PBYI - Navigating Puma's Stagnant Revenue And Rising Costs

2023-09-29 17:07:10 ET

Summary

- Puma Biotechnology's Q2 2023 earnings show stagnant revenue and tightening margins, raising concerns about its strategic positioning.

- The company has a favorable liquidity status with $74.4M in liquid assets and positive cash inflows, but a high debt-to-market cap ratio raises liquidity concerns.

- Nerlynx's slump in new prescriptions and uncertain market positioning, along with the speculative nature of alisertib, suggest a cautious approach to investing in Puma.

At a Glance

From a risk-adjusted standpoint, Puma Biotechnology ( PBYI ) straddles a precarious line. A flatlining top line, rising operational expenses, and uncertain pipeline prospects, particularly in a competitive kinase inhibitor market set a convoluted stage. The dual red flags of insider selling and moderate short interest add further murkiness to investor sentiment. Until the company offers tangible evidence of strategic reorientation or clinical breakthroughs, a bearish tilt is justifiable. Holding off on additional exposure seems prudent.

Earnings Report

To begin my analysis, looking at Puma Biotechnology's most recent earnings report for Q2 2023, the company managed to pull in total revenues of $54.6M, virtually unchanged from $59.5M in the same period last year. Importantly, a decrease in royalty revenue from $8.2M to $3M hints at diminished leverage in partnerships. Operating costs have expanded to $49.7M, notably with SG&A expenses rising to $24.5M from last year's $20.6M, indicating possibly aggressive marketing or increased overhead. While income from operations dropped from $12.1M to $4.9M YoY, it's concerning to see net income plunging from $9.4M to $2.1M, signaling tightening margins. Earnings per share diluted also dropped from $0.21 to $0.05. Notably, weighted-average shares outstanding-diluted increased marginally from 45.4M to 47.2M, indicating minor share dilution. Overall, these metrics suggest Puma is facing pressure on both the revenue and cost fronts, likely impacting its strategic positioning.

Financial Health & Liquidity

Turning to Puma Biotechnology's balance sheet as of June 30, 2023, the company has a sum of $60.0M in 'Cash and cash equivalents' and $14.4M in 'Marketable securities', totaling $74.4M in liquid assets. The net cash provided by operating activities over the last six months stands at $5.9M, translating to a positive cash inflow of approximately $0.99M per month. It's important to note that these values and estimates are grounded in past performance and may not be indicative of future outcomes.

Puma has a favorable liquidity status, supported by $74.4M in liquid assets and a positive operating net cash inflow. On the liabilities side, the company has a current portion of long-term debt amounting to $11.3M, along with long-term debt netting $87.6M. Considering the positive cash flow from operating activities, the company is in a stable position to manage its debt and other liabilities. Given the robust financial position and positive cash inflows, Puma could likely secure additional financing if needed, either through debt or equity instruments, although its current liquidity may not necessitate such actions in the near term. These are my personal observations, and other analysts might interpret the data differently.

Capital, Growth, Momentum, & Ownership

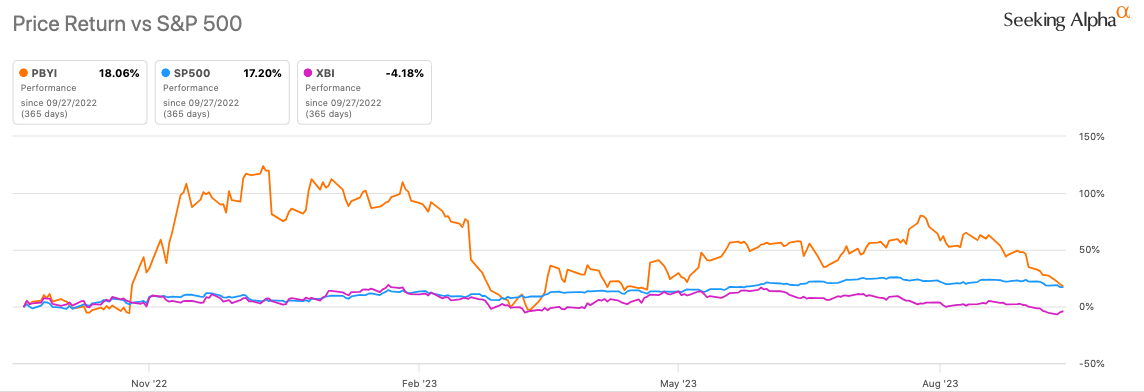

According to Seeking Alpha data, Puma Biotechnology's capital structure shows a high debt-to-market cap ratio, raising liquidity concerns but offering potential leverage benefits. The growth outlook is mixed; analysts project an initial EPS decline in 2024 followed by a rebound in 2025, with marginal sales growth. Momentum is volatile, underperforming SPY in 3M and 9M periods but outperforming in a 1Y timeframe.

