MKC:CC - Nathan's Famous Stock: Not As Tasty As The Hot Dogs

Summary

- Nathan's Famous has had an interesting operating history, with volatility present on both its top and bottom lines.

- Data for 2022 was promising, with sales and profits both rising nicely, but this doesn't make the company a great prospect.

- In all, the absence of material growth in recent years makes the company an okay play, but nothing special.

If you're a hot dog fan like I am, odds are you have heard of Nathan’s Famous ( NATH ). While many industry-leading brands tend to wind up owned by major diversified companies in the food space, this is not the case with every brand. One great example of this can be seen by looking at Nathan’s Famous. But in addition to this, the company does have its hands in other business activities. All combined, the firm seems to be a fairly solid operator. But this doesn't necessarily mean that is a great prospect to buy into. Although I have no doubt that the company will fare well in the long run, the combination of its trading multiple and its financial traffic record leads me to feel more comfortable rating it a ‘hold’ rather than a ‘buy’. This kind of rating indicates my belief that shares will likely generate upside that's more or less in line with what the broader market should experience.

A niche player in the food space

According to the management team at Nathan’s Famous, the company operates as a leading branded licensor, wholesaler, and retailer of products marketed under its Nathan’s World Famous Beef Hot Dogs brand name. The company, like many other food-centric firms that have achieved a sizable degree of fame, started off a long time ago. In fact, the firm initially began as a nickel hot dog stand on Coney Island back in 1916. Since then, the company has evolved into what it is today. To truly understand the company though, we should dig into the three major channels of distribution that the company operates.

For starters, the company has a licensing program where it contracts with other parties so that said parties may manufacture, distribute, market, and sell a wide variety of Nathan’s Famous branded products. These include not only the firm's hot dogs, but also its sausage and corned beef products, as well as its frozen crinkle-cut French fries. These products are sold in packaged form to supermarkets, mass merchandisers, and club stores across all 50 states. This particular segment accounted for 27.7% of the company's revenue during its 2022 fiscal year. However, that was responsible for an impressive 82.5% of the company's profits for that same year. The company also has what it calls its Branded Product Program. This particular portion of the company provides foodservice operators across a wide variety of venues the ability to capitalize on the company's brand by marketing and selling its hot dog products and other related offerings. Unlike the licensing program, Nathan’s Famous generates revenue not from a licensing fee, but instead from the sale of its products to these operators. According to management, these operations accounted for 57.7% of the company's revenue in 2022.

Next in line, we have the quick service restaurants the company has. These operate, unsurprisingly, under the Nathan’s Famous brand name. Excluding virtual kitchens, the company's restaurant system consists of 233 Nathan’s franchised units (which include 120 Branded Menu Program units), and four company-owned units, one of which is seasonal in nature. All of its company-owned locations are in New York. But the franchised units are spread across 17 States and 12 foreign countries. The company's virtual kitchens include 226 units spread across 19 States and four foreign countries. During its 2022 fiscal year, this segment was responsible for 12.9% of the company’s revenue.

