NHC - National HealthCare: Revising To Hold On Multitude Of Factors

2023-06-13 16:31:02 ET

Summary

- National HealthCare Corporation's fundamentals are deteriorating, with a smaller business size and decreasing earnings.

- The company's valuation is unsupportive at 51x earnings, making it an unattractive investment option in my view.

- There are more selective opportunities elsewhere, and allocating any weight to NHC would be an opportunity cost.

Investment Summary

In my December National HealthCare Corporation ( NHC ) publication, I noted the company's potential as "a tactical inclusion as a defensive overlay to reduce equity risk…and its ability to smooth equity returns". More clarity on rates, a slowdown in the pace of inflation, and potential near-term liquidity catalysts mean the funding window for selective investment is wide open. As such, I am revisiting the NHC investment thesis, reverting it to hold in doing so. The reasons for this are simple yet require a degree of explanation. This report will attempt to convey the critical facts in the NHC investment debate and what justifies a neutral viewpoint. Net-net, revise down to hold.

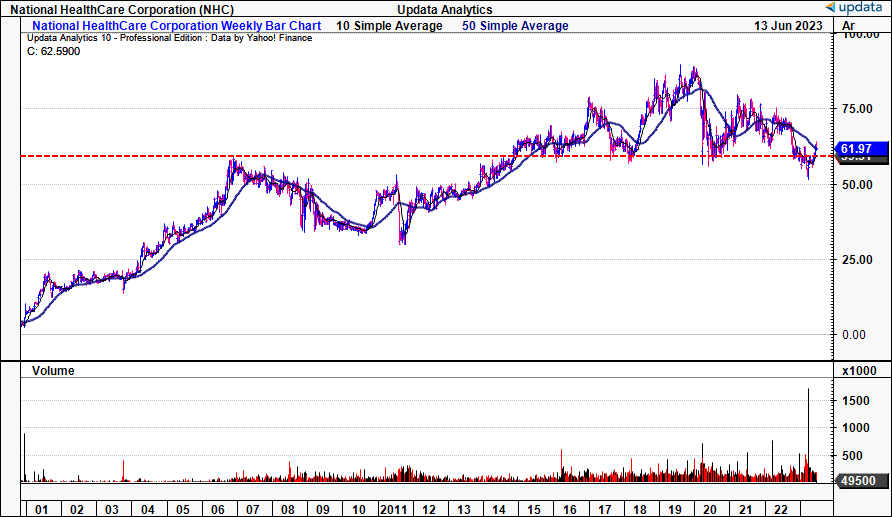

Figure 1. NCH equity stock performance, 2001-date (22 years)

- Note, the company trades in line with 2007 range

{kind=link}

Q1 Earnings Continue Earnings Trends

A look-back over the last few years of business shows NHC's performance to be less than appealing. This is attributed to the defensive nature of its stock in my view (coincidentally, also the factor I urged investors to position against last year, during the broad market selloff). However, a more thoughtful analysis of the future is now required, given that the markets have adapted, as they always do.

Operational breakdown

Looking at the quarterly numbers , the company booked an 11.2% increase in net operating revenues ("NOO") to $269mm and pulled this to $101.7mm gross. On inspection, the quarter's growth can be traced back to two underlying factors:

- Census Increase in Skilled Nursing Facilities : NOO was driven by a higher census within the company's skilled nursing facilities. A higher census suggests increased patient care in these facilities, leading to higher revenues, a sign of revenue growth downstream, in my opinion.

- Acquisition of Caris Healthcare : In June FY'21, the company acquired Caris Healthcare, a hospice provider, and this has begun to pull through to the top line. It pulled this down to core EBITDA of $20mm and earnings of $15.3mm or $0.76 per share ($3.04 annualized). This is a decrease compared to the net income of $21.3mm reported last year.

The critical fact I'd point out is that NHC has been scaling back its business size for several years. You can see this clearly in the progression of annual operating income, FY'18-23 TTM (the year 2023 is shown as the tailing 12 months up until Q1 2023):

Note: The year 2023 is shown as the trailing 12 months up until Q1 2023. (Data: Author, NHC SEC Filings)

A firm doing $49mm less in operations over a 10-year horizon is the antagonist to value creation in my view. Earnings are down $37mm since 2013, with minimal growth in between as well, perhaps one primary reason the equity value has been so flat.

