SIRE - Natural Resource Partners Appears Inexpensive With Multiple Ways To Win

Summary

- Natural Resource Partners (NRP) is multi-faceted with coal mineral rights, soda ash and CO2 sequestration exposure.

- If you believe in carbon sequestration, the units may be very cheap, if not, you may still see a return from rapid deleveraging.

- Management holds a material position, the CEO holds almost a 20% stake.

- The business is conservatively worth $66/unit today and that could increase with ongoing deleveraging to $93/unit on a 2-year view (assuming coal pricing remains strong).

It's easy to see why Natural Resources Partners ( NRP ) would be overlooked by the market, it's a K-1 filer, part of its earnings relate to coal and the stock has already had a good run along with many commodity-related plays.

However, NRP does appear attractively valued, the portion of the soda ash business that they don't own may be about to receive a transaction value that suggests undervaluation at NRP, and there's a material ESG play here via CO2 sequestration . Also, there's incentive alignment, management has been diligent in paying down debt and insiders own 25% of the units (CEO owns almost 20%). Finally, mineral rights plays are great businesses, they take a payment off the top from coal shipments from their land. This means they have virtually no costs and falling coal prices are less of a hit to profits when compared to running an operating business.

Valuation

I'll jump to the valuation because that's what gives me confidence in the units at these levels.

| Asset/Liability |

| Value () |

| Notes |

| Soda Ash Business (49% Stake) |

| 447 |

| $639M recent implied value (for 49% stake) based on a past transaction less 30% minority discount. This works out to approximately 11x current distribution cash flow that NRP receives. You can also triangulate this from the market cap of Sisecam Resources ( SIRE ), which owns the remaining 51% of the business for a current market cap of $474M at the time of writing, though the ownership structure at SIRE is more complex and buyout may be pending. |

| Coal Mineral Rights |

| 750 |

| Current run rate is around 300M/year operating profit, I normalize to 150M and assume 5x multiple. There is a relatively broad spread of outcomes here depending on your views on coal for the next few years. This valuation may be somewhat conservative. |

| CO2 sequestration capacity |

| 172 |

| Emerging business, 2 contracts in place currently, NRP may be able to own a material royalty on carbon storage (sequestration) on its acreage. As of Q3 2022 "carbon neutral initiative revenues" were $8.6M. These projects appear to utilize roughly 5% of available acreage and so full utilization may be roughly $172M, though the contract structure and payment are unclear. |

| Capitalization of corporate costs |

| 200 |

| Assume 20M annual costs at 10x |

| Estimated debt as of December 2022 |

| 100 |

| 149M as of September, assume further 50M of debt paydown to December 2022 |

| Preferred Stock |

| 250 |

| Book value |

| Resulting equity valuation |

| 819 |

| Per unit valuation |

| $66/unit |

| 12.5M units outstanding as of Sept 30, 2022 |

Sensitivities

I believe the soda ash valuation is relatively robust, and I suspect NRP could even sell it's stake to Sisecam (the Turkish firm that controls the remaining 51% of the soda ash asset) at around that valuation if it wished to. That said, I don't think management wants to sell this attractive business.

No Future For Sequestration

However, the valuation for coal royalties and CO2 sequestration are more debatable. If you believe the CO2 sequestration business is worthless, then the valuation falls to $52/unit , which is around the current price. However, if you think this, you also have to explain why they have taken in millions on current contracts.

Full Deleveraging

In terms of debt, the company is producing significant free-cash-flow currently, if that's sufficient to pay down all remaining debt and take out the preferreds over the next 18 months or so, then the 'debt-free' valuation rises to $93/unit .

Bullish On Coal

Regarding coal if you assume current earnings persist for the next five years, or are willing to consider a 10x multiple, then the valuation rises to $125/unit .

So in summary, you have to have some belief that carbon sequestration will become a meaningful business over time or believe coal prices will remain elevated for a few more years to see major upside from here. However, conversely there doesn't seem to be obvious downside unless both coal and soda ash see sharp profitability declines, as at steady state the cash generation of this business is significant compared to the value of the units.