{kind=link}

Ownership is predominantly institutional (41.34%), which could suggest stability but leaves room for activist investors. Insider trading reveals a recent trend of automatic sells , signaling potential caution. Short interest stands at 5.65%, indicating moderate investor skepticism but not a high-risk short squeeze scenario.

Investing in microcap stocks like Puma Biotechnology inherently involves greater risk compared to established players. Liquidity can be poor, making it difficult to enter or exit positions. Also, microcaps are often more sensitive to market volatility and economic downturns. Due diligence is absolutely essential, as the lack of comprehensive financial information and lower governance standards can obscure underlying risks.

Unpacking Nerlynx's Slump and Its Impact on Puma

Puma Biotechnology's financial performance presents a bifurcated storyline. A surface-level reading reveals a product revenue jump to $51.6 million. However, dig deeper, and you'll find that a one-off $1.5 million inventory drawdown inflates these figures, raising doubts about the revenue's long-term viability. The conundrum: Is this growth a mere statistical outlier or a leading indicator?

Turning our attention to Nerlynx, management attributes the 12.5% quarter-over-quarter slump in new prescriptions to cyclical fluctuations. While seasonality is a plausible element, it fails to account for the more alarming 4.1% year-over-year contraction. This discrepancy raises red flags about potential barriers - be it market saturation or intensifying competition - that management has yet to fully elucidate.

As we pivot to alisertib, the aurora A kinase inhibitor in Puma's pipeline, the clinical outlook appears encouraging. Preliminary trials, especially those evaluating synergistic effects with other agents, demonstrate a favorable safety profile and hint at therapeutic efficacy. However, the asset remains an enigma in terms of its market potential. Assessing alisertib's eventual worth necessitates not just a clinical but also an economic lens, particularly considering the burgeoning field of kinase inhibitors.

My Analysis & Recommendation

In light of the recent Q2 2023 earnings, Puma Biotechnology presents a less-than-clear-cut investment thesis. The revenue stagnation, especially in the context of a YoY decline in royalty streams, reflects potential headwinds in their core business. Their increased SG&A expenses pose questions on efficiency, particularly at a time when revenues are not showing a parallel rise. On the balance sheet, although liquidity appears strong, their high debt-to-market cap ratio could hinder their agility, especially when navigating a competitive oncology market.

Let's talk Nerlynx. In my view, the dip in new prescriptions isn't merely cyclical, despite management's portrayal. In a clinical setting, this often implies that either the therapeutic profile isn't compelling enough against competitors or that market saturation is nearing. Given the high stakes in oncology, small shifts in prescription behavior can herald tectonic changes. Could a competitor's drug, with a superior safety profile or fewer EGFR-related toxicities, be gaining traction at Nerlynx's expense? That's a dimension investors need to scrutinize.

As for alisertib, the early-phase excitement, while interesting, doesn't justify unbridled optimism. Aurora kinase inhibitors, although promising, are swimming in a pool teeming with potent, better-studied kinase inhibitors. If Puma intends to stand out, it must advance its clinical trials with surgical precision and present unequivocal data on alisertib's superiority in both safety and efficacy. This involves substantial R&D spending, and investors must be ready for this financial strain.

Moreover, insider trading trends showing automatic sells and moderate short interest lend themselves to a more bearish sentiment. Investors should also be cognizant of the volatility in momentum and the almost capricious market sentiment that Puma seems to carry right now. If you're considering adding more of Puma to your portfolio, it may be prudent to await stronger clinical or financial catalysts. At this point, activist investors might come into play given the high institutional ownership, potentially making the stock less stable than it appears.

Given the increasingly complex landscape and growing concerns around sustainable revenue growth, I would advise investors to maintain a "Hold" stance on Puma but with decreased confidence. Until there's clarity on Nerlynx's market positioning and alisertib's long-term viability, exacerbated by the financial misalignments in Q2 2023, a more conservative approach appears warranted. With stagnant revenue, ballooning expenses, and clinical uncertainties, this isn't the time for cavalier bullishness. Keep your powder dry for now; Puma needs to earn your bullish bet.

For further details see:

Navigating Puma's Stagnant Revenue And Rising Costs