PSA - National Storage: Room For Improvement And A Lot To Prove But Valuation Looks Good

2024-01-12 07:35:56 ET

Summary

- National Storage Affiliates is a real estate investment trust specializing in self-storage properties.

- Self-storage services are resilient during economic crises due to consistent demand driven by life events.

- The self-storage market is growing due to population growth, urbanization, and consumerism, with a fragmented market offering acquisition opportunities.

- The quality of the company is somewhat lower than that of its competitors, but valuation adjusts to this and it's still a good business to invest in.

Investment Thesis

National Storage Affiliates Trust operates in the appealing self-storage sector, which exhibits structural characteristics that render it stable and with growth potential - making it an attractive prospect for investment.

This article will delve into an analysis of National Storage and its primary competitors to articulate why I believe the company holds significant potential for improvement , making it an enticing investment opportunity. However, this also implies that the company has much to prove before claiming victory. Additionally, I find the valuation appealing at the current price, leading me to believe that the risk/reward balance is favorable, and, in my opinion, it is a ' buy '.

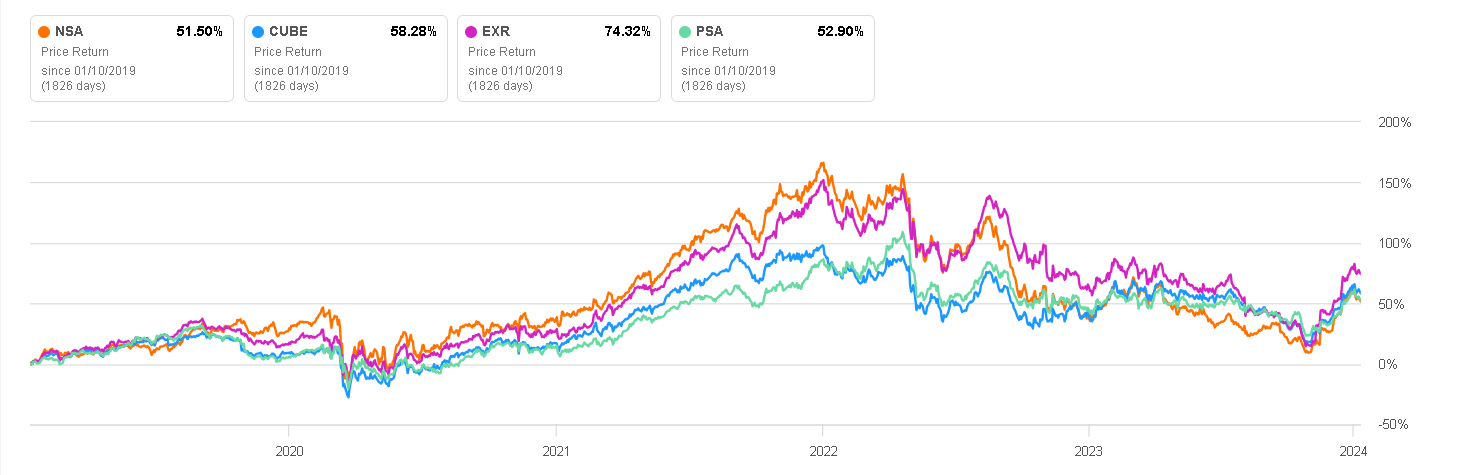

NSA Price Return vs Competitors (Seeking Alpha)

{kind=link}

Business Overview

National Storage Affiliates (NSA) is a real estate investment trust specializing in the ownership, operation, and acquisition of self-storage properties in the United States. This is a business that is quite simple to understand and even somewhat boring, however, it proves to be much more intriguing for investment purposes than initially perceived.

Not Even 2008 Crisis Was a Problem

Self-storage services tend to exhibit resilience during macroeconomic crises because the demand for such services is typically driven by significant life events such as relocation, downsizing, marriage, divorce, or family bereavement. These events tend to persist irrespective of economic conditions, ensuring a consistent level of demand. Additionally, the provision of month-to-month rental agreements enhances customer flexibility, streamlining the renting process compared to committing to a fixed term, such as a year.

