CNK - National CineMedia Soared 115% With 362 Million Shares Traded: Insight Into The Ch.11 Bankruptcy Filing

2023-04-13 09:25:00 ET

Summary

- National CineMedia soared 115% because shareholders are not being wiped out in Ch.11 bankruptcy.

- A critical hearing, which I attended via Zoom, was held very late on April 12 that clarified a number of issues.

- A critical contract with Regal Cinema, which is owned by bankrupt Cineworld, is a major hurdle.

- National CineMedia, Inc. is paying $15 million for 13.8% equity in the newly organized entity and secured creditors are getting 86.2% under the RSA.

- Unsecured noteholders get 5-year warrants under the condition that an official unsecure creditor committee is not appointed by the U.S. Trustee.

There has been a lot of confusion regarding National CineMedia, Inc ( NCMI ), that owns 98% of National CineMedia LLC, which filed for Ch.11 bankruptcy on April 11. After reading various docket filings and attending the First Day Hearing that was held very late on April 12, I hopefully will be able to clarify the status of this very complex bankruptcy. With 372 million shares traded yesterday, there appears to be significant interest in the bankruptcy proceedings in this in-theater advertising company.

AMC Transaction Clarification

Before starting on this bankruptcy case, there needs to be some clarification on the recent AMC Entertainment Holdings ( AMC ) filing. AMC did not actually buy NCMI shares. Some traders thought AMC was buying the stock based on the 13G filed on April 10 - wrong. AMC received 16,581,829 NCMI shares under the terms of Exhibitor Services Agreement -ESA. AMC did not actually buy the shares in the market. This was also explained in a March 29 8-K filing.

Bankruptcy Filing and RSA

National CineMedia, Inc. itself did NOT file for bankruptcy - 98% owned National CineMedia, LLC did file for bankruptcy (case 23-90291) in Texas late on April 12. Judge David Jones was assigned the case. (Note: I think he is one of the best current bankruptcy judges. I don't expect any irrational rulings by him.) The Declaration by the CFO Ronnie Ng ( docket 14 ) contains the restructuring support agreement - RSA.

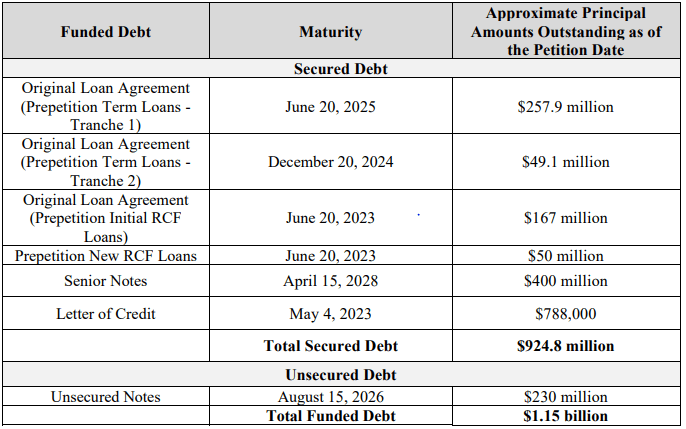

These are the recoveries under the RSA :

* National CineMedia Inc, which is what NCMI shareholders own - National CineMedia Inc will use $15 million cash on hand to buy 13.8%, subject to dilution, of the equity in the newly organized LLC. Technically they are not actually getting a direct recovery for their 98% ownership. The RSA even states "shall receive no recovery on account of such Interest in the Debtor and such Interests shall be cancelled." They are "only" getting the ability to buy $15 million of the new LLC. If that 13.8% is actually worth more than $15 million, some might try to assert the difference is a de facto recovery. That is what a lawyer representing a group of unsecured noteholders asserted at the hearing held very late on April 12 (a hearing a PDF file recording is available on docket 75). Since creditors with higher priority are not getting full recovery, this would be a violation of the absolute priority rule section 1129(b)(2) unless the classes receiving less than full recovery vote as a class to approve this "gifting". It seems at this point, some of the unsecured noteholders might be against this based on the lawyer's statement.

* Secured debt holders are getting 86.2%, subject to dilution, of the new equity in the LLC. All the secured debt is being equitized.

