EYE - National Vision: Life After Walmart Seems Shaky

2023-08-17 04:49:59 ET

Summary

- National Vision Holdings is a major eyewear player in the US, but its growth has lagged behind competitors Luxottica and Warby Parker.

- EYE reported in-line earnings for Q2 2023, but its future growth prospects remain uncertain.

- We ascribe a sell rating amidst an anticipated reduction in eyewear spends, lofty valuation, and downside risks due to the end of partnership with Walmart.

Investment Thesis

National Vision Holdings ( EYE ) is among the largest eyewear player in the US with ~1,400 stores across the country. It operates through five brands including America's Best and Eyeglass World offering eye exams, eyeglasses, and contact lenses to budget-conscious and low income consumers. However, its growth has continually lagged its peers Luxottica and Warby Parker ( WRBY ) and its future seems blurry post the surprise end of its partnership with Walmart. With the elevated inflation, the eye wear spends is likely going to be in check as EYE caters to consumers most exposed to the impacts of a looming recession. We ascribe a sell rating amid weakening growth prospects and lofty valuations compared to its peers.

Lagging Growth

EYE has a relative underperformance compared to its peers Luxottica and Warby Parker. It had an outsized same store sales in the first half of 2021 driven by favorable comps as COVID and the lockdowns have had a significant impact on the business. However, post normalization, it continued to face significant pressure in driving sales growth despite a positive momentum in its America's best brand.

Same Store Sales Growth

| 1Q21 |

| 2Q21 |

| 3Q21 |

| 4Q21 |

| 1Q22 |

| 2Q22 |

| 3Q22 |

| 4Q22 |

| 1Q23 |

| 2Q23 |

| EYE |

| 36% |

| 77% |

| 0% |

| 1% |

| -7% |

| -12% |

| -8% |

| -2% |

| 1% |

| 1% |

| LUX |

| 7-9% |

| 11% |

| 10% |

| 9% |

| 3% |

| 2% |

| 3% |

| 3% |

| 7% |

| 2% |

| WRBY |

| 26% |

| 96% |

| 31% |

| 18% |

| 10% |

| 14% |

| 8% |

| 10% |

| 12% |

| 11% |

In Line Earnings

EYE reported in line set of numbers for Q2 following the early pre-announcement with comp growth of 1.0% driven by strength in managed care customers, modest pricing, and increased exam capacity. Gross m argin declined 120 bps YoY primarily driven by higher optometrist-related costs (-140 bps effect) and reduction in other components of service revenue partially offset by higher exam revenue (+90 bps effect) and additional pricing actions and freight tailwinds. EBITDA margin declined by 250 bps as a result of lower gross margins and SG&A deleverage driven by higher payroll and performance-based incentive compensation along with occupancy deleverage. It reported an EPS of $0.17 in line with consensus expectations.

Balance sheet remains stronger with Net Debt/ TTM EBITDA of just 1.9x and liquidity of ~$550 mn, including cash balance of $250 mn with no borrowings under its revolving credit facility. Inventory position declined 6% YoY but still remains elevated amidst pressure on gross margins.

It expects 2023 EPS to be at or above the midpoint of their previous guidance range (previous guidance range of $0.42-$0.60, now implying EPS of $0.51-$0.60).

End of an Era

EYE announced the end of its partnership with Walmart that began three decades ago which led to the shares cratering about 20%. Walmart contributed ~$350 mn in sales in 2022 and $15 mn in EBIT $ which forms ~17% of total revenues and 25% of total EBIT. This includes agreement for EYE to operate Vision centers inside select Walmart locations (to end in Feb 2024) along with AC Lens ( to end in June 2024). Assuming a 25% effective tax rate, EPS contribution could be estimated at $0.14 in 2022 from Walmart partnership (~22% of total), however, the contribution in 2023 is expected to be lower.

Management expects that it can mitigate the financial impact from exiting the agreements by focusing on growing its America's Best and Eyeglass World brands along with cost saving initiatives. However, its core business has been struggling with lackluster comps while higher spending on remote medicine initiatives may take several years to pay off, putting them in a tough situation.