The robustness of self-storage services is exemplified by the performance during the economic crisis of 2008 of key companies like Public Storage, Extra Space Storage, or CubeSmart- all direct competitors of National Storage, which did not report their financial statements at that time. On average, during 2009, these companies decreased their revenue by only 2% , and by the following year, most of them had already recovered it. In other words, these REITs experienced only a modest annual revenue decline during the most substantial real estate crisis in recent history. If this is not resilience, I don't know what is.

{kind=link}

Attractive Structural Characteristics of the Sector

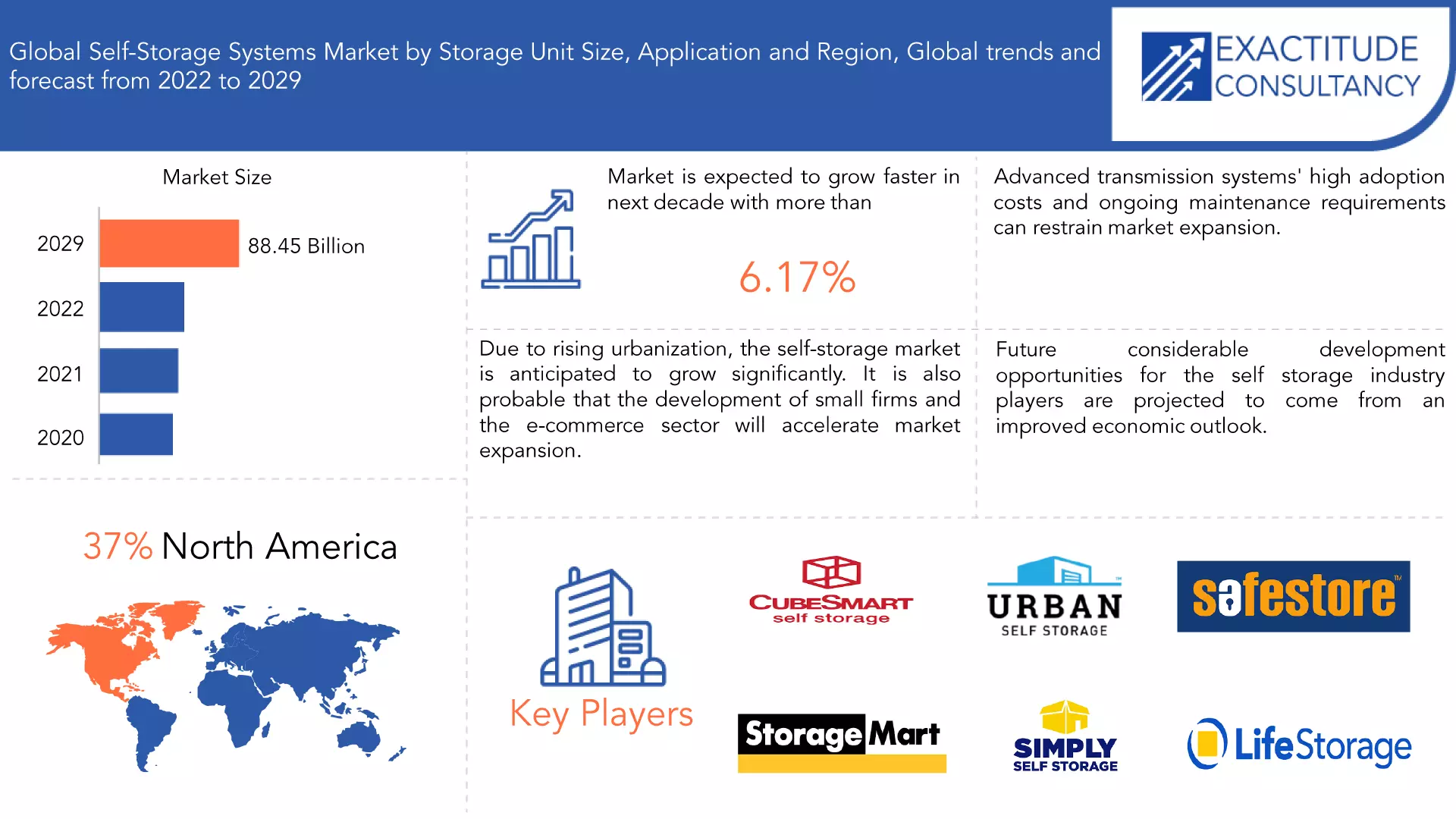

In recent years, the self-storage market in the United States has seen notable growth, with expectations that the global market will continue expanding at mid-single digits until at least 2029 . This growth is primarily driven by the steadily increasing U.S. population, as a larger populace typically results in heightened demand for storage solutions. Urbanization and demographic shifts, such as the trend of millennials relocating to cities for employment opportunities, contribute to the rising need for extra storage space.

Moreover, the prevailing culture of consumerism and the inclination to accumulate possessions also play a significant role in fueling the demand for storage space. As individuals acquire more belongings, the necessity for additional storage arises to accommodate items that may no longer fit in their homes. Given the escalating costs of apartment rentals, individuals might opt for smaller living spaces, leading to a surge in the demand for supplementary storage spaces to house possessions that can no longer be accommodated in their downsized residences.

Self-Storage Market (Exactitude Consultancy)

