NRP - Natural Resource Partners: Differentiated Resource Play With Economic Leverage On Capital

2023-10-18 18:00:00 ET

Summary

- Natural Resource Partners has improved its capital structure and enjoys cost differentiation benefits, driving economic returns.

- Broad market coal pricing continues at elevated rates compared to pre-pandemic range.

- Technical indicators corroborate further upside potential for NRP's stock price, with fundamental backing to a target of $111-$119 per share.

Investment Briefing

Broad commodities remain within a long-term super cycle leading to robust equity gains for selective players positioned along the value chain. However, investing in this space comes with its challenges, all the way from "mine to metal", as the saying goes. For instance, amongst miners + producers, there is no differentiation on product. Those selling coal are all selling coal, and the market dictates pricing, even with offtake and purchase agreements in place. It therefore usually comes down to production advantages; who is the low-cost producer, who enjoys the most capital efficiency, lowest capital intensity and so forth. Therefore, any company that shows marginal improvements vs. peers should be heavily considered.

Asset replacement costs are also typically high, meaning maintenance CapEx and reinvestment requirements could hinder the cash key players can throw off to their owners by way of owner earnings and distributions.

On close examination, Natural Resource Partners L.P. ( NRP ) looks to possess differentiated economic characteristics that suggest it is a buy amid this latest commodity and global CapEx cycle.

The standout features are:

- NRP has focused heavily on cleaning up its capital structure, paying down debt principle and retiring preferred equity,

- The company appears to enjoy cost differentiation benefits, with high post-tax margins driving exceptional business returns,

- It is growing economic returns with less capital employed into the business to run its operations,

- Related to (4), around 50–60% of sales convert as economic earnings to shareholders (above a 12% hurdle rate),

- The stock trades at 5.9x trailing earnings, offering ~4% distribution yield and 33% trailing cash flow yield.

As a reminder, NRP owns a diversified set of mineral assets in the U.S., boasting interest in coal assets, along with its 49% interest in Sisecam Wyoming, a trona ore mining and soda ash production company. It has ~13mm acres of coal rights, where its coal is used in steel production and energy. Meanwhile, its soda ash production is used in the glass production and chemical industries.

Net-net, I rate NRP a buy based on the factors discussed in this report, eyeing $111–$119 per share in equity value downstream.

