NGG - National Grid: Regulators Cap Upside In The U.K.

2023-09-26 06:54:24 ET

Summary

- Ofgem have put regulated WACCs at pretty low levels, limiting the UK business from benefiting from incremental growth due to electrification investments.

- We think NGG operates in quite an oppressive environment in the UK, but at least they have almost 50% of profit from the US and are piling in CAPEX there.

- While the US business improves the NGG picture, the blended business setup, particularly the return-over-WACC wedge, is not that great.

- Investors can do better than a high capital intensity and weak return company at a 13x PE in the current markets.

National Grid (NGG) is probably fairly valued right now, but only because of its US business. Regulated utilities can be great when regulators go along with the fact that inflation requires higher regulatory WACCs. We feel that the UK's Ofgem has been a bit too harsh, and it proves that NGG's operating environment involves a regulator that will limit the upside on the UK business. We don't see particular appeal of NGG at current prices, and rate it a hold. Operating income can only grow if CAPEX grows in these sorts of regulated utility businesses, and the small wedge between cost and return of capital limits how much incremental shareholder value can be created by growth opportunities in electrification. At least there is substantial US exposure for National Grid, and in the US the problems of an oppressive Ofgem are not present. We pointed out the usefulness of a non-US exposure in our last article on NGG some time ago where our view of Ofgem has only gotten worse considering rate hikes and developments in baseline cost of capital assumptions for all other sectors and securities. They will be able to create incremental shareholder value there, but in the UK it remains the case that the returns for the investments that will be required to equip UK networks won't be worth the investment based on market cost of capital figures. While a blended wedge over WACC at around 2% is alright, it's nothing to write home about either in the current environment where there are plenty of on-sale equities. The PE looks somewhat fair, but if there is any electrification premium in NGG, it's not really deserved considering the investment dynamics, and for those reasons we don't see any upside.

NGG and Ofgem Comments

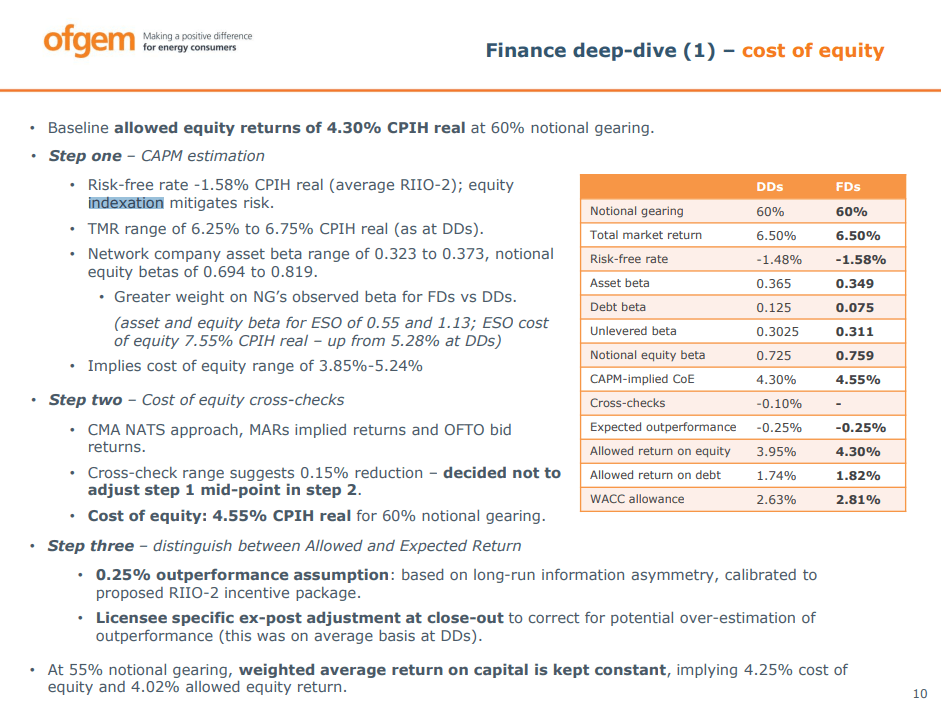

Regulated utilities usually all work the same way. The national regulator of the transmission and distribution of electricity and usually also gas determine a regulated WACC or cost of equity, that is used to compensate regulated utility companies, which have been given concessions to operate these public utilities, for investments that they make in the assets they operate.