{kind=link}

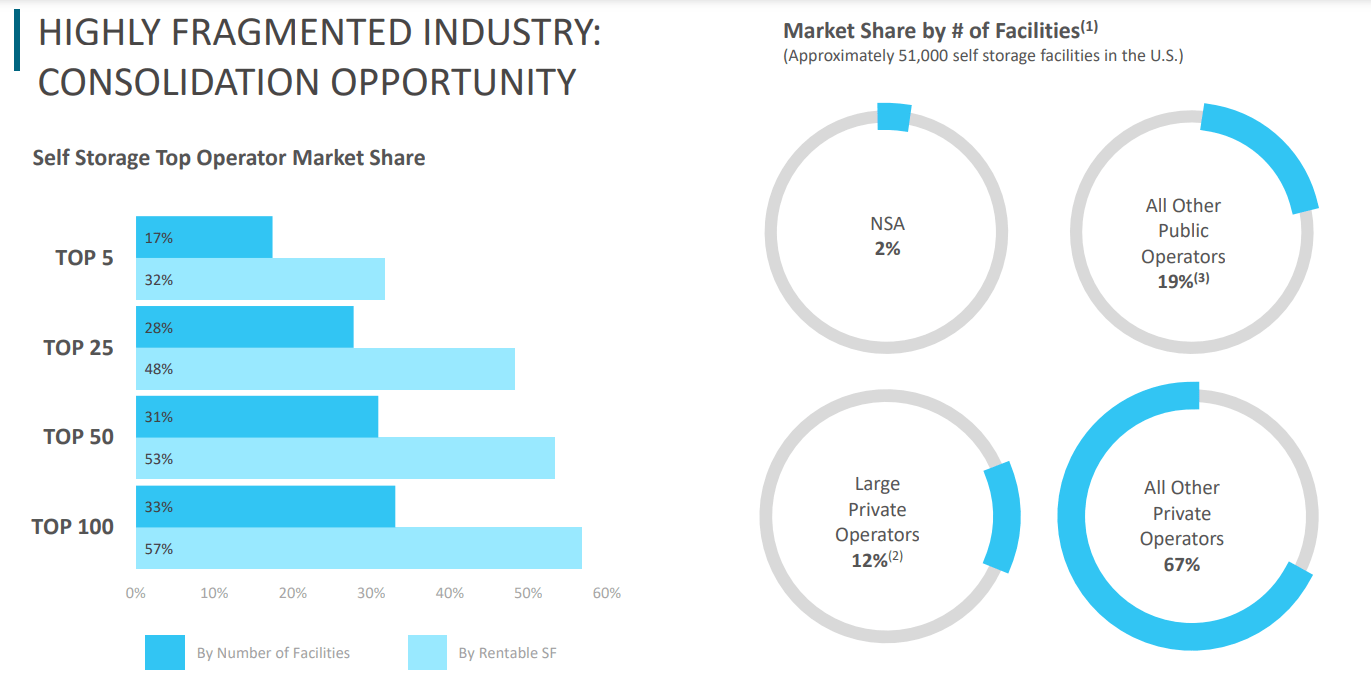

The self-storage sector is characterized by fragmentation , featuring numerous small and independent operators alongside a handful of larger national players. The relatively low barriers to entry in this industry facilitate the establishment and operation of facilities by entrepreneurs and local investors. In comparison to certain other real estate sectors, initiating and managing a self-storage facility may necessitate less initial capital and expertise.

The four primary players dominating the sector include Public Storage (PSA), with a revenue of $4.48 billion in the last twelve months, Extra Space Storage (EXR) at $2.32 billion, Cube Smart (CUBE) with $1 billion, and National Storage generating $860 million in revenue. Notably, U-Haul (UHAL), originally focused on moving items transportation, has recently ventured into the lucrative self-storage segment, capitalizing on its extensive distribution network and strong brand presence. All of these are listed on the stock market, so later we will compare them with National Storage, since the opportunity cost of not investing in the best player in the sector should not be ignored.

National Storage Investor Presentation

{kind=link}

Even though the five major competitors mentioned boast substantial revenues, they collectively represent only 30 to 40% of the total square footage available for self-storage rental and 15 to 20% of the total number of facilities available for rent. The majority of the market share, ranging from 60 to 70%, is dispersed among numerous small competitors. This fragmentation positions these smaller entities as potential merger and acquisition targets for larger players, fostering significant inorganic growth within the industry. It is not uncommon to observe larger competitors viewing each other as merger targets, as evidenced by the recent case of Extra Space Storage and Life Storage .