5.875% 4/15/2028 Mortgage Bonds

finra-markets.morningstar.com

* Unsecure noteholders get 5-year warrants There is, however, a major condition - no appointment by the U.S. Trustee of an Official Unsecured Creditor Committee. These committees are very expensive and often spend $10 million on professional fees according to statements at the recent hearing. "...if a Creditors’ Committee is appointed, holders of Unsecured Funded Debt Claims shall receive no recovery or such recovery as to be agreed upon by the Required Consenting Creditors and NCM." (I like this idea. Too often professional fees are so high that they have a very negative impact on actual unsecured creditor recoveries.) The lawyer representing unsecured noteholders at the hearing stated he wants a committee appointed. The U.S. Trustee lawyer also strongly indicated a committee will be appointed. It is sort of funny, but Judge Jones liked the idea of perhaps not having a committee and that unsecured creditors should decide - as is his style, he joked about this.

5.75% 8/15/2026 Unsecure Notes

finra-markets.morningstar.com

Long-Term Debt

{kind=link}

Major Issue - Bankrupt Regal Rejecting the ESA

This in-theater advertising company was formed in 2005 by AMC, Cinemark ( CNK ), and Regal Cinema, which is now owned by bankrupt Cineworld Group ( CNNWQ ) and then eventually went public a few years later. A major issue in this bankruptcy case is that Regal's parent company is also in bankruptcy. There is a very critical Exhibitor Services Agreement - ESA between all three movie theater companies and National CineMedia LLC. Regal wants to reject ( Cineworld docket 576 ) that agreement under section 365(a) . Much of the hearing on April 12 covered this issue.

One of the problems is that Judge Marvin Isgur is handling the Cinemark bankruptcy case and Judge Jones is handling National CineMedia. A hearing on this ESA contract rejection was set for April 13 before Judge Isgur, but Judge Jones and Judge Isgur communicated during the hearing last night, which is very unusual. Judge Isgur agreed that there would not actually be any arguments heard on April 13. Regal wants better terms or even to completely cancel the ESA. Lawyers for National CineMedia stressed in court that the ESA with Regal is "vital" to their business going forward.

There is confusion regarding the rejection of the ESA by Regal and the National CineMedia RSA list of conditions. Regal actually accepting the current ESA is not a condition, even if some of the wording implies that. The condition, Regal Approval Order, means, in general. that there can be a new Regal ESA as long as National CineMedia creditors consent. Regal does not have to accept the current ESA contract as a condition under the RSA. Even Judge Jones initially thought that was one of the RSA conditions. This is critical because it is extremely unlikely that Judge Isgur would not allow Regal to reject the ESA because that is their right under section 365(a). If that was an actual condition, this RSA would be DOA, in my opinion. I expect there will be negotiations and some modifications followed by an eventual new ESA.

RSA Milestones

cases.omniagentsolutions.com

Valuation of New Equity

There seems to be a potential arbitrage trade. Using the effective number of 181,235,640 NCMI shares, after converting all units to stock on a 1 for 1 basis, according to the filing by AMC and the latest NCMI price of $0.44, the total equity value is $79.7 million. (The number of shares could increase under the terms of the various agreements with the three theater companies.) This compares to only $15 million being paid for 13.8% new equity. This $79.7 million implies a total value of $578 million without factoring in potential of additional shares or dilution. With secured debt trading at about 30 cents on the dollar, the market value of the secured debt is $277 million. Using the 86.2% and $277 million, the secured debt traders are implying a $321 million valuation.

A classic arbitrage trade would be to sell short NCMI and buy secured debt. Given the current irrational meme trading in bankruptcy stocks and the cost to carry the short side of the trade, I am not doing this trade.

Conclusion

This is a rather complex Ch.11 bankruptcy case. The parent company, National CineMedia Inc., is not in bankruptcy, but 98% owned limited partnership, National CineMedia LLC is in Ch.11. Technically the parent company is getting no recovery, but is being able to purchase 13.8% equity in the new LLC for $15 million. A party to a critical contract is also in Ch.11 bankruptcy and is trying to reject that contract. Unsecured noteholders get warrants under the condition the U.S. Trustee does not appoint an Official Unsecured Creditor Committee, but the Trustee seems that she would rather "play by the book" and appoint one, even if it could mean less recovery for unsecured claim holders.

There is currently an arbitrage between the valuation implied by equity traders and secured debt holders. Given all these complexities, I am rating NCMI securities neutral/hold until we get better clarity on a number of issues.

For further details see:

National CineMedia Soared 115% With 362 Million Shares Traded: Insight Into The Ch.11 Bankruptcy Filing