NHC - National HealthCare: Little Room For Further Upside Reiterate Hold

2023-08-29 12:29:23 ET

Summary

- National HealthCare Corporation stock has seen a short-term increase, but questions remain on the scope for further upsides.

- The profitability of NHC's business based on capital deployment is unattractive, in my view.

- Current valuations suggest that growth potential may have already been priced in.

- Net-net, reiterate hold.

Investment updates

Following the last publication on National HealthCare Corporation ( NHC ) the stock has caught a reasonable short-term bid. My questions are on how likely this is to continue, and what economic factors are behind the repricing. Here I'll run through all of the moving parts in the NHC investment debate, paying close attention to the value drivers of the company, and how rational the market's expectations are.

NHC is a mature, well-established entity that provides numerous services across an entire suite of facilities. It continues growing its portfolio of sites, but the profitability of the business based on what level of capital is deployed are unattractive to me. This is despite the company's lengthy dividend history, which you can see in Figure 1(a) below. You've got $955mm in capital at risk producing $24mm in net-operating earnings, just less than 250bps return on investment. If market returns closely resemble business returns over time, this could be a risk to further upside. The company's current valuations also imply a great deal of the growth potential has been already priced in, if not over-extended.

Net-net, I continue to rate NHC a hold, with the view that 1) recent price action doesn't allow for much growth headroom, 2) there are soft economic characteristics on the amount of business capital, and 3) its unsupportive valuations. Reiterate hold.

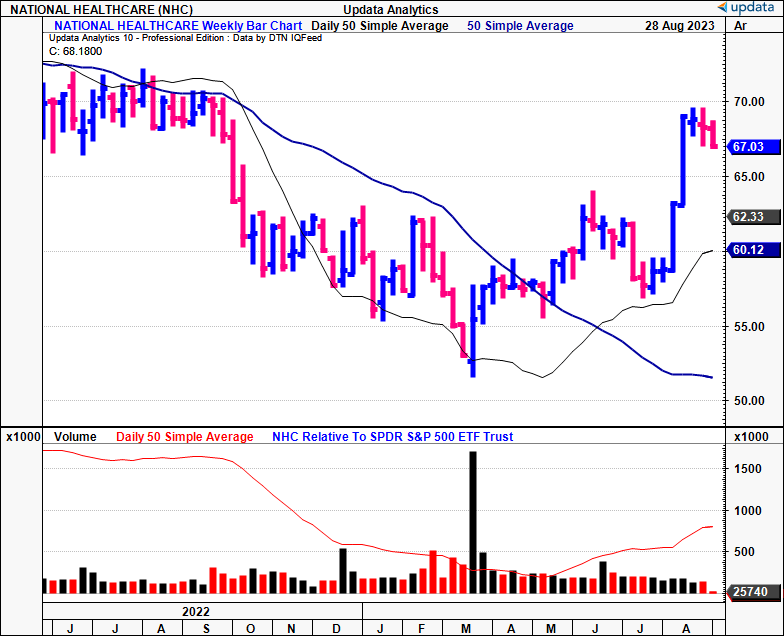

Figure 1.

{kind=link}

Figure 1a.

{kind=link}

Critical investment facts - Q2 earnings, returns on capital, valuation

The crux of NHC's business is that it provides a spectrum of healthcare services through its senior health facilities. It had over 8,700 beds on its books, in addition to a broad suite of 88 diversified facilities ranging from hospice, assisted living and behavioral health. It books revenues via inpatient services in its skill nursing sites, in addition to home care/hospice services. The following critical updates are relevant to the reiterated hold thesis.