Key Ratios and Competitors

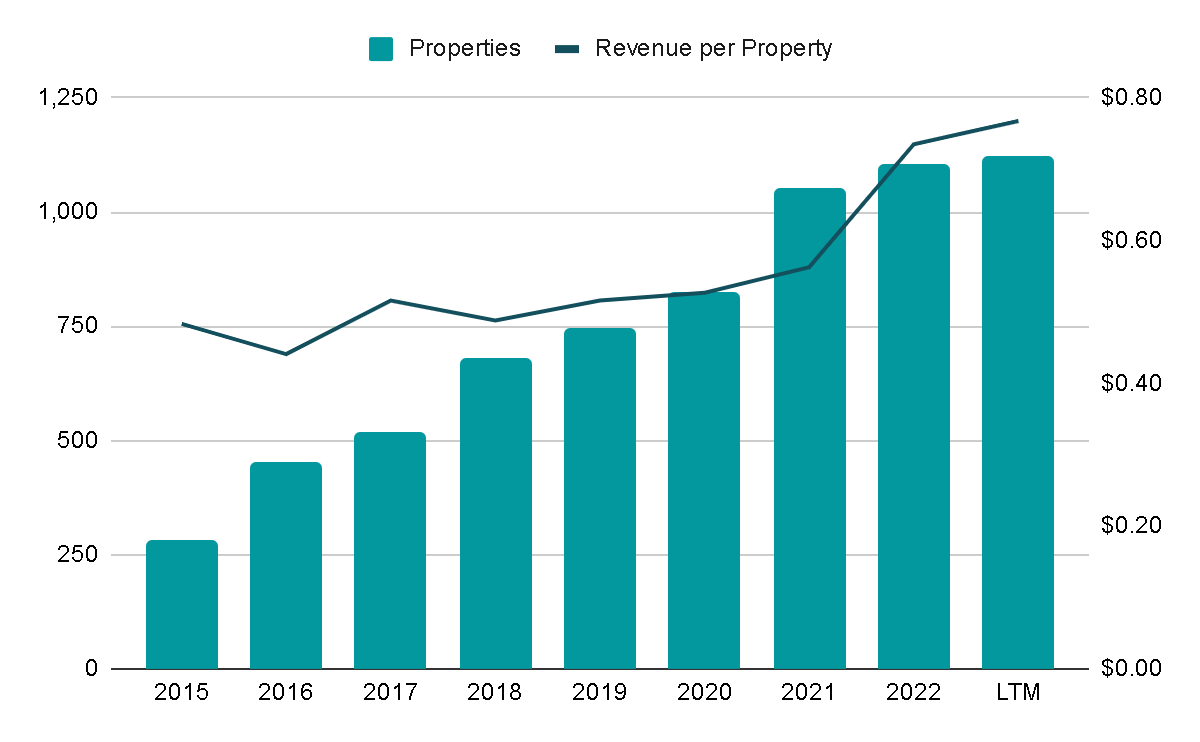

Since 2015, the company has achieved almost 30% compounded annual revenue growth by annually increasing the number of properties by 22%, facilitated by the ease of building self-storage facilities and available M&A opportunities. The remaining 6% annual growth stems from an increase in Revenue per Property. This can be accomplished by adjusting prices, for instance, in response to inflation. This adjustment is relatively straightforward since individuals storing their belongings in a facility are less likely to risk losing their stored items.

Simultaneously, the Funds From Operations ((FFO)) margin has risen from 34% in 2016 to the current 40%. Yet, there remains significant potential for expansion, as we will explore later. FFO margin serves as an ideal metric for analyzing REITs because it excludes certain items, such as the sale or purchase of assets, that could distort purely operational profits from Net Income.

