NWG - NatWest: Cheap Again After The Recent Sell-Off

2023-05-11 02:07:09 ET

Summary

- NatWest shares have slipped in recent weeks, and they once again trade at a discount to tangible book value.

- Business has thus far remained quite resilient, helped by a concentrated domestic banking market that gives it an edge on funding costs.

- These shares remain cheap below 1x tangible book value and at around 6x my 2023 EPS estimate, notwithstanding risks to the bank's earnings potential.

To say that NatWest ( NWG ) has had a bumpy ride over the years would be understating it. The gilt market debacle in the UK and fears regarding the health of the US banking system are merely the latest in a long line of headwinds to face the British bank, whose stock has nonetheless been gaining traction since I first covered it with a 'Buy' rating back in 2021.

{kind=link}

Source: Seeking Alpha

Up around 35% since then in local GBP terms (with dividends), these shares have done well, and despite cooling off following bank failures in the US they are also still up around 14% (again with dividends) since my most recent piece late last year. Note that ADR performance varies (for better or worse depending on the timeframe) due to USD/GBP currency fluctuations.

As expected, NatWest's profitability has received a significant boost from higher interest rates. It was the most interest rate sensitive of the big UK players, and that formed a component of my buy case here alongside a valuation that has typically been below tangible book value per share ("TBVPS"). NatWest does face risks on funding costs and credit quality, but with its business looking resilient and the stock recently slipping back below TBVPS I'm inclined to think that it remains good value.

Deposits Holding Up Well

Recent events in the US banking space have demonstrated that higher interest rates aren't always great for banks. Funding costs are rising quickly, squeezing net interest margins ("NIM") and the profitability of many lending-centric players, particularly the smaller ones.

