NATR - Nature's Sunshine Products: Revenue Growth Resumes

2023-09-05 01:19:46 ET

Summary

- Nature's Sunshine Products' revenue increased by 11.9% YoY, while operating margin reached 6%.

- Rising prices for the company's products and strong trading trends in the markets of Europe and Asia will continue to support financial performance.

- I believe that the recovery in the North American and Chinese markets will contribute to revenue growth in the coming quarters.

Introduction

Shares of Nature's Sunshine Products ( NATR ) have risen 91% YTD. Although the company's stock has risen strongly, I believe that the strong operating and financial trends of the business will continue to drive the stock higher in the coming periods.

Investment thesis

I believe that a recovery in sales in North America and China will support revenue growth in the coming quarters as consumer behavior normalizes. Moreover, cuts in logistics costs could push the gross margin up next year, which could also lead to stock repricing. In addition, I would like to note the company's strong guidance both in terms of business growth and profitability.

Company overview

Nature's Sunshine Products is a company that manufactures and sells food and personal care products. The main brands are Nature's Sunshine and Synergy WorldWide. The company operates in the markets of North America, Europe, Asia and Latin America.

2Q 2023 Earnings Review

Over the past four quarters, the company's revenue performance has been under pressure in all major markets, such as Asia, Europe and the United States, due to both lower real consumer incomes and negative pressure from covid restrictions in China, however, in Q2 2023, we can see the first signs of normalization of growth rates.

Revenue growth by geography (%, YoY) (Company's information)

If we look at the dynamics of operating expenses, we can see a similar trend. Spending on SGA (% of revenue) has been at an elevated level over the past two quarters due to declining economies of scale, which put pressure on the operating profitability of the business.

In 2Q 23, the company's revenue increased by 11.9% YoY . The geography of Europe and Asia made the largest contribution to revenue growth, where sales increased by 24% YoY and 16% YoY, respectively. Gross profit margin increased from 71.7% in Q2 2022 to 72.6% in Q2 2023 due to higher product prices and a favorable product mix.

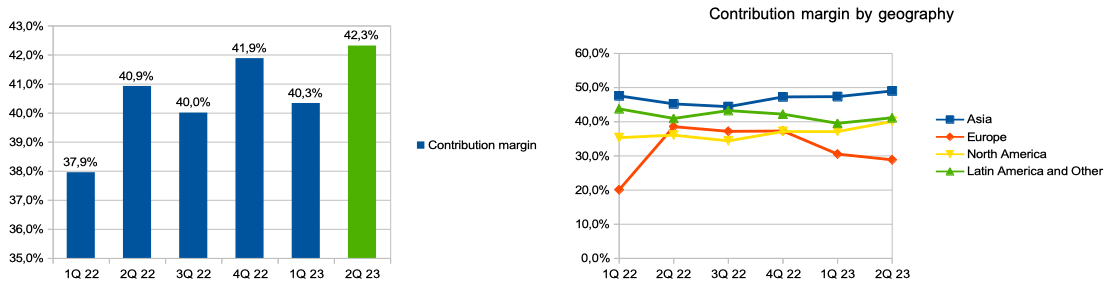

Contribution margin increased from 40.9% in Q2 2022 to 42.3% in Q2 2023 due to an increase in Asia from 45.2% to 49.0% and in North America from 36.1% to 40, 1%, while in Europe the company showed a decrease from 38.6% to 28.9%.

Contribution margin & contr. margin by geography (Company's information)

{kind=link}

Spending on SGA (% of revenue) increased from 35.4% in Q2 2022 to 36.3% in Q2 2023 due to higher service prices in China, while spending on volume incentives (% of revenue) decreased from 30.8% in Q2 2022 to 30.3% in Q2 2023.

Op. expenses (% of revenue) (Company's information)

{kind=link}

Thus, operating margin increased from 5.5% in Q2 2022 to 6.0% in Q2 2023

Operating income margin (Company's information)

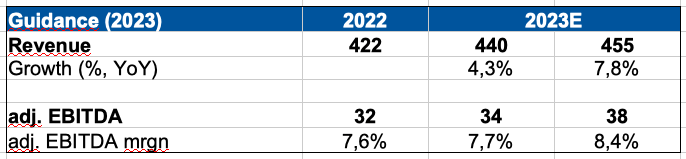

In addition, the company provided guidance for 2023. Thus, management expects sales to be around $440-$455 million, which implies revenue growth of 4.3% - 7.8% YoY. You can see the details in the chart below.