{kind=link}

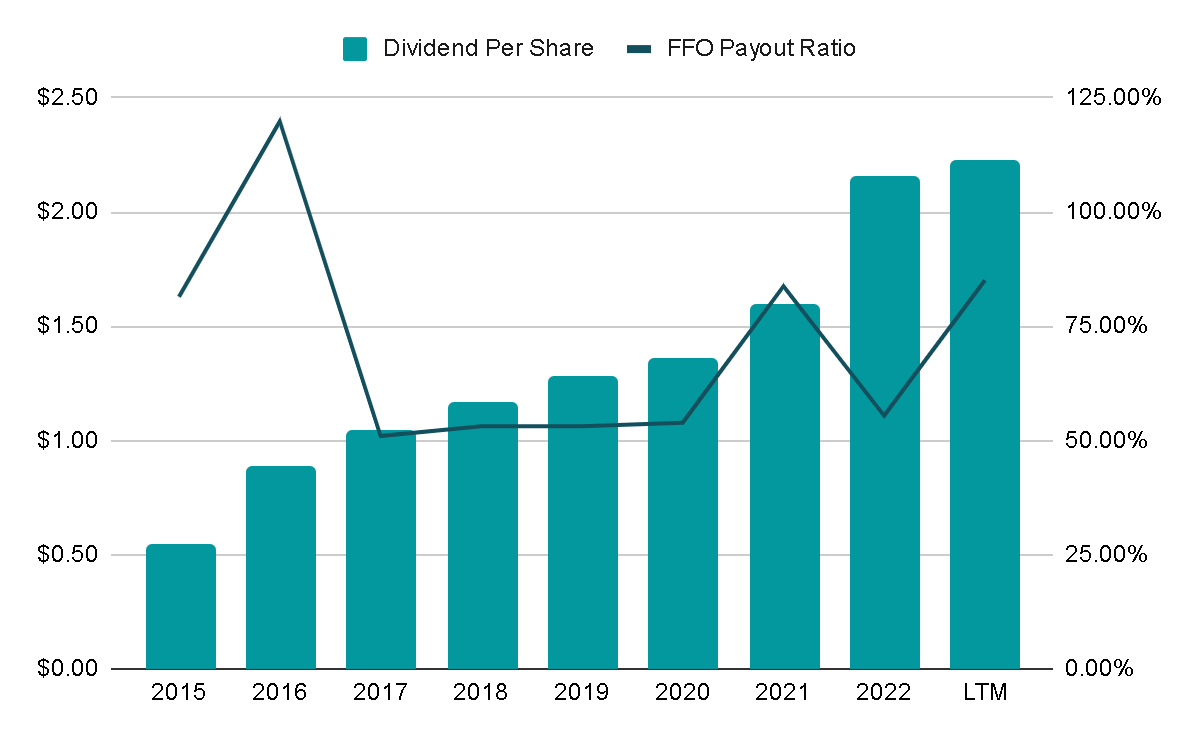

Another crucial aspect of investing in any REIT is the consideration of dividends . In this regard, there has been a noteworthy annual increase of 20% in the dividend per share distributed each year since 2015. Additionally, this increase has, on average, represented only 70% of the Funds From Operations, and the current level is at 85%, making the dividend quite sustainable.