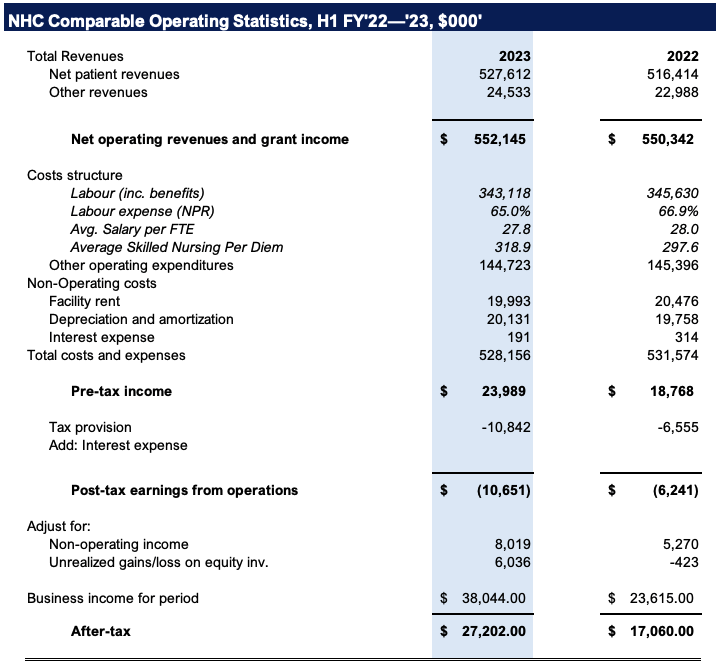

1. Q2 FY'23 insights

NHC booked operating revenue growth of 4.1% in Q2 (note: grant income is included in operating revenues here), clipping $282.6mm for the period. Same-store revenues were up 11.5% YoY, excluding the divestiture of two facilities and stimulus income. For the H1 FY'23, labor expense as a percentage of net patient revenues was down ~190bps YoY, whereas the average SNF per diem (those temporary positions either filled through agency or casuals) was ~$319, up from $297.90 the year prior.

Figure 2.

{kind=link}

It pulled this down to $23.9mm in pre-tax income for the YTD, after a small reduction in OpEx and financing expenditures . Further, adjusting for the unrealized gains/losses on its equity investments, and additional non-operating income, it booked $27.2mm in H1 FY'23 earnings after tax.

My key takeouts from the quarter are as follows:

- One critical aspect of NHC's revenue growth are the occupancy rates within its skilled nursing facilities ("SNFs"; occupancy is also known as the overall patient census) . It had 68 of such facilities on its books at the end of Q2. Critically, both owned and leased SNFs recorded an overall census of 87.9% in Q2, up ~300bps from last year. Similarly, for the YTD, NHC reported an overall census of 87.7%, a growth of 400bps. Quarterly inpatient revenues pulled to $236.7mm for Q2 and $462.9mm for the year so far. Average quarterly revenue per SNF was thus $3.4mm.

- It brought one SNF online in May, along with 4 additional facilities-2 hospice and 2 homecare agencies. These contributed $5.89mm to Q2 revenues.

- At the same time, its divestiture of 7 SNFs off its books in reduced turnover by >$17mm with a cost reduction of just ~$5mm.

- CMS also unveiled its final rule for FY'24 Medicare payment rates and policy adjustments for skilled nursing facilities in Q2. It is slated to become effective from October 1st this year. Critical to NHC-CMS outlined a net rise of 4%-around $1.4Bn- in Medicare Part A payments to SNFs compared to 2023 rates. The rule included:

- An incremental gain of 3% to the market basket rate;

- A 3.6% market basket forecast error adjustment;

- These will be offset by a 20bps productivity adjustment.

- A notable 2.3% decrease (c.$790mm) in the 2024 SNF Payment Prospective Systems rates.

The last point stems from the 2nd phase of the rule covering SNF payments, the Patient-Driven Payment Model ("PDPM") parity adjustment. The PDPM is said to be a patient-centered approach in determining how payers such as Medicare reimburse SNFs. It was introduced back in 2019, in place of the former Resource Utilization Group, or RUG-IV for short. Tennessee also implemented its own 2024 SNF rate increases, and management foresees a $15mm annualized tailwind from this starting next year.

Aside from that, the company increased its dividend by 2 cents per share and will return $0.59/share to equity holders, marking the YTD capital return to $1.16/share. Collectively, these results are rather flat in my view and despite the regulatory tailwinds on the CMS side, the growth fueling NHC's operating engine isn't generating much horsepower.

2. Capital employed, returns produced

The financial results do little to present the kind of value NHC is creating or destroying for shareholders. A more thoughtful analysis of the economic characteristics is needed.

Figure 3 outlines the company's post-tax earnings as a percentage of the capital NHC has deployed into its operations (net operating profit after tax are equal the post-tax earnings here). Rolling TTM periods are used for each income measure, balance sheet items are recorded at book value each period. All relevant items are included in the calculus, and cash is taken in full given optionality and its propensity to be deployed. Non-operating income and unrealized gains/losses on equity investments are not recorded as earnings.

By Q2, $955mm in capital at risk produces just $24mm in post-tax earnings from operations. This equates to $1.57/share in NOPAT produced on $62.40/share of capital at risk, or 2.5% trailing return on the capital deployed. But it has lifted FCF/share from $5.67 in 2021 to $15.80/share in Q2 FY'23. Nevertheless, FCF has been unstable for the company over this time.

As a yardstick, measuring the profits generated per $1 of capital employed into a company's operations is a better gauge of performance and value-add than profits as an absolute number. Outpacing the opportunity cost of capital is a fundamental point in value creation for shareholders, and to return on investment. The equity benchmarks are the hurdle to beat. A 10-12% compounding price return isn't unexpected for the S&P 500 index on any given year, and is considered to be the average. This is the required rate of return each prospective company must produce on its own capital allocations in order to create additional market value.

