NVGS - Navigator Holdings: Celebrating Its First Dividend Payment

2023-08-17 12:40:09 ET

Summary

- Navigator Gas is realizing the cash flow potential of its flexible vessels and ethylene export terminal. The company has initiated a dividend program and expanded the share buyback program.

- The company's fleet of handy-size vessels can load multiple forms of cargo, ensuring high demand and high charter rates.

- Navigator Gas is using its excess cash flows to fund growth projects, pay down debt, and reward shareholders, leading to potential dividend and share buyback growth in the future.

Thesis

Navigator Gas ( NVGS ) is a small shipping company that is finally realizing the potential of its highly flexible handy-size vessels and ethylene export terminal. The company has been hitting several high notes recently with the announcement of a newly instituted dividend program, a second installment of its share buyback program, and expansion plans for its ethylene export terminal.

The foundation for this small shipping company is centered in the flexibility of its assets, and the never-ending need for energy products which continue to be in high demand in markets such as Europe and Asia. The unique ability of its vessels to load multiple forms of cargo ensures its vessel remain in high demand and achieve high charter rates.

To celebrate NVGS's newfound status as a cash-producing investment, I will evaluate how NVGS is deploying its excess cash flow to fund growth projects, paydown debt, and reward shareholders. This analysis will show that NVGS is a viable candidate for a dividend growth portfolio.

Who is Navigator?

Navigator Gas is a growing shipping company that is expanding its fleet of handy-sized vessels while also expanding its land-based ethylene export terminal capabilities. The current fleet stands at a total of 56 vessels with a complementary export terminal with the capacity to export one million tons of ethylene per year.

Handy-sized vessels are the Swiss army knife of the shipping industry being relatively small in size compared to VLGC vessels (Very Large Gas Carrier) but excelling in versatility. These vessels have the ability to carry a multitude of different product types. The most advanced handy-size vessels in NVGS's fleet can transport eight different product types that include ammonia, propane, ethylene, and propylene.

These energy products are used in the agricultural, petrochemical, electrical power, and residential heating industries, and thus help support the building blocks of modern society. NVGS participates in the trade of these energy sources that is made possible through the large margin differential between the United States and the rest of the world.

The New Dividend

In the past, Navigator has been adamant that it would not pay dividends at the expense of its growth goals. At that time, it was financing multiple new vessels and an ethylene export terminal. Now, as we are approaching the completion of that growth phase, and previous projects are mature enough to be contributing to the company's bottom line, the management team has revisited this idea.

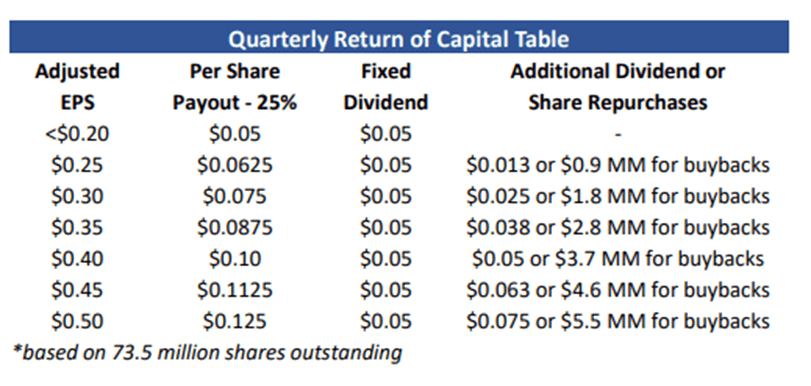

A variable dividend program has been established that meshes well with the somewhat volatile shipping industry. The company has provided guidance going forward for what investors should expect and how it relates to company earnings. The program includes both a fixed and variable return program that targets a 25% return of net income to shareholders that will be allocated between dividends and share buybacks.

{kind=link}

Following Q2 earnings, NVGS reported EPS of $0.36 per share. The company has allocated $0.05 per share as the fixed dividend and elected to allocate the remainder ($3 million) of the shareholder return package in the form of share repurchases. The $6.7 million scheduled to be returned during Q3 equates to an annualized return of $26.8 million or a combined 2.7%. While this is nothing to write home about, it is an important first step to take as a cash-generating asset.

