LRLCY - Natura &Co: Transformation's Cloudy Horizon

2023-09-06 23:16:09 ET

Summary

- Natura &Co faced cultural integration challenges following its acquisitions over the last few years, impacting financial performance.

- Q2 results showed improved gross margins but higher transformation costs, while the sale of Aesop and a possible sale of The Body Shop aim to enhance the company's financial position.

- Long-term growth prospects remain uncertain due to Brazil's high interest rates and relatively high share multiples, warranting a neutral stance.

Natura &Co ( NTCO ) is a leading Brazilian company in the distribution of cosmetics for hygiene and beauty, operating globally with the Natura, Avon, and The Body Shop brands.

The company has pursued a strategy focused on integrating Natura and Avon in Latin America, leveraging the company's competitive advantages in the direct sales channel within this regional market. However, with the company's shares currently trading at 15 times its EBITDA, investors must understand that Natura&Co is not a bargain.

While there is potential for improved operational prospects for Natura&Co and the potential sale of The Body Shop brand following the sale of Aesop to L'Oréal in April this year, I still have difficulty seeing a clear path for long-term growth for the company. This is particularly challenging due to the adverse economic scenario in Brazil, characterized by high interest rates that should persist for a while.

Navigating Natura&Co's Growth and Challenges

A few years ago, in 2020, Natura&Co made a significant acquisition: Avon. Until around 2018, Natura&Co's financial results had been relatively stagnant, and its stock prices had remained relatively flat. Typically, stock performance closely mirrors a company's financial results over the long term. However, with the acquisition of Avon, Natura&Co experienced a surge in its stock price, rising by as much as 200% shortly after the deal. The market had high expectations due to this expanded operational diversification and the added value it brought to Natura&Co.

However, as time passed, the company faced challenges, particularly maintaining a consistent corporate culture. Besides Avon, Natura&Co acquired The Body Shop in 2017 and Aesop in 2012, an Australian company. This expanded its operational scope and introduced different cultural dynamics from various countries and continents. Natura's management found it challenging to navigate these cultural differences, which significantly impacted its financial results. Consequently, the company had to reassess its strategy for delivering value to its shareholders.

More recently, Natura&Co completed the sale of Aesop to L'Oréal ( OTCPK:LRLCF ) in April this year for $2.5 billion—a significant sum considering that Aesop contributed 15% of Natura&Co's total revenue. This influx of cash eased concerns regarding the company's high debt levels, affecting its profitability. Natura&Co has a net debt/EBITDA ratio of 4.17x, reflecting its high leverage.

Natura&Co's IR

With this cash injection and a renewed focus on Latin America, particularly its operations in Brazil, Natura&Co is poised to improve its financial performance. The potential sale of The Body Shop could indeed happen and might serve as a catalyst for the company to concentrate on its core business. Some estimates suggest a valuation of approximately R$3.5 billion (about $707.4 million) for The Body Shop, considering that Aesop was sold for $2.5 billion. Although The Body Shop contributes about 10% of Natura&Co's revenue, it has faced declining results recently. Thus, a potential sale could remove a stumbling block from the company's path and unlock positive results.

Recent Q2 Results

Natura&Co has indeed shown signs of improvement in its operational performance. The company reported robust results for the second quarter, with noteworthy expansion in the Natura&Co brand and gross margin, albeit accompanied by higher transformation costs.

Regarding Natura & Co's consolidated net sales in Brazilian Reais, excluding Aesop's figures, there was a 4% decline compared to the previous year (or 2% in constant currency).

Natura&Co's IR

This decrease can be attributed to the robust performance of Natura&Co LATAM, which saw a 15% increase compared to the previous year due to productivity enhancements. However, this growth was offset by several factors:

-

Avon LatAm encountered challenges in preparing for Wave 2 (the integration of the Avon brand scheduled for the next cycle) and struggled in an unfavorable macroeconomic environment, leading to a decline in performance.

- Optimization efforts in Avon's Home & Style category led to a decline of 37%.