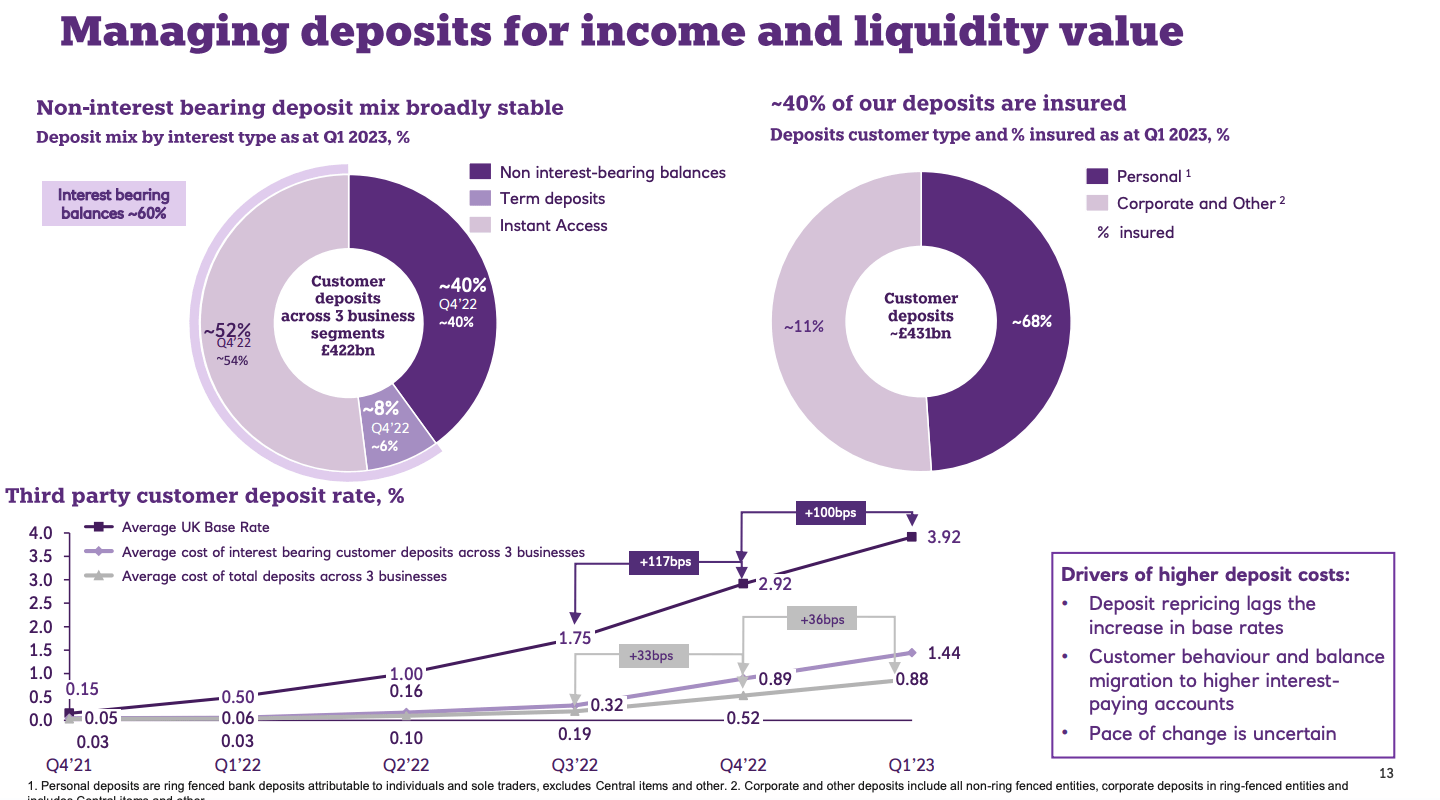

That is one of the reasons I like NatWest. With £190B in retail deposits, it is the number two deposit gatherer in a banking system that is highly concentrated, with a handful of banks controlling the lion's share of UK deposits.

{kind=link}

Source: NatWest Q1 2023 Results Presentation

With that, customer deposits did fall 2.6% sequentially in Q1 2023, though this was primarily due to higher tax payments by customers. Management expects full-year 2023 deposit balances to be "broadly stable or modestly lower", implying a fairly resilient deposit franchise. Deposit costs only rose by 36bps sequentially in Q1 (versus a 100bps rise in the average UK base rate), with the bank's net interest margin ("NIM") rising 2bps sequentially (excluding notable items) to 3.27%.

Profitability Up Significantly

NatWest stood to gain the most from higher interest rates of the big London-listed banks, and with the base rate now at 425bps, credit quality remaining strong, and OpEx cost growth fairly muted, it is seeing a big improvement in underlying profitability.

