NTCO - Natura &Co: More Risk Than Reward

Summary

- While 2022 was a challenging year, Natura isn’t out of the woods yet.

- In addition to the withdrawn guidance and recent fines, the leverage levels are also a concern.

- An Aesop sale could de-risk the investment case, but it remains early days.

- The valuation isn’t cheap enough relative to the risks, and I would hold off at these levels.

Leading beauty company Natura &Co ( NTCO ) has underperformed the benchmark Ibovespa index in 2022 and ended the year with more bad news - its subsidiary Avon Products has been sentenced to pay out a not insignificant fine amounting to a mid-single-digit % of its cash position. With guidance also dropped in the last quarter, uncertainty around the earnings trajectory is high, and there could be more downward revisions ahead.

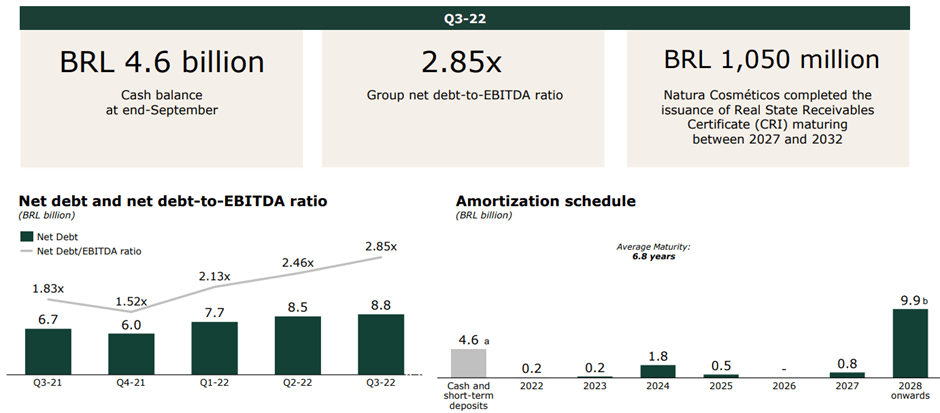

Perhaps the most pressing concern is the leverage at ~3x net debt/EBITDA, along with the cash burn and one-off restructuring costs, which could drive a dilution event in the near term. The silver lining is that the new management team could still delay a liquidity crunch by unlocking P&L efficiencies and potentially also by raising funds via a minority stake sale of Aesop, a luxury cosmetics brand within the NTCO portfolio. Still, the stock isn't all that cheap at ~7x forward EBITDA; pending reinstatement of the guidance and improved visibility into the restructuring, I am on the sidelines.

Avon Fine Further Weighs on the Liquidity Runway

NTCO recently published a notice to the market, disclosing a ~$46m fine ($36m in compensatory damages and $10m in punitive damages) with regard to litigation in the US involving key subsidiary Avon Products. This case, related to asbestos contamination in its talc products that may have contributed to cancer development, is one in a long line of lawsuits faced by Avon in recent years (note Avon faced ~200 talc lawsuits in 2021). With peers like Johnson & Johnson ( JNJ ), Revlon ( REVRQ ), and L'Oréal S.A. ( LRLCY ) also suffering losses in similar talc-related litigation , the outcome was perhaps unsurprising.

Per the NTCO release, Avon stopped the sales of these products in the US in 2016, so we should hopefully be reaching the end of the line on the asbestos litigation front. While Avon claims to have a strong case to overturn the verdict (note the decision isn't final), I think it would be prudent to pencil in the full balance sheet impact (~5% of the Q3 cash position) at this point. The ESG impact is also worth considering - I wouldn't be surprised to see a minor de-rating in the coming months as NTCO stock becomes a less attractive option for ESG flows.

{kind=link}

Withdrawn Forward Guidance is a Major Overhang

The negative litigation news comes on the heels of NTCO withdrawing its guidance numbers following the Q3 earnings result (material fact published here ). This covers not only P&L line items like revenue and EBITDA but also potential synergies from the Avon Products combination. While the latter was a negative surprise, NTCO's prior decision to postpone its forward guidance for revenues (R$47bn-49bn previously) and leverage (<1x net debt/EBITDA target previously) through FY24 means the official withdrawal had likely been priced into market expectations.