{kind=link}

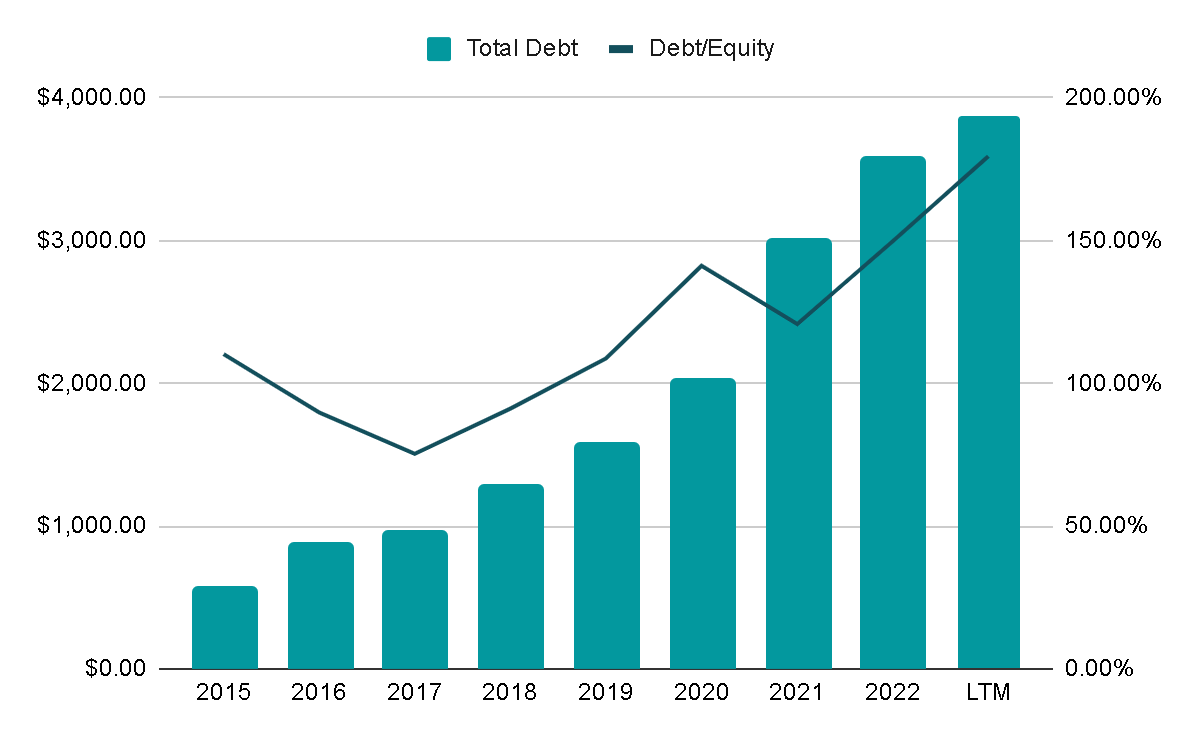

However, one concerning aspect is the issue of debt , a significant component for any REIT. Currently, NSA has total debt of $3.87 billion, resulting in a relatively high Debt/Equity ratio of 179.5%. While still manageable, this ratio has been increasing year after year. It is essential to scrutinize whether the company should continue sacrificing financial strength for growth.