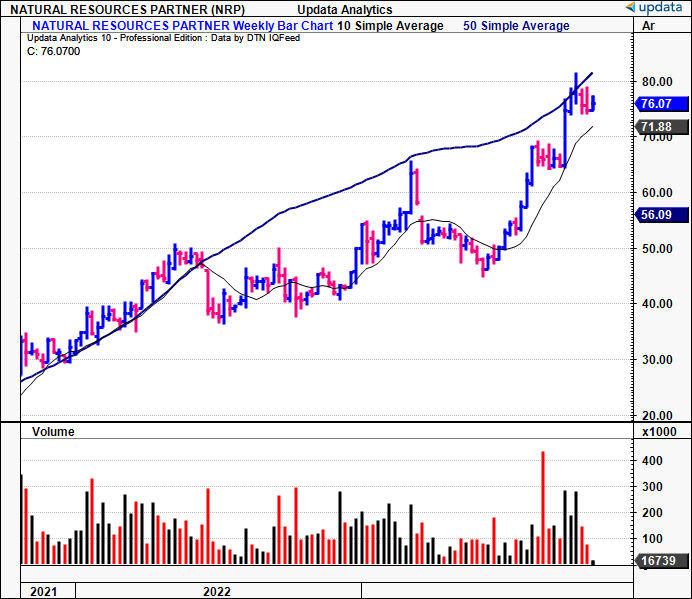

Figure 1. NRP 2-year weekly price evolution, strong bids in 2023

{kind=link}

Critical facts pattern supporting structural buy thesis

1. Market backdrop

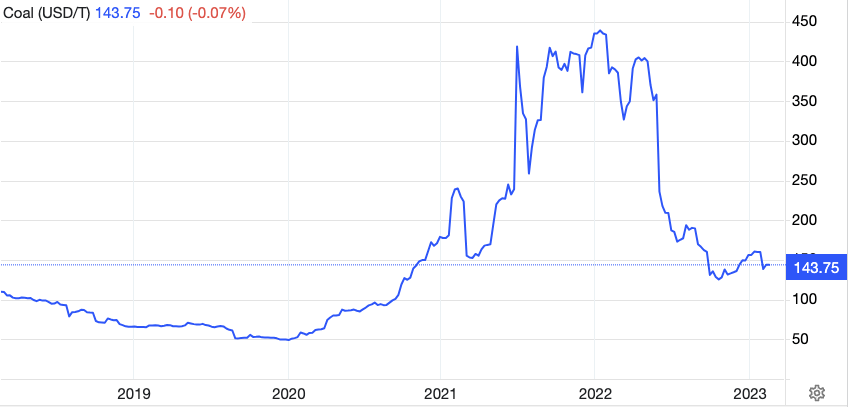

NRP's competitive positioning is sensitive to the underlying mechanics in the coal market in my estimation. Spot coal prices have cooled off their 2022 highs and now trade at $143/tonne at the time of writing (Figure 2). Notably, this is still above pre-pandemic range, with 2019 prices commanding anywhere from $50—$100/tonne.

Figure 2.

{kind=link}

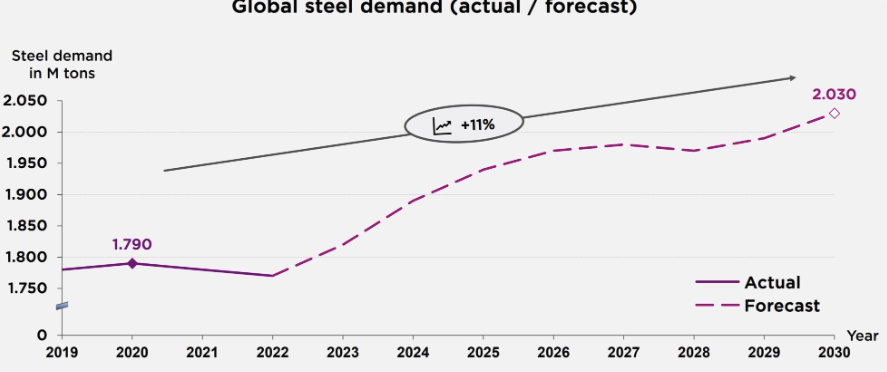

Coal's primary end use is in the production of steel. According to the World Coal Association, around 70% of global steel production relies on metallurgical/coking coal. Insights from Bronk & Company project that global steel demand will rise from 1.8Bn tonnes to 2Bn tonnes from 2020—2030, driven by an increase in industrialization from emerging markets.

Figure 2a.

{kind=link}

Goldman Sachs research also expects coal to "stay relevant", particularly with demand pull coming out of India with its transition to renewable energy. "India may need to add c.23GW more coal capacity than what the government targets" , it says, up to 50% more in the investment bank's modelling.

In terms of broad commodity demand, UBS investment research expects broad commodity indices to rise another 5–10% by yearend, with "robust demand for crude oil, expectations for stronger policy actions by China, and supply discipline".

It's preferred sector is energy, and there are tailwinds pointing to another uptick in coal, as it says "...higher Commodity markets prices may prompt some switching from natural gas to coal at utilities this autumn".

It projects coal at $125/mt by yearend, with a potential consolidation to $120/mt across 2024, as seen below.

Figure 2c. UBS Energy commodity forecasts, August 2023

Source: UBS Investment Research

2. Recent numbers + improving capital structure

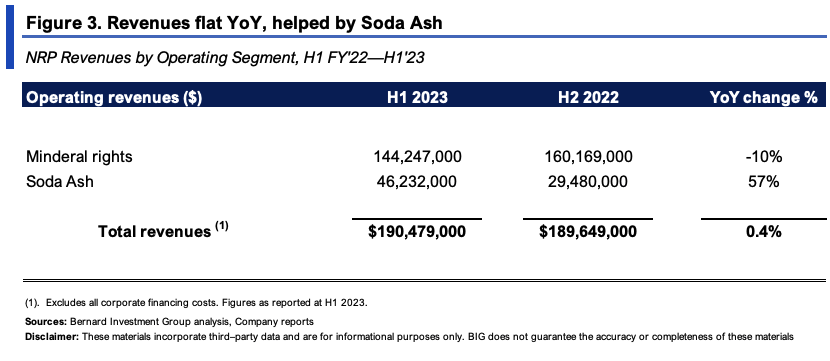

NRP put up Q2 top-line revenues of $91.3mm, down ~9% YoY given the decrease in metallurgical coal prices. For the first half, revenues were $190.5mm, and it produced $154mm in FCF and reduced its leverage ratio to 0.6x.