{kind=link}

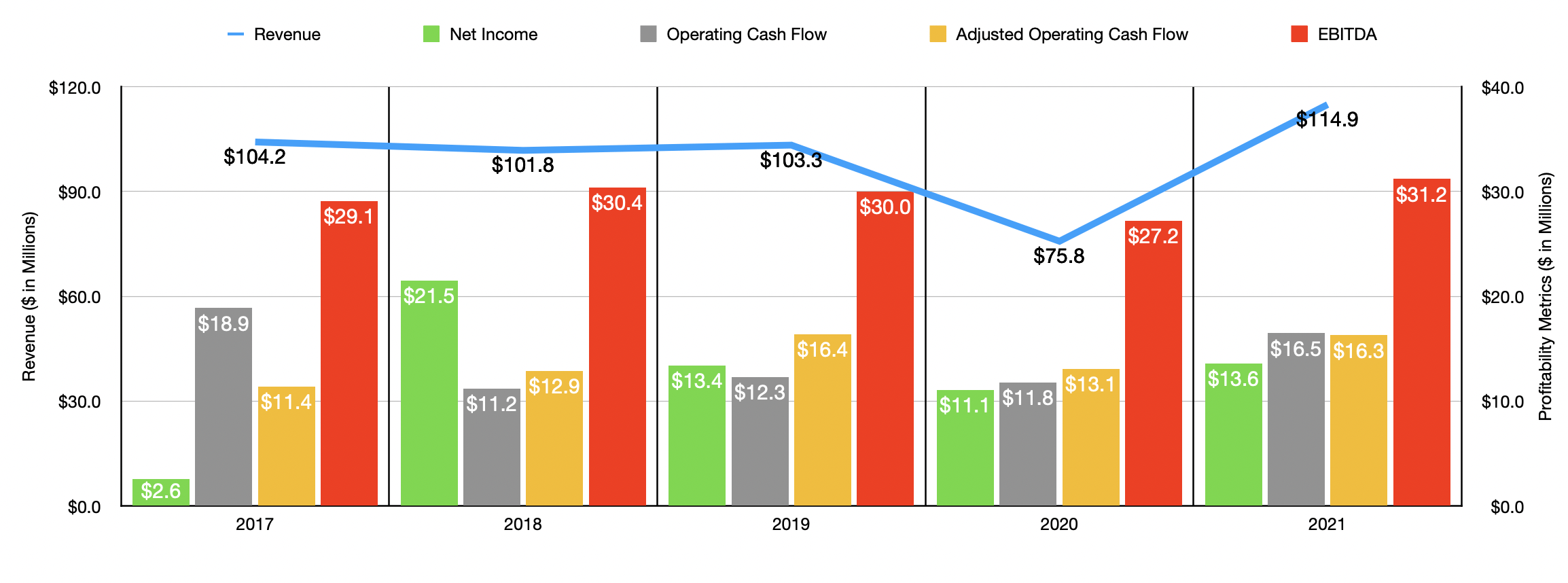

Over the past five years, the financial picture for the company has been a bit lumpy. Net income dipped from $104.2 million in 2018 to $101.8 million in 2019. In 2020, revenue increased slightly to $103.3 million before plunging to $75.8 million during 2021. Then, during the 2022 fiscal year, sales came in at $114.9 million. You can see a similar level of volatility when it comes to the firm's bottom-line results. Over the past five years, net income ranged from a low point of $2.6 million to a high point of $21.5 million. In this case, there was no clear trend for the business. Other profitability metrics followed a similar path. Operating cash flow, for instance, moved in a fairly narrow range of between $11.8 million and $18.9 million. The only time we got a hint of a trend was when looking at this number when adjusted for changes in working capital. Between 2018 and 2022, this metric rose from $11.4 million to $16.3 million. Though the two years prior to that did show year-over-year declines. And finally, EBITDA for the company was almost flat during this time, ranging from a low point of $27.2 million and a high point of $31.2 million.