{kind=link}

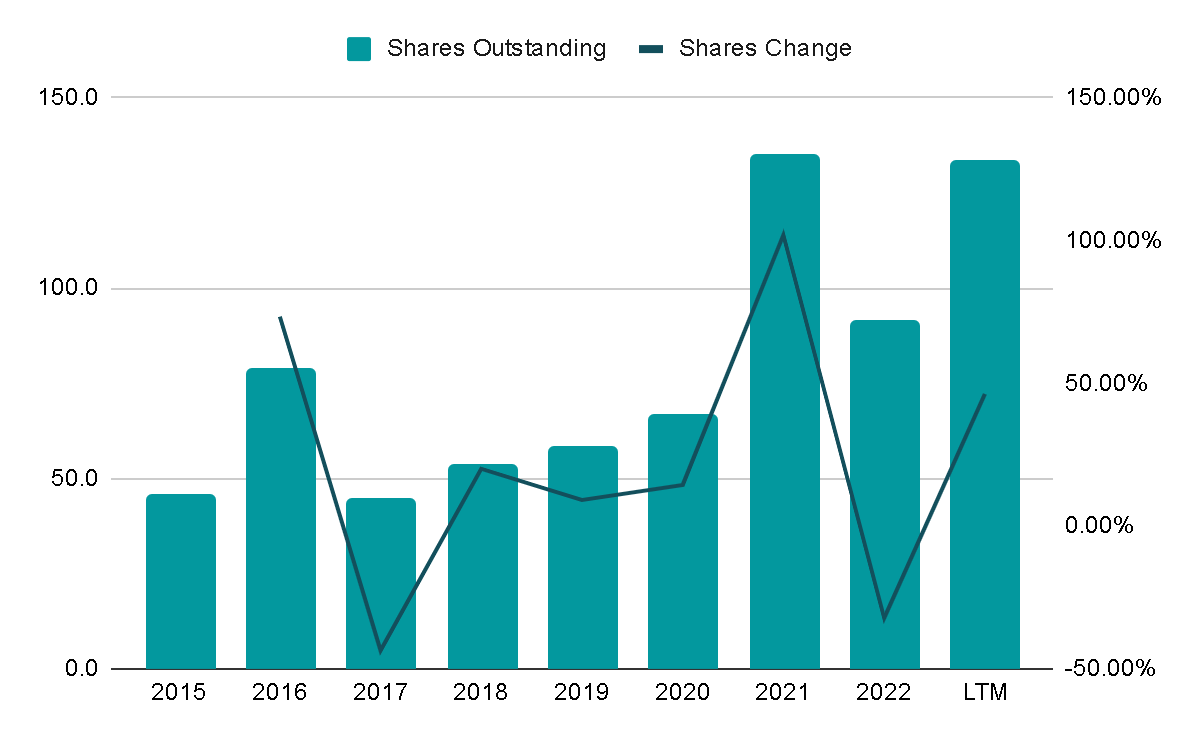

Furthermore, it's important to note that the company tends to dilute shareholder s considerably, issuing shares at rates of 20% since its IPO. Although this has been done to finance growth and has been justified by the 10% annual growth in revenue per share (accounting for dilution), continued issuance of shares without expected returns could potentially lead to value destruction.

While these issues don't seem like serious problems or imminent risks, they should be considered carefully, as they are akin to playing with fire.

{kind=link}

To contextualize these figures, we can also analyze the main competitors of National Storage. The table below suggests an apparent correlation between a company's scale and its Funds From Operations margin , which may be attributed to economies of scale, where fixed costs like property management, administrative expenses, and marketing are spread across a larger portfolio of properties. This, in turn, leads to lower average costs per unit, contributing to improved FFO margins and could explain why smaller companies, such as National Storage, are keen to expand rapidly.

It's noteworthy that the company is currently trading at a certain discount compared to its peers. In my opinion, this discount is justified. While National Storage has experienced the most growth in the last five years, it also carries more debt than its counterparts and has lower margins due to its smaller size, which, as we previously discussed, is a crucial factor in the dynamics of these companies.

