PSA - National Storage Affiliates: Buy This 7% Yielding Self-Storage REIT

2023-10-17 16:00:46 ET

Summary

- National Storage Affiliates is a well-managed self-storage REIT with an impressive track record of growth.

- The market seems to be overly-rotated on a normalization of NSA's operating fundamentals after 2 years of gangbuster growth.

- It trades at a substantial discount to peers and sits below my fair value estimate, giving investors a high-yield opportunity.

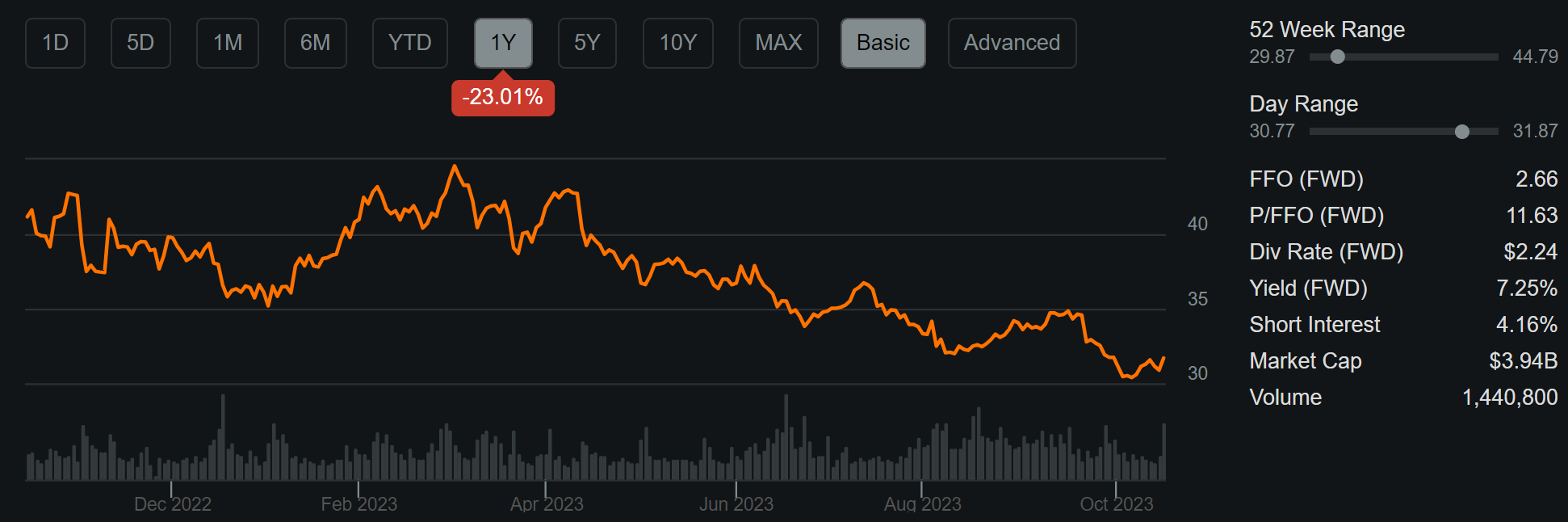

It's been a while since I last visited National Storage Affiliates ( NSA ) here back in January with a 'Buy' rating, noting its industry-leading growth over the past 5 years, among other points. The stock has seen its share of ups and downs since then, rising as high as $44.79, and at present, trades toward the low-end of its 52-week range, as shown below. In this article, I revisit NSA and discuss why I remain bullish on the stock at the present valuation, so let's get started!

{kind=link}

Why NSA?

National Storage Affiliates is the smallest of the 'Big 4' self-storage REITs. Its property portfolio is predominantly located within the top 100 metropolitan statistical areas and consists of 1,117 properties in 42 states and Puerto Rico.

NSA has seen a substantial downturn in price, as mentioned earlier. Speculating on specific reasons for the share price downturn over the past 12 months is difficult, but I would presume that higher interest rates are one cause, as REITs have plenty of competition from fixed-income investments, and higher rates pose a risk for debt refinancing.

