NPK - National Presto Industries: Fairly Valued Based On Current Conditions

2023-03-09 09:24:17 ET

Summary

- National Presto Industries had something of a mixed year in 2022, with sales ultimately falling, but the second half of the year showing some bright spots.

- The firm's balance sheet is robust, and the long-term outlook for the business will likely be positive.

- But given how shares are priced, there are better prospects that can be had on the market today.

One of the very first companies that I ever bought shares in was National Presto Industries ( NPK ). As a small firm with a robust balance sheet and that has a history of being a diverse enterprise from an operational perspective, the business definitely piqued my interest. After some time, however, I did end up selling my stock in the firm. But I've never lost interest in it and I occasionally like to revisit it to see whether or not it may make sense to buy it again. Recently, shares of the company have experienced a nice bit of upside relative to the broader market. This can be a good sign that additional strong performance is right around the corner. Shares of the business are also not unreasonably priced. But with its fundamental condition showing mixed signs, I can't pull the trigger just yet. In fact, instead of being bullish about the business, I do believe that there are plenty of reasons to be neutral on it. Because of this, I've decided to keep it rated a 'hold' to reflect my view that the stock should generate upside or downside that more or less matches the broader market moving forward.

Reasons to be neutral abound

The last article that I wrote about National Presto Industries was published in early November of 2022. Leading up to that point for the prior few months, shares had done quite well. But sales reported by the company, as well as profits, were showing weakness. At the end of the day, I felt as though the long-term picture for the business was still solid. But given how the stock was priced and because of the deteriorating fundamental performance of the firm, I believed that a 'hold' rating was appropriate as opposed to something more bullish. Since then, however, the company has continued to experience upside. Shares are up at 11.9% while the S&P 500 is up only 5.6%.