Looking at the divisional breakdown:

- Mineral rights:

- First-half revenues were down ~10% to $144.3mm.

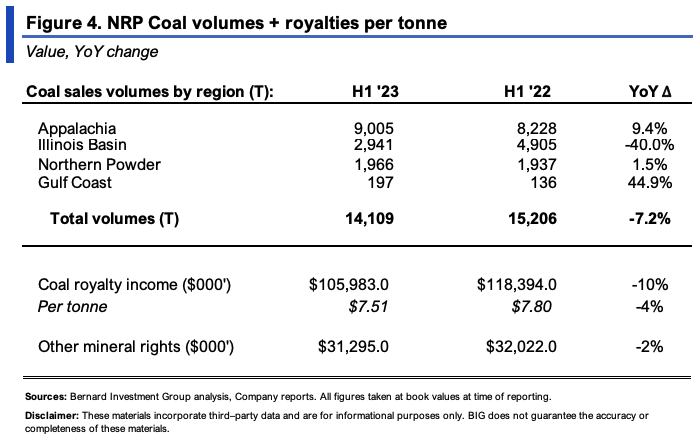

- This was underscored by lower sales volumes, down 7.2% YoY on aggregate to 14,109 tonnes. However, Gulf Coast volumes were up ~45% YoY, along with a 9.5% growth in sales volumes in the Appalachia region (Figure 4).

- Royalty income also decreased 10% YoY to $105.9mm or $7.51/tonne.

- For Q2 the division produced $56mm in FCF. Management is constructive on supply/demand ("S&D") for metallurgical coal in the market "due to long-term demand trends and the lack of investment in new met supply".

- Soda Ash:

- It booked H1 '23 revenues of $46.2mm, up 57% YoY as demand in domestic and international markets ratchets higher.

- Soda Ash prices have cooled off throughout FY'23 off their 2022 highs, as new supply from China enters the market, and an overall pullback in demand.

- Moving forward, management projects that pricing at its Sisecam Wyoming asset to remain strong, "as a result of negotiated 2023 domestic sales contracts entered into at the end of 2022".

- It produced $19.3mm in FCF in H1 in its soda ash segment from higher distributions from this asset.

{kind=link}

{kind=link}

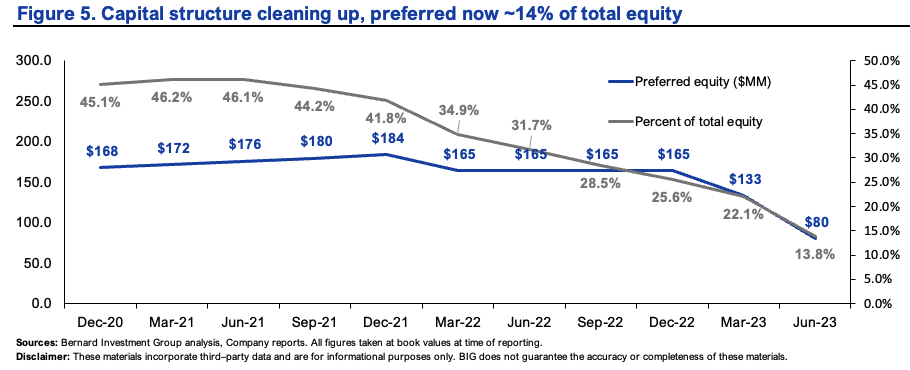

Another takeout is NRP's balance sheet management, as mentioned earlier, in particular, its retirement of a large portion of preferred equity tied up in its net asset value.

In 2020, preferreds comprised 45% of total equity value, with $168mm in obligations, rising to $184mm by December 2021.

In the last 12 months, it has reduced this figure to $80mm, otherwise 13.8% of total equity.

The benefits of this are:

(i). Commons have a greater residual claim over the balance sheet,

(ii). A higher portion of the company's cash flows can be siloed as distributions to common equity holders.