I expect the company to focus the variable component of the return package toward share buybacks. The company currently views its stock as being a significant discount to book value and therefore is a compelling return on investment for shareholders. The chart below compares the book value and market cap of NVGS and other energy shippers such as FLEX LNG ( FLNG ) and Dorian LPG ( LPG ). You can see that NVGS does in fact trade at a discount while its peers tend to trade at a premium to their book value. The current book value is 11.6% higher than its market value.

Y charts

The Three Pillars of Growth

NVGS has three pillars of growth that will enable it to grow both its assets and the cash flow potential for shareholders.

1. NVGS employs highly flexible vessels to optimize vessel utilization and fleet economics.

2. Its ethylene export terminal located in Morgan's Point is being expanded to capture the growing demand for ethylene. The expansion of this terminal not only builds cash flows but builds demand for its shipping fleet, providing an uplift to charter rates.

3. A focus on debt reduction is built into the company's cost structure, which will pave the way for higher free cash flow in the future.

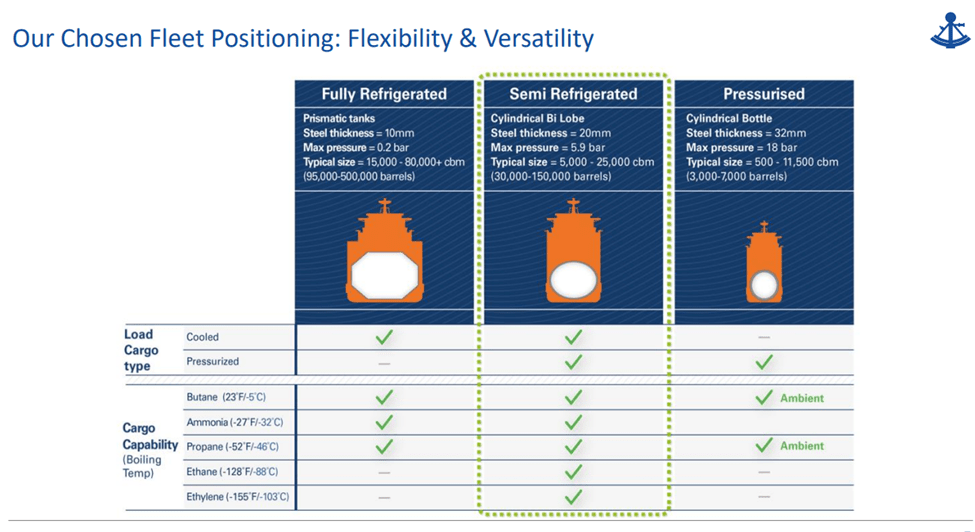

Flexibility

The flexibility of NVGS's fleet allows it to optimize trade routes by discharging a product and then subsequently loading a separate product for delivery to another location. This allows for triangular trade routes to efficiently transport energy products. This stands in contrast to that of VLGCs that often travel home empty-handed following a delivery voyage.

The versatility of the company's target vessel type is shown below.

{kind=link}

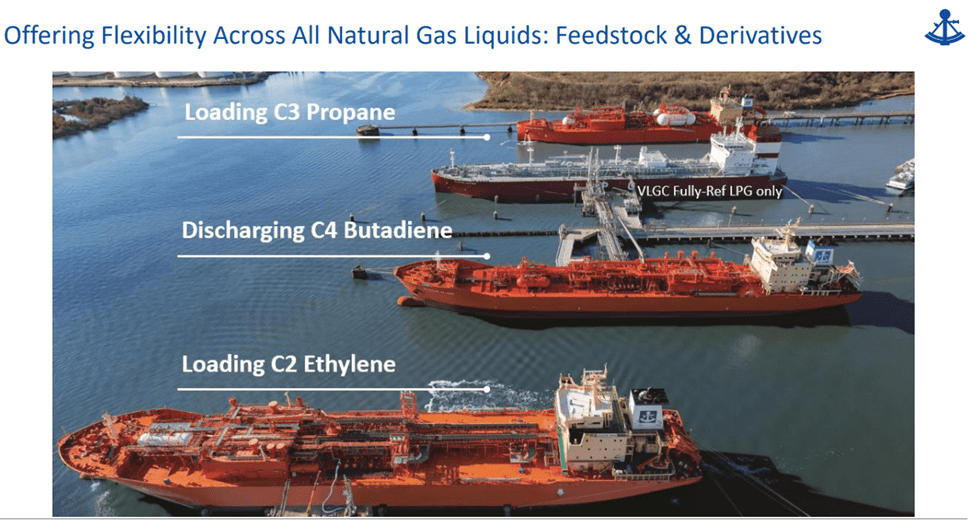

The efficiencies created by this flexibility are also shown below where three different vessels are handling three different products. It is easy to see how this can translate into high utilization factors and superior economics for its handy-size fleet. As a result, the fleet has averaged a utilization factor of roughly 90% .