{kind=link}

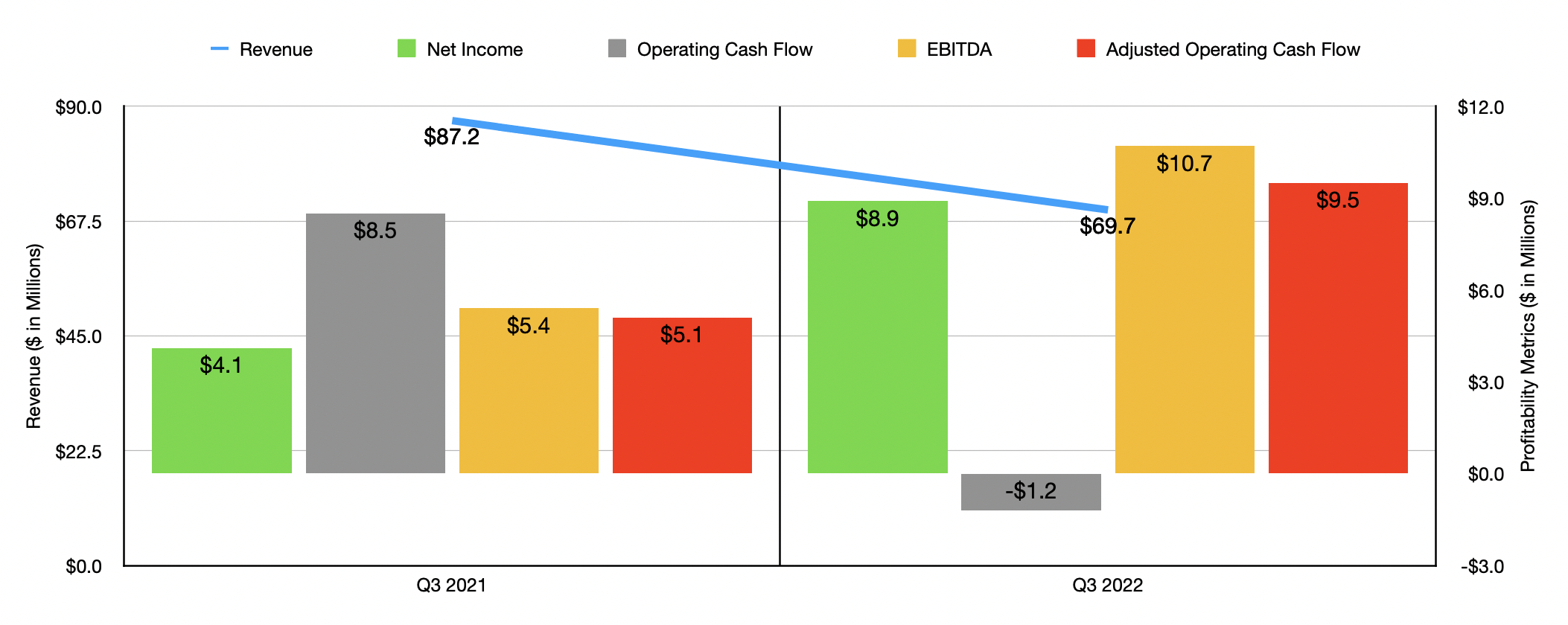

Frankly, I am a bit perplexed as to why the stock has moved up so much more than the broader market has. To see what I mean, we need only look at data covering the most recent quarter . This is the third quarter of the company's 2022 fiscal year. During that time, revenue totaled $69.7 million. That's 20.1% lower than the $87.2 million reported one year earlier. This plunge in revenue was driven almost entirely by a decline in sales associated with the company's Defense segment. A reduction in shipments caused revenue to drop 28.6% from $59.3 million down to $42.3 million. By comparison, the Housewares/Small Appliances segment reported a modest 2.2% drop in revenue from $27.7 million to $27.1 million, while the Safety segment reported a surge in sales from $0.155 million to $0.216 million. Even though the business did experience some pain from a sales perspective when it comes to the Defense segment, it's worth noting that backlog of $497.9 million comes in quite a bit higher than the $460.8 million reported at the end of the 2021 fiscal year. In addition to this, in late October of last year, the Defense segment purchased the equity interests of a high-volume manufacturer of precision metal parts and assemblies that are primarily for the defense and aerospace industry. That entity has annual revenue of around $18 million. Some of the optimism centered around share prices may relate to that growing backlog and the acquisition in question.

On the bottom line, the picture has looked a bit different. Despite the decline in sales, profits for the business rose from $4.1 million to $8.9 million. A jump in the company's gross profit margin from 12.9% to 24.5% was largely responsible for this. The biggest improvement on this front came from the Housewares/Small Appliances segment, with profits shooting up in response to price increases and a change in product mix. Lower ocean cargo and inland freight costs also aided in pushing this margin higher. Other profitability metrics mostly followed suit. Operating cash flow did decline from $8.5 million to negative $1.2 million. But if we adjust for changes in working capital, we would have seen an increase from $5.1 million to $9.5 million. Meanwhile, EBITDA for the company jumped from $5.4 million to $10.7 million.