Soda Ash Is a Great Business

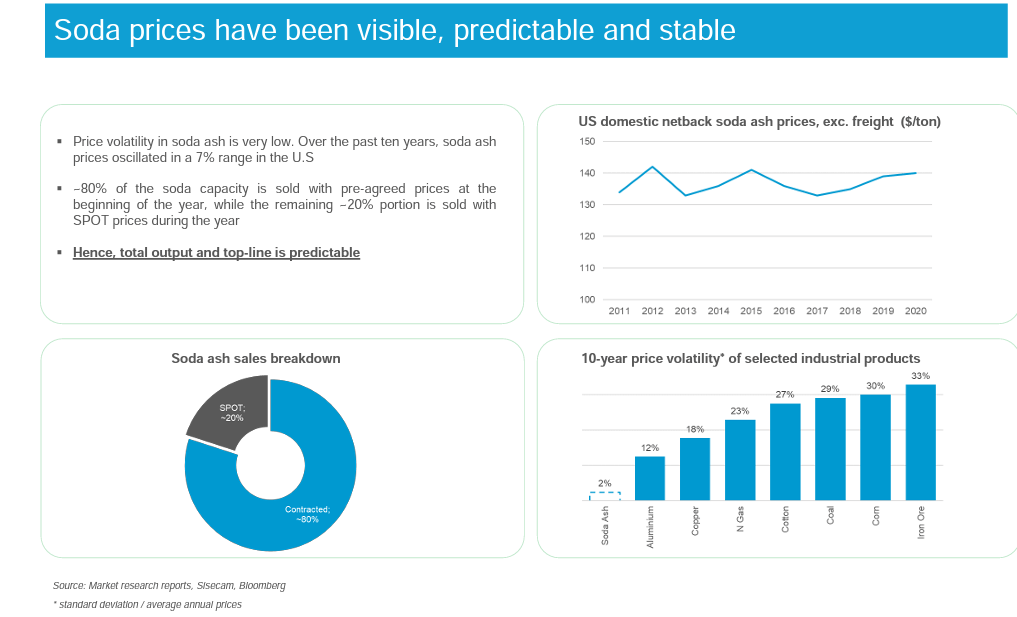

Soda Ash is a great, stable business. Soda ash is used primarily to make glass but has many other uses from batteries to cleaning products. The Wyoming asset is a low-cost, natural producer. Price volatility is low, and the Wyoming site may expand production 40% over the coming years. Currently NRP receives $10M in quarterly distributions, but this may increase.

{kind=link}

Sisecam Investor Presentation

Not Coal, But Mineral Rights

Yes, the company derives significant earnings from royalties from coal mining on its land today. Though even here we should note that around half of this business is metallurgical coal (an ingredient for steel production, not a fuel as such).

However, the future may look quite different, the same land can be used for CO2 sequestration projects, and this is starting to happen, though the company hasn't split out the earnings yet in full detail. Other uses for the land such as geothermal energy projects and earning credits for carbon sequestration through forestry, are possible too. This is what NRP said regarding carbon sequestration in their most recent 10-Q (for September 2022).

We continue to identify alternative revenue sources across our large portfolio of land and mineral assets. We own the rights to sequester carbon dioxide ("CO2") on approximately 3.5 million acres of pore space in the southern United States. As announced previously, in the first quarter of 2022 we executed our first subsurface CO2 sequestration lease on 75,000 acres of underground pore space we own in southwest Alabama with the potential to store over 300 million metric tons of CO2. In October of 2022, we announced our second subsurface CO2 transaction with the execution of a lease for approximately 65,000 acres of pore space we control near southeast Texas with estimated storage capacity of at least 500 million metric tons of CO2. In total, we have approximately 140,000 acres of pore space under lease for carbon sequestration with estimated CO2 storage capacity of 800 million metric tons. While the timing and likelihood of additional cash flows being realized from these activities is uncertain, we believe our large ownership footprint throughout the United States will provide additional opportunities to create value in this regard and position us as a key beneficiary of the transitional energy economy with minimal capital investment.

And then on the subsequent earnings call , the company suggested $2/ton as a potential price for sequestration projects:

So with subsurface CO2 sequestration, the parties that would pay us for the use of our pore space will have significant capital expenditures they will have to make. But I think – so it's going to be something much less than the market value of the credits that we would receive. But I would suspect that if you used a couple of dollars a ton, that's probably a good guesstimate at this time, simply because the industry is so new, and that's a relatively [indiscernible] number.

It's obviously early days with carbon sequestration, but given NRP owns a lot of storage space here with effectively no associated costs (for NRP), the economics could become very attractive and early contracts are not trivial.

Ways To Win

There are a few positive catalysts here, they include:

- Continuing CO2 sequestration projects enable the market to value that business as material

- Continued paydown of debt and preferreds make the business debt-free on an 18-month view

- Coal pricing normalizes slower than anticipated leading to further periods of super normal earnings

- The soda ash business is acquired for a premium by the majority owner and/or the capacity expansion project boosts earnings materially over time

- Releveraging - the company has relatively low leverage currently (both in absolute terms and compared to history), if management can deploy cash effectively for productive assets, then releveraging the business could grow earnings power for unitholders substantially.

Risks

Still there are risks too:

- CO2 sequestration may not progress as expected and roadblocks to broad adoption may occur

- They are a minority owner of the Wyoming soda ash asset and may see distributions cut, or the business run in a way that is less favorable to them

- Coal prices and/or volumes may collapse

- Capital allocation may become a risk as the company is de-levered (though management has performed commendably so far)

- MLPs aren't always run in a way that favors common unitholders, who typically have limited rights

Other Valuation Metrics

It is also important to note that NRP also pays a $3/unit distribution currently for a 5.5% yield and that may increase in the future. Also, the business may be trading around 3x FCF, though the coal segment is likely over-earning in the current pricing environment. Still there likely is room for the distribution to increase as debt is paid down and preferreds are likely removed from the capital structure. Management has stated this is their current intent.

Conclusion

After valuing the coal and soda ash businesses somewhat conservatively, it appears you are getting a free call option on other uses for the land that NRP has the rights to. CO2 sequestration may be primary use here, but the company is also exploring geothermal projects and other activities. The strong cashflow profile and distribution means you may see a meaningful return just from the current earnings power of this business (more if strength in coal persists), and unusually for an MLP, management appears aligned with unitholders.

For further details see:

Natural Resource Partners Appears Inexpensive With Multiple Ways To Win