Guidance 2023 (Company's information)

{kind=link}

My expectations

Despite the fact that I do not expect the company to show a significant increase in operating margin in the next 2 quarters, I believe that continued solid revenue growth may support the company's quotes. First, I think North America revenue will continue to recover as consumer behavior normalizes and new customers increase in the online sales channel.

We're actually seeing improvements in buying behavior. And I think we're -- historically, we were seeing our order count hold steady, but average order was way down. And this was kind of the first time in a while where both orders were growing and average order was growing. So that's an encouraging sign for us.

In addition, as I wrote in the previous section, the company's guidance for 2023 assumes revenue growth of 7.7%-8.4% YoY, however, if we pay attention to expectations regarding 2H 23, we see that the company expects that the revenue growth rate in 2H 23 will be 3.6%-10.9% YoY.

Secondly, I expect that the company's initiatives to reduce logistics costs can provide significant support to the dynamics of business profitability. According to management comments during the Earnings Call , the company plans to reduce supply chain costs by approximately $10 million, which is equivalent to about 8.2% of cost of sales in 2022. Thus, we can expect additional support for the company's gross margin of about 300 bps in 2024.

Yeah. We talked about a $10 million savings target that we're working to accomplish over 24 months. And so if you do the math on that, then it's a little less than 300 basis points.

Drivers

Revenue: an increase in the number of buyers due to an increase in the online presence and an effective marketing campaign, as well as an increase in the average check due to the rebranding of existing products, can support revenue dynamics in the following periods.

Margin: optimizing supply chain costs could boost gross profit margin in 2024.

Risks

Margin: an increase in logistics and marketing costs can have a negative impact on the operating profitability of a business.

FX: dollar strengthening against other currencies (EUR, CNY etc.) may lead to a decrease in the company's revenue in dollar terms.

Macro (general risk): a decline in real consumer incomes could put pressure on consumer spending in the discretionary segment, which could contribute to a slowdown in business revenue growth.

Valuation

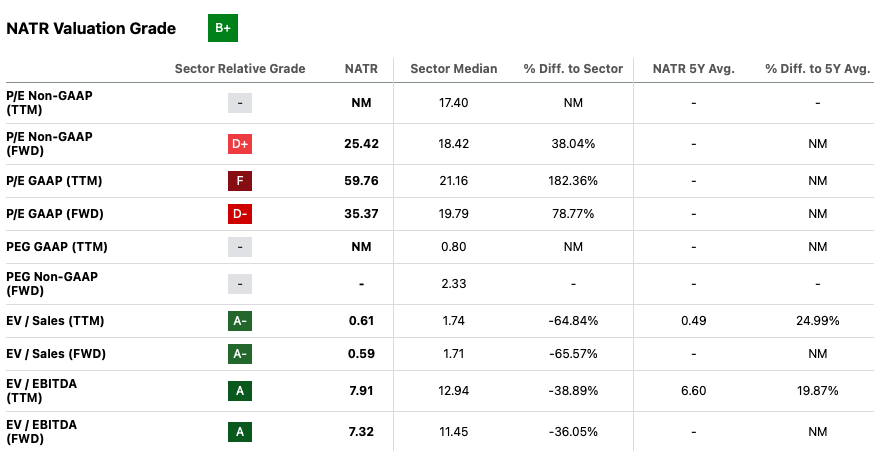

Valuation Grade is B+. On EV/EBITDA ((FWD)) and EV/Sales ((FWD)) multiples, the company trades at 7.5x and 0.6x, respectively, implying a discount to the sector median of around 34% and 64%, respectively. I believe that the current level of quotes looks attractive not only based on the relatively low valuation according to multiples, but also due to the presence of growth drivers/catalysts such as a recovery in revenue growth and a potential improvement in profitability during 2024.

{kind=link}

Based on the company's guidance for 2023 and an EV/Sales multiple of 0.8x, which still implies a discount to the sector median of around 54%, I believe the fair price for the share is around $19.5 with an upside potential of 17%.

Valuation (Personal calculations)

Conclusion

Thus, based on the relatively low valuation of the business by multiples, the recovery in revenue growth, strong guidance and the potential to improve the business' margins, I believe we still have an attractive long entry point. My investment idea is based on a possible recovery in business growth and profitability, however, I am open to changing my recommendation to HOLD in the future if I see continued pressure on sales in the US, Europe or Asia markets, or if the company's initiatives to optimize supply chain costs turn out to be less effective than expected.

For further details see:

Nature's Sunshine Products: Revenue Growth Resumes