{kind=link}

3. Economic drivers of value

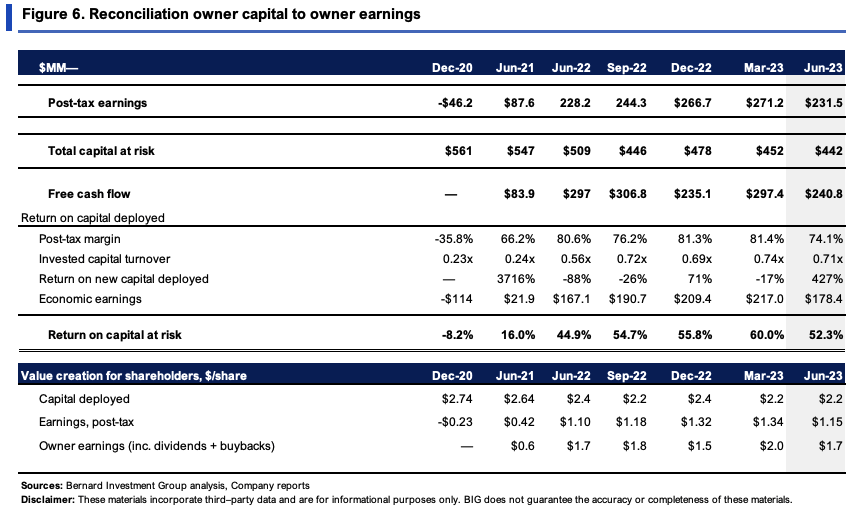

NPR has reduced capital investments deployed into the business from $2.74/share to $2.20/share from 2020—'23. Critically, the earnings produced on this capital have increased from $0.42/share in 2021 to $1.15/share last period (TTM values). This produces a return on existing capital of 50–60% in the last 12 months on a rolling TTM basis.

So it is increasing earnings with lower required capital to operate.

The key value drivers of this are:

- Post-tax margins of 70—80%, on capital turnover of ~0.7x,

- It has only put ~60% of the capital provided by investors to work, the remaining recycled as distributions to its owners.

Point (1) is the most critical to the debate. Typically, those along the energy chain (producers in particular) cannot differentiate on product or price, as discussed earlier. It usually comes down to production/operating advantages.

But given NRP's exceptionally high margins, it appears the firm enjoys cost differentiation ad consumer advantages, likely driven by its mix of coal, soda ash, and its royalty revenues. These are exceptional economics that insulate the company against peers in my opinion.

{kind=link}

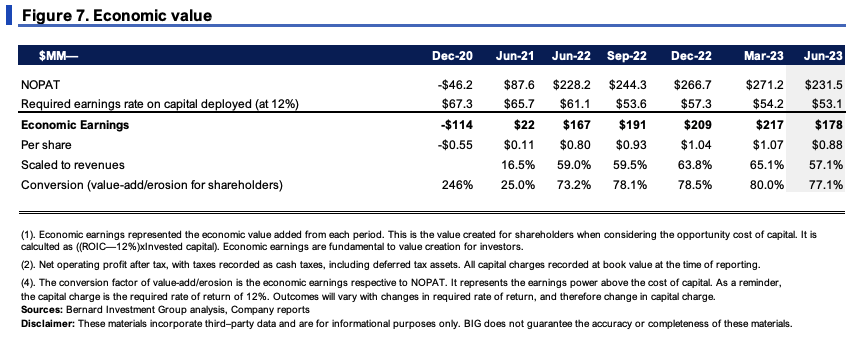

Capital productivity is therefore a standout. Our 12% threshold return is easily met in this instance, with the company producing $0.88 in economically valuable earnings to us last period, in range with prior periods (12% is the long-term market return and hence the opportunity cost).

One should be immediately suspicious when economic returns on deployed capital reach >50%. To observe their validity, they should be scaled to revenues:

- Here it's noted that NRP has returned ~60–65% of sales as economic earnings to shareholders since 2022 (at a 12% hurdle rate),

- This indicates more than half the company's top line is economically valuable to NRP's owners, notwithstanding any distributions paid directly as cash/dividends.

- Since 2020, it has produced >$920mm in economic earnings for shareholders, supporting its atmospheric rise off $12/share in early 2020.

{kind=link}

4. Technicals supportive of further rating

Objective technical measures corroborate NRP's advancement to higher market values.

One, the market profile of NRP's price-time distribution from Q1—Q3 shows potential for a vacuum towards the $81+ mark. Markets tend to rotate from areas of high usage to low usage to fill a longer-term distribution. In that vein, you can see in Figure 8 traders have continued to fill the distribution around the $73–$76 region, leaving a pocked of low usage superior to the collection of price opportunities.

Figure 9 displays this in a more convenient fashion. You can see where trading needs to occur in order to complete the full distribution from Q1–Q3. This is clearly a negatively skewed market, supporting the notion for small incremental price gains to the upside.