{kind=link}

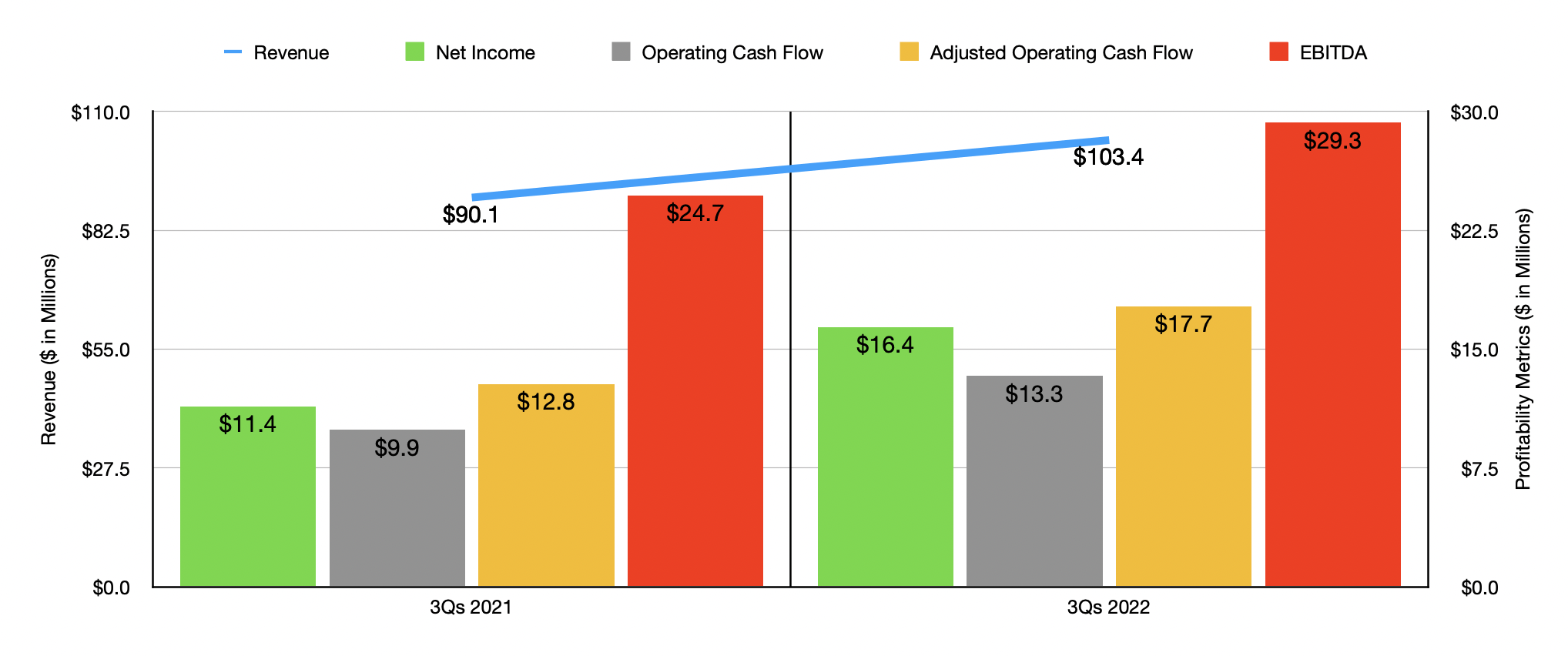

During the first nine months of 2022 , the company did see something of a breakout from a revenue and profitability perspective. Sales of $103.4 million beat out the $90.1 million reported one year earlier. This increase of roughly 15% was driven largely by a 19% increase from its Branded Product Program thanks in large part to a 14% rise in the volume of hot dogs sold and because of a 5% increase in average selling prices. License royalties revenue grew by 8% during this time because of a 9% increase in the average net selling price of its products with the companies that it contracts with. The company also saw a 12% increase in revenue associated with its company-owned restaurants because of higher traffic at its Coney Island locations. During this time, franchise fees and royalties for the company rose by roughly 9% because of higher sales at airport locations, highway travel plazas, shopping malls, movie theaters, and casino locations.

With this rise in revenue also came higher profits. Net income during the first nine months of 2022 totaled $16.4 million. That's up significantly compared to the $11.4 million reported during the first nine months of 2021. Operating cash flow rose from $9.9 million to $13.3 million. If we adjust for changes in working capital, it would have risen from $12.8 million to $17.7 million. And finally, EBITDA for the company expanded from $24.7 million to $29.3 million. Management has not provided any guidance when it comes to 2022 results in their entirety. But if we annualize results experienced so far, we should anticipate net income of $19.6 million, adjusted operating cash flow of $22.5 million, and EBITDA of $37 million.