Moreover, NSA has seen a slowdown in demand for rental units since the early pandemic years, when people were stuck at home and cleared out space (thereby needing self-storage) to make living at home more amenable. This weakness is reflected by same-store occupancy trending down to 90% during Q2, down from 95% in the prior year period. Before investors panic, it's worth noting that NSA's occupancy has simply normalized and still sits higher than where it was in pre-pandemic times, as reflected by 88% occupancy at the end of 2019.

Unlike its peers like Public Storage ( PSA ) and Extra Space Storage ( EXR ), which have grown in recent times through large acquisitions, such as Simply Storage for PSA and Life Storage for EXR, NSA pursues a more measured approach through working with Participating Regional Operators, otherwise known as PROs. PROs have a vested interest in NSA through operating partnership units and NSA benefits from their local market expertise and sourcing capabilities.

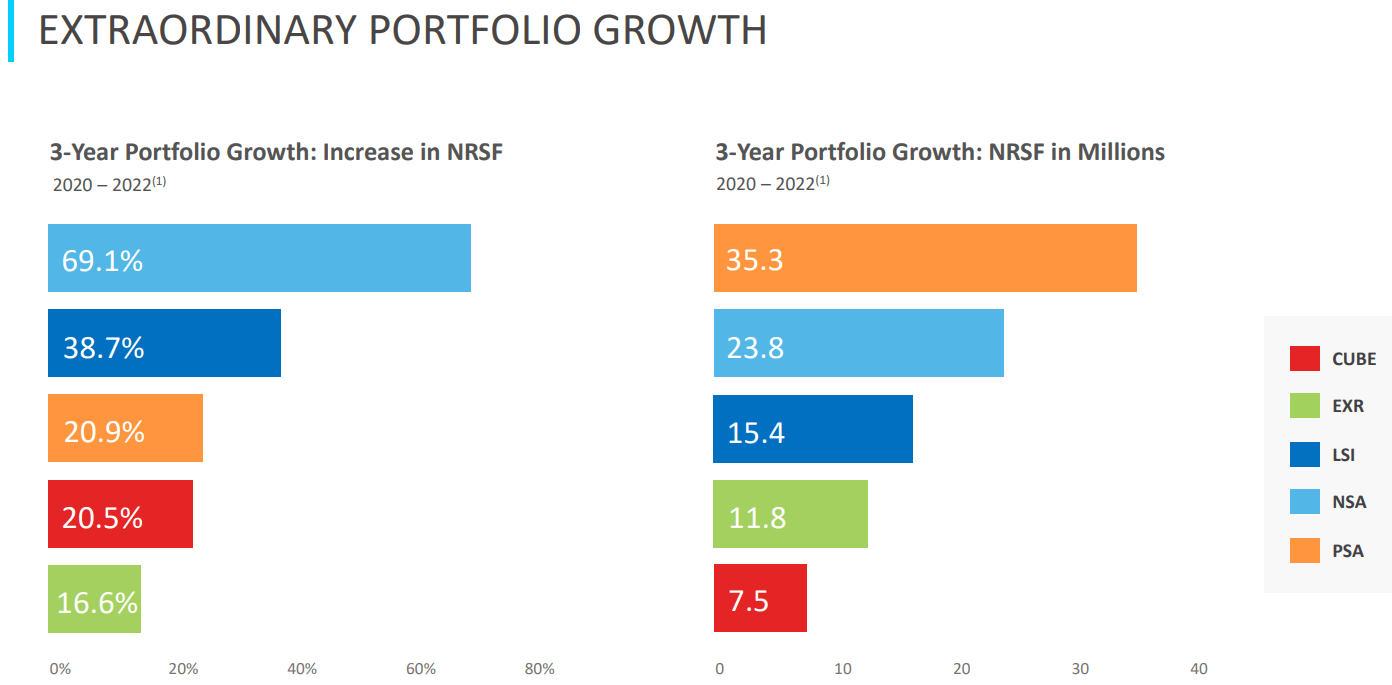

PROs serve as NSA's eyes and ears on the ground as they are well-equipped at identifying investment opportunities and serve as a captive pipeline of sorts, should they agree to be fully acquired by NSA down the road. This strategy combined with other acquisitions and joint ventures has enabled NSA to grow substantially over the past 10 years. As shown below, NSA has led its peers on portfolio growth on a percentage basis over the past 3 years and ranks second (behind PSA) on a net square footage basis.

