ATROB - National Presto Industries: Recent Growth Does Not Warrant Further Upside

2024-01-18 06:57:20 ET

Summary

- National Presto Industries has shown mixed financial performance, and shares have not been as cheap as desired.

- The company has transitioned to focus on the Defense segment, which has seen growth and improved profits.

- The Housewares/Small Appliances segment has experienced a decline in revenue and is a drag on the overall business.

- Though shares are cheap relative to similar firms, NPK stock is still not cheap enough to justify an upside, especially given its historical lack of growth.

One company that has always had a special place in my heart is National Presto Industries ( NPK ). Back when I was in college, sometime around late 2009 if memory serves me right, it was one of the first five companies that I ever bought stock in. After making a modest profit, I ended up selling. But ever since then, I have thought of the company in a favorable light. Unfortunately, I have rarely thought of the business as an attractive investment opportunity. Because of how shares are priced and some issues that the business has had from time to time, I have often taken a more neutral stance on it.

This kind of stance was what I maintained when I revisited the company in the last article that I published about it in late August of 2023. At that time, the company was showing signs of improvement in some respects, especially when it came to the Defense segment. But overall financial performance remained mixed and shares were not as cheap as I would like them to have been. This ultimately led me to keep the company rated a 'hold' to reflect my view that the stock would be unlikely to outperform the broader market for the foreseeable future. So far, that call has proven to be fairly accurate.

While the S&P 500 is up 9.1% since then, shares of National Presto Industries have generated upside for investors in the amount of 6.4%. Fast forward to today, and the firm is showing continued mixed results. But for the most part, the picture shows a firm that is continuing to grow. Despite this and despite how shares are priced relative to similar firms, I would argue that the business still makes for a better 'hold' candidate than it does anything else. But if the stock should pull back any meaningful amount or if fundamentals continue to improve, my opinion on the matter could change.

A company in transition

One of the things that I have really always appreciated about National Presto Industries is the fact that it is a mini conglomerate. The firm has a market capitalization of only $577.6 million as of this writing. But historically speaking, it has had multiple revenue streams. When I first bought stock in the company many years ago, the business was split between three different sets of operations. The first involved the production and sale of adult incontinence products. The second involved the sale of ammunition and non-lethal defense products. And the third involved regular household appliances.

{kind=link}

Today, the company looks a bit different. It still owns both the appliance and defense operations. But it has long since divested itself of its adult incontinence products. In its place, there is another segment called Safety, which produces and sells different types of sensors to monitor for things like carbon dioxide, smoke, humidity, water, and more. But this is a very small part of the company. During the first nine months of the 2023 fiscal year, the Safety business accounted for just under $1.1 million of revenue, or about 0.4% of overall sales. The bulk of the business nowadays is under the Defense segment, with sales during the first nine months of the year totaling $179.9 million. That's 74.2% of overall revenue. This is up from the 56.9% of revenue that the segment accounted for in the first nine months of 2009. But it's not because the segment has grown. In fact, revenue for it is actually lower than it was back then. Instead, the disappearance of the adult incontinence products, combined with a decline in the Housewares/Small Appliances segment, was responsible for this shift.

For better or worse, at least recently, the increased exposure to the Defense segment has proven to be a positive for shareholders. If we strip out the $7.9 million loss that the Safety segment had during the first nine months of 2023, we find that the Defense segment accounts for 74.3% of the company's overall operating profits. As this segment grows, the firm's bottom line is also improving nicely. And growth is something that the company has seen as of late. Consider, for instance, the first nine months of 2023 from a revenue perspective. During that time, sales came in at $242.5 million. That's 16.8% above the $207.6 million reported one year earlier. Although the Safety segment of the company more than doubled in size, that increase barely does anything for the enterprise. And over this window of time, the Housewares/Small Appliances segment has actually seen revenue drop by 14.9%.

The vast majority of the sales increase, then, has come from the Defense segment. At a time when the Housewares/Small Appliances segment of the company suffered because of a drop in unit sales, as well as reduced pricing and an unfavorable product mix, the Defense segment saw a 33% jump in revenue because of higher shipments associated with the company's growing backlog. That backlog, as of the end of the most recent quarter, was $554.9 million. That's comfortably above the $497.9 million reported for the same quarter of the 2022 fiscal year. So if anything, revenue should continue to climb from this point on.

With this rise in sales has come improved profits. Net income of $21.4 million in the most recent quarter beat out the $18.5 million reported one year earlier. Operating cash flow went from negative $3.3 million to positive $28.8 million. If we adjust for changes in working capital, we would get a rise from $21.4 million to $27.4 million. And meanwhile, EBITDA for the company expanded from $23.6 million to $26.2 million.