{kind=link}

Diversified Earnings

Being able to support multiple products ensures that Navigator is not exposed to extreme sensitivity to any one commodity. For example, if a market disruption occurs in petrochemicals, those ships can be redeployed to transport ammonia or LPG. Navigator looks to continue to build on this strength by adding CO2 to its product mix, as announced by the formation of a new joint venture .

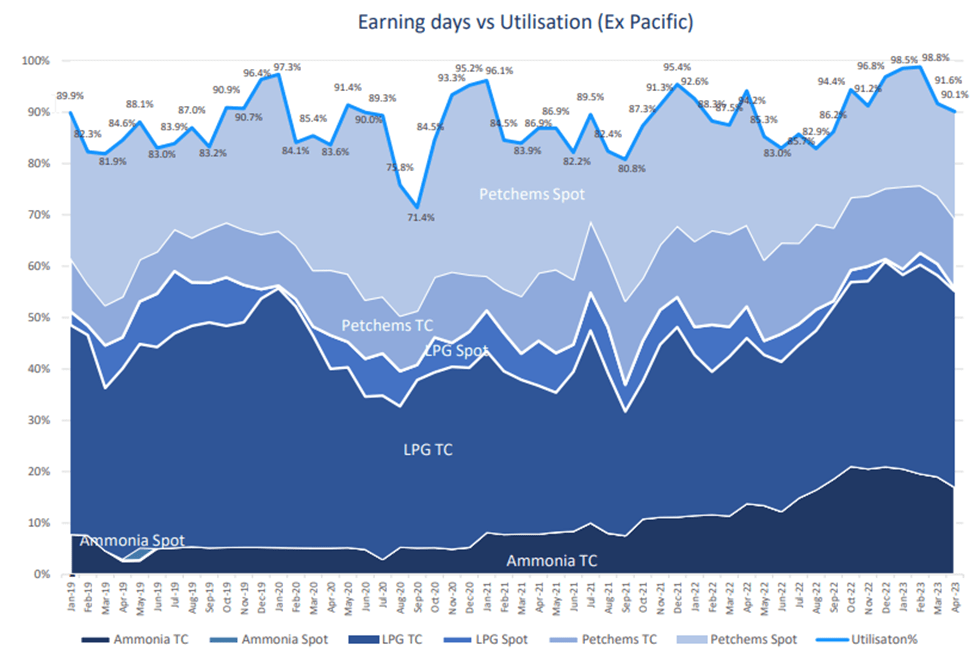

Navigator's fleet is also diversified in its contract mix. The fleet is currently deployed either under long-term fix rate time charters or periodic spot charters. The fleet is currently deployed roughly 50/50 between fixed time charter contracts and the spot market. This allows for steady earnings while also allowing the company to capture premium rates in the spot market for petrochemicals and LPG.

{kind=link}

Connecting Vessels To Shore

Navigator has not been quiet about its desire to continue to build a value chain for the molecules it transports. NVGS currently owns 50% of the ethylene export marine terminal at Morgan's Point, Texas. This terminal was placed into service in 2020 and is in such demand that it is operating above nameplate capacity by 11% in Q2 .

To capitalize on this demand, Navigator is currently in the process of expanding the capacity of this terminal. Final capacity is planned to increase by 50% at a minimum, with the maximum final rating at three times the original design (one million tons per year). This project is expected to cost $125 million. If the final capacity approaches the three-million-ton mark, this would be an extremely efficient use of capital as the original terminal construction costs were $146 million .

