ICE - Nasdaq: Winner Facing Headwinds

2023-06-10 07:13:29 ET

Summary

- NASDAQ has experienced significant growth and margin improvement, with increased subscription revenue and diversification.

- Market conditions are attractive, but cyclicality remains an issue as company's reliance on capital markets is evident.

- Anti-Financial Crime (AFC) segment offers diversification potential, and continued expansion in this area is essential for the company's success.

- With an EBITDA-M of 32% and NIM of 18%, the company is of extremely high quality. It has a wide moat and deep expertise, implying long-term success.

- We suggest caution until market conditions improve, as growth is materially slowing.

Investment thesis

Our current investment thesis is:

- Nasdaq (NDAQ) is generating margin improvement alongside growth, as well as increasing its subscription revenue and diversification.

- Market conditions are attractive, with increased demand for Insight services, Fraud and Money Laundering support, as well as ESG services. Nasdaq is leveraging its brand and deep expertise to develop its products.

- Although diversification is reducing cyclicality, this remains an issue.

Company description

Nasdaq, Inc. is a global technology company that serves the capital markets and other industries.

The company operates in three segments:

- Market Platforms - offers various trading services, including equity derivative trading and clearing, cash equity trading, fixed income and commodities trading and clearing, and trade management service businesses.

- Capital Access Platforms - sells and distributes market data, develops and licenses financial products, operates listing platforms, and offers investor relations and governance solutions.

- Anti-Financial Crime - provides anti-financial crime management solutions, including market surveillance and compliance software.

Share price

Nasdaq's share price has trended unrelentingly in one direction, returning over 450% to shareholders in a decade. A solid 10 years of financial performance backs this, with the outlook for the business far improved.

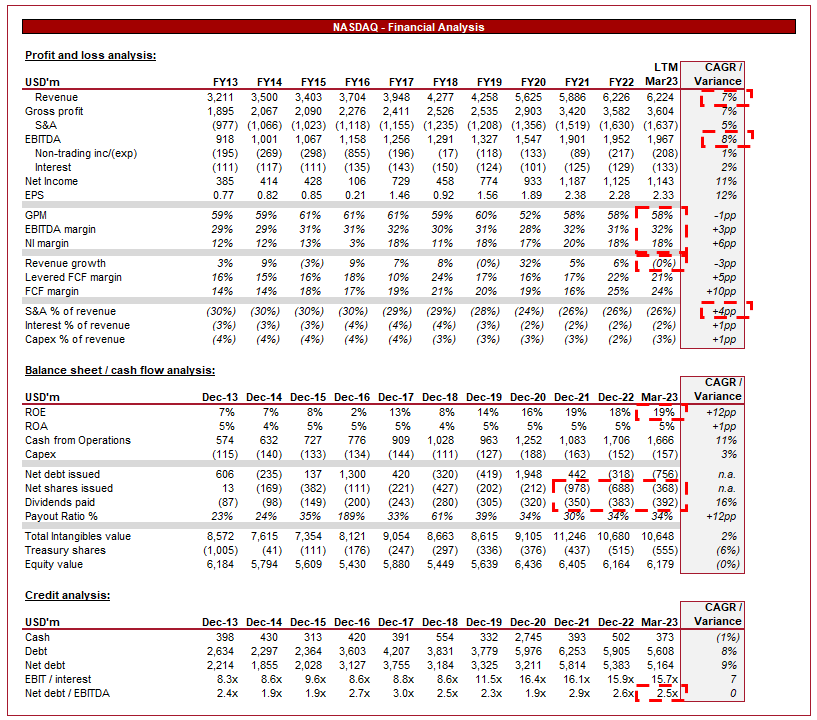

Financial analysis

NASDAQ Financials (Tikr Terminal)

{kind=link}

Presented above is Nasdaq's financial performance in the last 10 years.

Revenue

Nasdaq has grown revenue at a CAGR of 7%, driven by a period of rapid expansion for capital markets. Post-GFC, we experienced record low interest rates, which encouraged investment into markets in search of returns.

