TD - National Bank of Canada: Things Are Slowing Down

Summary

- In 2022, National Bank of Canada reported solid earnings growth of 11% YoY with positive operating leverage.

- But underneath this headline number, things actually seem to be slowing down at National Bank of Canada, as Q4 earnings were down 4% YoY, driven by an increase in provisions for credit losses.

- Growth is expected to slow going forward, and since National Bank of Canada is trading at fair value, there is no alpha to be made.

Dear readers/followers,

As you may know by now, I am mainly a Real Estate guy, but I like to diversify my real estate investment trust ("REIT") exposure into other sectors. One of those sectors that I have been fairly bullish on since last fall is Financials. I already own a handful of U.S. banks, but recently I became interested in diversifying my exposure into Canada, as I view some Canadian banks are extremely well-positioned and capitalized.

I already own Bank of Nova Scotia ( BNS , BNS:CA ), but looking at the price action of major Canadian banks, I couldn't help but notice that the National Bank of Canada ( NTIOF , NA:CA ) has outperformed all others over the past two to three years. In this article, I want to analyze its past performance and see how it's positioned going forward.

Financials

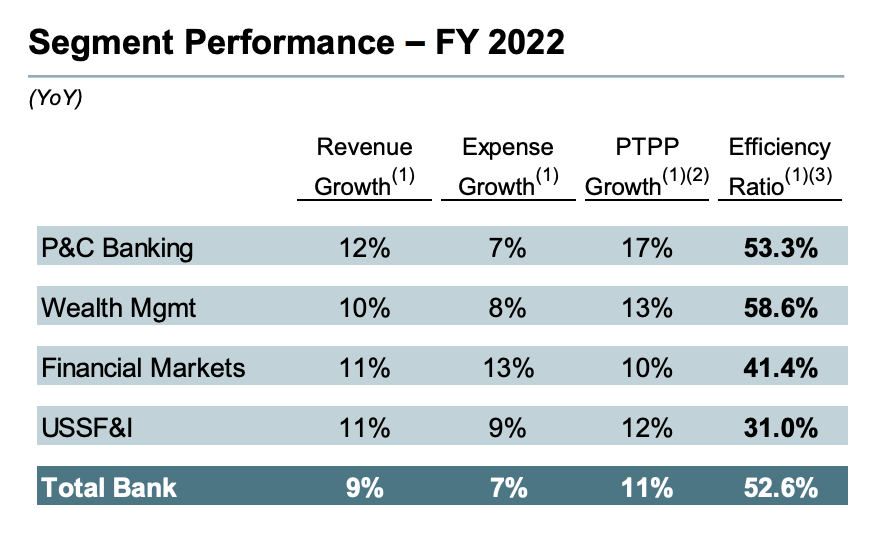

The National Bank of Canada reported solid fiscal Q4 2022 results , growing their topline revenue by 9.0% YoY while their PTPP Earnings (pre-tax pre-provision) increased by 11.4% YoY. These increases were driven by overall good results across all four segments that the bank operates in. Disciplined cost management resulted in positive operating leverage of 2.1% as expenses increased by only 6.9%.