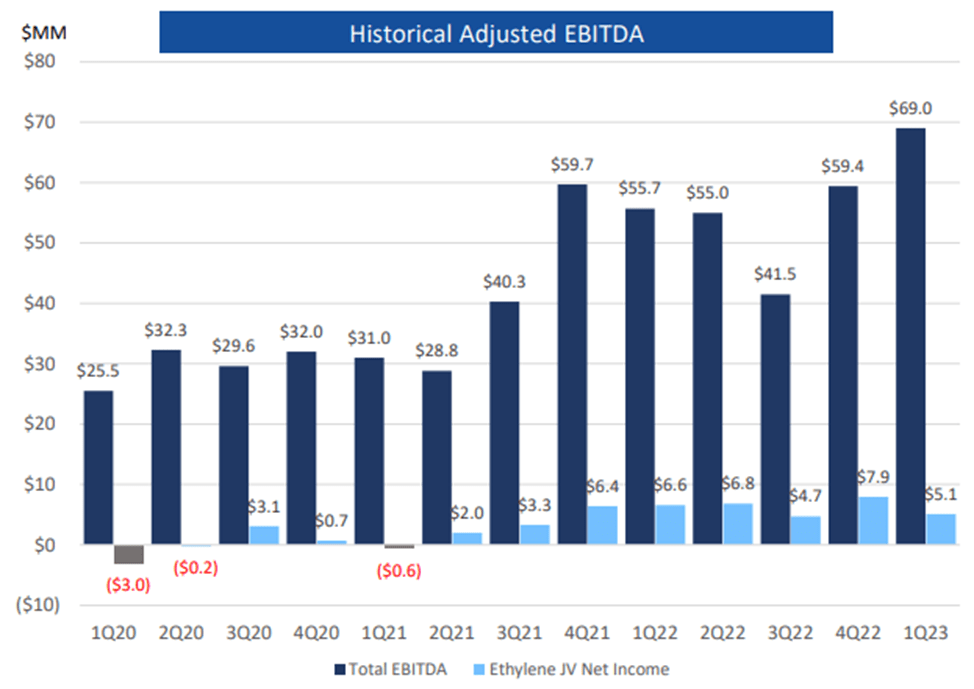

This terminal provides another form of reliable revenue and profitability. Being an infrastructure asset, this terminal generates revenue through processing fees, and as such, has been a consistent performer. This terminal has provided over $5 million in net income in six of the last seven quarters. Tripling the size of the terminal would obviously be a sizeable enhancement to NVGS's earnings potential. This project is slated to go into service in the second half of 2024.

{kind=link}

Debt Reduction

One possible negative for Navigator is that at times, the company has had elevated debt levels. Significant portions of this debt were taken on to finance growth projects such as building of new vessels and construction of the ethylene export terminal. Now that all of these assets are in service and generating revenue, it is time to turn the page and start reducing some of the long-term debt. The company has made some good headway but still has significant work ahead of it to do.