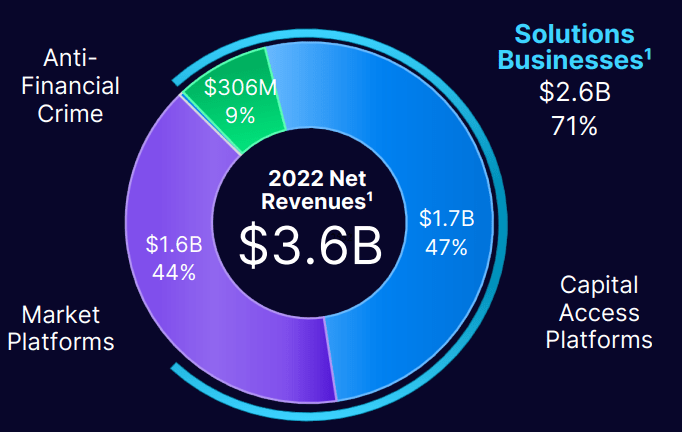

Nasdaq's revenue is highly diversified, with no single division comprising more than 47% of revenue in FY22. This said, the company is clearly reliant on capital markets, given the interconnected nature of both Market Platforms and CAPs.

{kind=link}

Market Conditions

Before discussing the company's revenue streams further, it is worth exploring current market conditions.

Following a strong decade, we have seen equities experience a bear market. The S&P 500 remains 10% down from its 31/12/21 level. This is driven by two key interconnected factors. Firstly, the rapid rise in inflation. This has caused financial issues for many people across the Western world, with the cost of living increasing substantially. This has impacted demand within the economy, causing a knock-on effect across many businesses. Secondly, the lifting of interest rates in response to inflationary conditions. With the cost of capital increasing, many businesses are facing issues with financing. Also, the discount rate for a company's future cash flows is also higher, with both factors contributing to a decline in valuations. Further, it now costs investors more to purchase assets, and they also have more alternatives to equities.

These factors have all contributed to less demand for equities, reducing transaction volumes and discouraging investment.

Market Platform

Market Platform is a core part of Nasdaq's offering, allowing investors the opportunity to conduct full trading services (transaction and post-transaction). This revenue stream is dependent on trading volume, with Nasdaq taking a commission for its services. Further, the business also generates recurring revenue for access to its marketplace.

In the most recent quarter, growth was driven by Marketplace technology, which has seen continued demand for trade management services.

Market Platforms (NASDAQ)

What is slightly concerning is the flatlining of Trading Services, which is a reflection of the current bear market. This is acting as a drag on the business and reflects its exposure to cyclicality.

Capital Access Platforms

CAP is Market Platform's sister service. This comprises 3 main revenue streams, Data and Listing services, Index, and Workflow and Insights.

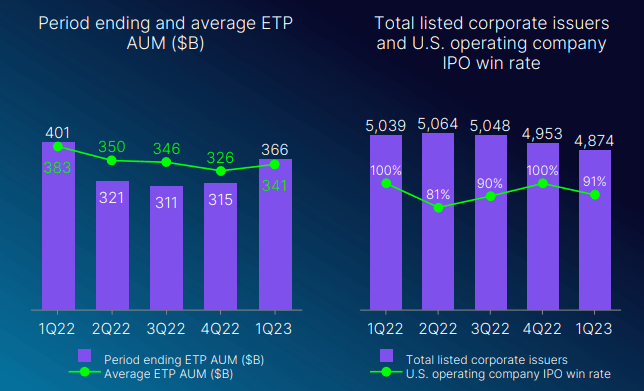

Nasdaq's monopolistic position is reflected in its Listing activities, with the company having a 91% win rate in IPOs (within the US) in Q1'23. Nasdaq has deep expertise and infrastructure in this segment specifically, implying an inability of new entrants to materially dislodge the business. During bear markets, we generally see the number of IPOs decline, as Managements hold off in fear of poor valuations. This is illustrated in the table below, contributing to slowing revenue growth (2% Y/Y).

