NGVC - Natural Grocers: A Simple Retail Model With Steady Returns And Clear Undervaluation

2023-05-09 11:07:47 ET

Summary

- Natural Grocers is worthy of more research, selling at a below normal valuation, in a nearly recession-proof industry.

- Operating margins have been steady for years and could improve as younger consumers are generally more health conscious.

- A solid 3.6% dividend yield, easily covered, and limited company liabilities argue in favor of a buy decision around $11 per share.

A company on sale today, after a steep share price decline from 2022, focused on retailing healthier natural and organic food items, vitamins, herbal supplements, alongside minimized-chemical shampoos and soaps is Natural Grocers by Vitamin Cottage ( NGVC ). Based in Colorado, the organization operated 164 stores in the U.S. West and Midwest during 2022.

From my perspective, the investment proposition has become quite appealing on the -60% price pullback from $23 a share in May 2022 to $8 earlier this year.

YCharts - Natural Grocers, Weekly Equity Price, 5 Years

When you consider the regular margins this growing health-food retailer generates each year, while reviewing an underlying valuation approaching its cheapest ever, why not dig deeper into upside investment potential?

The Business

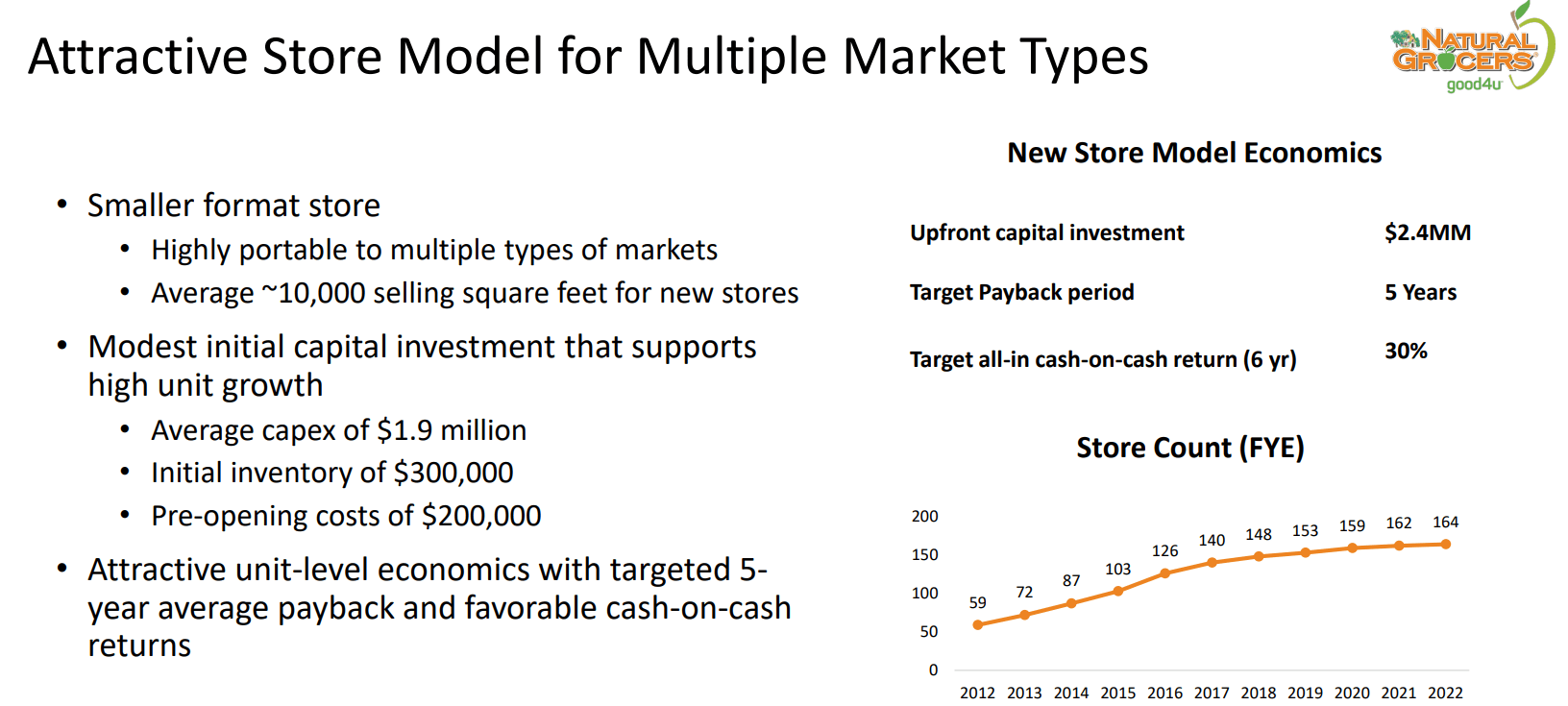

The best way to describe the store format is it is a cross between a Whole Foods Market grocery store and a GNC/Vitamin Shoppe , with square footage for size in between the two. The company is driven to be your local, ease of access point to shop for health foods and related products. And, with a smaller property footprint than a full-sized grocery store, each brick-and-mortar asset requires less capital to build, fewer employees to manage the flow of goods and sales, while holding modest inventories for quicker dollar turnaround (most inventory is on the shelf). From a financial perspective, the goal on each new location opened is a full return of invested capital after five years. Then, future operations should provide heightened/compounding profits on both rising general inflation and increasing appetites for organic/health items.

Natural Grocers - May 2023 Investor Presentation Natural Grocers - May 2023 Investor Presentation Natural Grocers - May 2023 Investor Presentation Natural Grocers - May 2023 Investor Presentation

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Margins and Financial Position

Over the last decade, the company has maintained a rough 28% gross margin on sales, and a final profit margin between 1% and 2%.

YCharts - Natural Grocers, Profit Margins, Since 2012

Gross and final net margins actually stack up quite well with other peer and competing grocers like Kroger ( KR ), Albertsons ( ACI ), Sprouts Farmers Market ( SFM ), Grocery Outlet Holding ( GO ), and SpartanNash ( SPTN ). And, I cannot come up with sound logic why future margins will change materially in a negative fashion.

YCharts - Natural Grocers vs. Peers, Gross Margins, 5 Years YCharts - Natural Grocers vs. Peers, Net Income Margins, 5 Years

