NGGTF - National Grid: Long-Term Play But Lacking Upside

2023-04-26 00:29:47 ET

Summary

- National Grid plc is a company that provides electricity, gas transmission, and distribution services.

- NGG has grown through acquisitions and incremental pricing improvements.

- The business is investing heavily in capex, as it builds the clean energy infrastructure of the future.

- Margins are fantastic and forecast to improve, generating cash primarily for capex but also to support good dividends.

- NGG is trading at an EBITDA premium to its peers, suggesting no upside based on our assessment.

Company description

National Grid plc ( NGG / OTCPK:NGGTF ) is a company that provides electricity, gas transmission, and distribution services. It operates in the following segments: UK Electricity Transmission, UK Electricity Distribution, UK Electricity System Operator, New England, and New York.

National Grid is a strategically important business in the UK as the provider of electricity and gas across much of the nation, but is also an important part of US infrastructure, with its operations in NY and NE.

Share price

NGG's share price has traded sideways in the last decade, with the business experiencing improving financial performance but offset by commitments to improving national infrastructure, reducing potential distributions.

Financial analysis

{kind=link}

National Grid Financials ( Tikr Terminal )

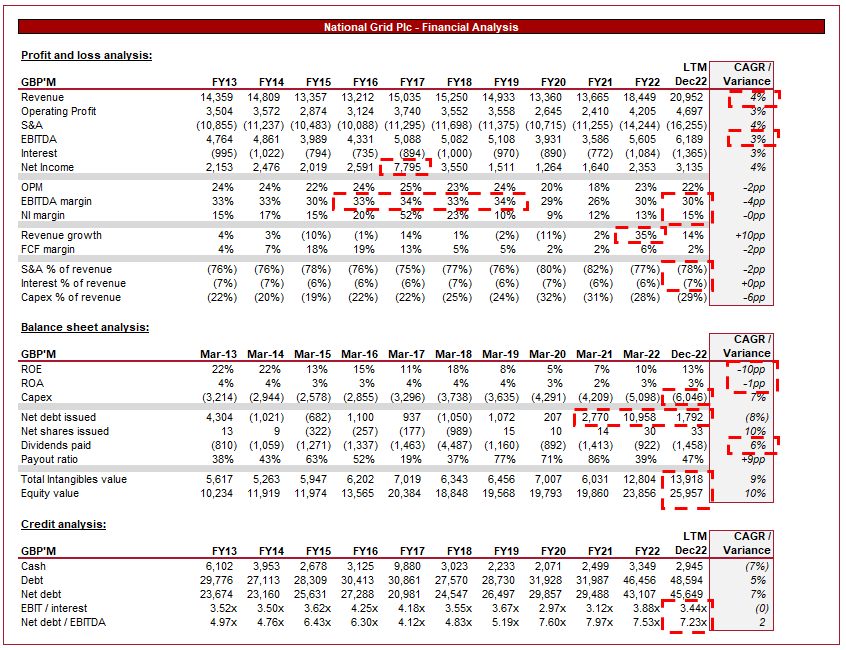

Presented above is National Grid's financial performance for the last decade. The business has grown extremely well, while also investing heavily in National infrastructure.

PL

Revenue has grown at a CAGR of 4%, supplemented in large part by acquisitions across the historical period. As an energy provider, NGG operates in a highly regulated market, which restricts its ability to price aggressively. In New England for example, NGG has achieved annual rate adjustments.

A large revenue driver was the acquisition of Western Power Distribution , which is the largest electricity distribution network operator in the UK. This was offset by the sale of its Rhode Island gas and electricity business. In a commoditized business such as this, it is key that NGG continues to acquire quality businesses as a means of growing beyond inflation.

As climate change becomes a major concern globally, the shift towards renewable energy and decarbonization is increasing. The UK government has set a target of net zero carbon emissions by 2050, which means NGG will need to invest a significant amount in the modernization of the UK electric grid. This is an ongoing process but NGG is progressing well, generating improving returns from clean energy. An example of this is Interconnectors, which has seen a 153% increase in operating profit between H1'23 and H1'22, intending to have 90% of the energy imported by interconnectors be from zero-carbon energy sources.

Current inflationary conditions have also contributed to improving revenue in the most recent year. Much of the inflation we are seeing stems from energy prices, as the Russian invasion of Ukraine has thrown the world's energy market into chaos. The UK's current inflation rate is 10.4%, showing a stubbornness in its decline.

With significant non-GBP exposure, NGG continues to have FX risk with the translation of its income to Stirling. This is somewhat offset in the US due to its Dollar-marked debt.

H1'23 revenue (National Grid)

Due to the regulated nature of the business, margins are somewhat constrained in how they can move. As a result, much of the movements are a reflection of the company's product mix at any one time. We note a decline in EBITDA-M in the latter part of the decade, likely driven by the sale of the gas segment. Further, we see things improving in the last 2 years, which WPD has likely contributed to.