{kind=link}

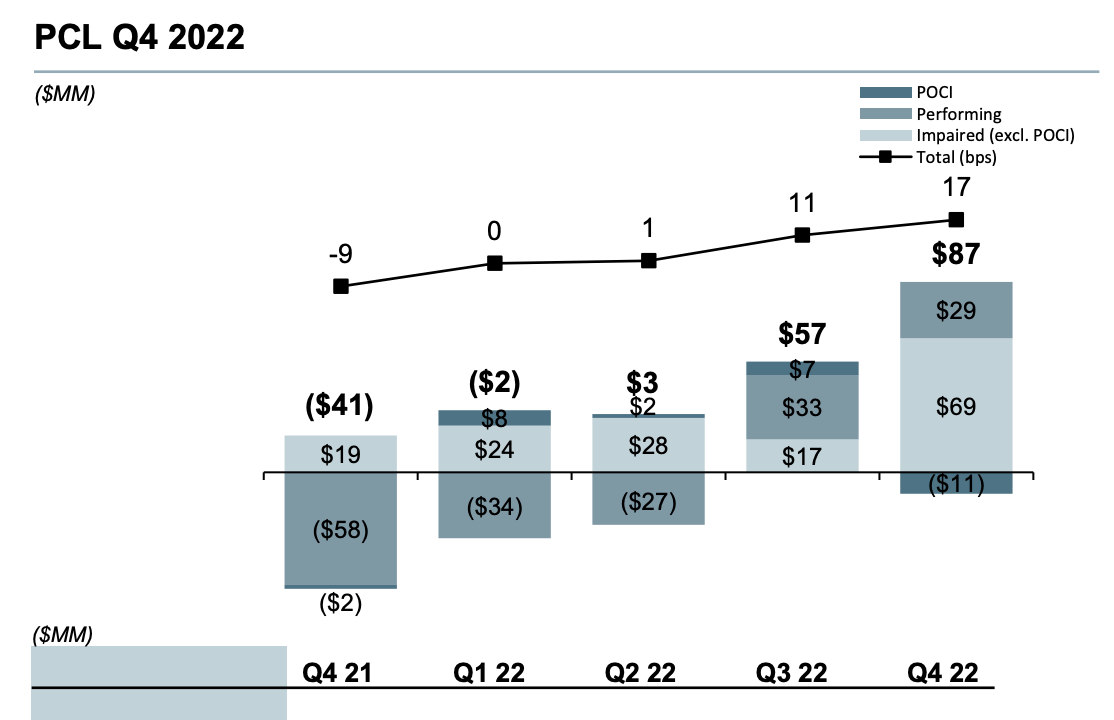

Those are pretty good overall results, but when we look closer, we actually see things slowing down. In particular, in Q4 2022, earnings were down about 4% YoY ($2.08 vs $2.17 per share in Q4 2021) largely because of an increase in provisions for credit losses that continued to climb throughout 2022 and reached $87 million in the final quarter. This is a significant increase when compared to total net income of $738 million in Q4 2022.

