a total RoR of negative 6.63%. This is an exercise in why valuation isn't just something to sometimes look at, but why it's a crucial component of a conservative investment approach that results in positive returns despite a negative market.

I write some macro articles where I go through things like portfolio strategy that could lead to returns like this in a down-year - but in this article, I'm going to revisit a company that I believe will continue to underperform due to the simple valuation of the business.

Let's review NDAQ.

Reviewing Nasdaq - the Company

Nasdaq actually is an acronym for the National Association of Securities Dealers Automated Quotations. Its history goes back to 1971 to its founding, by what is now called FINRA. It was the first electronic stock market in the world, though initially, it was just a way to get quotes - trades came a lot later than that.

The company took step after step towards becoming a functioning stock market, and it joined the LSE in 1992 to be the first intercontinental linkage.

Let me be clear - Nasdaq is without a doubt, a market-leading and superb/great company. That is not in dispute. In fact, that is rarely in dispute when I write about a company because I rarely waste my time on companies i consider to be "bad".

What I make clear in articles like this one, is why the company isn't the best thing to buy at the moment. Big difference, and one that many investors need to be reminded of after the tech-froth of 2020-2021.

I'm hoping that you didn't make the mistake of paying $337/share for stocks like Carvana (CVNA) which would mean that if you didn't sell, you're at a 99%+ loss today, but if you did, there's a lesson to learn here (though not just one if we're talking Carvana).

Don't just buy great companies - or companies you believe in - make sure you get them cheap. If we could get Nasdaq cheap, that would be amazing. The company was a pioneer in early online trading - it started back in 1998 when most of us were using the internet through dial-up modems. The company's main index is the Nasdaq composite, published since its inception. The company also went public in 2002 via an IPO, and merged with the OMX in 2007, including the Nordic exchange operators.

Today, NDAQ offers three comprehensive levels of quotes, and caters to various levels of market makers and traders - and it operates direct exchanges across the entire world, NA, and Europe.

The company's operations are categorized into the Nordic Market, the Baltic Market, and First North, an alternative exchange.

Nasdaq Inc has 46% long-term debt to cap, a market capitalization of $30.4B, and a BBB+ credit rating. The company is a tech business, generating sales revenue through the offering of data, analytics, software, and various services. It's split into four segments, each centered around various platforms and end users.

NDAQ IR (NDAQ IR)

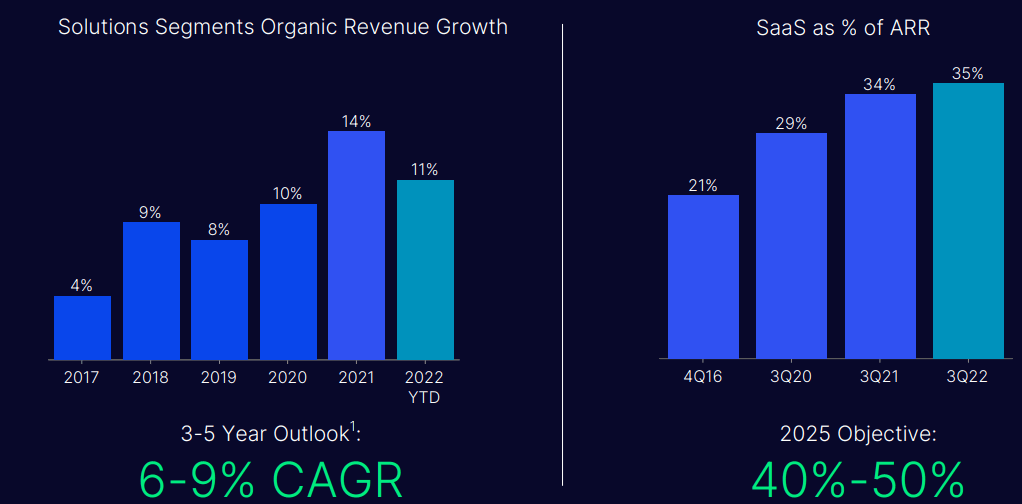

It grows both inorganically and organically, and the company's recent results have been solid. Remember, the company isn't overexposed to any one specific of these segments. The largest revenue is around 38% from market services - other than that, and Market tech being small, it's a pretty decent and stable split.