{kind=link}

Encouragingly, NSA was able to price its rentals competitively despite a normalization in the occupancy rate. This is reflected by same-store revenue growth of 2.8% YoY, outpacing the 1.4% SS expense growth during the same quarter, resulting in a still respectable SS NOI growth of 3.4% compared to the prior year period.

Looking ahead to Q3 results coming up on November 1st and beyond, I would expect to see both internal growth through rent increases and opportunistic external growth through captive pipeline acquisitions. Management updated on its captive pipeline potential through the work of PROs during the last conference call :

" We think [property sourcing] is the strength of ours. [The Captive Pipeline] sits at $1 billion to $1.5 billion of properties that are not in the REIT yet, and the PROs are very actively working outside of the REIT today to find good properties, acquire good properties or build new properties, which will then eventually come into that captive pipeline. "

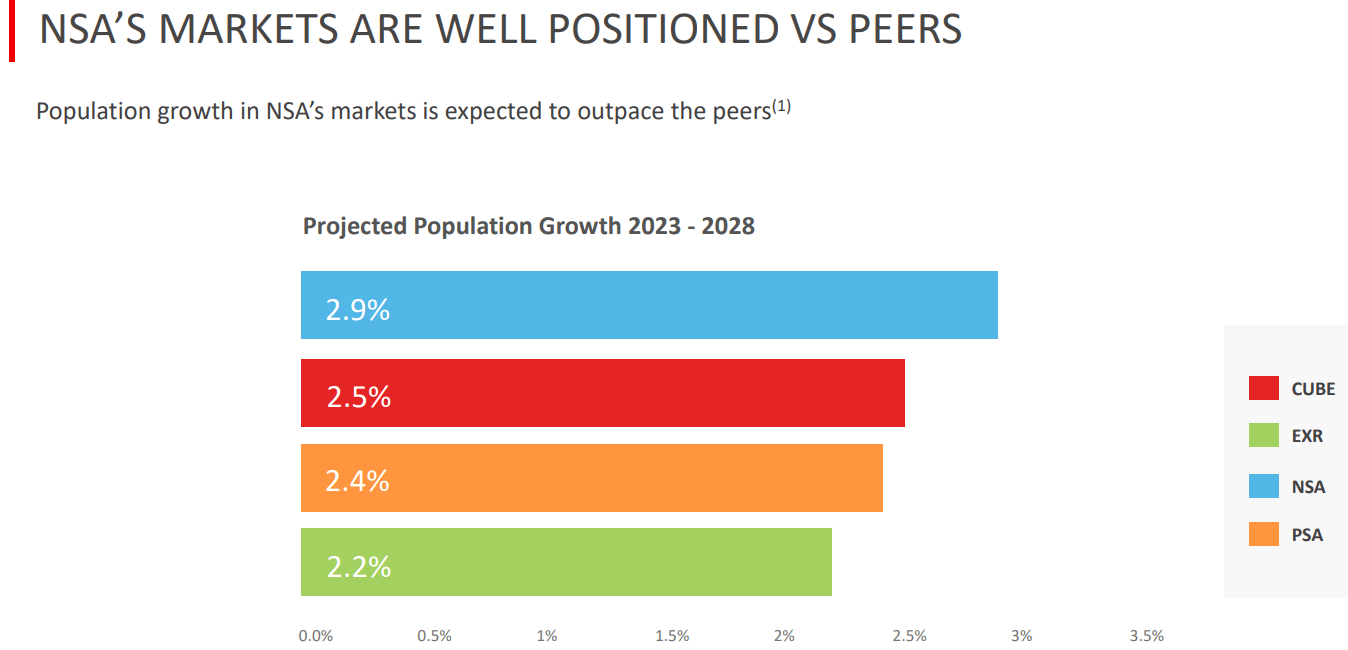

Internal growth potential is supported by above-average population growth in NSA's markets relative to peers and by rent growth potential due to a typical 10x10 Unit Annual Rent as a % of Median HH Income sitting at the lowest at 2.2% compared to the next lowest peer's ( CUBE ) 2.4%.