This infrastructure superiority allows Nasdaq to leverage its brand to provide other related services. Nasdaq indexes, a link for exchange-traded products, have an average AUM of $341bn as of Q1'23. AUM has declined noticeably since the level seen in FY21, contributing to a Y/Y decline in revenue of (10)%.

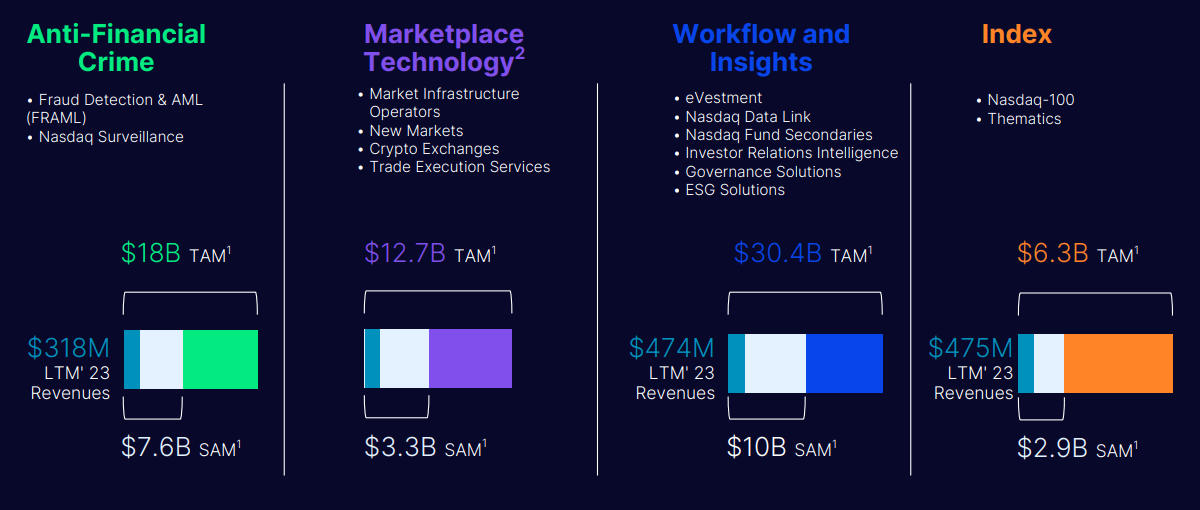

The financial industry is increasingly adopting technology to improve efficiency and accuracy and as a means of achieving an edge. This is not just within the financial sector but the wider economy, as we are well into a "data era". Technology has developed to the extent that it is able to quickly and reliably analyze information to provide insight and information for decision-making. Nasdaq is investing in advanced technologies like AI, machine learning, and blockchain to enhance its trading, clearing, and settlement services. Not only this, but we believe this investment could be highly bountiful for its Workflow and Insights segment.

The preferences of investors are shifting, with an increasing focus on environmental, social, and governance ((ESG)) factors. This is driven by demand from investors for exposure, as well as changing legislation forcing businesses to transition. Nasdaq has responded to this trend by launching ESG-related indexes and developing ESG services. These services have remained resilient despite the weakening market conditions, contributing to a 4% Y/Y increase in revenue within the Insight segment.

As we mentioned previously, this segment is intertwined with MP. MP has maintained its growth due to the recurring nature of revenue, creating a level of stickiness. CAP does not have this, contributing to a revenue decline of (1)% for the division.

Capital Access Platforms (NASDAQ)

{kind=link}

Anti-Financial Crime

Finally comes AFC. This is by far the smallest division but should not be underestimated. This segment is also subscription-based, generating additional ARR for Nasdaq.

The financial industry is subject to a wide range of regulations which are becoming increasingly complex, in conjunction with the cost of breaches also rising. The reason for the complexity is the same reason for crime (a major reason for breaches) increasing, which is technological development. Increased resources to commit crimes require an equally improved defense, which Nasdaq is offering with its AFC segment.