The regulated WACC should be based on the risk-free rate as well as some amount of risk premium for the value-add that comes with actually having to execute the investments and improve these utilities, so they can serve the public and their changing needs. Usually CAPM is used, and there may be some benchmarking and indexation. For transmission and distribution concessions, it is especially important in light of the renewable transition, where electrification will be putting more pressure on the grid.

Ofgem made its final tariff determinations that for some years already have been subject to appeals by National Grid for making the compensation more 'fair' in National Grid's eyes. Costs of capital due to Western rate hiking have continued to increase, and have made the determination by Ofgem even less attractive. The previous period's regulated cost of equity based on the notional gearing is 7% . That's quite high considering where benchmark rates used to be. Clearly, Ofgem feel they overpaid NGG in the last period, so now it's around 4.5% , so less than before. Due to rate hikes that appear to be higher for longer, 5.25% is the current benchmark rate for the BoE which serves as the benchmark rate for debt, where cost of debt should always be lower than the cost of equity. Regulated costs of capital are the returns that NGG make on its investments in the UK, and having a 4.5% as the cost of equity is not a good start to get a fair WACC. The figures are determined in typical CAPM fashion and there is some indexation to inflation and rates but to long-term and insensitive benchmarks. The starting point is pretty low considering how much the rate environment has changed, certainly beyond Ofgem and NGG's expectations at the time of the final determinations.

{kind=link}

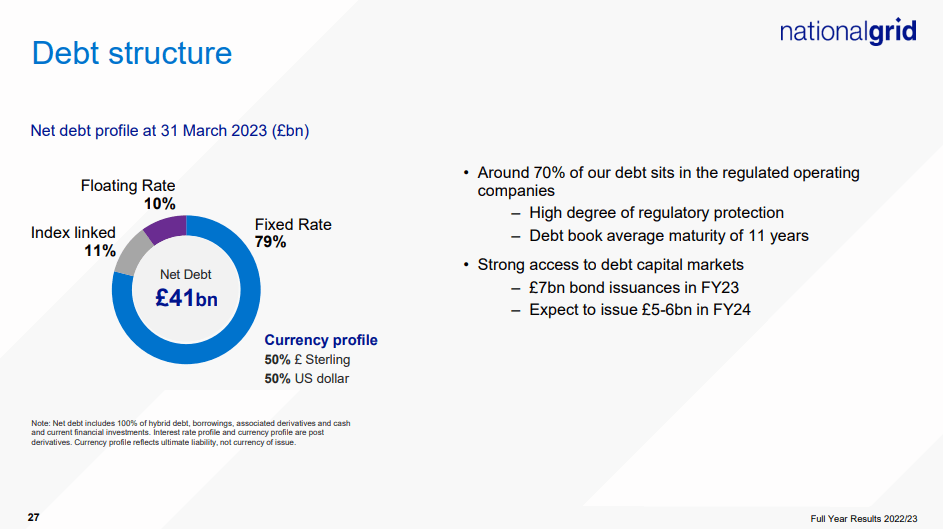

As said, National Grid is appealing this figure, and mentions that the future of their company involves higher CAPEX and lower returns, which is not a good combo. Note that Ofgem only regulates the UK business, and that at least the long-dated current debt structure established before rate hikes does allow for a wedge in performance, but remember that it's the marginal figures that always matter in economics and marginal cost of capital is not being well covered by the regulated WACC.

{kind=link}

Ofgem has been more difficult than even the South American countries , and other nations whose public balance sheets are in worse condition. While there are some clauses for outperformance, and of course NGG can leverage to a greater degree than the notional level and does so at attractive and fixed rates, National Grid is simply not a regulated utility that is operating in a particularly friendly environment.