Figure 8.

Data: Updata

Figure 9.

Data: Updata

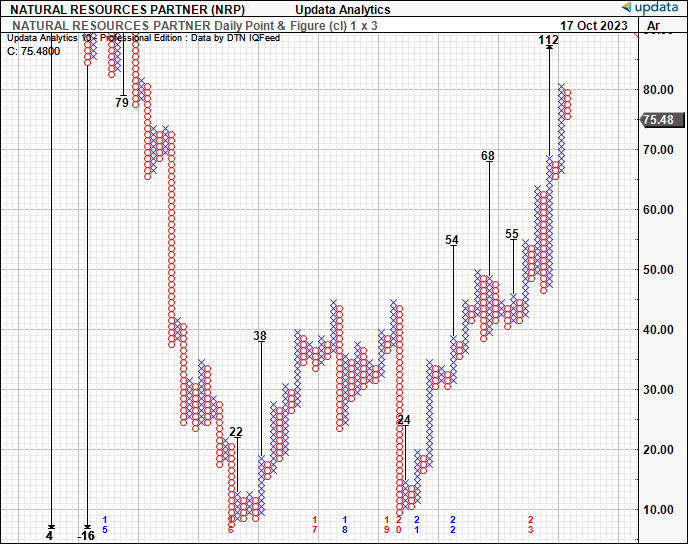

Two, we have upside targets to $112/share on our point and figure studies, which have captured each of the upside moves well to date (Figure 10). NRP is now approaching a set of resistance lines (not shown) and we'd be looking to this region should it nudge through this area. With the buying thrust that's been shown to date, the $112 is a convincing target, and one that can't be ignored.

Figure 10.

{kind=link}

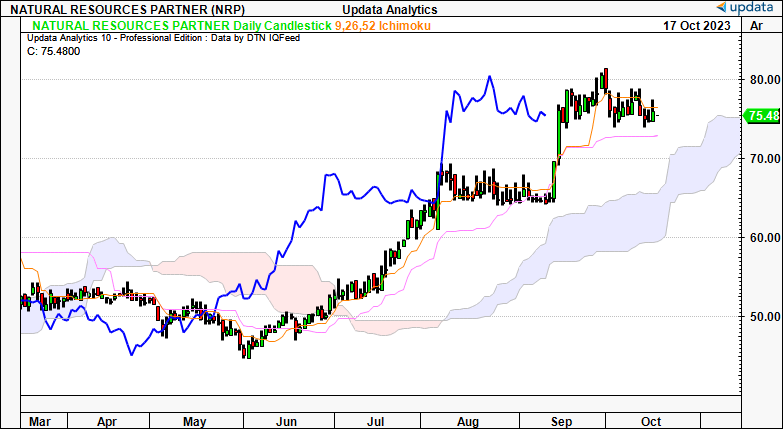

As to trend action, both cloud charts in Figures 11 and 12 do the talking:

Figure 11— Daily cloud chart, looking to the coming weeks

- Both price and lagging lines are well above the cloud and this supports a bullish view.

- Prices have been backing and filling into congestion from September–date, with a series of tight closes.

- If you look back to Figure 1 at the start of this report, you will see the ascending weekly volume (inc. buying volume) that has led us into this base. Secondly, each prior base (of varying time) has preceded another spike to the upside.

{kind=link}

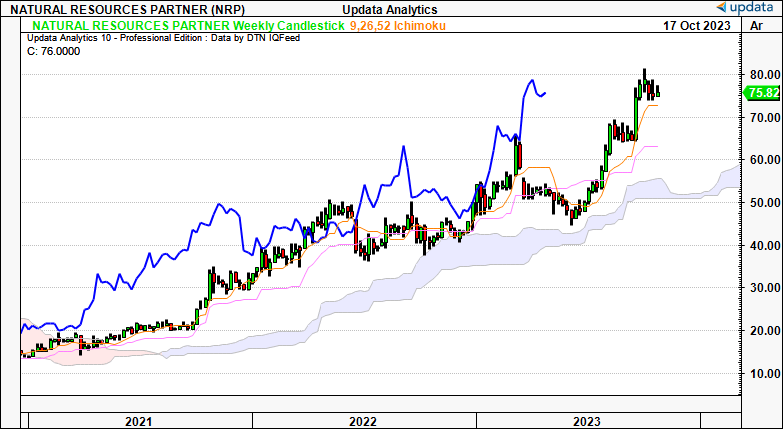

Figure 12 —Weekly chart, looking to the coming months of trade

- The weekly chart, looking to the coming months, is particularly supportive.