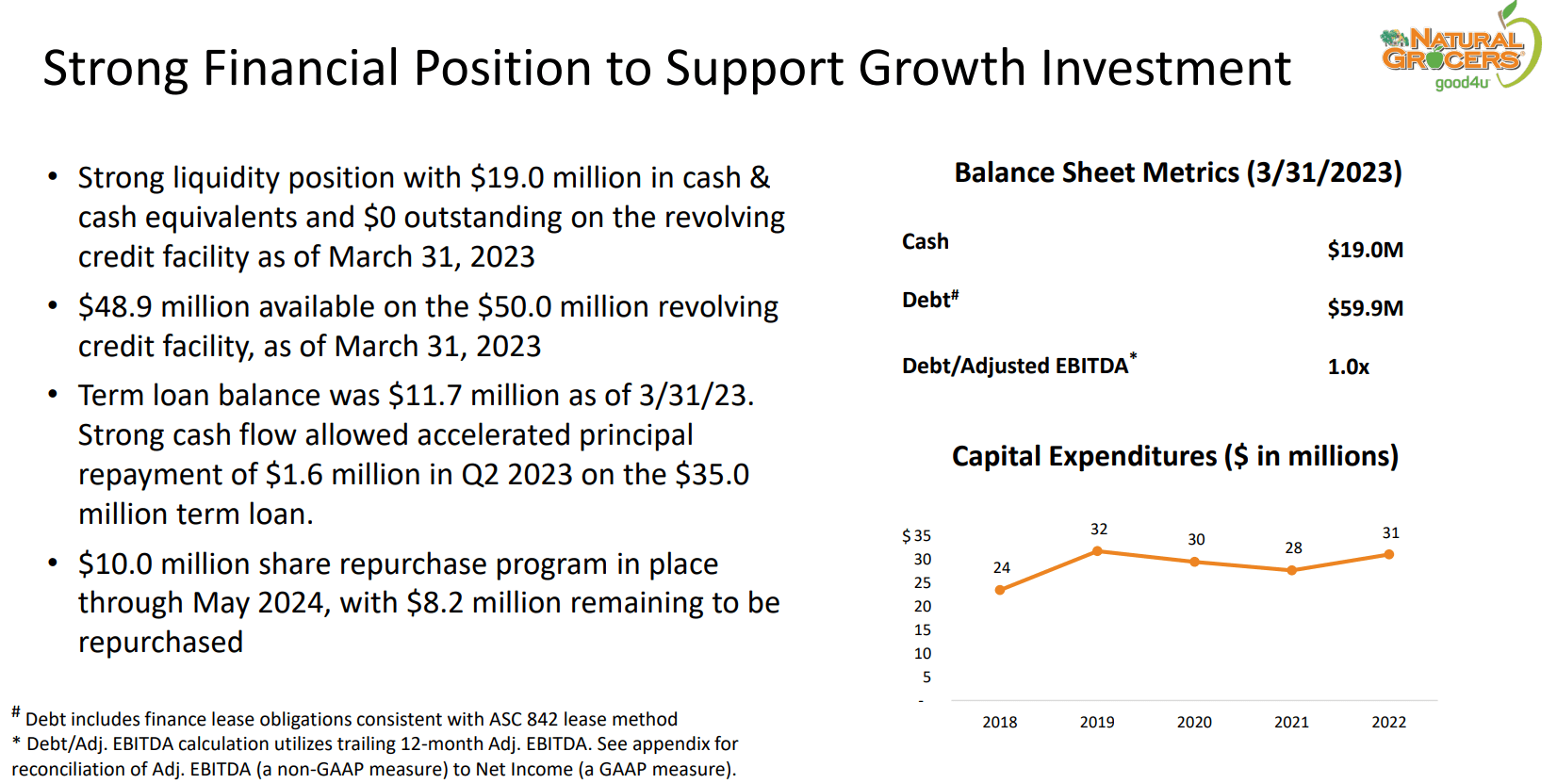

The company runs a smart, low-leverage balance sheet, which has helped keep margins steady and operations running smoothly during economic booms and busts since 1955.

Measured against a total equity market capitalization of $260 million presently, $19 million in cash and $60 million in total debt were held on March 31st, 2023.