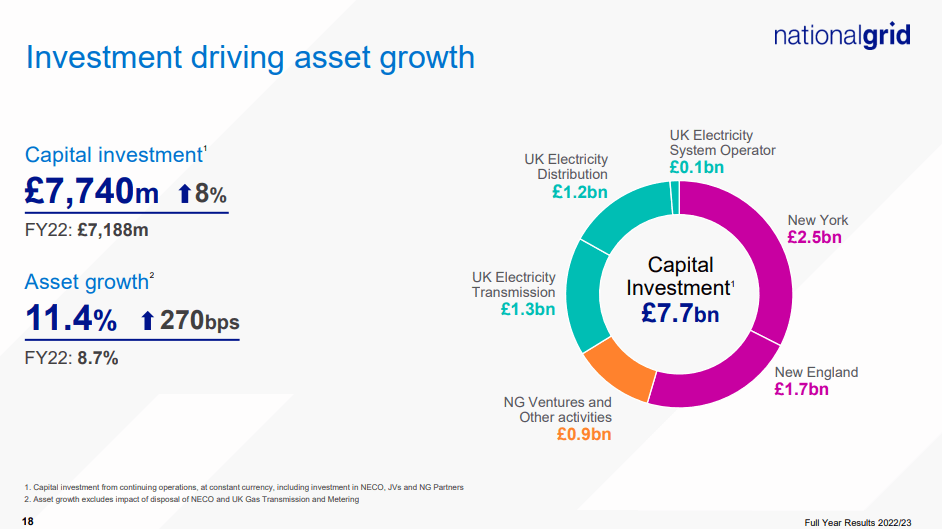

Around 38% of operating profit is coming from the US, where regulated returns on investments made into the regulated utilities comes at decent rates, around 9% for some recent projects. This is a blessing for the company and means at least the slightly more than half of their CAPEX being focused on the US will be capable of delivering shareholder value creation.

Even now we can see in their performance that incremental fixed capital investment, which is necessary to grow the regulated asset base and increase profits, is large compared to profit developments. Some investors doubtlessly believe that National Grid might be a good electrification play, but any secular growth provided by electrification in the UK concession is going to have to be provided by large CAPEX balances whose return is weak compared to benchmarks and indeed compared to its US concession, where benefits from higher investment required in the grid will at least be felt by investors. Incremental shareholder value creation, requiring returns to be higher than costs of capital, will mostly come from their New York and New England concessions in the US.

{kind=link}

Bottom Line

Higher capital intensity and weak regulated returns in their still important UK business, which by the way also needs maintenance investment, means that NGG's debt is growing more quickly, and their operating cash flow is already exceeded by the current rate of CAPEX, half of which is in the UK. The forced reinvestment in the UK for maintenance and some RAB growth comes at a WACC that is unappealing. While appeals may work, the fact that it's such a pain to get appropriate WACCs in the industry should be a red flag for investors. The CNMC in Spain is quite similarly investor unfriendly. They are more extreme than Ofgem, and that is why their regulated utilities are cheaper. In some other geographies, regulated utilities have been nice, since they see higher inflation and rates be acknowledged in tariff reviews. For the time being, Ofgem have made NGG unhelpful in this regard. The only real value lever is being able to leverage its assets which is not the most encouraging investment set up and well as pile in entirely to the US concessions, but the whole UK business will not be able to benefit from electrification trends since the return bestowed for equipping that network won't be worth the capital required to conduct those projects.

US and UK CAPEX (Q4 2023 Pres)

{kind=link}

For valuation, we avoid a complex model. Just consider the earnings yield at around 7% based on current PEs. While the earnings are not really at risk since the concessions are safe and financed by prominent national balance sheets, the quality of earnings isn't very high due to capital intensity. A 7% earnings yield isn't great in the current market considering benchmark risk-free rates are closing in on 5% in most Western geographies. To get more technical, what matters is the discussion of incremental shareholder value creation, which is a technical DCF concept and standard that determines how much shareholders benefit from additional sales, or if they even suffer from additional sales which is possible too. Investors likely think that NGG is some sort of electrification play, but if returns on capital are equal to or lower than cost of capital for the UK business, electrification investments in the UK will not add value to shareholders, they could even detract value. Moreover, fixed capital intensity is very high, which means limited benefit from sales growth even if returns > WACC, and more intense value destruction if WACC is greater than the return. While there is a decent wedge in the US business, likely around 3-4% based on their returns for recent projects, with almost a 0% or even negative wedge in the UK given Ofgem figures and recent rate developments which may become the status quo due to deglobalisation and other inflationary factors, the blended wedge is around 2% over WACC for NGG which is not that great considering it's also a naturally capitally intense business. With more capital intensity, you'd want the negative cash flow effect from high CAPEX to at least interact with a higher return, like in an industrial business. 2% is not good compared to the benchmarks we're used to for industrial projects, which usually have substantially higher excess returns than that. Because of the weaker earnings quality and sub-par investment returns from forced investments in the UK concessions, we just don't see NGG as a smooth ride, and think we can find better companies with higher quality earnings in the 12-14x PE range. At least their business is safe (at least until the next Ofgem review in 2028), and for that, we understand that there'd be some market for the stock at current prices. But we just don't see any upside and would rather look at companies with more of an angle.

For further details see:

National Grid: Regulators Cap Upside In The U.K.