NHC - National HealthCare: An Ultimate In Defensive Overlay For Equity Portfolios

Summary

- National HealthCare is just about as defensive as they come with respect to shareholder returns.

- The company lends investors a potential defensive overlay into equity portfolios as a stabilizer of returns.

- Our findings show NHC justifies its inclusion in an equal-weight balanced portfolio, from constant weight down to 2% of the equity risk budget.

- Shares look fairly priced up to $77.80, and valuations open up further when making necessary adjustments to GAAP earnings.

- We rate NHC a buy and advocate its inclusion as a defensive overlay in equity portfolios.

Investment thesis

With volatility in equity markets set to remain in situ for the foreseeable future, we advocate investors start to shift up in the resiliency and quality spectrum. That means seeking out defensible names that will stabilize equity returns as a defensive overlay in equity portfolios.

With that in mind, we turn to National HealthCare Corporation ( NHC ) and demonstrate it has the features to meet this hurdle. Shares look adequately priced at current multiples and we have clarity into exactly what we're buying into with NCH as required adjustments to GAAP earnings are minimal. For those investors looking to clamp equity drawdown and reduce equity beta, NHC looks to be attractively priced to fulfil this mandate. From the data outlined below, we rate NCH a buy on a $77.80 valuation.

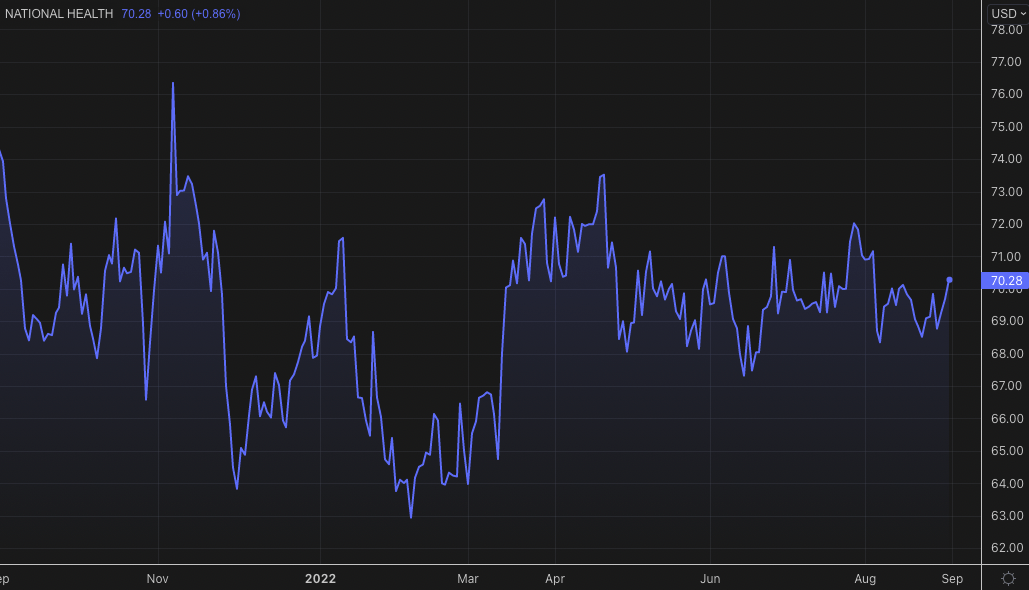

Exhibit 1. NHC 6-month price action

{kind=link}

Q2 earnings exemplify resiliency premium

Second quarter earnings were largely in-line with normalized results. The consistency in operating measures gives confidence in the accuracy of estimating expected returns for NHC, without drifting too far from the longer-term averages. Net operating revenue of $271.3 million was up ~310bps YoY and included a ~970bps YoY gain in net patient revenue. Of this amount, $227 million came from inpatient services and $32.3 million was from home and hospice revenue - up 124% YoY.

