NHC - National HealthCare: Tactical Resiliency Remains Needs To Drive Higher ROIC

Summary

- NHC remains an attractive name to smooth equity returns in a cross-asset portfolio of high quality securities.

- Even still, the company has some work to do in order to drive value creation down the line.

- In particular, measures of ROIC and ROE are thin, and we'd like to see some upside on these going forward.

- Net-net, we continue to rate NHC a buy at a suggested price range of $69–$75.

Investment Summary

Earlier in the year, we had called for investors to consider adding a basket of resilient, low-vol stocks as a defensive overlay to equity portfolios, in order to reduce equity beta and clamp drawdown. One such name we would draw investors' attention to is National HealthCare Corporation ( NHC ). As a reminder, in August, we rated NHC a buy for the reasons above, noting its propensity to keep drawdown, standard deviation of returns, and equity beta at a minimum when included into a cross-asset portfolio of equal weightings.

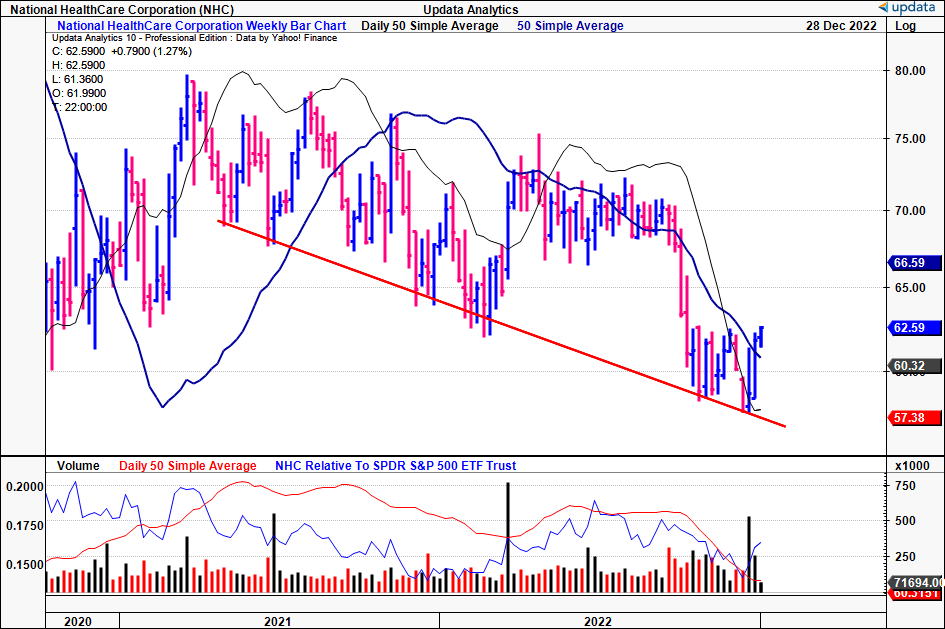

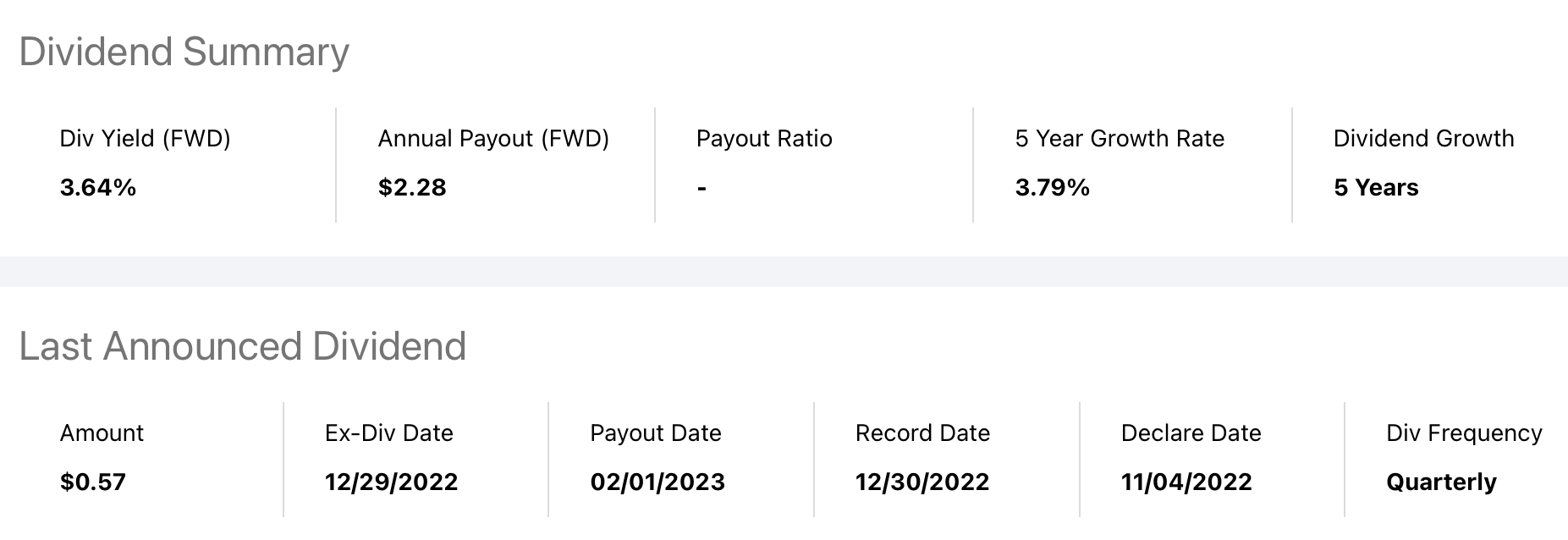

Since that publication, the NHC share price has since incurred a marginal selloff from previous highs of $69. It now trades 10% below this mark at the time of writing. Aside from that, the company has maintained its stream of dividend payments to shareholders [Exhibit 2], adding some downside cover looking ahead.

Nevertheless, I'm here today to reinstate our buy rating on NHC, citing its strengths as a tactical inclusion as a defensive overlay to reduce equity risk. I should stress, that this is a tactical recommendation, and not a strategic one. In other words, we're looking at NHC's inclusion into a broader set of holdings, and its ability to smooth equity returns. We covered this heavily in our previous publication. You can read that, and the respective portfolio weighting studies we performed, by clicking here:

- NHC: An ultimate in defensive overlay for equity portfolios [see: " Exhibit 4: Portfolio backtesting "].

Despite this, we are now turning more tentative on the position, and note the company has a bit of work to do in order to command a re-rating of multiples to the upside. It is therefore essential to remain active on this name, and not accept any further losses in share price. On that, we will exit the position if the stock is to fall below $56. Net-net, we retain a suggested price range of $69–$75, and continue to rate NHC a buy.

Exhibit 1. NHC's weekly price action in 2022

{kind=link}

Exhibit 2. NHC quarterly dividend, with forward payout and yield.

Data: Seeking Alpha, NHC, see: "Dividends".

{kind=link}

NHC Q3 earnings flat, with lack of earnings leverage

Talking of NHC's latest set of earnings , we'd note it was a flat period for the company. Whilst we don't expect to see large growth percentages in this relatively defensive name, we also don't expect to see a slowdown in key operating metrics.

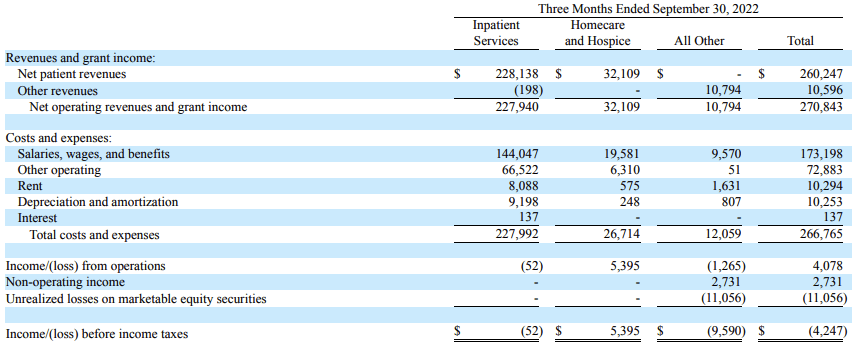

For example, we noted that quarterly net patient revenues increased 210bps YoY to $260.2mm. This corresponds to roughly $2.90mm in net patient revenue per day during the quarter. Overall revenue of $270.84mm was down 210bps YoY, however. In addition, the average census at owned and leased skilled nursing facilities was 83.7% for the quarter, up from 82.0% same time last year. From these figures, and the company's 8,726 bed capacity, we calculated the quarterly occupancy rate to be ~96%.