ARR has increased due to continued penetration into the SME banks, a clear target market for Management. Further, Tier 2 banks are particularly interested in payment fraud services, a key concern. The value proposition is high as there is no solution for businesses but to continually receive such services. This reduces the risk of churn.

In the most recent quarter, signed ARR increased by 20% and continues on a positive trajectory despite the market weakness. SaaS models are judged on the "Rule of 40", with AFC achieving 49 in the LTM. This offering is Nasdaq's true diversification potential, and so we would like to see continued expansion.

AFC (NASDAQ)

Commercials Trends

The financial industry is becoming increasingly global and the expectation is for this to continue. As we see further growth in developing nations, we will see western capital move toward these regions. Further, wealthy individuals in these regions will look to purchase equities in the west. Nasdaq has looked to improve its exposure to other regions by improving access to markets.

Nasdaq faces competition from other exchanges, including the New York Stock Exchange (ICE), and emerging exchanges such as the IEX. This competition has the potential to dilute Nasdaq's performance although we are yet to see a material effect.

Despite the market share in core markets, Nasdaq estimates strong growth potential across its key markets. This looks to be driven in large part by developments in the market rather than winning new customers, implying innovation is required. This creates execution risk.

{kind=link}

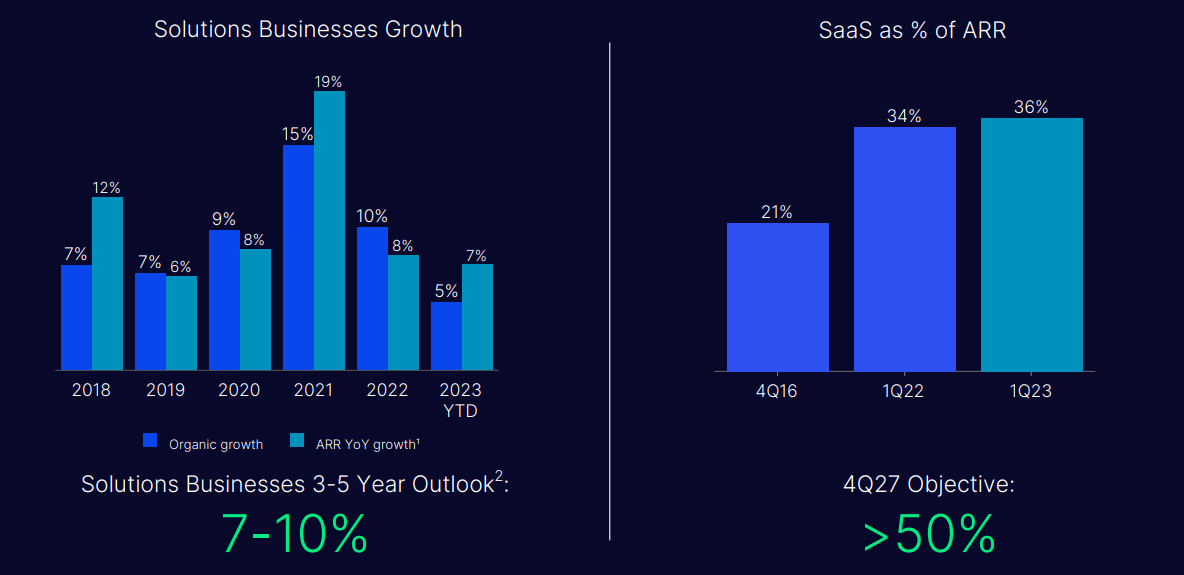

SaaS revenue has reached 36%, with management targeting 50% by FY27. This will help reduce the cyclical performance of the business we have thus far. Our view is that this is key to transitioning the business to a premium valuation, as otherwise, investors face double exposure to markets when investing in this equity.