Alas, despite the growth trends observed within the quarter, this didn't pull vertically down to the P&L. Earnings were clamped by the following:

- Less government stimulus income was compared to the previous year; $0 this quarter, versus $10.6mm the year prior.

- Inflationary pressures on labor costs also contributed to the decreased adjusted net income, which is not unique to the company. Still, you'd expect these pressures to normalize going forward. If not, there could be a deeper issue.

This operational divergence is seen in Figure 2. Note, the gapping in operating income to revenues since 2013. As revenues have been climbing persistently to c$125mm, the level of recorded operating income on this has clipped to record lows <$20mm, from ~$600mm in 2013. This suggests significant operational inefficiencies and a lack of value for shareholders - no matter what the top line does, there are no earnings left over at the 'end of the year' for the company's owners.

Figure 2.

Data: Author, NHC SEC Filings

Investment implications

NHC's presence in the senior healthcare market is also critical to its business economics. In terms of operating capital, it operates multiple facilities and care units. These in turn produce income for the company, via the service[s] provided on-site. The increasing need for healthcare services driven by the aging population could be a positive outlook for NHC's business in my view. As the general population ages, the demand for senior health care services, including skilled nursing, assisted living, hospice care, and so forth, is expected to rise.

Specialized care units, such as for Alzheimer's disease, high-level care units, and sub-acute nursing units are a non-negotiable within the entrails of society. Again, this argument has a defensive flavor for an investor, because NHC's turnover is relatively impervious to major swings within the business cycle. Hence, you've got a potential name to turn to during an economic downturn.

Looking at the quarter, it's also worth noting that the total census at owned and leased skilled nursing facilities averaged 87.4%, ranging back to pre-pandemic times; plus, the addition of Caris Healthcare's hospice assets increased net operating revenues and grant income as mentioned earlier. I'll be paying close attention to these moving forward. I'll be scrutinizing this, and the company's operations, by comparing:

- the firm's incremental investments made over time, with

- the market's reward/punishment following said investments.

Presuming the market is an accurate judge of fair value over time, this is a fruitful exercise. Recall, a firm creates value for its shareholders when it reinvests the profits it generates into future growth opportunities at a generous profit. The key value test is if the firm generates returns on these investments above what investors could have got elsewhere.