{kind=link}

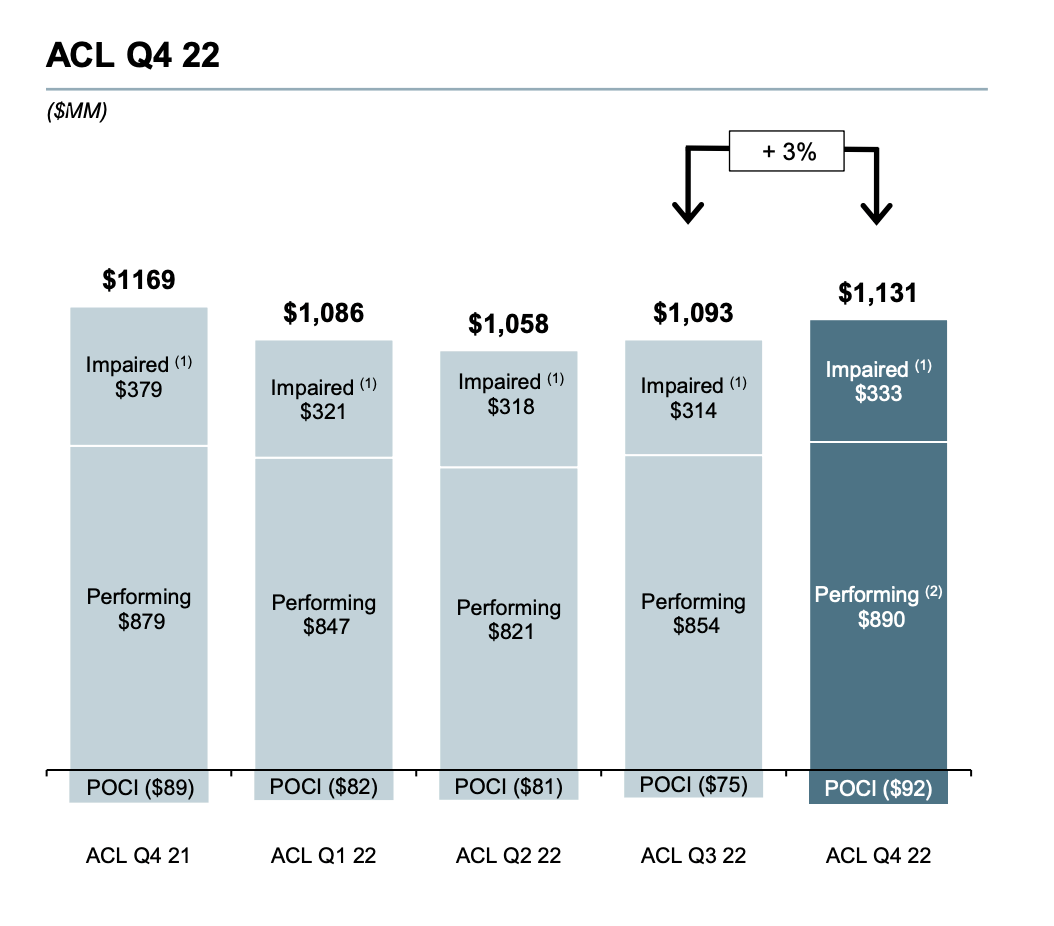

Of course, this is not unusual during times of deteriorating macroeconomic conditions. Increasing interest rates are acting as a double-edged sword, increasing the bank's revenue as it's able to charge higher interest on some of its loans but at the same increasing the proportion of loans that fail, leading to provisions for losses. Banks know this, so they try to prepare by putting aside money into an allowance for credit losses ((ACL)). National Bank of Canada has increased its ACL by 4% QoQ as they try to maintain a prudent level of allowances in light of continued uncertainties. Their current allowances remain about 47% above pre-pandemic level.

{kind=link}

To sum up, the bank had a really good year in all of its segments, but things seem to be slowing down as the macroeconomic situation worsens and rates increase. This environment allows the bank to charge higher interest to its clients but poses a risk that if rates become too high, demand for loans will drop. Moreover, it forces the bank to increase its ACL significantly in anticipation of loan defaults. In short, the bank could be in for a bumpy few years if inflation doesn't go away and/or the economy falls into a recession. For this reason, analysts are forecasting only modest growth of around 3% annually for the next two to three years, and I agree with the prediction.

Valuation

I like to evaluate banks on two metrics - price to earnings and price to book. I like to compare the price to earnings ratio to that of peers and also to the historical average of a given company. National Bank trades at 10.14x earnings, which is on the higher end when compared to peers, with only RBC trading higher at 12.1x earnings. BMO is the outlier here, but other than that I would consider a P/E of 9-11x as fair when compared to peers, so on this front the bank seems fairly valued here.

Comparison to its own historical averages paints a similar story. The current P/E multiple of 10.14x is only slightly below the historical average range (3-, 5-, and 7-year medians) of 10.7-11.0x.

In terms of price to book, the bank currently trades at 1.73x compared to an average of 1.63x for all 5 major Canadian banks. Ideally, we want P/B to be as low as possible and ideally below one, but that isn't the case for any Canadian bank. BNS and BMO have the lowest P/B multiples, which goes hand in hand with their lower P/E ratios - this is likely because they're expected to grow slower compared to the other three banks. Relative to its own historical average, the current multiple is slightly below the historical average range (3-, 5-, and 7-year medians) of 1.79-1.81x. In summary, I see the stock as fairly valued.

| Bank |

| Price to book |

| National Bank of Canada |

| 1.73x |

| Toronto-Dominion ( TD ) |

| 1.72x |

| Royal Bank of Canada ( RY ) |

| 1.93x |

| Bank of Nova Scotia |

| 1.37x |

| Bank of Montreal ( BMO ) |

| 1.41x |

| Average |

| 1.63x |

With the stock fairly priced, the expected total return will have come from the dividend yield + earnings growth. With a dividend yield of 3.8% and earnings expected to grow by only about 3% per year for the next two to three years, the overall return is likely to only be around 7% annually.

Verdict

National Bank of Canada had strong results in 2022, but if we look closer we start to see things slowing down significantly, mainly due to increased provisions and allowances for credit losses. National Bank of Canada's fast growth in earnings might be over for now, and the bank might be in for a few bumpy years before the economy stabilizes and inflation comes down. The stock had a decent 20% run from its October lows and is now fairly valued. With no multiple expansion in sight and a relatively low expected growth of 3% per year, I see no alpha here, and, therefore, rate National Bank of Canada at a "Hold" at $75.00.

For further details see:

National Bank of Canada: Things Are Slowing Down