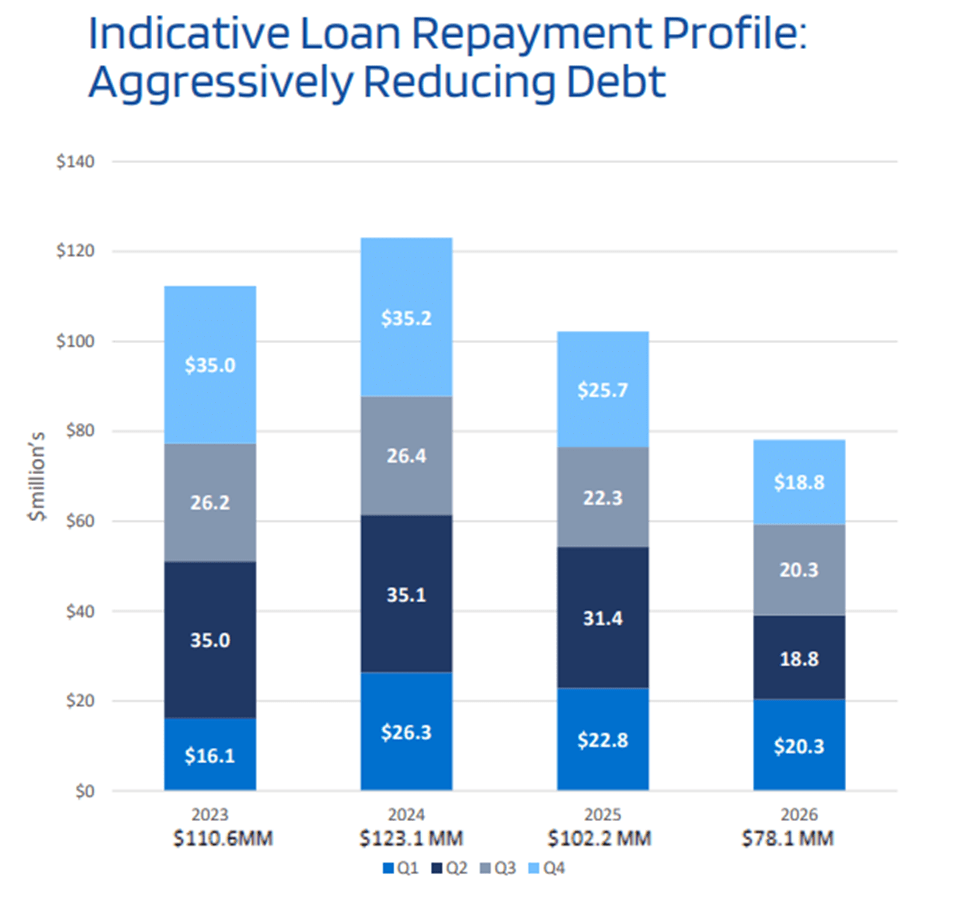

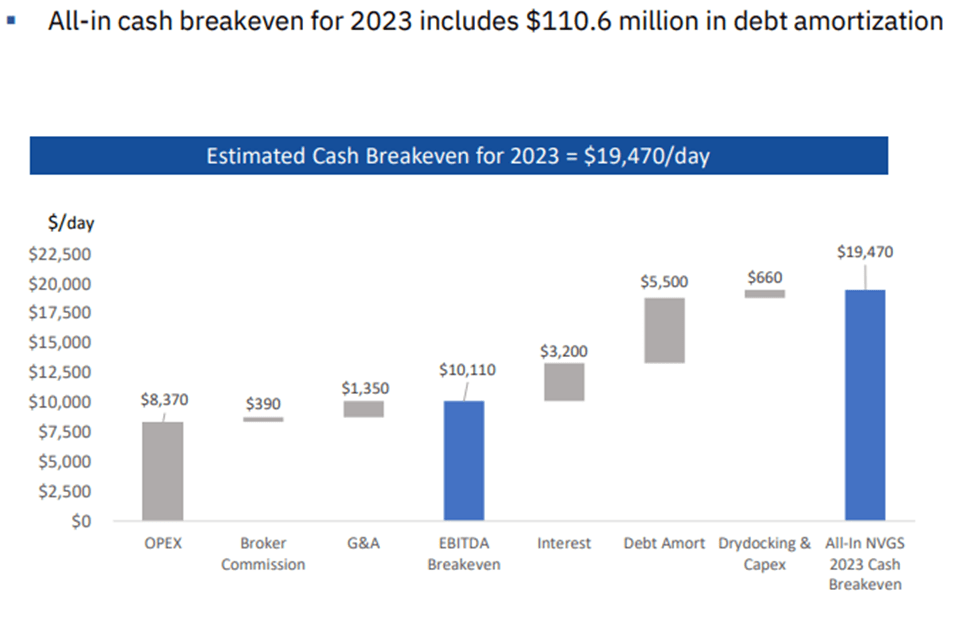

One positive I can give NVGS is that it has a solid plan in place to improve its financial footing. With $290 million in maturities due in 2025, an actionable plan needs to be in place. The company has mapped out estimated quarterly payments to pay down these debt facilities prior to their maturities as is shown below. More importantly, the company has budgeted these payments in their cash-breakeven estimate for the fleet. This breakeven value of $19,470/day includes $5,500/day of revenue diverted toward debt retirement.