{kind=link}

Risks for NSA include higher for longer interest rates, as 20% of its debt is variable rate. This was reflected by higher interest expense pushing down FFO per share by 4.2% YoY, offsetting the gains from the aforementioned same-store NOI growth. Also, the self-storage space is well-known for being at risk from oversupply due to their easy-to-develop nature. However, supply from higher-leveraged private market players may be muted during this rate environment.

Nonetheless, NSA demonstrated its ability to source relatively low-cost capital in this high-rate environment, as reflected by its issuance of a 5-year $120 million unsecured notes at a 5.75% effective rate. Net debt to EBITDA also sits at the low end of management's target range at 6.1x (down from 6.3x at the end of the first quarter).

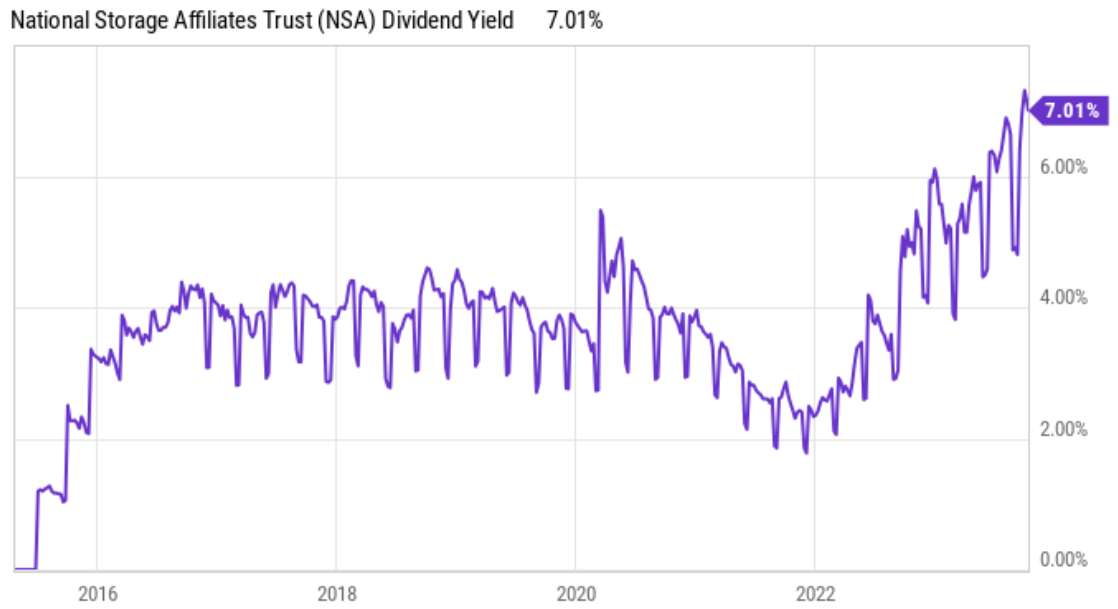

Meanwhile, NSA pays an attractive 7.1% dividend yield that's covered by an 84% payout ratio and comes with a 5-year dividend CAGR of 14.3%, although I wouldn't expect dividend growth to be as high in the near term due to the impact of higher interest rates. As shown below, NSA's dividend yield currently sits at one of its highest points over the past 10+ years.

(Note: The following graph shows TTM dividend yield. Forward yield is 7.1%)

{kind=link}

Turning to valuation, I find NSA to be attractive at the current price of $31.69 with a forward P/FFO 11.9 sitting far below its normal P/FFO of 20.4. Granted, I don't expect NSA to trade anywhere near its normal P/FFO due to near-term interest rate headwinds. However, I believe the market is being a bit too pessimistic around the stock.