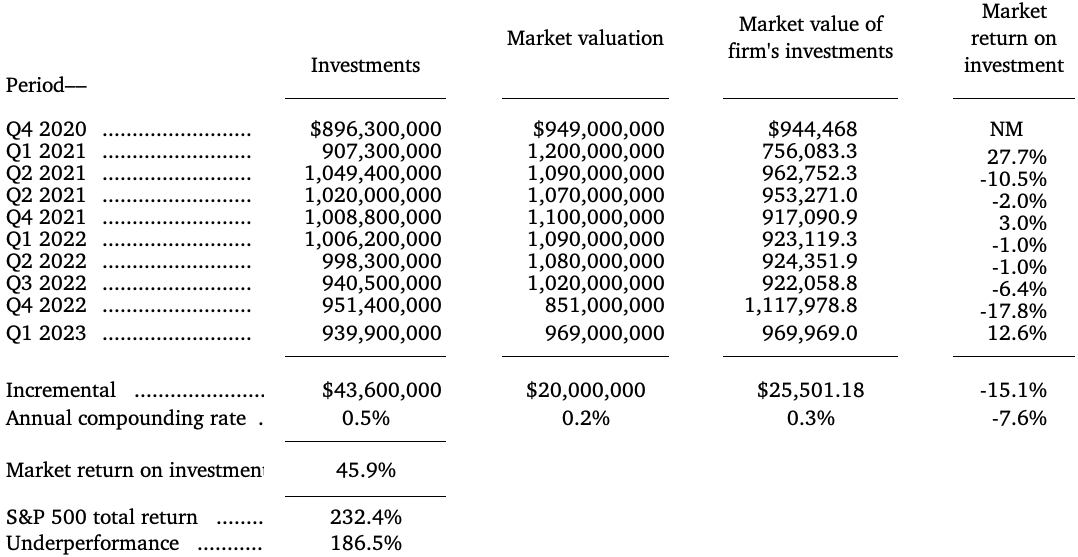

NHC still needs to deliver on this critical assignment. You'll note below the firm has increased its capital base by an average of 50bps per period since 2020 (rolling TTM periods) for a $43.6mm total investment (Table 1). However, investors have only increased the company's market valuation by $20mm (to the time of writing), just a 20bps compounding rate. The profits generated from NHC's investments are below standard, and the market responded accordingly. There is every indication this kind of trend may continue going forward, based on my analysis.

Table 1.

Note: market value of firm's investments is calculated as book value of invested capital divided periodic market capitalization, on a rolling TTM basis. (Data: Author, NHC SEC Filings)

{kind=link}

For a firm to attract sophisticated capital, it should be rotating the capital it puts at risk through growth investments into additional market valuation over time - an indication the investments were a success (in the market's eyes). You'll note that the market typically even pays a premium to the carrying or book value of the assets and operational value, as there is value in a firm's operations as a going concern over its liquid value.

With NHC's numbers, the issues are abundantly clear in this regard. The market return on investment, i.e., the market's reward on NCH's incremental capital, has compounded at a negative rate of 7.6% over the testing period. As such, it suggests the profits generated have been sub-par, and that has in fact been the case. The company averages ~2-4% return on existing capital each period (measured by the TTM post-tax earnings generated) - well below the market's hurdle rate of 10-12% (long-term averages). Results are wider over the testing period, with just a 46% gain in incremental market value vs. the S&P 500 index's 232% incremental return, a 186% underperformance.

How then, does one advocate to buy the company now when going forward - outside of a defensive argument? That, my dear readers, is a difficult task to endure. In my view, the case for stonewalling one's portfolio with "flatliners " such as NHC has receded, to be replaced with more tactical positioning going forward. The major reason underlining this - capital is more valuable in the investor's hand than in NHC's, evidenced by the return it is producing on its own investments, versus what the market can provide a passive investor.

Valuation

Naturally, valuation factors are critical in providing some balance to, or at least saving the buy thesis. But investors are trying to sell their NHC positions at ~51x the TTM earnings as I write - quite the ask if I were to opine. You're buying $2.36 in dividends estimated for FY'23 as well (3.8% yield as I write), not enough to offset that premium. Further, the business looks to pull in $1.22 of earnings this year, below the $2.74 in 2020 and $4.47 in 2019. Consistent with the findings in this report, the valuation outlook is equally as compressed.

As a reminder, we're being asked to pay $51 for every $1 in NHC's future earnings, earnings that by all means look to continue eroding on the smaller size of the company. The company's annual dividends are noted but aren't really growing, and may become unsustainable if the current earnings trends prevail. Given the plethora of headwinds discussed in this report, I simply cannot get into paying that kind of price for NHC.

The sector trades at 19x forward earnings and this is a reasonable number in my view. Assigning this multiple to the firm's trailing earnings of $1.22 derives a price target of just $24, highlighting the valuation disconnect. It is clear investors (long-term buyers, no doubt, who are willing to pay above 'value' given their long-term view) in NHC's stock value its long-term prospects and will pay a premium - yet, I believe given the fundamental backdrop, 51x earnings is far too steep of an ask in my playbook. This also supports a neutral viewpoint from my end.

In Short

In summation, there are numerous factors to suggest NHC remains a 'defensive' holding that could potentially smooth equity returns in one's long account. However, there is more to consider than this on the strategic side. Number one is the fundamentals are deteriorating, even with a smaller business size. The opportunity to enter isn't now. Number two, valuations are completely unsupportive at this current level of business. At 51x earnings, you may as well lock the money up for the next half-century. Finally, there are more selective opportunities elsewhere. To allocate any weighting to NHC (or additional weight) would be a severe opportunity cost to the spate of companies generating fundamental and valuation growth. Net-net, revising back to hold.

For further details see:

National HealthCare: Revising To Hold On Multitude Of Factors