{kind=link}

Margins

Nasdaq's margins are highly impressive. The company has an EBITDA-M of 32% and a NIM of 18%.

Across the historical period, we have seen impressive improvement, with 3ppts gained in EBITDA-M and 6ppts in NIM. This is a reflection of operating cost leverage, with S&A spending declining to 30% of revenue while GPM remains flat.

We believe margin improvement will be supported by the growth of AFC, which already experienced a 7% increase in OPM Y/Y. As the service grows and achieves scale, margins will rapidly rise.

Balance Sheet

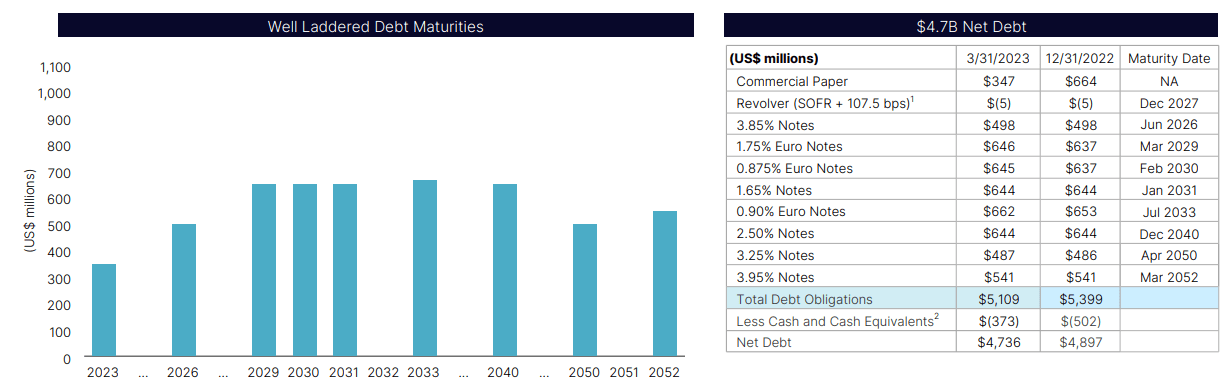

Nasdaq is conservatively financed, with a ND/EBITDA ratio of 2.5x. This gives the company flexibility to invest in growth or M&A if required, although given Nasdaq's cash generation is so high, this is unlikely.

Further, the majority of debt is fixed and the maturities are well managed. This reduces the risk of any material issues as debt is refinanced.

{kind=link}

Distributions to shareholders are in the form of both dividends and buybacks. Dividend payments have grown at a CAGR of 16% in the last 10 years, reflecting an improvement in payments in line with growth.

Valuation

Valuation (TIkr Terminal)

Nasdaq is valued at 16x NTM EBITDA and 21x NTM earnings.

The company is trading at a noticeable premium to its historical average and we believe this is justified. The key value drivers are:

- Nasdaq has achieved continued margin improvement, with no evidence to suggest a ceiling has been reached. Conversely, there is scope for improvement.

- Greater scale has been achieved without compromising margins.

- ARR continues to increase, reducing the impact of economic cyclicality.

- AFC has the ability to provide diversification benefits and reduced reliance on Capital markets.

- Competition has not dislodged Nasdaq's position in capital markets.

- General commercial trends, such as ESG, are positive value drivers long term.

This said, it is difficult to see where alpha can be generated above and beyond Nasdaq's current valuation. With continued market uncertainty and LTM revenue growth at 0%, there is the risk that sentiment changes if revenues decline.

Final thoughts

Nasdaq is a winner. Revenue growth will continue so long as markets attract investment, which all evidence suggests will continue. Margins are fantastic and Nasdaq's ability to generate continued improvement is impressive.

Our only concern with the company is that it remains cyclically linked to market conditions. Diversification and increased subscription revenue have protected the company from declining revenue thus far, but it looks to be grinding to a halt. With no material change to conditions thus far, we suggest caution.

For further details see:

Nasdaq: Winner Facing Headwinds