Further, the composite skilled nursing facility per diem increased by ~240bps compared to the same quarter in the previous year. Whereas private pay per diem rates lifted by c.330bps. It's also worth noting that Medicare per diem rates increased by a similar amount of 220bps, while managed care per diem rates increased by 610bps YoY.

Exhibit 3. NHC service cost-revenue breakdown, Q3 FY22.

Data: NHC Q3 FY22 10-Q, pp.30-31, see: "Segment Reporting"

{kind=link}

Speaking more of Medicare, there are a few talking points here. For instance:

- The company booked $4.77mm in our net patient revenues for supplemental COVID-19 Medicaid payments, down from $5.05mm last year.

- Following the end of the CARES Act, that temporarily suspended Medicare sequestration from May FY20–March FY22', the full 2% reduction was reinstated from July. As a reminder, the Medicare sequestration policy is put in place to decrease fee-for-service Medicare payments by 2% on an annual basis. After the 2% reduction was fully reinstated, NHC report that it experienced a corresponding decrease in net patient revenues by approximately $1.5mm during Q3 2022 compared to the same time last year.

- CMS also released its final rule for reimbursement rates outlining FY23, pertaining to skilled nursing facilities. The new rates began on October 1st, providing a ~2.7% increase for FY23. This equates to ~$904mm compared to the FY22 rulings.

It's also worth pointing out that in September, NHC transferred the operations of 7 skilled nursing facilities located across Massachusetts and New Hampshire [both located in the U.S]. This resulted in a further YoY decrease of $5.1mm in net patient revenues for the quarter.