{kind=link}

Source: NatWest Q1 2023 Results Presentation

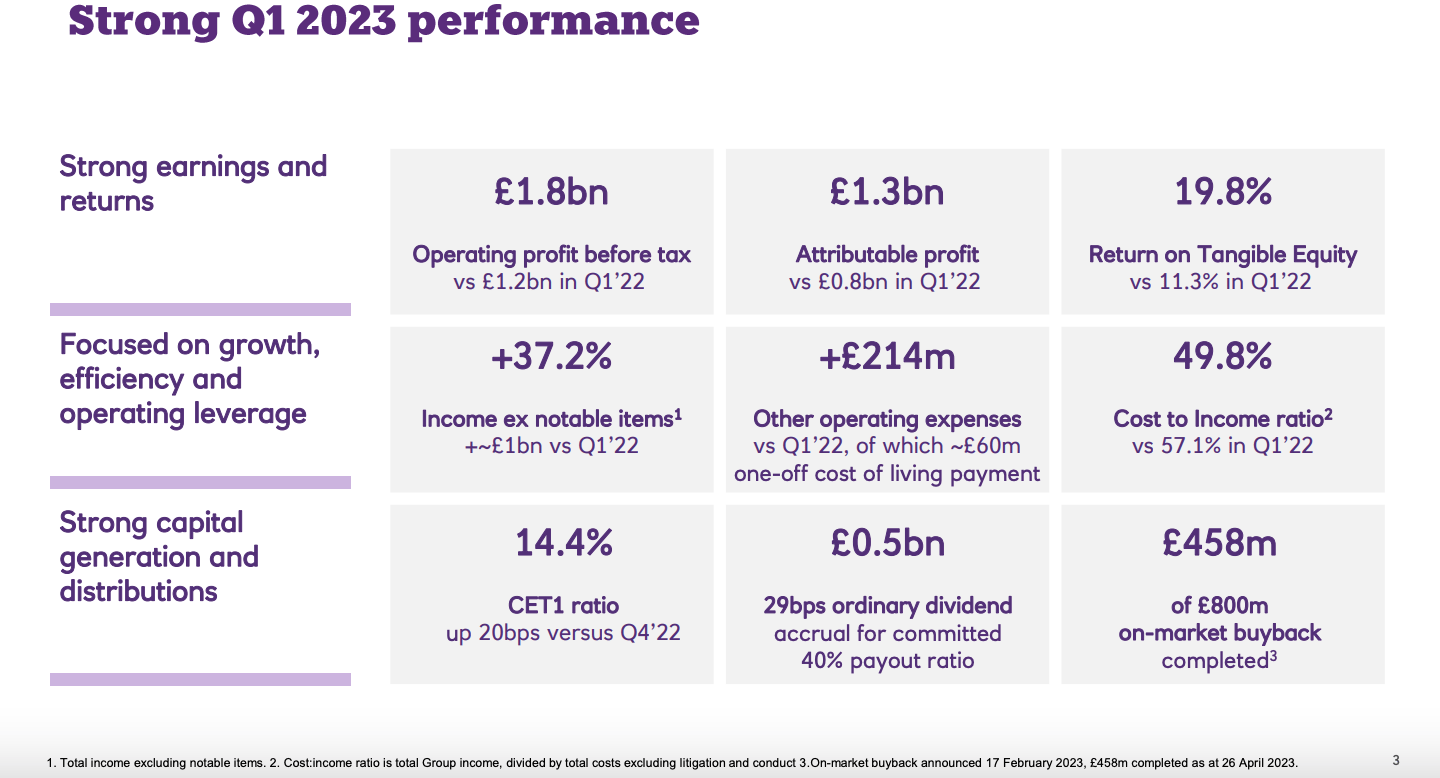

Q1 pre-provision operating profit was £1.89B, an increase of 20% sequentially and 60% year-on-year. I was a bit worried on operating expenses in my last update, with management yanking the previously flat outlook for 2023 costs in light of higher inflation. More color has since been provided, with new guidance for 2023 other operating expenses (i.e. excluding litigation and conduct costs) landing at £7.6B. That would represent a little over 4% growth both year-on-year and versus 2021, much lower than the headline rate of inflation.

Credit quality remains much stronger than I expected, with the loan impairment rate landing at just 0.07% in Q1. All told, that was good for a 19.8% return on tangible equity last quarter.

Shares Again Below Tangible Book Value

Having hit a high of over 308 pence per share earlier in the year, NatWest shares now trade at just 260.7 pence apiece. That is equal to around 0.93x Q1 TBVPS, 6x my 2023 EPS estimate (43.5 pence) and, based on management's stated 40% payout ratio, represents a 6.7% forward dividend yield.

Given management's 2023 and mid-term guidance of a 14-16% ROTE, anything below tangible book value looks very cheap to me, with my fair value closer to 1.2-1.3x TBV per share (~345 pence, or $8.70 for the ADRs). That implies around 33% upside from the prevailing price.

Value multiple expansion has formed part of the 'buy' case here since I have covered it, but I would add that it is not necessary to achieving attractive total returns. Indeed, on 6x tentative FY23 EPS NatWest shares can deliver good returns simply via dividends and stock buybacks. This has partially been the case to-date, with cumulative dividends of over 30 pence per share worth 15% of the share price at initial coverage less than two years ago.

