ABOS - Navigating Acumen's Alzheimer's Risk And Reward

2023-10-03 11:03:22 ET

Summary

- Acumen Pharmaceuticals' ACU193 shows promise as a potential treatment for early-stage Alzheimer's Disease, targeting amyloid beta oligomers with a more favorable safety profile.

- Q2 earnings show increased operating expenses and a net loss expansion, but a recent capital injection extends the cash runway and lowers the threat of near-term dilution.

- Market sentiment is cautious, but the Phase 1 results and financial stability suggest a potential buying opportunity for risk-tolerant investors.

At a Glance

From a clinical standpoint, Acumen Pharmaceuticals' ( ABOS ) ACU193 appears to be carving out a potentially revolutionary niche in Alzheimer's treatment. The specificity of ACU193 for amyloid beta oligomers could herald a step-change in safety, particularly in reducing ARIA-H (hemorrhage), an often debilitating side effect. This carries significant weight for particular genetic cohorts that are prone to ARIA-H and could expand the drug's target market. Financially, Acumen's robust cash runway of 74 months and a strong current ratio of 31.9 augurs well for its near-term stability. However, the 29.5% year-over-year escalation in operating expenses serves as a cautionary note, indicating the financial toll of clinical ambition. While the strong liquidity position minimizes dilution risks in the near term, Acumen remains a high-risk proposition due to looming Phase 2 and 3 trials and elevated operational costs. Investors would do well to closely monitor upcoming trial milestones and fiscal metrics in subsequent quarters.

Q2 Earnings

To begin my analysis, looking at Acumen's most recent earnings report for Q2 2023, several indicators warrant attention. Operating expenses surged to $13.5M from $10.4M YoY, a 29.5% increase largely driven by a $1.8M uptick in R&D expenditures. Net loss slightly expanded to $11.6M from $10.2M. Importantly, weighted-average shares outstanding exhibited modest dilution, growing from 40.5M to 41.0M, a 1.3% increase. On the flip side, interest income showed an impressive jump to $1.88M, up from $260K, partially mitigating the operational loss.

Financial Health

Turning to Acumen's balance sheet , post-July offering, the liquid assets pool swells to $266.8M-comprising the original $144.8M plus the $122M injection from the follow-on offering . The current ratio, recalculated with the new total current assets ($271.5M), against the existing total current liabilities ($8.5M), escalates to 31.9. Despite the previous monthly cash burn rate of approximately $3.6M, this significant capital infusion extends the cash runway to a robust 74 months. While past data is not necessarily indicative of future performance, it remains a noteworthy metric for gauging financial stability.

Considering the elongated cash runway and enhanced liquidity, the necessity for Acumen to secure additional financing in the near term is decidedly low. These are my personal observations, and other analysts might interpret the data differently.

Equity Analysis

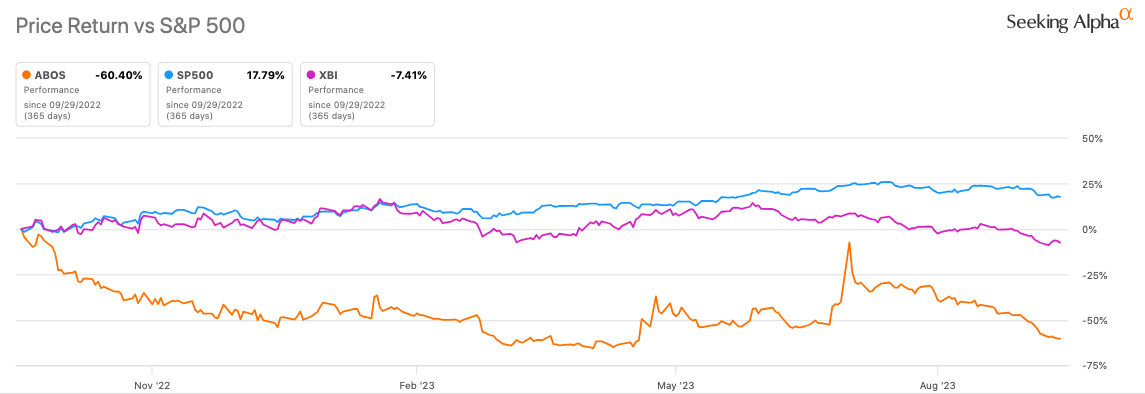

According to Seeking Alpha data, Acumen has a market cap of $240.15M, signaling market caution more than confidence given its potentially disruptive Alzheimer's treatment. Analysts project negligible revenues into 2025, emphasizing the early stage of its drug development. It's underperformed the SPY considerably, with a 1-year decline of 60.4% vs. SPY's +17.79% gain.

{kind=link}

The options trading data, specifically the lower volume and wide bid-ask spreads, hint at elevated implied volatility and a lack of consensus on directional sentiment. Short interest stands at 6.61%, indicating some skepticism. Significant ownership is seen with PE/VC Firms holding 38.48%, implying vested interests in long-term outcomes. Institutional holdings show more positions decreased (38) than increased (21), raising concerns. Insider trading reveals a net positive activity with 5,119,341 more shares bought than sold in the last 3 months, thanks to notable investments from Ra Capital, lending a bullish undertone.