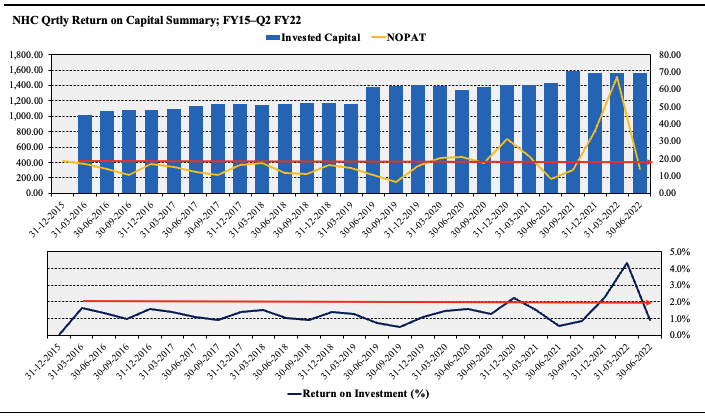

As seen in Exhibit 2, operating measures for the company have remained steady over the 7 years to date on a sequential basis. In keeping with our investment thesis on this name, the low earnings volatility has inflected to equally as steady share price returns, by estimate. The resilient nature of NHC's earnings to remain steady throughout various market cycles is the kind of exposure we advocate investors position towards in H2 FY22 in order to step up in the quality spectrum. Note, despite the fact net earnings decreased substantially YoY, this time last year, NHC booked a $95 million non-cash gain on acquisition in Q2 FY22.

Exhibit 2. Quarterly operating measures enhance the predictability of the company's future cash flows and improve the accuracy of valuation estimates

Data: HB Insights; NHC SEC Filings

Noteworthy is that FCF [net of dividends] has declined sequentially alongside FCF yields since FY19, as seen above. However, we also note that a declining or negative FCF yield is a desirable characteristic when the company's return on investment ("ROIC") comfortably exceeds its cost of capital and there is adequate capital available.

The size of the investment pool in NHC's valuation gives insights into the capital and labor intensity of the business. On inspection, it spent $4.97 on tangible assets to generate $1 of revenue last quarter but spent just $0.46 on labour for the same. It also spent more than $10 on its asset base per $1 of NOPAT generated. It also made a $1.56 billion capital investment to deliver $271 million in revenue and $14 million in NOPAT last quarter [17% and 0.9%, respectively]. From this perspective, the company's business model appears capital heavy.

In this regard though, NHC shines through and presents with compelling value. As seen in Exhibit 3, annualized TTM ROIC comes in at over 18% from quarterly results, a figure that has also remained steady to date. Here we examined the level of NOPAT generated from the last period's invested capital and noted equally as resilient results. As such, Q2 NOPAT earnings per share comes in at $8.45, and annualized ROIC easily beats the WACC hurdle of 4.02% by 4.5 turns. Therefore, whilst capital intensity is high, this is balanced by adequate return on investment of ~18% p.a.

Exhibit 3. Return on investment easily surpasses annual WACC of 4.02% by 4.5x

Demonstrates that capital intensity is reasonably high for the company on a tangible-capital basis [labour capital intensity is low vs. asset intensity].