{kind=link}

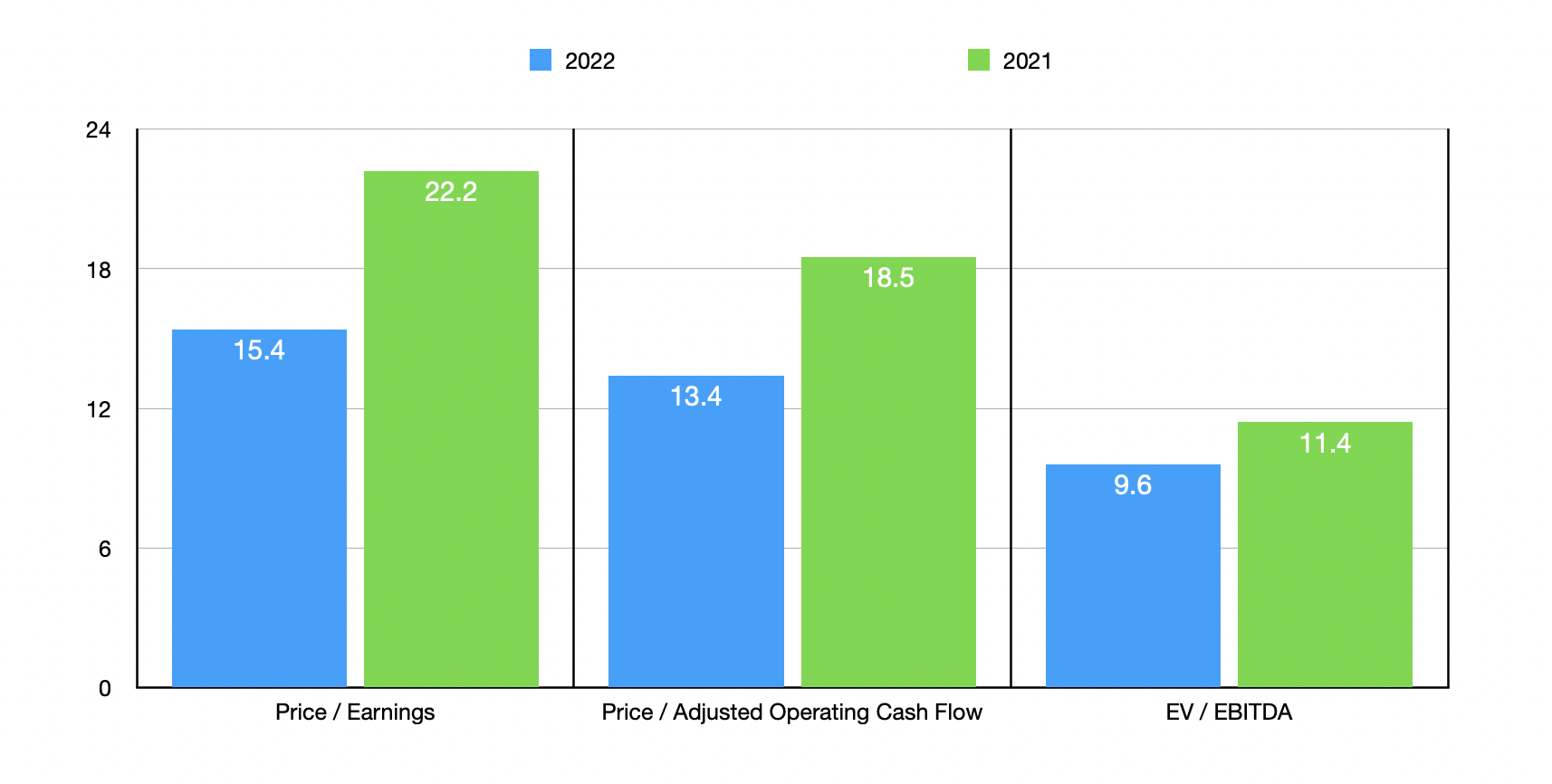

Based on these figures, the company is trading at a price-to-earnings multiple of 15.4. The price to adjusted operating cash flow multiple should be 13.4, while the EV to EBITDA multiple for the company comes in at 9.6. These numbers compare favorably against the 22.2, 18.5, and 11.4, respectively, that we get when using data from 2021. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 5.6 to a high of 29.5. Using the price-to-operating cash flow approach, the range was from 5.5 to 30.8. And using the EV to EBITDA approach, the range came in at 3.3 to 21.5. In all three cases, two of the five companies were cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Nathan's Famous |

| 15.4 |

| 13.4 |

| 9.6 |

| Hormel Foods ( HRL ) |

| 24.6 |

| 21.8 |

| 16.9 |

| General Mills ( GIS ) |

| 15.7 |

| 15.1 |

| 14.1 |

| McCormick & Co ( MKC ) |

| 29.5 |

| 30.8 |

| 21.5 |

| Tyson Foods ( TSN ) |

| 7.2 |

| 8.7 |

| 5.4 |

| Cal-Maine Foods ( CALM ) |

| 5.6 |

| 5.5 |

| 3.3 |

Takeaway

Based on the data available, I will say that I find myself intrigued by Nathan’s Famous. Using data from 2022, the company looks just cheap enough to normally warrant a soft ‘buy’ rating with me. Having said that, I have doubts about the firm's ability to continue to generate heftier profits than it historically has. Add on top of this the mixed operating history the business has demonstrated and how it's priced compared to similar firms, and I feel as though a more appropriate rating at this time is a ‘hold’ to reflect my view that the stock should perform along the lines of what the broader market should.

For further details see:

Nathan's Famous Stock: Not As Tasty As The Hot Dogs