If a firm takes the profit it generates, invests this into future growth, it would have to generate a return above our 12% hurdle rate to have created additional shareholder value. Intelligent investors should expect this of their companies in my view. And it's not an unreasonable expectation-they expect this given the type of investments available to businesses (which are typically more expansive and lucrative). I'd also accept these returns in the absence of financial growth-what's more important to me is the profits as a percentage of the capital invested by the business.

NHC's tremendously low returns are indicative of a mature company that has little to no avenues to deploy surplus capital and enjoy exciting growth. Both its post-tax margins and capital turnover are tight, suggesting it doesn't enjoy consumer or production advantages, which is a risk in my eyes given it is in the business of healthcare services-so you'd expect some consumer or pricing advantages if it were capturing a large share of the market. These economic factors support a neutral view in my opinion.

Figure 3.

{kind=link}

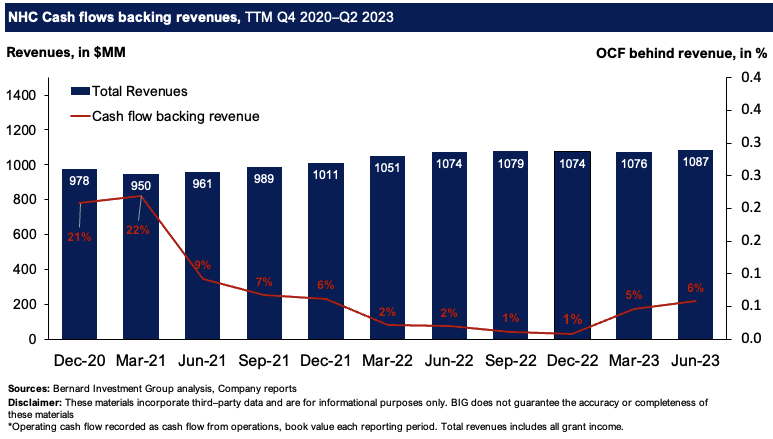

Operating cash flows are equally as important to supply the cash that can be deployed into future investments. Revenues are less meaningful if the degree of cash flows backing these are light.

Figure 4 shows the OCF behind NHC's revenue clip on a rolling TTM basis. All revenues are included, along with all sources of operating cash flow each period. Critically, cash flows backing turnover have slipped from 22% in 2021 to just 6% last period. Hence, the additional revenue growth has not converted into additional cash flows. To me this also supports a neutral stance. I'm looking for cash compounders, especially in companies this mature and this size. The cash has to come from somewhere-it can't just be the "free cash flow to the firm" each period-that is residual. Cash flows have to flow in from operations in order to sustain a level of attractive business and without these economics, NHC's are unattractive in my view.

Figure 4.

{kind=link}

Valuation and conclusion

The stock sells at 33x trailing earnings and 13x EBITDA. The cash flows mentioned earlier see it trade at a 6% trailing cash flow yield.

Further, taking the enterprise value vs invested capital as a cleaner measure of p/book value, the firm is fairly priced, and hasn't created additional market value above the capital deployed into the business. In fact, the market value added (market cap less invested capital) is just $50mm as I write, hardly an indication the market values NHC's assets highly.

Trading at 1x invested capital also links to a ROIC/hurdle rate ratio of just 0.2x for the company. You'd expect an ROIC/hurdle rate of >1 and for it to be higher than the EV/IC number to suggest there's growth yet to be priced into the company's market values. Looking at what the model has spat out, this indicates that ~4.8x of the company's expected growth has already been priced into NHC's market value, leaving little to no room for outsized return given the underlying economics in my opinion. For reference, if the company was producing 15% return on its capital (>the 12% hurdle) the ROIC/hurdle rate would be 1.25x, indicating that only 0.8x or 80% of the growth had been priced into its corporate value (1.25/1.01 = 0.8). At 25% ROIC, it would be just 50% (2.08/1.01 = 0.5). The current $964mm or $68 per share market price is not attractive in my eyes. Hence, NHC looks overvalued on this valuation calculus.

Figure 5.

Note: Comparing market values to invested capital is a fundamental tenant to observing value creation for shareholders. For more, see "Valuation: Measuring and Managing the Value of Companies" (McKinsey 2020). (BigInsights, company filings, Bloomberg Finance)

A core tenet to seeing companies generate shareholder value over the long term is to benchmark the earnings produced on the capital put to work into business operations. This immediately tells us if the company generates satisfactory returns (both cash and profits) on the capital it has employed. NHC's economic characteristics don't align with the expectations I'd have in adding it to the long account. Granted, it continues with financial growth each period, but it is a capital-intensive business that doesn't spin off piles of cash to its shareholders (even with dividends). Its ability to finance future growth typically stems from asset disposals to obtain the cash, and we saw evidence of this in Q2 FY'23. Further, multiple selective opportunities do present with these desired characteristics right now. Net-net, I continue to rate NHC a hold.

For further details see:

National HealthCare: Little Room For Further Upside, Reiterate Hold