Overall, our view is that the company's profitability profile is highly attractive and its relative stickiness cannot go without saying.

Balance sheet

Moving onto the balance sheet, we see NGG raising a substantial amount of debt in most years, experiencing periodic bouts of deleveraging. This is a reflection of how the company must operate, with substantial investments in infrastructure. Capex spending has grown at a rate of 7%, representing 29% of revenue in the LTM period. This investment will yield future returns as these assets come online and begin generating returns but will be a consistent drag on cash over time.

Further, NGG sold a 60% stake in its Gas business to a consortium led by Macquarie, with the sale agreed at £9.6BN. Interestingly, the consortium has the option to purchase the remaining 40%. This would put critical UK assets in the hands of foreign owners, which could come with scrutiny and potentially hamper any future deals. Our view is that these assets are key to the value of NGG, but understand that assets will need to be sold over time as a means of funding future expansion and deleveraging the business. The reality is a compromise needs to be found between the quality of existing assets and the infrastructure investment that is required to modernize domestic assets.

Dividend payments have grown at a respectable 6% but have experienced periods of fluctuation as the business executes its strategic initiatives. The current payout ratio sits at only 47% but does not factor in the cash cost of capex, which will continually be required. It is unlikely that we will see dividends grow beyond the inflation rate.

These factors have contributed to an ND/EBITDA ratio of 7.2x. Our default view for most businesses is that a 3x level is a maximum, suggesting NGG is substantially overleveraged. Some nuance is required here, however, given how sticky revenue is and how profitable the business is. Current EBIT coverage suggests the business is operating at a similar level to most of the 2010s, a period of good profitability. Fitch currently rates the company a BBB+ .

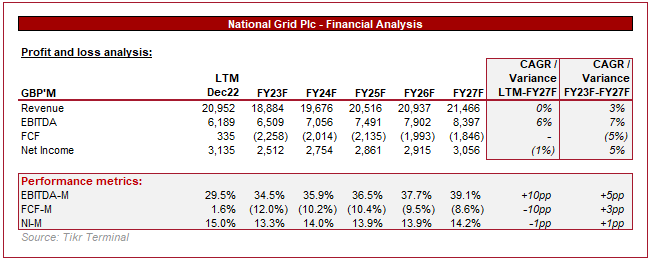

Outlook

{kind=link}

National Grid outlook ( Tikr Terminal )

Presented above is Wall Street's consensus view on how the next 5 years will unfold.

Revenue growth is expected to be mild, growing at the long-term inflation rate of 3%. This looks to be a conservative view of the business, with no M&A or substantial assets coming online expected, which looks reasonable.

Margins are expected to expand impressively, returning to their peak level. This will alleviate some of the debt pressures as capex spending continues.

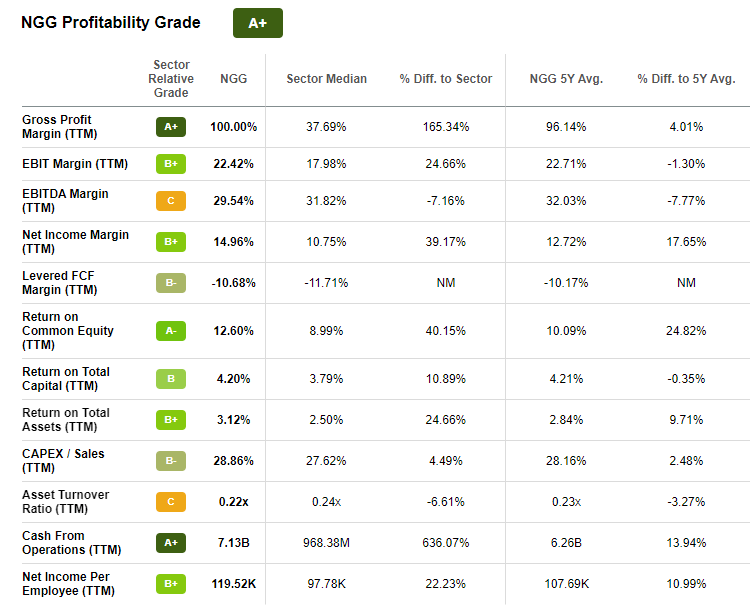

Peer comparison

In order to assess NGG's relative performance to the market, we have compared the business to the utility sector utilizing Seeking Alpha's grading system.

{kind=link}

Profitability (Seeking Alpha)

As we mentioned previously, NGG's profitability is fantastic. This is reflected in its A+ grade, with the business substantially more profitable than its peers. This score is skewed by the company's GPM and scale ((CFO)) but importantly is generating more NI and a greater EBIT.