{kind=link}

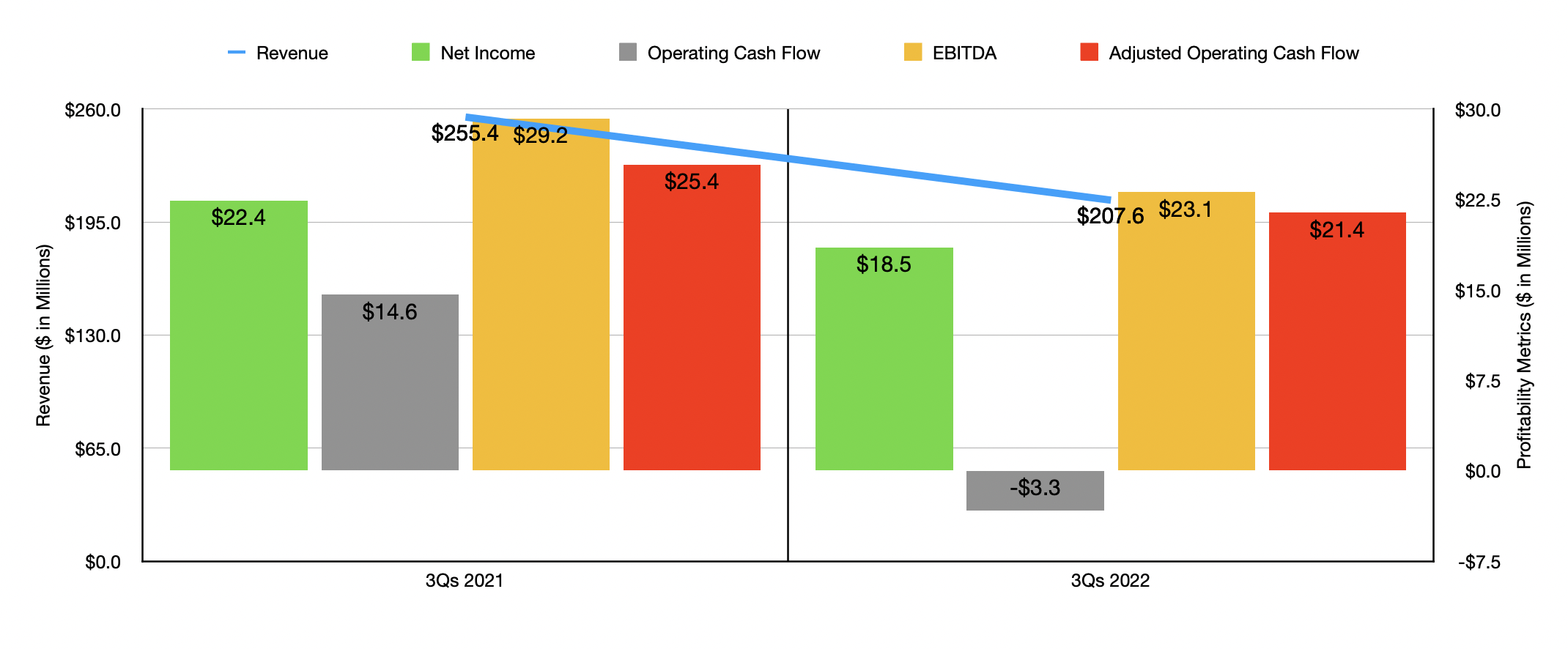

The sales picture for the third quarter of the year was very similar to what the company saw for the first nine months as a whole. Revenue of $207.6 million came in below the $255.4 million reported for the first nine months of the 2021 fiscal year. However, the improvement in profits is something new. For the first nine months of 2022, the company generated a net profit of $18.5 million. That's down from the $22.4 million reported one year earlier. Operating cash flow went from $14.6 million to negative $3.3 million. The adjusted figure for this also worsened, dropping from $25.4 million to $21.4 million. And finally, EBITDA declined from $29.2 million to $23.1 million.

{kind=link}

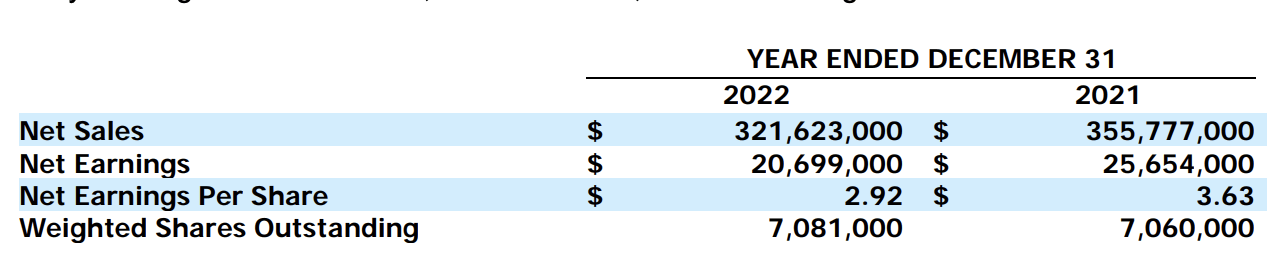

It is worth mentioning that management did reveal preliminary results covering 2022 as a whole. Sales of $321.6 million were lower than the $355.8 million reported for 2021. Net income over this time also dropped from $25.7 million to $20.7 million. No guidance or estimates were provided for the other profitability metrics. But a rough approximation from my end suggests that adjusted operating cash flow should have come in at around $31.1 million, while EBITDA should have totaled $26.1 million. Based on this lower profitability for 2022 as a whole, management has also reduced the size of their dividend. For the 2023 fiscal year, the company declared a regular dividend of $1.00 per share, plus a special dividend of $3 per share. The record date of this was March 1st, with a payment date of March 15th. But this represents a significant reduction compared to the $4.50 seen in 2022 and the $6.25 reported for the 2021 fiscal year.

