NGVC - Natural Grocers: Pressure On Revenue And Margin Growth Continues

Summary

- High inflation continues to affect consumer preferences and traffic dynamics in Natural Grocers' stores.

- Rising freight and wage costs, as well as declining economies of scale, are putting pressure on margins.

- The lack of catalysts for growth and high risks do not allow publishing a recommendation other than “Sell”, despite the small fundamental potential.

Introduction

Shares of Natural Grocers ( NGVC ) have risen 14% YTD. Despite the fact that the company operates in the consumer staples sector and has the ability to pass on higher inflation to the end consumer, continued pressure on store traffic continues to weigh on business growth and operating margins. In my assessment, NGVC is trading slightly below fair levels, however, in my personal opinion, the current fundamental upside does not reflect the risks that come with investing in the company's shares.

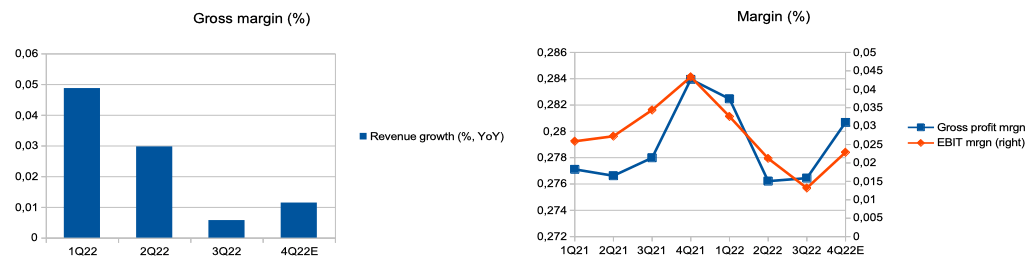

Short survey of Q1 23 (fiscal) report

The company's revenue reached $280.5 million, demonstrating an increase of 1.1% YoY. Comparable sales grew by 0.5% due to the growth of the average check by 1.5% , but the number of checks decreased by 1.2%. The main driver of average ticket growth is still high inflation, which the company can pass on to the end consumer, but the business is facing pressure from traffic in stores.

Thus, in view of high inflation and rising prices in stores, some consumers may change their own consumer preferences, as a result, the company faces the consumer squeeze effect. Gross margin improved slightly compared to previous quarters and reached 28%, however, it is still at a level lower than in 2021. Thus, the operating margin was 2.3%, which is better than in the previous 2 quarters, however, the results are still weaker than during 2021. You can see the details of the results in the charts below.

{kind=link}

Projections

I decided to build a model of the company's financial results in order to evaluate the business and make my own assumptions about future financial results. Below, you can see my main assumptions on the basis of which I built a business valuation model:

Revenue growth: I assume that inflation growth in 2023 will continue to have a negative impact on the traffic dynamics in the company's stores, so I predict revenue growth at 0% by the end of 2023, then I conservatively assume revenue growth at 1.5% to 2026.

Gross margin: I conservatively assume in my model that the gross margin will be around 27.5% until 2026. In my opinion, gross margin, like traffic dynamics, is one of the most important stock drivers and one of the most sensitive indicators.

Store expenses: I forecast store expenses at 22.5% in line with historical trends and the company's plans to open new stores.

Administrative expenses: I predict administrative expenses at 3% of revenue.

You can see my projections of the company's future cash flows in the chart below.

Yearly projections

Forecasting (Personal calculations)

Valuation

To value a company, I prefer to use the DCF method. In my personal opinion, building a DCF model is the preferred way to value a consumer staples company. I prefer DCF because:

1. The company operates in a stable market where building a DCF is the most preferred

2. We have a long period of historical observations, based on which we can make assumptions about future results

3. Building a DCF model allows you to take into account changes in the growth rate of revenue and the level of operating expenses in future periods

The main inputs in my model are:

WACC: 5%

Terminal growth rate: 3%

DCF model (Personal calculations)

Multiples

In addition, I calculated P/E and P/S multiples for the company based on my sales and net income forecasts. You can see the results of my calculations in the chart below.

Multiples (Personal calculations)

Risks

Macro: high inflation and a decline in real consumer incomes may have a negative impact on consumer spending, which is a negative factor for the company's revenue in the next periods.

Consumer squeeze: higher prices for key products could lead to a change in consumer food preferences, which could have a negative impact on the business's revenue growth in the future.

Competition: increased competition may lead to a decrease in market share and lower operating margins due to increased operating costs. According to management comments , a potential merger between The Kroger Company and Albertsons Companies could adversely affect the company's future competitiveness.

Margin: a decrease in the average check, a decrease in traffic, an increase in freight and distribution costs, as well as a decrease in economies of scale can lead to pressure on the level of operating profitability of the business in the future.

Drivers

Revenue growth: new store openings, the ability to pass on higher inflation to the end consumer, average check growth, store traffic growth may have a positive impact on revenue growth in the future.

Margin: increasing the share of private brands, growing economies of scale, and effective control of operating costs could support operating margins in the coming periods.

Macro: decrease in inflation, recovery in consumer confidence, and growth in consumer income may also have a positive impact on business growth rates.

Conclusion

According to my DCF model, the fair share price is $11 with an upside potential of 7%. In my personal opinion, the current level of fundamental upside potential of the shares does not fully reflect the risks that investors in the company's shares may face in the coming quarters. In addition, in my personal opinion, we will see continued pressure from inflation in the first half of 2023, so I do not see positive catalysts for stock growth during the first half of 2023. I am happy to amend my model and change my view when I see a change in macroeconomic conditions and when the company is able to demonstrate improvements in operating and financial performance.

For further details see:

Natural Grocers: Pressure On Revenue And Margin Growth Continues