- Price and lagging lines have surged to the upside, gapping the distance between themselves and the cloud top.

- The cloud itself is also in continuation of its longer-term up trend that's been in situ since late 2021.

- So on the long-term time frame, I remain bullish on NRP's technicals.

{kind=link}

Valuation and conclusion

For all the constructive points outlined thus far, NRP is still priced at 5.9x trailing earnings , 5.2x trailing EBIT, and 4.1x trailing NOPAT for that matter. Two significant points are relevant here.

For starters:

- From Q2 '22—'23, it averaged a 73% return on new capital committed to the business (it was 427% last period), calling for $399mm in NOPAT going forward.

- At the same 4.1x trailing multiple, this warrants a market value of $1.6Bn (4.1x399 = $1,598), otherwise 70% value vap.

Secondly:

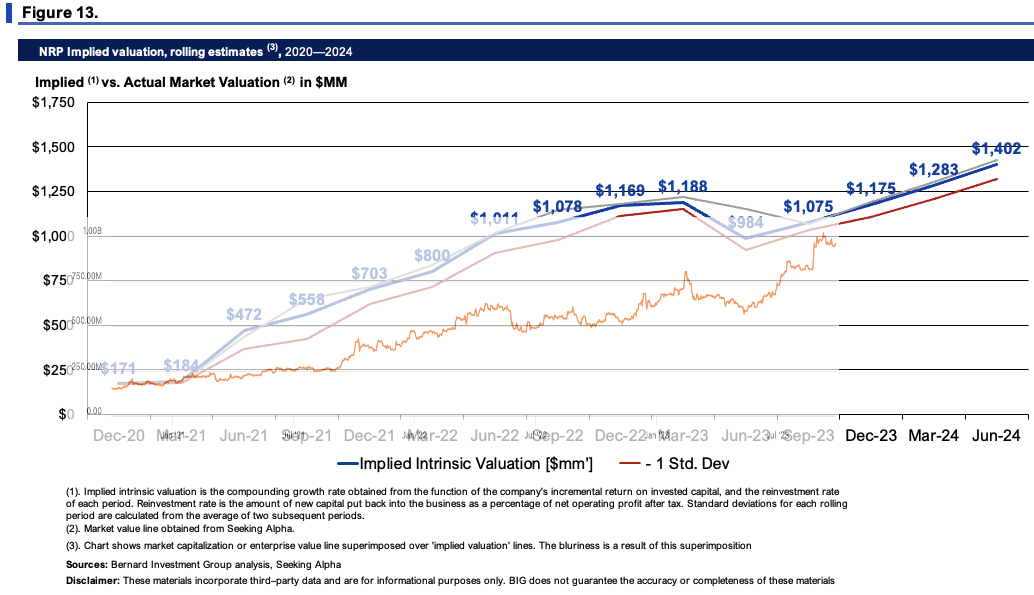

- Compounding the firm's intrinsic value at the function of its ROIC and reinvestment rates, its ascent is well justified on sound economic principles (Figure 13).

- Extending my projections out to FY'24, which are based on NRP's steady state numbers, implies the company could trade fairly at $1.4Bn market value.

In both cases, the stock appears undervalued, and this is supported by the fact it trades at a 4x EV/invested capital multiple, which, compared to its business returns outlined earlier, implies that only ~62% of its earnings power is captured at its current market value (Figure 14).

{kind=link}

In short, there is a wealth of data corroborating the growth story for NRP. In particular, its competitive positioning is supported by differentiated economics that see it claim exceptionally high margins, not something you'd expect in this arena. Market technicals support a buy rating as well, and in my opinion, the company remains undervalued based on earnings power and asset factors. I believe it could trade fairly at $111—$119 per share, should it continue at this pace.

Key risks include the following:

- Potential drawdowns in market coal pricing, crimping NRP's top-line revenues and sales volumes,

- Macro-level risks which could spill over to broad equity markets, including the inflation/rates axis,

- Geopolitical risks which could result in a flight to quality and reduce risk appetite for aggregate investors,

- Any setbacks at NRP's core assets across its coal and soda ash production sites.

These risks should be recognized in full before proceeding further. Net-net, I rate NRP a buy.

For further details see:

Natural Resource Partners: Differentiated Resource Play With Economic Leverage On Capital