{kind=link}

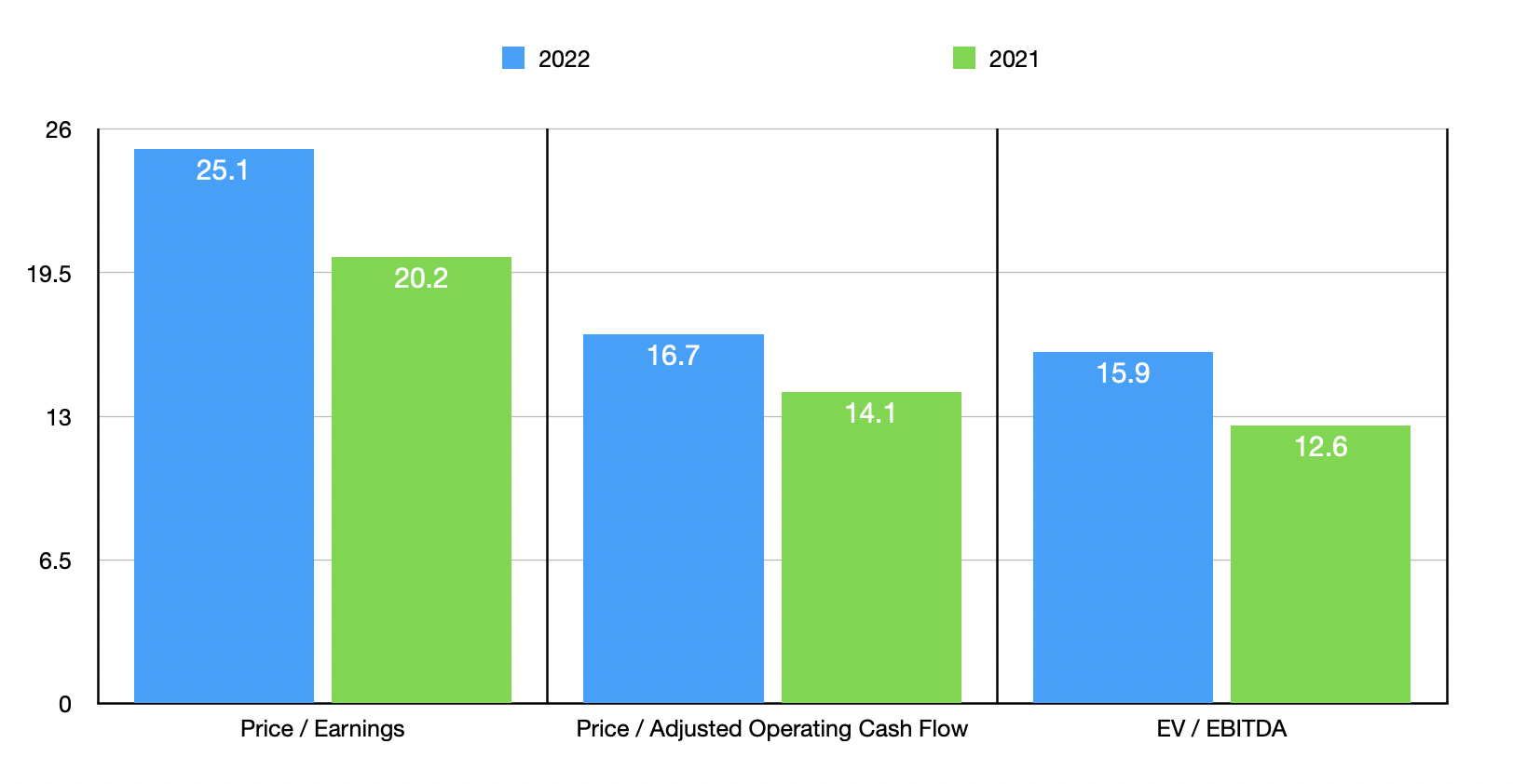

Based on the data provided, I estimated that the company is trading at a price-to-earnings multiple of 25.1. This is up from the 20.2 reading that we get using data from 2021. The price to adjusted operating cash flow multiple also seems to have increased year over year, climbing from 14.1 to 16.7. The same can also be said of the EV to EBITDA multiple, which I have pegged at rising from 12.6 to 15.9. Normally, I would like to compare the business to similar firms. But because of its diverse operations, fairly small market size, and the fact that even its largest segment is so unique relative to what else is out there, I think it could be more misleading to value the company next to other enterprises rather than on its own.

Takeaway

Operationally, I have no problem with National Presto Industries. In the long run, I suspect the company will do just fine. It's a unique business with many peculiarities that investors should enjoy. The firm has no debt and, as of the end of the third quarter, had cash and cash equivalents of $105.5 million. That's significant compared to the market capitalization of the business. Having said that, shares are not exactly the cheapest on the market and profits for 2022 were down compared to 2021. Yes, we did see some improvement near the end of the year. But it's unclear how long that can last. Add on top of that the continued decline in distribution from 2021 through 2023, and I think that this makes sense as a 'hold' rather than as a 'buy'.

For further details see:

National Presto Industries: Fairly Valued Based On Current Conditions