3Q22 are the latest results we have. They more or less confirm what we already knew in terms of EPS stability and slow growth. The company is in the midst of a SaaS revenue transformation, with SaaS sales now 35% of the recurring revenues on an annual basis. NDAQ saw a close to a double-digit increase in the top line on an Annualised recurring basis, around 6% growth in Net, but around 15% growth in YoY non-GAAP EPS, implying bottom-line improvements.

My problem with the company certainly isn't growth - NDAQ is growing well, and it's growing in the right fields as well.

{kind=link}

The market is supportive of these trends and forecasts - we can actually expect things to move north for the company, based on the long-term dynamics of the market, which include digitalization, increased demand for SaaS as well as anti-financial crime tech, and increased outsourcing of specialized tech. All of this moves in tandem with NDAQ's appeal. And while the market may be down this year, there's a backlog of companies that are waiting for the market to become more welcoming to IPOs again.

If I owned any sort of company, even if I knew it was a 100% successful one, I wouldn't be IPO'ing it in today's climate. It's a Risk-off time - asking people to go into whatever it is would be, as I see it, foolhardy today.

But the future still exists.

On a fundamental level, there really is nothing to worry about when it comes to NDAQ. The company is simply "too good" when it comes to fundamentals and results. It has also been repurchasing significant amounts of common shares over the past 4 quarters, especially when share prices were at a trough - as well as paying down debt, to where net debt is now no more than 2.6x to non-GAAP EBITDA - an impressive level.

Nasdaq makes money both by trading and non-trading revenues, and the company has an excellent history of delivering revenue growth, improved margins, and superb EPS growth over time. Since 2017, the company has nearly doubled its annual earnings. Its TAM is inarguably no lower than $50B at the very least, which would imply that company segments have the real potential of quadrupling over the long term.

Recent results are solid - fundamentals are solid - how's valuation?

Nasdaq Valuation

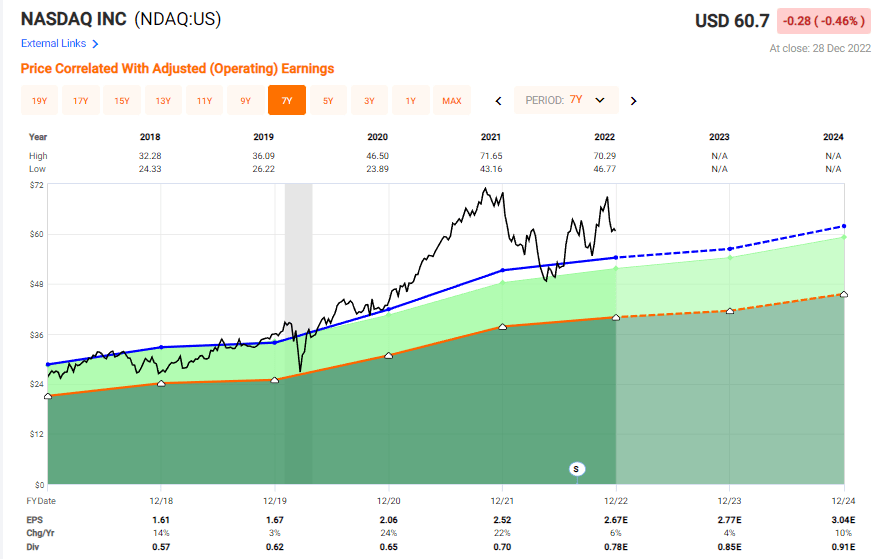

Fundamentally, there is nothing not to like about Nasdaq as a company. The fact that you could pick this company up at 8X P/E back in the dot-com bubble is insane and makes one wish that one had invested for returns in quadruple digits.

But since 2020, the valuation has taken a right turn at Crazy-town. And despite trying to leave Crazy-Town, which it did a few times during May and June when you could have bought it at cheaper than 20x, the company is currently long-term renting a room in that particular place and seems to refuse to leave it behind.