{kind=link}

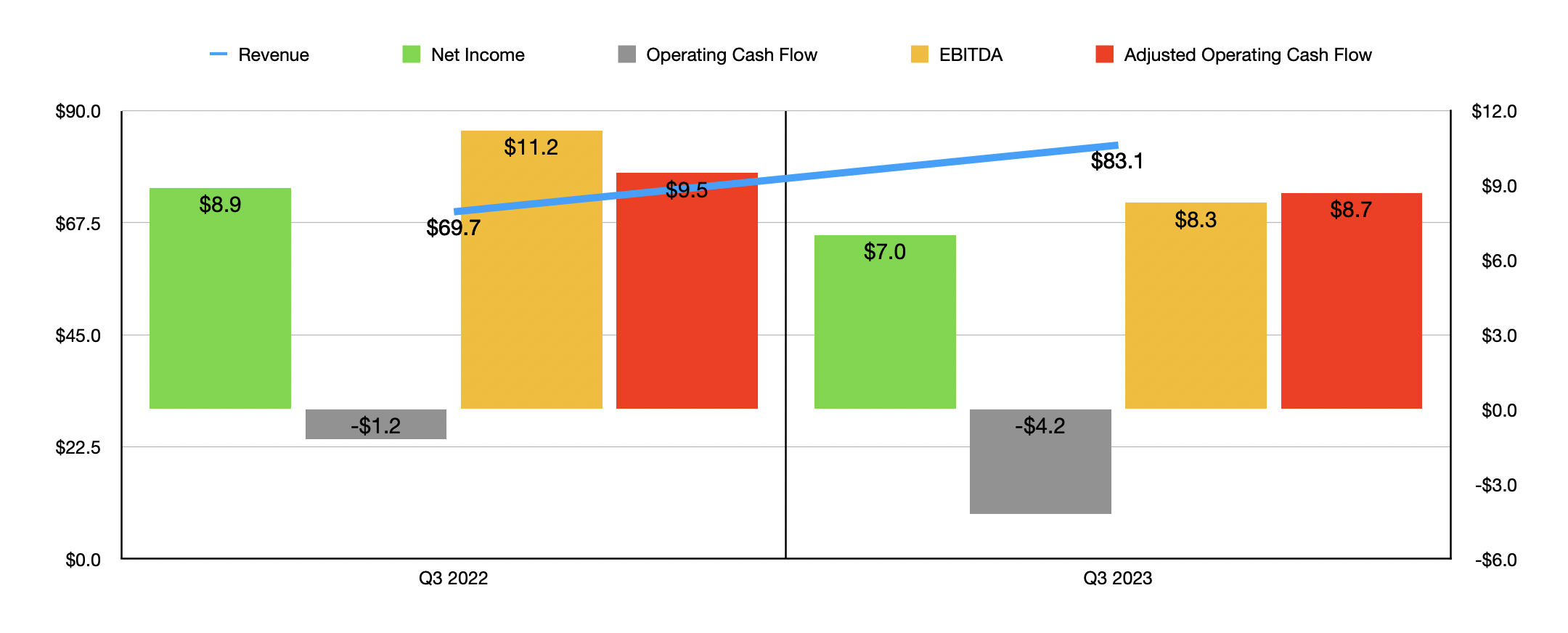

This is not to say that everything is going great for the business. The third quarter of the 2023 fiscal year showed some rather mixed results. Thanks to the 44.8% surge in revenue associated with the Defense segment, revenue in the most recent quarter totaled $83.1 million. That's well above the $69.7 million reported one year earlier. However, bottom line results have come under some pain. This came about even as operating profit for the Defense segment jumped by 44.9%. And it was driven by continued pain associated with the Housewares/Small Appliances business. As revenue dropped from $27.1 million to $21.5 million, operating profit plunged from $3 to only about $760,000. The drop in units shipped, combined with weaker pricing, severely impacted margins associated with this business. There were also some other costs, such as an extra $357,000 associated with self-insurance.

Because of this pain, not only did net income for the business decline from $8.9 million in the third quarter of 2022 to $7 million at the same time of the 2023 fiscal year, but other profitability metrics also worsened as well. Operating cash flow went from negative $1.2 million to negative $4.2 million. On an adjusted basis, it declined from $9.5 million to $8.7 million. And lastly, EBITDA fell from $11.2 million to $8.3 million.

{kind=link}

In addition to struggling with some of these operations, shares just are not as cheap as I would like them to be. If we annualize results experienced so far for 2023, we should anticipate net profits of about $23.9 million, adjusted operating cash flow of $36.5 million, and EBITDA of $33.6 million. Using these figures, I was able to value the company as shown in the chart above. I then compared the company to five similar firms as shown in the table below. Using the price to earnings approach and the price to operating cash flow approach, I found that two of the five companies ended up being cheaper than it. But because of the $95.4 million in cash that the business has on hand, with no corresponding debt, its enterprise value results in only one of the five companies being cheaper than it on an EV to EBITDA basis.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| National Presto Industries |

| 24.2 |

| 15.8 |

| 14.4 |

| Astronics ( ATRO ) |

| 5.7 |

| 186.7 |

| 53.9 |

| AerSale ( ASLE ) |

| 108.8 |

| 17.8 |

| 55.5 |

| Kaman ( KAMN ) |

| 37.8 |

| 7.5 |

| 44.0 |

| Triumph Group ( TGI ) |

| 6.5 |

| 5.2 |

| 16.5 |

| Ducommun ( DCO ) |

| 34.1 |

| 18.2 |

| 13.5 |

Takeaway

Given how shares of National Presto Industries our priced relative to similar enterprises, you might think that I would be bullish on the business. However, that's not the case. For starters, because other parts of the company dragging it down, sales under the Defense segment or actually lower than they were when I first founded the business back in 2009. It's also clear that the Housewares/Small Appliances business continues to be a drag. If management were to consider offloading this, my mindset might change. But between how the stock is priced on an absolute basis and the absence of growth over the past several years as a whole, I believe that the 'hold' rating I assigned the stock previously still makes sense.

For further details see:

National Presto Industries: Recent Growth Does Not Warrant Further Upside