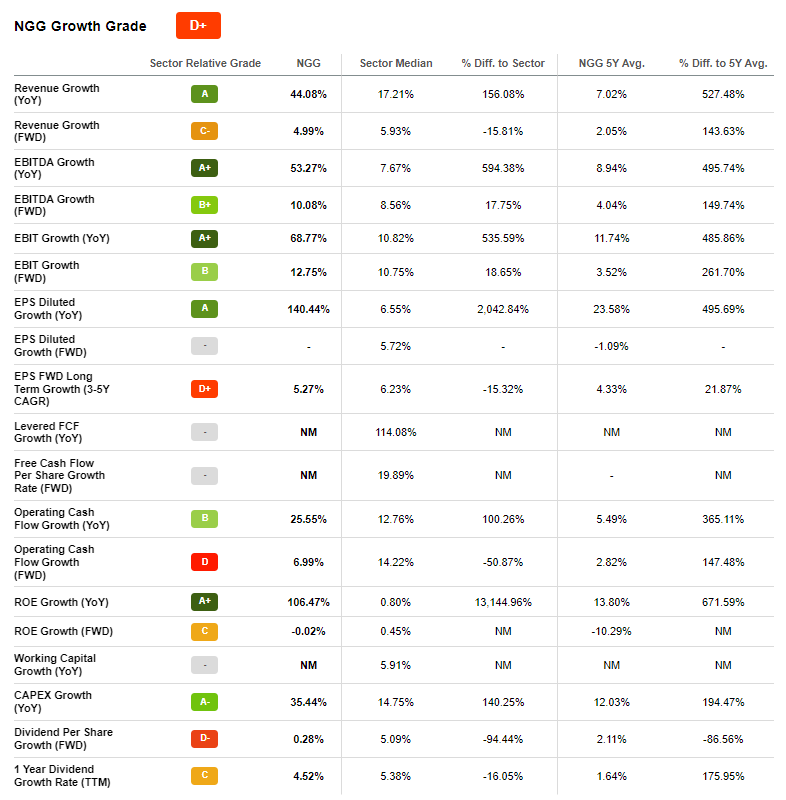

{kind=link}

Growth (Seeking Alpha)

NGG scores far worse on growth, primarily because of dividends and EPS forecasts. We would argue that this is harsh as on a forward revenue and EBITDA/EBIT basis, the business does just fine.

Valuation

Based on the factors we have discussed, we would expect NGG to be trading at a slight premium to its peers. Profitability will always be superior to growth when comparing mature businesses, as the growth delta will likely never compensate for the profitability difference, which is the case here.

{kind=link}

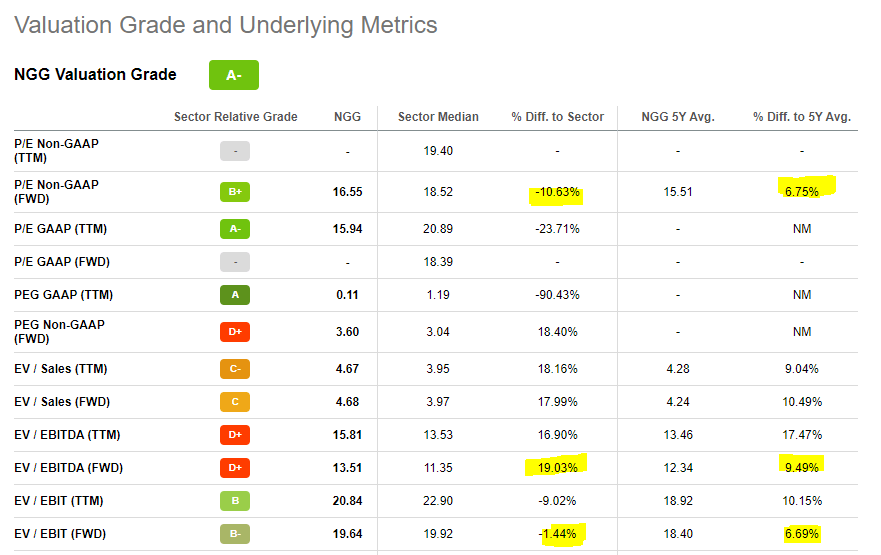

Valuation (Seeking Alpha)

NGG stock is currently trading at a 19% premium to its peers and a 10% premium to its 5-year average on an NTM EV/EBITDA basis. NTM EV/EBIT and non-GAAP P/E both marginally suggest the opposite (-1.4% & -11%), although NGG continues to trade at a premium to its 5-year average (7% & 7%).

Our view is that there is some upside here, but unlikely to be a substantial amount given the business is showing a premium valuation. Investors looking for a pure-income play could do well with a current yield of 4.4%.

Final thoughts

NGG is a strategically important business that will contribute significantly to building the future energy infrastructure of the UK. We are currently in a once-in-a-lifetime energy transition as the world moves toward clean energy. This poses a financial risk to the business from a financing perspective, but equally an opportunity for growth.

We like the profitability, Management, and the company's outlook. Our only real issue is that the valuation does not leave investors with much room for upside. This said, those looking for just income will win with NGG.

For further details see:

National Grid: Long-Term Play, But Lacking Upside