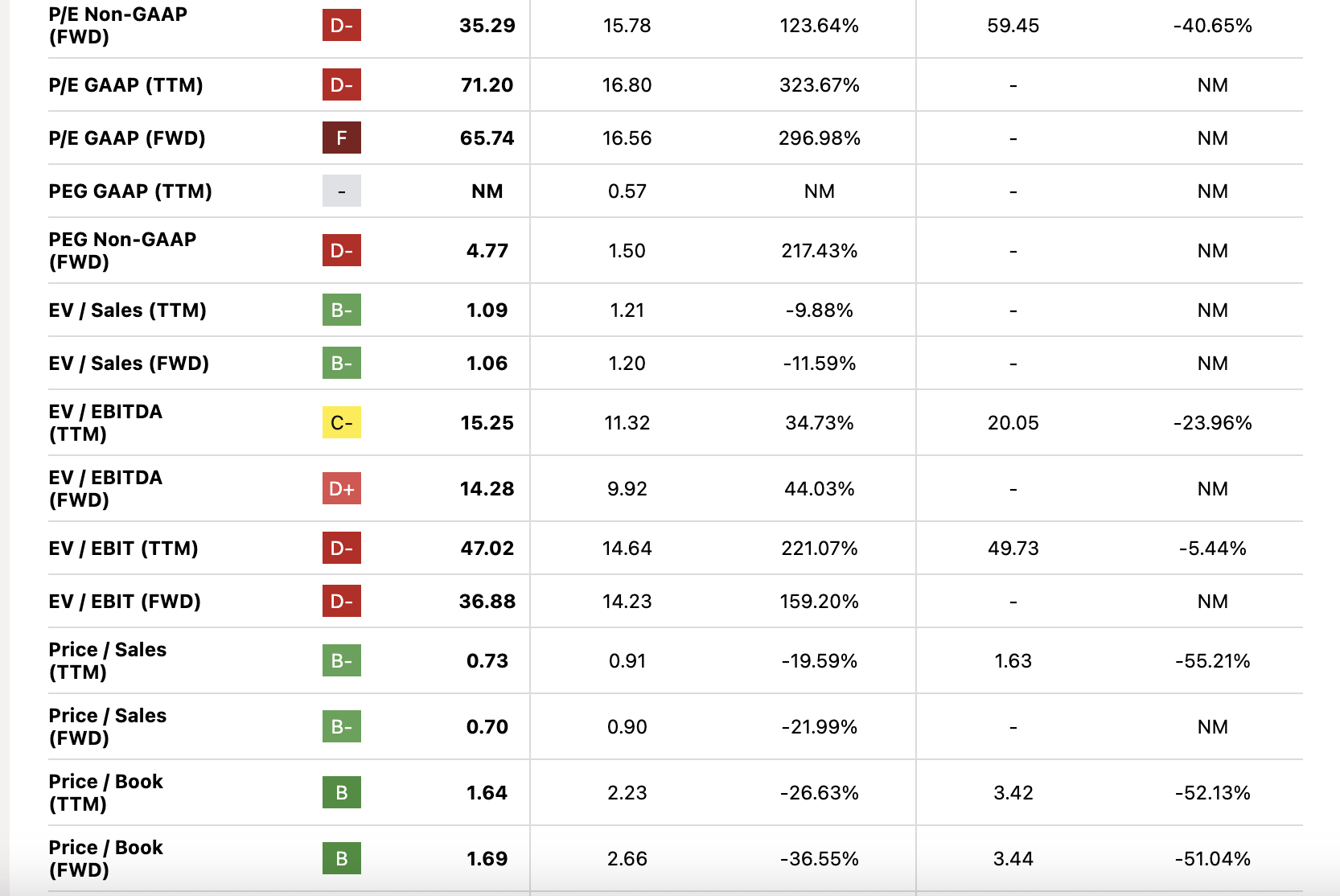

Valuation

Despite its shares declining 20% since the Walmart announcement, EYE's valuation remains lofty. While the company benefits from its network reach and growth potential, its outlook remains uncertain and it would be significantly challenged in finding growth avenues to fill the 20% profit hole.