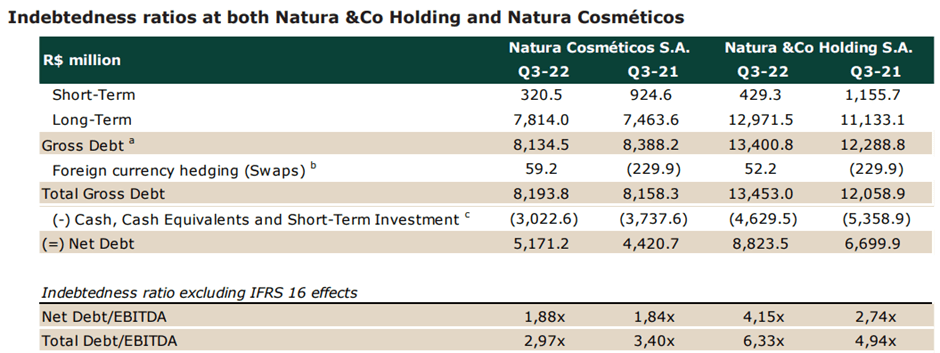

At this point, my biggest concern is the lack of guidance on debt levels. NTCO closed its last quarter at ~4x net debt/EBITDA adjusted for leases, which is quite a long way off the prior leverage target. The silver lining is that the NTCO debt covenants are linked to the Natura Cosmeticos subsidiary (i.e., Natura ex-Avon), so there remains headroom for now. For context, excluding Avon, leverage at Natura Cosmeticos stood at 1.9x net debt/EBITDA vs. the 3x covenant (both on a lease-adjusted basis). Yet, NTCO will need to contend with a tougher macro this year, along with one-off cash costs from the ongoing restructuring at Avon International (~$39m upfront for the discontinuation and ~$10m/year of incremental capex through 2025). Thus, how NTCO manages the cash burn will be key - in the first nine months of FY22, the company has already incurred a ~R$755m decline in its cash balance.

{kind=link}

Aesop Optionality is Key

Over the last month or so, several news reports have cited NTCO's plans for a stake sale or a full divestment of its high-growth Aesop business, a luxury cosmetic brand focused on skin and hair care. For context, NTCO fully acquired the company in 2016 after an initial ~65% stake purchase in 2013. Following the acquisition, management accelerated the expansion of the brand, driving a >30% net sales CAGR through 2021, along with strong profitability. Thus, unlocking value from Aesop makes sense - as a standalone, Aesop would likely command much higher valuation multiples vs. NTCO's current ~5x forward EV/EBITDA. It remains early days, but the company is clearly committed, having hired several banks to shop the asset.

Of note, the latest reports of a partial sale represent a departure from prior efforts to execute an IPO or spin-off. Given the unfavorable market conditions following the rate hikes over the last year, unlocking value via a minority stake sale may be the optimal course of action here. Not only does it allow for increased funding and continued business consolidation, but it also leaves the door open for an eventual IPO down the line. Per the news reports, preliminary valuations are within the $1bn-1.5bn range, implying ~9x EV/EBITDA at the midpoint. While this is below where most luxury cosmetics peers like Estee Lauder ( EL ) and L'Oreal trade, it is still above NTCO's ~7x forward EBITDA, so a transaction would likely be accretive. Perhaps more importantly, a sale would help de-risk the NTCO balance sheet, mitigating another follow-on raise in the coming quarters.

More Risk Than Reward

On the heels of a difficult 2022, Natura &Co has been hit with more bad news; this time concerning litigation in the US involving its Avon Products subsidiary, which will entail a sizeable outlay (relative to its cash position) for the fine. This wouldn't be a major issue if not for the burn rate at ~R$755m YTD and leverage (currently at ~3x net debt/EBITDA). With the weakening fundamentals also leading to management pulling back guidance, uncertainty is high, and more downward revisions to earnings could be on the horizon.

From here, execution will be key - NTCO needs to deliver on efficiencies from the ongoing restructuring and also raise capital from a minority stake sale of Aesop to stave off a dilution event. Yet, the stock likely isn't adequately discounting the risks at ~7x forward EV/EBITDA, and thus, I would remain sidelined ahead of the Q4 earnings report.

For further details see:

Natura &Co: More Risk Than Reward