- The Body Shop continued to grapple with challenges, experiencing a 12% drop in sales. This was partly due to elevated inventory levels and adjustments in the channel mix, with The Body Shop at Home also encountering difficulties.

A significant highlight was the consolidated gross margin, which increased by an impressive 4.3 percentage points compared to the previous year. Favorable price and product mix dynamics drove this improvement across all Business Units, notably LatAm. Conversely, the Adjusted EBITDA margin expanded by 2.3 percentage points. This was attributed to increased investments in marketing and research and development (R&D) at Natura&Co's LATAM and Avon International. However, it is essential to note that transformation costs amounting to R$240 million were 15% lower year-over-year.

Natura&Co's

The net loss amounted to R$732 million, primarily influenced by rising financial expenses owing to the persistently high leverage, which reached 7.2 times the net debt-to-adjusted EBITDA ratio. This situation is expected to be alleviated by funds from Aesop starting in the third quarter, although Aesop's results will continue to exert pressure on overall performance.

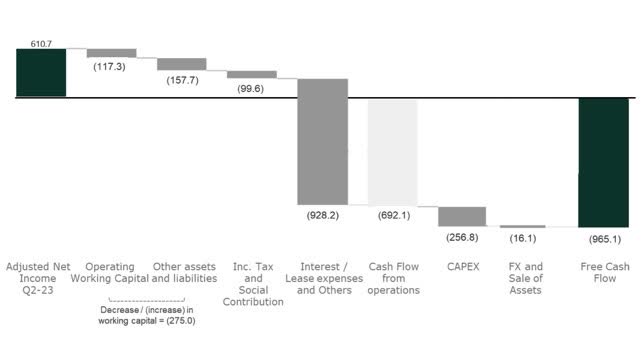

Additionally, cash flow was negatively impacted, with an outflow of R$965 million, compared to a negative figure of R$610 million in the same period the previous year. Nevertheless, there was an improvement in working capital dynamics across all segments, which is a positive development.

{kind=link}

Natura&Co's IR

Implementing Wave 2 in Peru and Colombia has facilitated cross-selling between Avon and Natura, enhancing productivity among Beauty and Wellness Consultants (CFT). However, a reduction in the representative base is expected due to the higher minimum order requirement.

Furthermore, inventory levels at The Body Shop franchisees improved during the second quarter, although they remain higher than in 2019 in some regions, particularly in the Asia-Pacific area. The company's management continues to optimize The Body Shop portfolio, focusing on accelerating the skincare category.

Natura&Co LATAM's gross margin (adjusted EBITDA margin), excluding Argentina, remains robust at 13%. Additionally, the company is actively managing its liabilities, including the repurchase of Avon 2043 bonds, as announced in July.

The Bottom Line

Despite improving its position through the sale of Aesop and the potential for a stronger balance sheet with the sale of The Body Shop, the long-term outlook still appears somewhat uncertain.

There isn't clear visibility regarding the company's growth in the coming years, especially considering the likelihood of high interest rates persisting in Brazil for an extended period. This could pose significant challenges to the company's ability to leverage its operations effectively.

Furthermore, Natura&Co's shares currently trade at relatively high multiples. Despite expectations for EBITDA to nearly double by the end of 2024, potentially reducing the EV/EBITDA ratio to 9.5x, it remains above both the historical industry average and the Brazilian stock exchange average (which stands at an EV/EBITDA of 7.9x).

Seeking Alpha

Moreover, the strong performance of Natura&Co's shares, appreciating by approximately 60% until September of this year, is likely already factored in due to the anticipated reduction in Brazil's basic interest rate. The Central Bank of Brazil's most recent report suggests that the rate is expected to close the year at 11.75%. The Brazilian Real ((BRL)) appreciation against the US Dollar ((USD)) has also contributed to this performance.

Given these factors, I don't currently view Natura&Co's value as a clear opportunity. While the company is demonstrating improved results and smoother operations, and the current price may be justifiable considering the associated risks and uncertainties of the business, I maintain a neutral stance in this case.

For further details see:

Natura &Co: Transformation's Cloudy Horizon