Acumen's ACU193 Shows Promise for Early-Stage Alzheimer's

The Phase 1 INTERCEPT-AD study of Acumen's ACU193 demonstrated significant promise in both efficacy and safety for early-stage Alzheimer's disease [AD]. The drug is a first-in-class amyloid beta oligomer (A?O)-targeting antibody, a distinction that sets it apart from currently approved treatments like Leqembi. While Leqembi targets broader amyloid plaques, ACU193 focuses on A?Os-smaller, toxic aggregates directly implicated in AD pathology. This specificity not only offers a different mechanistic approach but also presents a more favorable safety profile.

Data from the study demonstrated a 25% reduction in amyloid plaque load at 60 mg/kg every 4 weeks and a 20% reduction at 25 mg/kg every 2 weeks, implying robust efficacy (both p=0.01). Importantly, the occurrence of ARIA-H (hemorrhage) was substantially lower at 8.3% in ACU193-treated patients compared to 17% incidence seen in past Leqembi clinical trials. ACU193's specificity for A?Os may mitigate the risk of ARIA-H, offering a safer alternative. This is particularly noteworthy for certain patient groups that are genetically more prone to developing ARIA-H, such as APOE4 homozygotes, where ACU193 demonstrated a nearly absent incidence of these side effects.

In summary, ACU193's unique targeting of A?Os may not only offer a potentially more effective treatment for the neurotoxic species directly involved in AD but also a more favorable safety profile compared to existing therapies like Leqembi. Given the data, ACU193 could serve a broader and more differentiated patient population, especially those who are more vulnerable to safety concerns like ARIA-H.

My Analysis & Recommendation

In wrapping up my analysis on Acumen Pharmaceuticals, investors need to be acutely aware of both the promise and the precariousness of this biotech play. The Phase 1 INTERCEPT-AD study data is a shot of adrenaline to the bullish thesis, notably for its dose-dependent efficacy and safety profile. The potent and specific targeting of A?Os could be a game-changer in Alzheimer's therapeutics, positioning ACU193 as potentially safer and more efficacious than incumbents like Leqembi. However, let's not forget, that the company has a long road ahead-Phase 2 and Phase 3 studies, regulatory hurdles, and fierce market competition.

The operational financials should not be glanced over. While the company's Q2 2023 performance shows increased operating expenses and a net loss expansion, these figures are in line with a company aggressively pursuing a revolutionary therapeutic avenue. The recent capital injection extends its cash runway substantially and the 31.9 current ratio significantly minimizes immediate financial risk, lowering the threat of near-term dilution.

From a market sentiment perspective, Acumen's underperformance relative to SPY and the lackluster volume in options trading could be seen as market trepidation, perhaps even a potential buying opportunity for risk-tolerant investors. Still, the high level of PE/VC Firm ownership and insider buying may indicate a belief in the company's long-term prospects. However, the declining institutional holdings and 6.61% short interest serve as flags of caution. These metrics offer a complex but calculated market tableau: there's both skepticism and guarded optimism.

In the immediate term, investors should scrutinize the initiation and any subsequent readouts from the Phase 2 study. Be on the lookout for updates on patient enrollment rates, as slower-than-expected enrollment could put a damper on the stock. Furthermore, monitor any indications from regulatory bodies that could either boost or bust the bullish sentiment. Keeping an eye on R&D expenses in the next earnings report will also be crucial to understand if the company is maintaining its focus on ACU193's development.

Given the compelling Phase 1 results, financial stability due to recent capital infusion, and initial market sentiment, assuming an investor has the risk tolerance for early-stage biotech, I would tilt towards a "Buy" recommendation for Acumen. Yet, this is not a clarion call for an all-in investment. It's a calculated gamble, one that needs to be balanced with a keen eye on upcoming clinical milestones and fiscal prudence.

As in all such investments, the need for portfolio diversification can't be overstated, and any allocation towards Acumen should be commensurate with your risk tolerance and investment objectives. Remember, it's not just about being right; it's about being right for the right reasons, continuously reassessed with incoming data.

Risks to Thesis

Although I lean towards a "Buy" for Acumen Pharmaceuticals, several factors could upset this recommendation. First, the elevated operating expenses raise questions about financial discipline. While R&D is critical, unchecked spending may indicate poor management. Second, the Alzheimer's drug landscape is littered with past failures; optimism around Phase 1 data can be a trap, especially given the complex pathogenesis of Alzheimer's. Third, the high current ratio, while generally positive, may also signal inefficiency in capital use. Lastly, market sentiment is notably cautious, as evidenced by underperformance relative to SPY and higher short interest. Keep these contrarian points in sharp focus.

Also note that investing in microcap companies like Acumen Pharmaceuticals comes with a unique set of risks that warrant careful consideration. Liquidity is often lower, making both entry and exit more challenging and potentially costly due to wider bid-ask spreads. The stocks are generally more volatile and subject to rapid price swings. Additionally, these companies are frequently in the early stages of product development, making them highly dependent on the success of a few key projects. Regulatory setbacks or clinical failures can drastically affect the stock price. Information asymmetry is another concern; with less analyst coverage and available data, investors may find themselves at a disadvantage. Furthermore, microcap stocks are more susceptible to market manipulation and fraud.

For further details see:

Navigating Acumen's Alzheimer's Risk And Reward