Natural Grocers - May 2023 Investor Presentation

{kind=link}

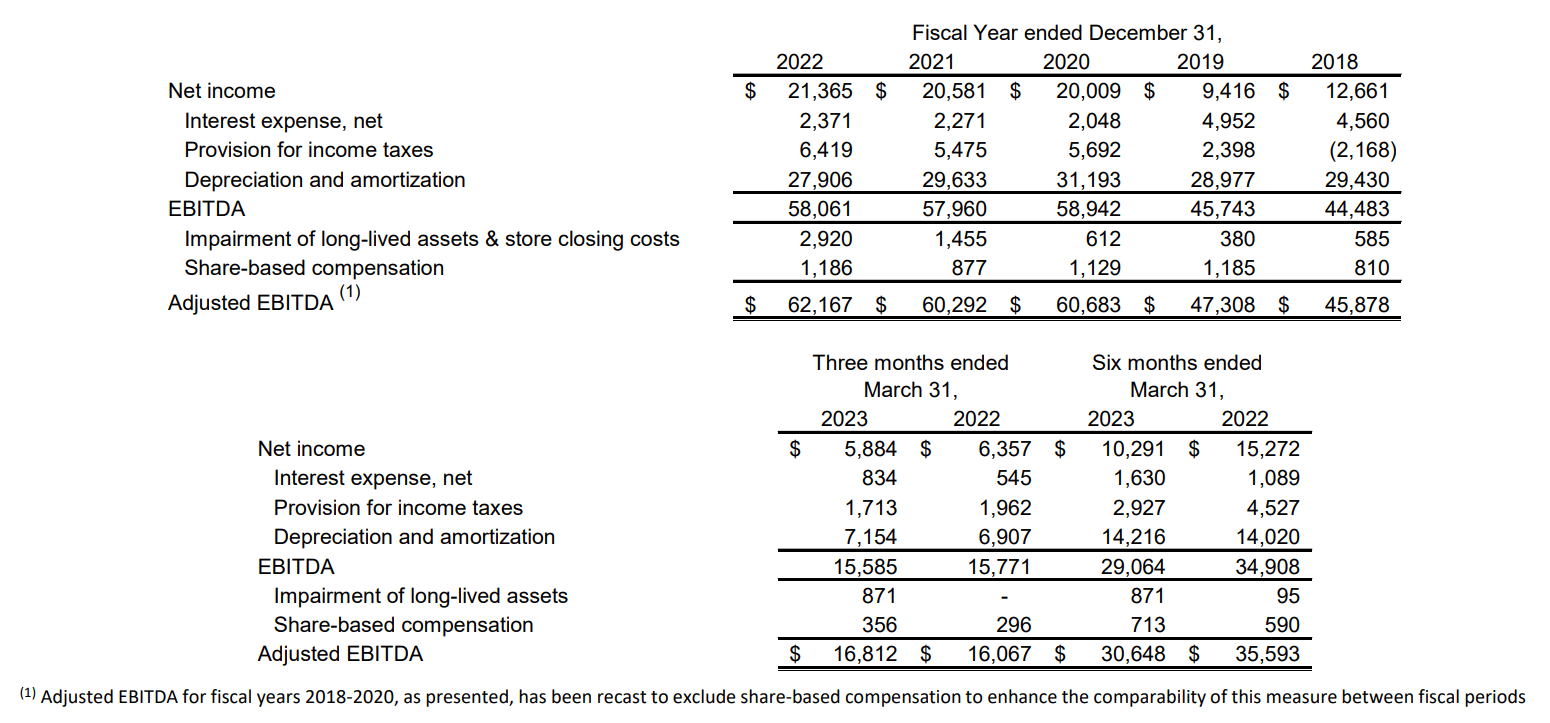

In addition, you can review below the steady income and EBITDA generation each year over the last five, including swings caused by COVID.

Natural Grocers - May 2023 Investor Presentation

{kind=link}

Valuation Story

The good news for investors is the share valuation since late 2022 has been approaching its lowest point since public trading began in 2012. A decade graph of price to trailing earnings, sales, cash flow, and tangible book value is drawn below. Overall, I can argue a combination of these valuation stats produces a 10-year "average" price target of $18 today, before shares move into overvalued territory (and this assumes flat operating results into 2024).

YCharts - Natural Grocers, Price to Trailing Fundamentals, 10 Years

When we account for debt and cash on the balance sheet, the enterprise valuation becomes even cheaper. Using this set of numbers and ratios, a "fair value" target of $20 to $22 seems appropriate. Of course, when shares first started trading, Natural Grocers was growing faster and retained something of a growth-valuation on Wall Street.

YCharts - Natural Grocers, Enterprise Value to EBITDA & Sales, 10 Years

On EV to EBITDA and revenues, Natural Grocers stands out as "the" value pick in the sector.

YCharts - Natural Grocers vs. Peers, Enterprise Valuation on Trailing EBITDA, 5 Years YCharts - Natural Grocers vs. Peers, Enterprise Valuation on Trailing Sales, 5 Years

Dividend Yield

Another super-bullish data point is Natural Grocers' dividend has risen from a below average payout and yield in 2019 vs. peers and the U.S. equity market (represented by the S&P 500), to one of the highest in the food retailing field.

YCharts - Natural Grocers vs. Peers, Trailing Dividend Yield, 3 Years

Plus, the current $0.81 EPS estimate by Wall Street for 2023 is double the $0.40 dividend payout. That works out to a relatively normal earnings coverage ratio of 2x (running 1.8x on a trailing basis) vs. the S&P 500, and only trails Kroger's setup from my industry peer list.