NDAQ Valuation (F.A.S.T graphs)

{kind=link}

We're in the midst of a correction. I refuse to believe that the correction is over. Further hikes in interest rates are coming, and I believe the compression that we've seen for a year will continue for some time going into 2023. The simple fact is, I would rather miss out on a company than overpay for an opportunity that later turned out to be too expensive relative to what I believe it to be worth.

That is the case with NDAQ currently.

Even on a fairly optimistic forward basis, estimating nearly 20x P/E for 2024E, the total ROR for the company due to the very meager dividend of 1.32%, that RoR would be about 2.24% here. That's 1.11% per year - including dividends. That means, without dividends, you would be realizing negative returns for the investment here, at a 20x P/E.

No thank you, is what I say to that particular possibility.

Yes, Nasdaq will likely grow. Yes, it's an excellent company. No, I don't see any conservative, realistic scenario where a near-20-30X P/E valuation for a Fintech and broker company - which is what Nasdaq is - would result in a good return for investors.

I would still be genuinely curious about someone seeing a conservative upside here. At 1.3% yield, this company's yield is less than inflation, and even at high expectations, a 1.11% annual RoR shouldn't be enough to entice anyone to run to buy the stock. However, if you're there, please let me know why you believe the company will perform better.

It's not as though I don't invest in stock exchanges. I have in fact done several successful purchases of stock in Deutsche Börse (DBOEY), and my position is currently up significantly in that particular investment. But again, it's all about that price paid.

Whenever I talk to someone - client or otherwise, even a reader, most of what I seem to be doing is explaining the basics of valuation investing to them.

NDAQ is currently considered a "BUY" by a particularly positive cadre of analysts following the stock. 15 of them from S&P Global give NDAQ a range starting at $55 and going all the way to $85/share. The current average comes to $66/share, meaning that most consider the company 8% undervalued here.

However, in a strange trend, only 4 of those 15 analysts consider the company a "BUY" here - an absolute majority of 9 are either at a "HOLD", no opinion, or "UNDERPERFORM". Reconciling that with that PT can be hard - but having analyzed such things for years now, let me tell you that I believe the consensus is that the potential for market underperformance on the part of NDAQ is high.

I don't think that low-ball target of $55 is far off, truth be told. At $55/share, the upside could be market-beating, and there is something to be said for NDAQ's stability. But I would probably target even lower to offset that premium somewhat, because I don't see double-digit growth in NDAQ's near-term future - certainly not as long as these headwinds and this environment persists.

And I believe this to be the case for the next 1-2 years at least.

When I call the company overvalued, I speak about earnings and valuation. While NDAQ will expand its earnings, I don't see that it will do so at a pace that will justify its high P/E valuation. Investing here will mean a lack of capital growth compared to what you could get elsewhere in the market.

My PT for NDAQ has averaged that 19.5x P/E for some time, and that comes to a range of $50-$55. I would consider $55 an acceptable entry for NDAQ, but you should be very positive if that's the case.

Thesis on the Common Share

Here is my current thesis for Nasdaq Inc:

- A company of excellent quality and beyond great renown, with great potential for any portfolio - at the right price. That right price isn't something we're able to get today - even with options.

- I consider the company, despite its great fundamentals and safeties, to be an unequivocal "HOLD". I would also rotate profits at this point if I was invested in the business, and buy something cheaper with greater upside.

- My price target for Nasdaq as a business comes to $55/share.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

3 out of 5 criteria were fulfilled, and both of the non-ones being valuation-related, this company is a no-go here.

Option Potentials for Nasdaq

I want to give you the option to "go in" at least, but I want to preface this by saying I wouldn't touch this at these premiums. These premiums are somewhat affected by today's generally bullish view on tech and the advancement we're seeing. You can generate 6.91% annualized here, but...

Option details (Author's Data)

...this one has a very high potential for assignment due to its timeframe, and given what's available on the market today, I wouldn't consider it all this attractive. My rule of thumb for CSPs is that I want close to a double-digit annualized RoR, and when we're more than 60 days out, I want it higher than this - or a higher margin of safety.

NDAQ is difficult here - but these are the approaches I could consider.

For further details see:

Nasdaq: That's Still A 'No' From Me