Performing an NPV analysis, I arrive at a fair value of $36.40. This is based on the current year FFO/share expectation of $2.66, a 3.5% growth rate (which resembles NSA's SS NOI growth during Q2, and a 5.75% discount rate, which resembles NSA's effective interest rate on bonds issued during Q2. This fair value estimate sits within the range of analyst price targets from $29 to $38 .

NPV Analysis (Produced by Author)

{kind=link}

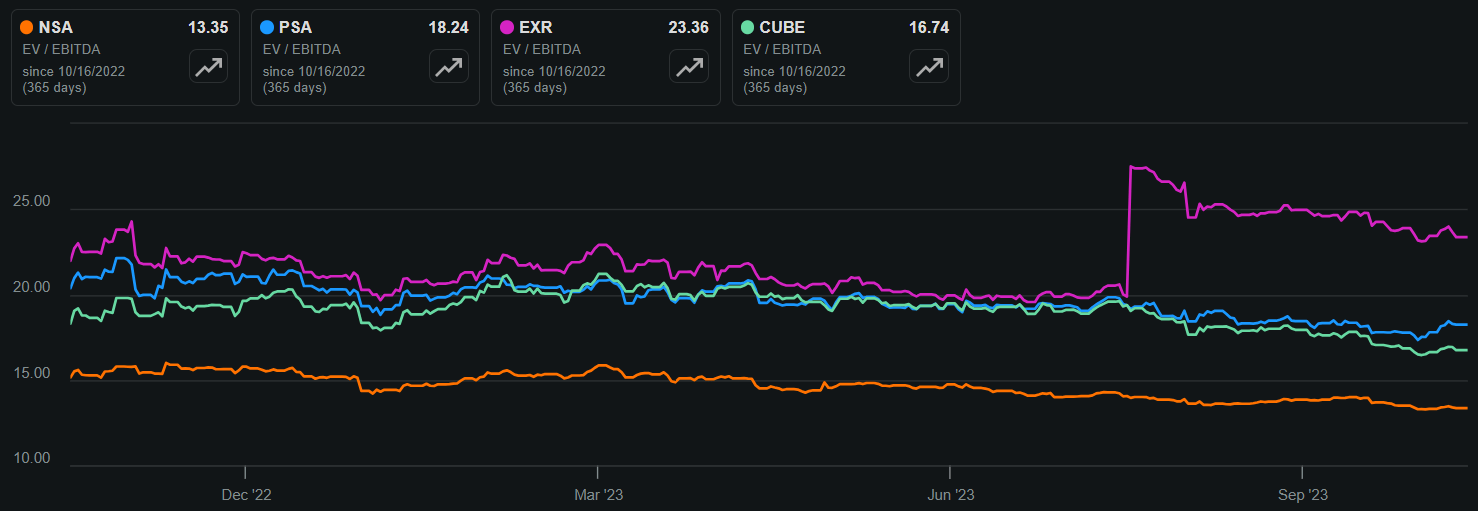

NSA also trades at a substantial discount compared to peers. As shown below, it carries an EV/EBITDA of 13.4, sitting well below that of PSA, EXR, and CUBE.

NSA & Peers' EV/EBITDA (Seeking Alpha)

{kind=link}

Investor Takeaway

Overall, I believe NSA is a well-managed and differentiated self-storage REIT that offers investors a combination of attractive dividend yield and growth potential. The company's unique PRO strategy has proven successful in driving portfolio growth and capturing investment opportunities.

While near-term growth may be muted due to higher interest rates and a slowdown in demand, I believe some of the slowdown is simply a normalization after a couple of years of gangbuster growth. Meanwhile, value investors get to take advantage of what I see as being overly negative market sentiment. As such, I maintain my 'Buy' rating on the stock.

For further details see:

National Storage Affiliates: Buy This 7% Yielding Self-Storage REIT