{kind=link}

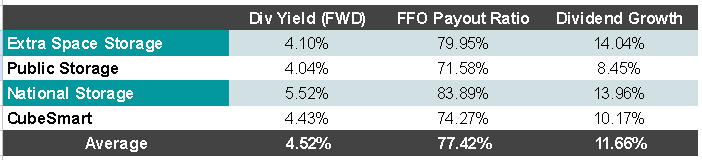

In terms of the dividend , National Storage currently boasts the highest dividend yield among its peers, offering a return of more than 5.5%. However, it is noteworthy that it is also the company that allocates the majority of its FFO to dividends. As mentioned earlier, while the current percentage of FFO Payout Ratio appears reasonable, assessing the sustainability of the dividend and the potential for future increases becomes crucial when determining the best company in the sector. It's relevant to explore companies with a more sustainable dividend and greater capacity to enhance it through an increase in the Payout Ratio, so it makes sense that the market demands a higher yield from National Storage.

{kind=link}

Valuation

In the valuation, I plan to quantitatively incorporate the qualitative aspects discussed throughout this article, providing an estimate of the potential return if one were to purchase at the current price.

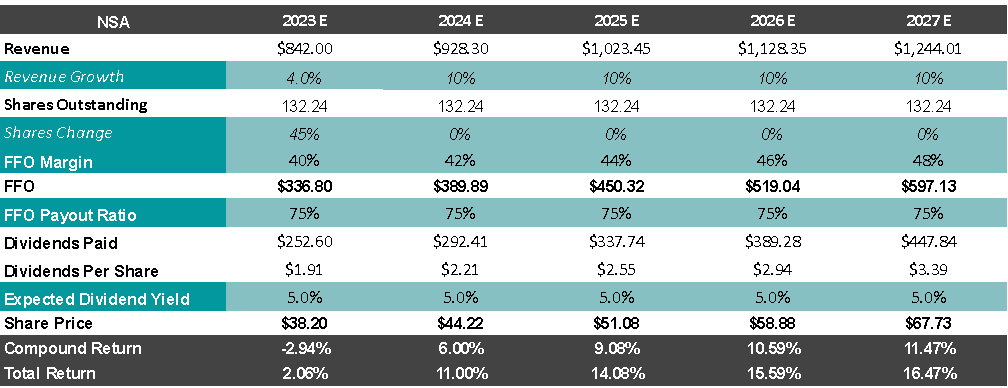

Considering the fragmented nature of the potential market and the company's current low market share, I anticipate double-digit growth in the upcoming years. This growth is expected to result from a combination of raising prices at rates of 2-4% and a 6-8% increase in the number of properties acquired. While the projected same-store revenue growth for this year is 2%, and property acquisitions have increased by around 2%, the company's potential for growth remains substantial. Additionally, there is the potential for an increase in the FFO Margin as the company gains scale. Even if it reaches 48% within five years, this would still be significantly lower than the current average margin of its peers, which stands at 62%.

{kind=link}

Conversely, I will penalize the company for the increase in shares outstanding, which has risen by 46% in the last twelve months. I also anticipate a slight decrease in the Payout Ratio towards the 75% average of the company and its competitors. Assuming a demanded dividend yield of 5% due to the company's need to prove itself further, the total return, including dividends, is estimated to be around 16.5%. This suggests a favorable return that, in my opinion, justifies the uncertainties related to the company's potential improvements in quality, market share gains, and debt reduction.

Final Thoughts

The company operates in a sector where it's challenging to go wrong. The business is stable, offering both organic and inorganic growth opportunities, and the competitive landscape is not overwhelming. There is ample room for the main players to expand. In the case of National Storage, the significant potential for improvement could serve as a driver of outperformance compared to its competitors, particularly in terms of stock market performance.

Nevertheless, it's crucial not to be overly optimistic about the company's promising aspects. There's still much to prove , and the substantial debt is a noteworthy concern. Additionally, the services offered by these companies are somewhat commoditized, with limited differentiation. Considering all these factors and the attractive valuation, I believe the company could be a ' buy ' at the current price, albeit with the acknowledged risks mentioned above.

For further details see:

National Storage: Room For Improvement And A Lot To Prove, But Valuation Looks Good