YCharts - Natural Grocers vs. Peers, Dividend Cover from Earnings, 3 Years

Final Thoughts

Insiders and management control about 40% of shares outstanding, with no reported sales over the past 3 months (and just 8,000 sold over the last 12 months). The founding Isely family owns much of the insider stake. So, small retail investors and management both want a higher stock quote over time. A major ownership incentive should continue to guide intelligent long-term decision making at the firm. Operating out of 21 states today, there's plenty of room to grow into the other 29, plus Canada possibly in future years.

From a technical trading perspective, you will notice on the 5-year total return chart below, a great time to buy Natural Grocers is when investment returns swing into a negative position vs. the S&P 500. The stock quote bottomed in December-January well below the S&P 500 zigzag, which has again proved a smart entry (at least so far). It is entirely possible NGVC is due for another 50% to 75% outperformance pop like 2018, 2021, and 2022. Such would push price closer to its long-term fair value.

YCharts - Natural Grocers vs. S&P 500, Total Returns, 5 Years

What are the downside risks? My thinking is the biggest investment risks are macroeconomic in nature. If we get a deep recession that affects consumer spending on food, or a stock market crash from today's still richly-valued point in time on Wall Street overall (according to total equity market cap to GDP output or the Shiller P/E), investment losses on paper are definitely possible. However, I suspect any Natural Grocer decline in price would outline nearly the same or an improved percentage rate vs. S&P 500 losses. I rate shares a Buy around $11, with a $15 to $20 price target in 12-18 months.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

Natural Grocers: A Simple Retail Model With Steady Returns And Clear Undervaluation