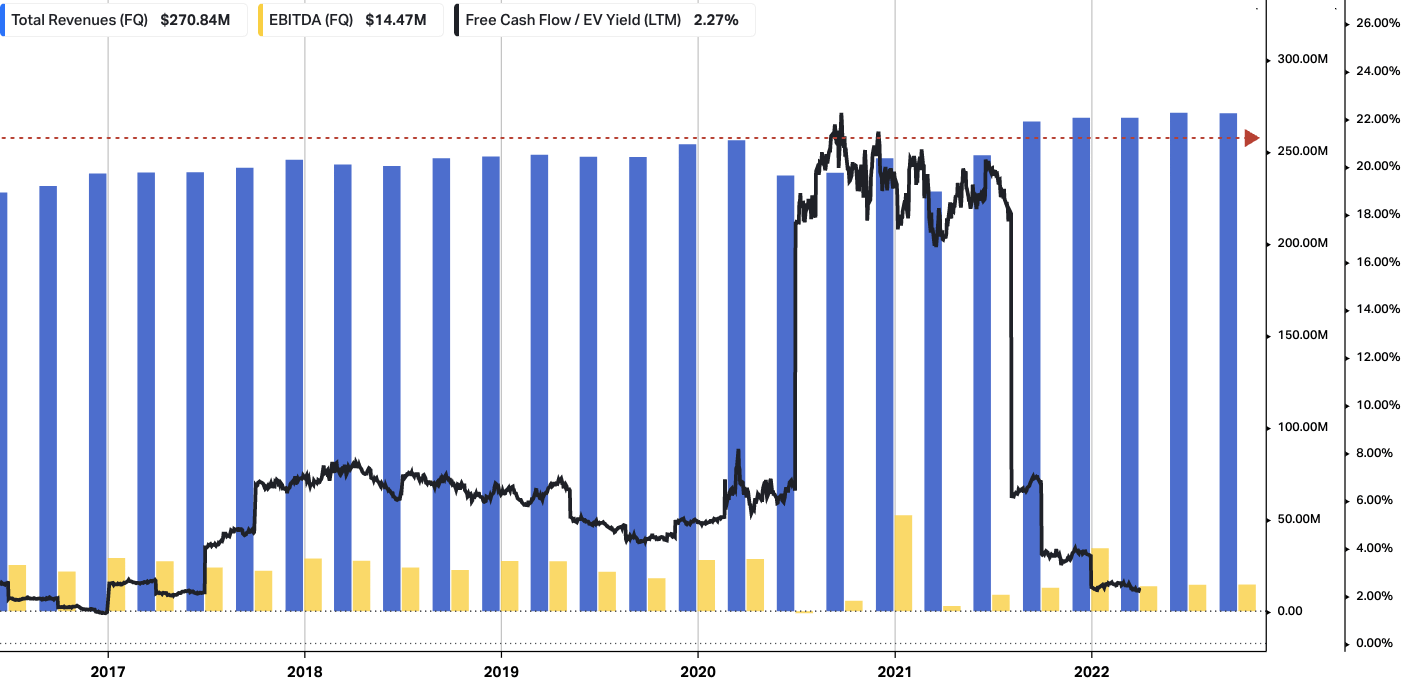

Given these headwinds, you can clearly see the flat sequential growth pattern NHC has exhibited at the top line from FY21, with core EBITDA corresponding with the same. Whereas in our previous analysis, we commented on the strengths in NHC's net patient revenue growth, this wasn't as abundant this period. This could be a downside risk looking ahead.

Exhibit 4. NHC sequential revenue, core EBITDA growth since FY17. Note the flat sequential incline over since FY21

Data: HBI, Refinitiv Eikon, Koyfin

{kind=link}

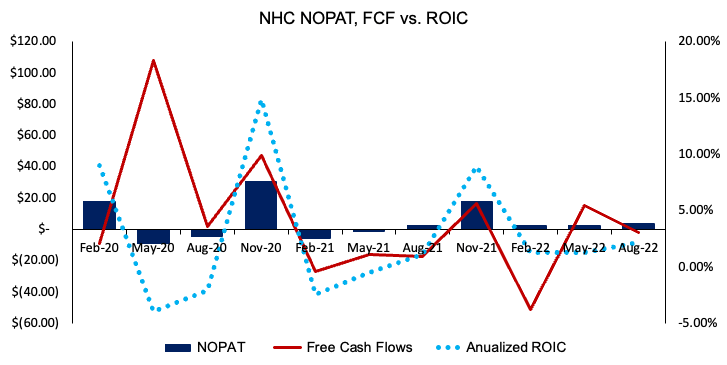

It's therefore unsurprising to see the level of return on invested capital ("ROIC") return to near-zero for the company over the same time [annualized]. You'll see below that, as NHC has realized a series of free cash outflows, the corresponding ROIC has been negligent.

This reminds us that NHC's operating model is of a high capital intensity, and therefore requires a substantial amount of CapEx and invested capital to maintain operations.

In our opinion, the problem with this, and the sub-par ROIC, is that it could potentially dampen NHC's ability to fund its own growth initiatives looking ahead, or will limit the ability for the company to allocate capital efficiently.

We'd like to see NHC take on additional capital budgeting measures in order to see an improvement in this area, possibly by addressing underperforming assets or operating segments.

Exhibit 5. The corresponding decrease in FCF and ROIC is a measure that would ideally improve in an environment where the cost of capital is increasing

Note: ROIC is calculated without the inclusion of Goodwill. (Data: HBI, NHC SEC Filings)

{kind=link}

Valuation

In our previous publication, we valued NHC at a suggested range of $69–$75 [see: Exhibit 7]. This corresponded to a forward P/E of 14.14x at the time. We are comfortable in retaining this valuation range.

You'll see on the chart below that we also have price objectives to $65.50, and this is a downside risk that must be factored into the investment debate.

It's also worth pointing out that NHC trades at just 1.1x book value , which is attractive considering its tight trailing ROE of 3.6%.