{kind=link}

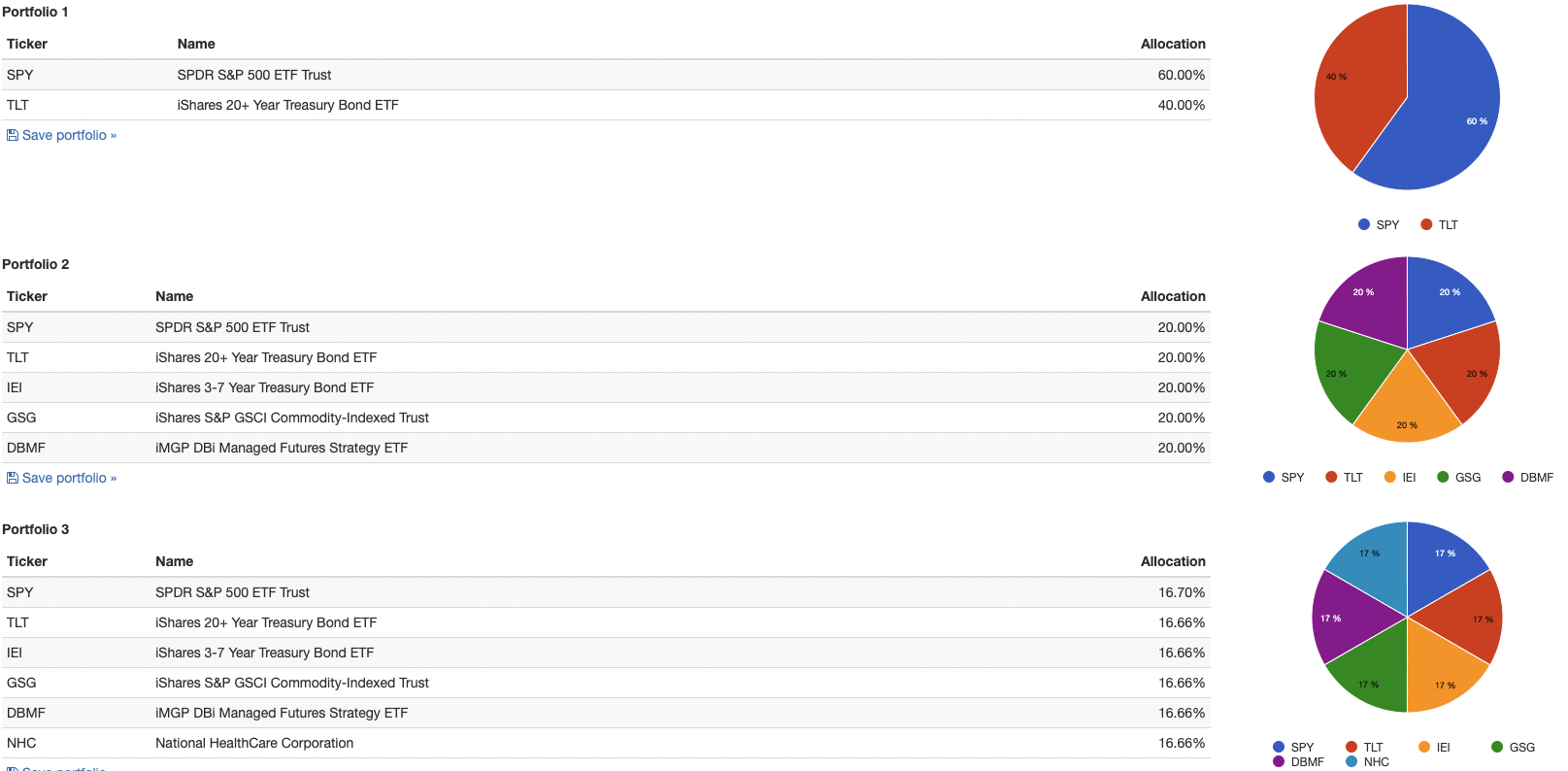

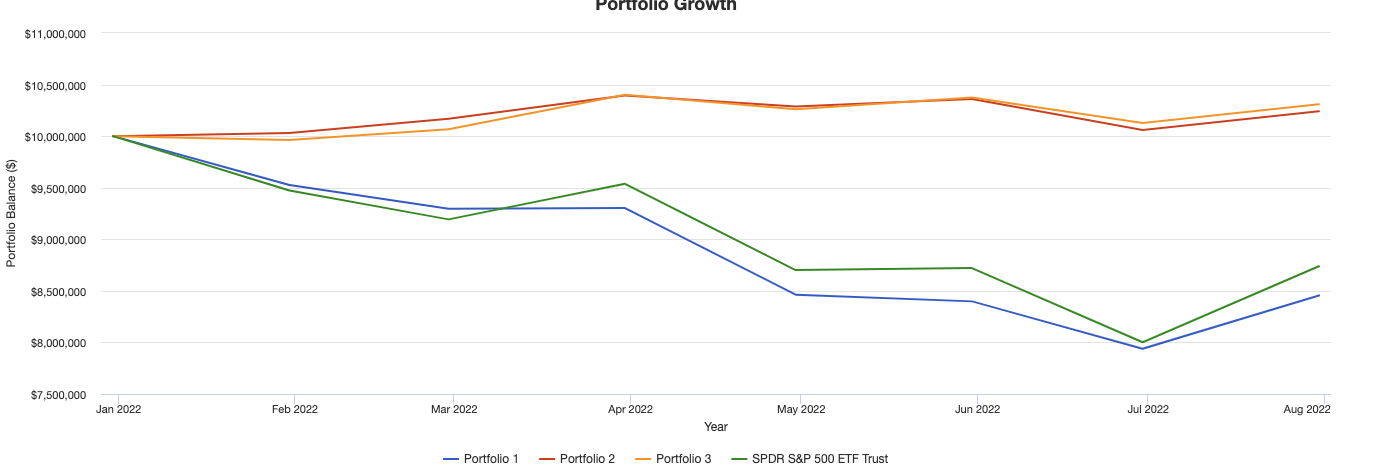

Portfolio backtesting

In order to perform the backtest sufficiently for insights about H2 FY22, we assume that the coming 6-9 months will somewhat resemble the period of January 2022-date from a macroeconomic perspective. In that vein, balanced portfolios - with a constant weight to alternatives - have outperformed benchmarks this YTD and clamped equity drawdown in the process. As seen below, compared to traditional 60/40 setups [portfolio 1], the balanced portfolio with equal weight to each risk budget [portfolio 2] has distributed a positive return of 2.14% versus the benchmark's -12.6% [alpha of ~10%], on a drawdown of 3.2% and standard deviation of 6.2%, with positive Sharpe and Sortino ratios.

Here we note the defensive premium of NHC. As seen in portfolio 3, that includes NHC on an equal weight basis to the equity bucket, returns increase by nearly 70bps whilst equity drawdown narrows by 140bps to just 2.6% with equal volatility of returns. However, this is a high Sharpe and Sortino strategy with ratios of 0.7 and 1.26, respectively. This trend continues in weighting NHC all the way down to 2% in the equity bucket.

This exemplifies our investment thesis for NHC. The defensive nature clearly shines through and stabilizes risk-adjusted returns. This is what has us trigger happy on the name, to add an overlay of resiliency into our equity risk.

Exhibit 4. Portfolio backtesting corroborates investment thesis of NHC as a defensive overlay to equity portfolios

Data: HB Insights, PortfolioVisualizer Data: HB Insights, PortfolioVisualizer Data: HB Insights, PortfolioVisualizer