Skewing More Toward Reward Than Risk

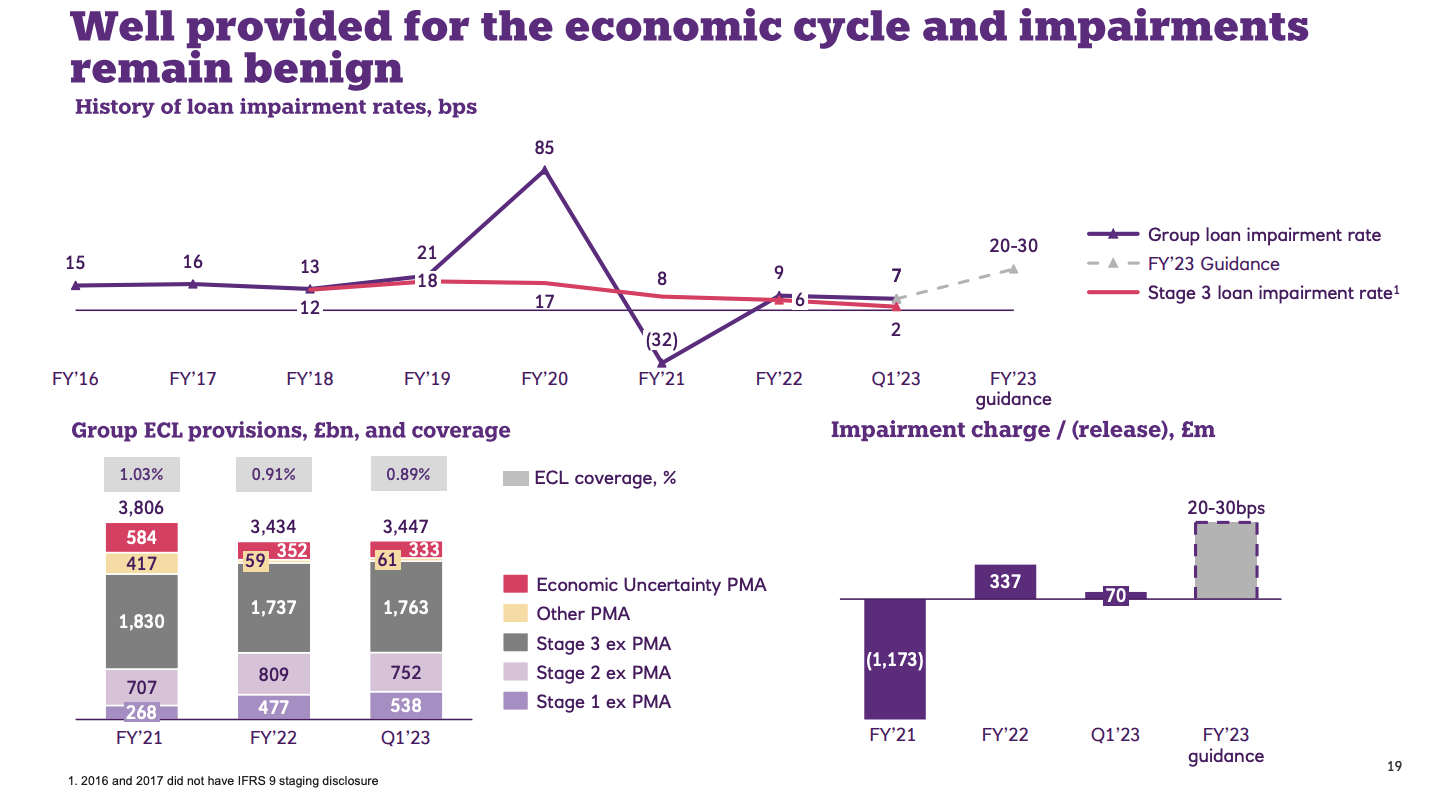

There are risks to the above which may explain the market's reluctance to assign the shares a higher valuation. Credit quality is one, with my FY23 EPS estimate and management's profitability targets resting on an 20-30bps through-the-cycle impairment rate (which is also the expected 2023 impairment rate). Depending on its severity, a recession in the UK could send the impairment rate higher than management's target range.

{kind=link}

Source: NatWest Q1 2023 Results Presentation

Interest margins are also a source of risk to earnings and profitability. Funding costs could increase more than expected, squeezing NIM, while a pivot back to lower interest rates would have the same impact. This would also erode NatWest's new-found higher levels of profitability; in a zero-rate environment the bank would struggle to generate a double-digit ROTE. There could also be some near-term upside here, though, as management's 320bps NIM guidance is based on a stable 4.25% Bank of England base rate, which will likely head at least a little higher.

We continue to expect net interest margin for the full year of around 320 basis points. This assumes the current UK base rate remains at 4.25% throughout 2023, up from 4% in our previous projections, and the average reinvestment rate of our product structural hedge for the full year is 3.6%, up from 3.3%, which is largely offset by our expectation of lower average deposit balances.

Katie Murray , NatWest Group CFO

I do think these risks are baked in the current share price. Note that EPS could decline by almost 40% relative to my 2023 estimate and these shares would still only trade on a P/E of 10x and an implied dividend yield of 4%. As a result, I believe NatWest shares skew more toward 'reward' than 'risk' at the current price, and I'm happy to maintain my 'Buy' rating.

For further details see:

NatWest: Cheap Again After The Recent Sell-Off