Exhibit 6. NHC price objectives to $65.50, after pullback in price distribution

Data: Updata

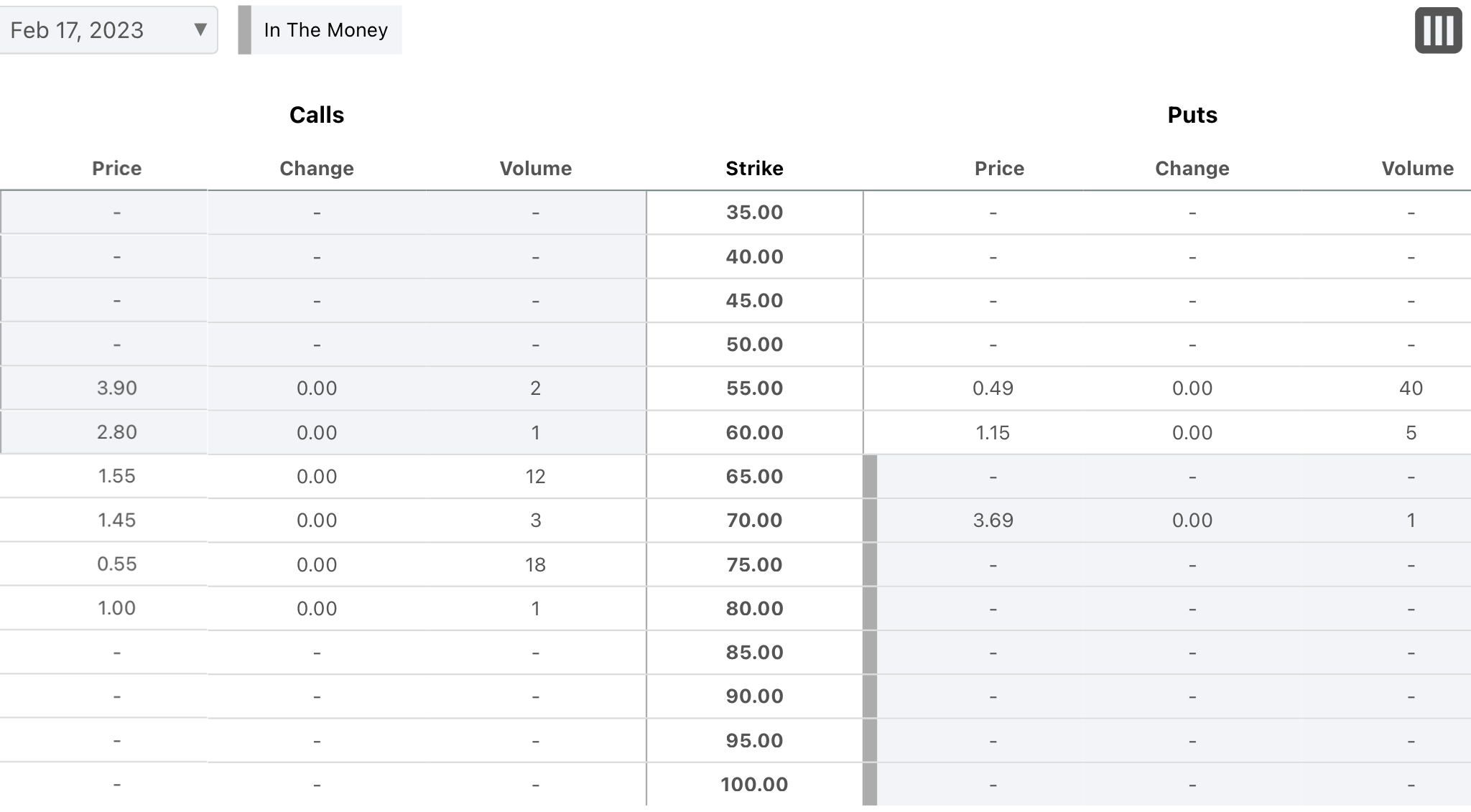

Given that NHC trades on a quite tight historical volatility, we felt it was prudent to examine the market's positioning in the stock for the next few months.

You'll see in the NHC options chain for contracts expiring February 2023 [Exhibit 7] that investors have positioned heavily in Feb 2023 calls around the strike depth of $65–$75, very much the same as our recommended price range. This confluence gives more confidence in using these targets.

Exhibit 7. NHC options chain, contracts expiring February 2023 [note: all contracts displayed are currently in the money only]

Data: Seeking Alpha, NHC, see: "Options"

{kind=link}

In short

Whilst we still see tactical value in holding NHC as a defensive overlay to equity portfolios, we'd also note there are downside risks in the investment debate, that are discussed in this report. Chief amongst these are the company's ROIC and flat sequential revenue growth. Should these trends continue, the price response in the NHC share price could be seen to the downside.

Nevertheless, we believe there is scope for the stock to re-rate to our suggested price range of $69–$75, and this is well supported by market positioning in the stock. Furthermore, despite the tight ROIC, and capital intensive operating model, there are a multitude of strategies NHC management can employ to drive additional value looking forward, not in the least rebalancing its core portfolio of assets. Net-net, we continue to rate NHC a buy, and would encourage investors to remain active on this name.

For further details see:

National HealthCare: Tactical Resiliency Remains, Needs To Drive Higher ROIC