{kind=link}

{kind=link}

{kind=link}

Reconciliations and valuation

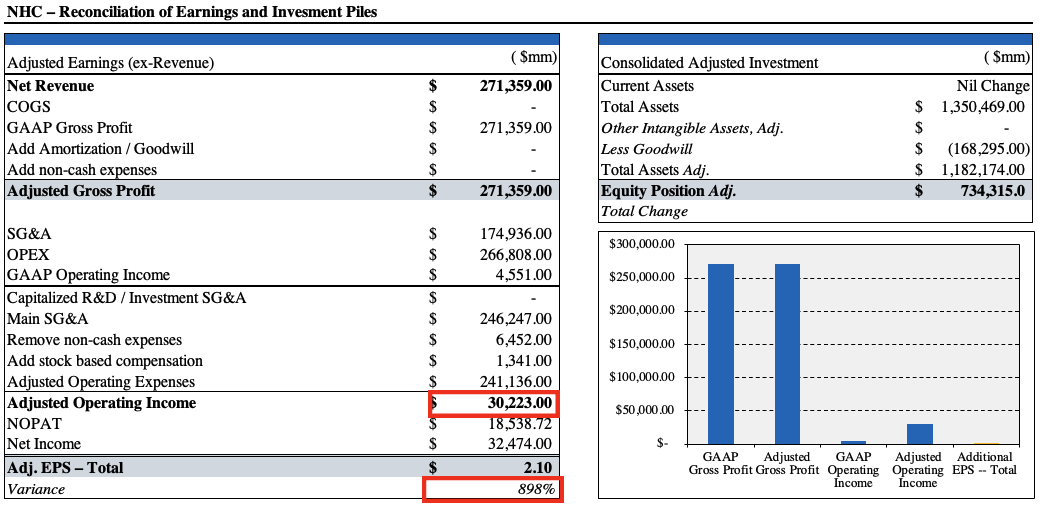

We've made the necessary adjustments to NHC's GAAP financials to reflect true cash earnings, as seen in Exhibit 5. In doing so, we reconciled $6.4 million in net non-cash expenses and included $1.3 million in stock-based compensation - itself down on the year. Post-adjustment, operating income lifts to more than $30 million, NOPAT to $18.5 million and earnings to $2.10 per share, up from GAAP EPS of $0.20. We also reconciled $168.2 million in goodwill on the balance sheet to produce an equity value of $734 million.

Exhibit 5.

Data: HB Investments US Equity Fund

{kind=link}

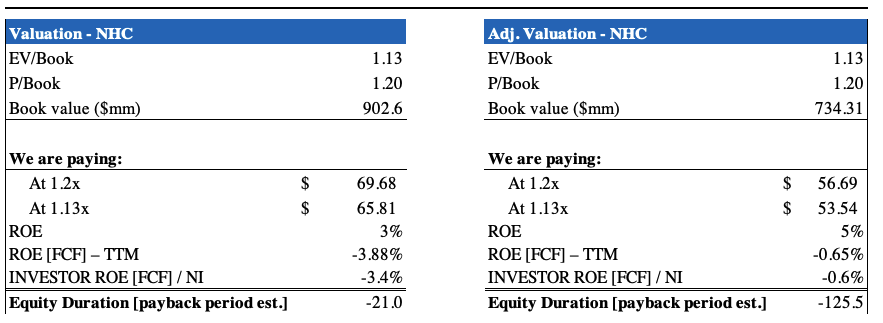

In this vein, we see compelling value in NHC in terms of the asymmetry in what we're asked to pay versus the potential value on offer. As seen in the Exhibit below, shares currently trade at a respectable 1.2x book value and 1.13x enterprise value ("EV") to book value. On these multiples, we'd theoretically be paying $65-$69, around about fair price.

However, post-adjustment, and at these multiples, the implied price we'd pay drops to just $53-$56. The question then turns to whether this does in fact represent a value gap to the upside.

Exhibit 6.

{kind=link}

In that regard, on our EPS forward estimates of $4.23, shares look to be priced fairly at $100, or ~$102, including FWD dividend estimates. Firstly, the market has priced NHC at ~16.5x forward P/E, ahead of the GICS Industry median of 4.13x, suggesting investors expect an above-market result in FY22/23. Shares also trade on a 3-year normalized P/E of 23x.

Below (Exhibit 7) is our valuation model that factors in the earnings pile of NHC's corporate value. It covers a range of valuation inputs that measure a breadth of valuation drivers to estimate fair value. We see shares priced fairly at ~$77.90 including forward dividends, presenting 11.6% or $8.10 in potential upside. If we perform the non-GAAP reconciliations, the value spreads to $131, and this must be factored in also.

Exhibit 7.

Data: HB Insights estimates

Therefore, we'd be paying an implied $53-$56 to receive a value of $77.80, a 39% or $21 per share differential. On adjusted values, it stretches to 133% or $75.

This is incredibly important in the valuation debate. Recall, an investment is typically worthwhile if the present value of expected returns exceeds the cost. It depends on how we look at this too. Firstly, if shares are 'worth' $77.80 pre-adjustments, and $131 post, in the first instance, our implied 'cost' is less than the return [$56 versus $21 return].

In the second, it is more so [$56 for $75 return]. Also, paying 7.1% [fair cost of equity] to receive 39%-133% is quite attractive. However, these are all implied values, and relative to the current market price, are less attractive.

Net-net, NHC possesses the resiliency characteristics that warrant its inclusion in equity portfolios as a defensive overlay. We rate it a buy with a $77.80 valuation.

For further details see:

National HealthCare: An Ultimate In Defensive Overlay For Equity Portfolios