{kind=link}

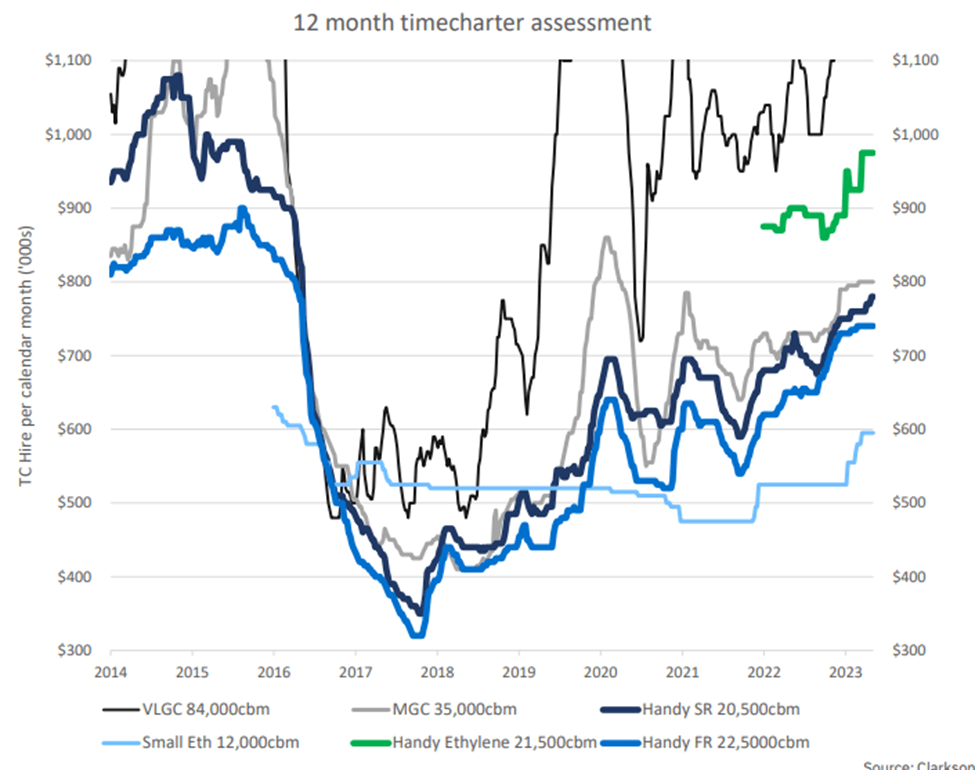

Providing additional margin that this plan will be successful is the current rising trend of handy-size charter rates. Q2 continued to build on this momentum with rates reaching $27,241/day. In addition to the $140 million of cash on hand, this leaves significant discretionary cash for deployment to fund debt reductions, growth projects (ethylene terminal expansion), and paying shareholders.

{kind=link}

Cash Flow Analysis

As shown above, a significant portion of the cash breakeven is associated to either retiring debt, or paying interest to service that debt. In fact, these expenses account for almost 45% of its cash breakeven. Therefore, it is easy to conclude that if the company is capable of conquering this hurdle, significant earnings potential can be unlocked.

Over the next 3.5 years, the company projects to have over $400 million in debt repaid. Not only will this account for nearly two-thirds of the company's current debt profile, but also significantly lower the company's breakeven point. A new breakeven baseline could be as low as $12,000/day barring any changes to operating expenses or potential dry docks.

Using the amortization plan for 2023, potential quarterly savings could exceed $35 million. After accounting for changes in taxable income, this would translate into an EPS boost of $0.30 to $0.35 per share. This also does not include any additional earnings associated with the ethylene terminal expansion or any increase in charter rates that may arise from that project.

With a variable dividend program, there's no telling how the company will allocate the shareholder returns but I believe there is compelling evidence to see expansion in both the dividend and share buybacks. This transition will be long term, but patient investors will be rewarded with both rising dividends and share appreciation.

Risks

The shipping industry has its fair share of volatility. The two main inputs to this volatility are demand for the shipped product and supply of the number of capable vessels for that product. In the 2017-2018 timeframe a significant number of newbuilds were brought into the marketplace. This dramatically increased the supply of transportation and charter rates dropped significantly. As it stands today, only three vessels are on order in the handy class segment and therefore should not meaningfully impact rates. This could however change in the future.

{kind=link}

Geopolitical events also can be a dramatic risk to energy supplies. NVGS has benefited significantly from the global trade disruption that occurred due to the Russian-Ukraine conflict. Europe has been forced to find alternative sources to meet the needs of its economy, this therefore has stimulated demand for ammonia and LPGs sourced from the United States.

This increase in shipping demand has created an increase in shipping rates as shown above. Should this dynamic reverse, it could materially impact the demand for U.S. sourced energy products and in turn, reduce charter rates.

Summary

Navigator has finally turned the corner from growth to cash generation. The next phase of its development still centers around improvements in its balance sheets and continuing to expand its terminal assets. Increasing its presence in terminal operations will provide increased earnings predictability.

Significant value can be unlocked by redeeming debt while also dramatically reducing the company's breakeven value for its shipping business. As its earning potential increases, shareholder returns will elevate as less funds are required to fund and retire outstanding debt.

Navigator Gas presents an interesting long-term dividend and total return growth investment option thanks to the initiation of the new dividend program. The company is valued at a discount to the book value of its assets and therefore also presents potential for share appreciation over the long term. I view NVGS as a buy under $14.00 per share for a dividend growth portfolio.

For further details see:

Navigator Holdings: Celebrating Its First Dividend Payment