{kind=link}

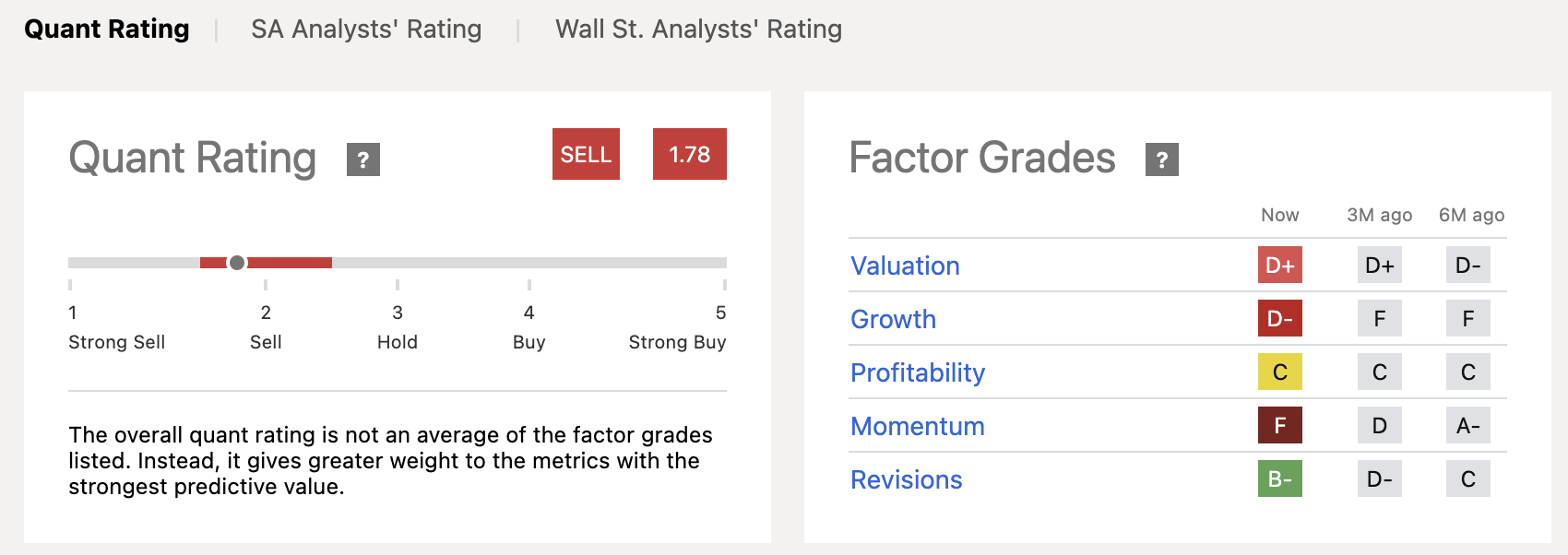

Seeking Alpha's Quant Rating ascribes a Sell Rating amidst declining growth and lofty valuations compared to its peers.

{kind=link}

We assume sales will decline MSD for 2024 with margins remaining flat to mildly positive partly helped by exiting the loss making AC lens business. We believe expected EPS will decline MSD for 2024 in line with the decline in sales and peg it at $0.45 range. We initiate at Sell with a target price of $15 at 35x 2024E, in line with its historicals.

Risks to Rating

Risks to rating include

1) Growth in America's Best brand driven by its dark stores and improving exam capacity could offset the loss of business by Walmart divestiture. Margins could further expand as a result of higher than anticipated cost benefit from the loss of Walmart partnership

2) Rebound in eyewear spend as a result of improvement in the overall economy which can spur growth

3) Higher than anticipated benefits from its cost saving initiatives which it expects to launch in 2024

Conclusion

EYE's sales trajectory has continually lagged its peers and its unexpected end of a decadal partnership with Walmart puts a bigger hole in its profit. We believe EYE's expectation that it can recoup the lost growth from its legacy brands could be challenged amidst continued risks on the optical repurchase cycle and its relatively soft traction with America's Best remaining a silver lining. The divestiture is hence likely going to push EYE's long term financial targets of achieving MSD comp growth & MSD adj. Operating margins even further. We ascribe a sell rating amidst elevated inflation pressuring EYE's low margin consumer and further lengthening the optical replacement cycle along with lofty valuations and downside risks due to Walmart loss.

For further details see:

National Vision: Life After Walmart Seems Shaky