NVGS - Navigator Holdings: Pegging Recovery On Expansion And Higher Exports

Summary

- Navigator Holdings is set to increase CapEx on Greater Bay Gas and the export terminal joint ventures to raise volume of exports.

- The company stated that it will not use debt to finance the joint venture programs.

- Navigator’s operating revenues for Q3 2022 rose 7.9% (YoY) with its adjusted EBITDA at $41.5 million against $40.5 million recorded in the same period in 2021.

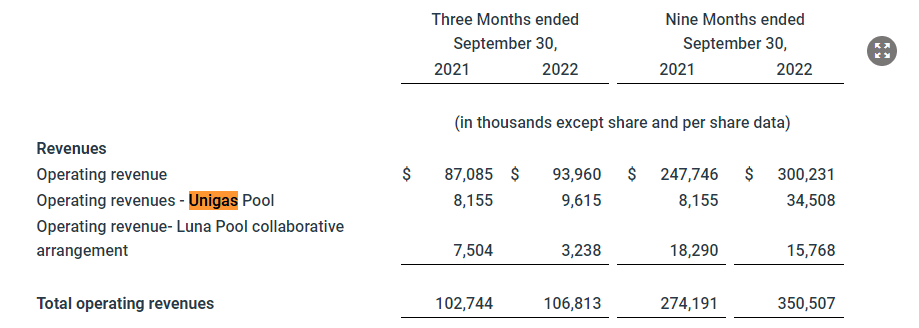

Navigator Holdings Ltd. ( NVGS ), a global owner and operator of liquefied gas carriers, missed its Q3 2022 EPS by $0.06 after reporting at $0.10 against analysts' estimates of $0.16. Operating revenue for the quarter rose 4% (QoQ) to $106.8 million against $102.7 million. Income gained as a result of increased earning days due to the deployment of more vessels on ammonia charters in 2H 2022.

Thesis

Navigator Holdings intends to increase its ethylene throughput by expanding its export terminal joint venture. This plan will see an increase in volume that will help generate additional revenue into 2025. The company also intends to capitalize on the highly competitive nature of U.S. propane as an alternative to oil in the petrochemical industry. Navigator is consequently increasing its production of liquefied gas to meet the increasing gas carrier demand. With more vessels expected in the coming years as CapEx grows, it will be interesting to see how the company handles utilization and time charter rates.

Joint Ventures

Navigator announced two joint ventures in Q3 2022 that sought to expand its operations in the global supply of liquefied gas. The two ventures involving Greater Bay Gas and the export terminal joint venture will not only see an increase in the number of vessels but the supply volume. One vessel was expected to have been acquired in December 2022 with an additional fleet to be added in 2023. Funding of this CapEx was a matter of concern since the company needed a low-cost capital program. It had witnessed a 22.96% (QoQ) drop in gross profit with a total debt of $881.4 million against a cash balance of $137.4 million.

As of December 9, 2022, Navigator announced that it had entered into a revolving credit facility agreement with $111.81 million to be made available. The company has the potential to secure more credit since its total assets are worth $2.1 billion. For this agreement, Navigator used five of its vessels as security for the term loan. We are not sure if this financial agreement will be used to finance the joint ventures, since no debt is allowed within the joint venture itself. Still, the company will be required to make a quarterly payment of $3.1 million from Q1 2023. It is supposed to make a final balloon payment on December 7, 2028, about 3 years into the intended commercialization of the export terminal joint venture.

With up to $237.7 million in current assets, including $137.4 million in cash, Navigator is still in a solid position to execute a good deal of its capital expenditure. In the Greater Bay Gas JV, Navigator owns 60% while the rest, 40% is owned by Greater Bay Gas. Here, the company is set to acquire 5 ethylene vessels by the beginning of 2024 for $233 million. Two of the ships were built in 2018 at 17,000 cm while the remaining three were built in 2018 at 22,000 cbm.

CEO Mads Peter Zacho stated,

The joint venture with Greater Bay Gas will result in a reduction in the average age of Navigator's fleet and will allow us to take advantage of more efficient vessels that are lowering our emissions and also offering improved economics for our customers.”

Navigator intends to be the market leader in the seaborne transportation of petrochemical gases like ethylene, ethane LPG and ammonia being part of the mix. Europe's thirst for energy continues to grow as the Russian invasion of Ukraine rages on. In Q2 2022, the company explained that it increased its vessels to 7 on the ammonia charters. At the time, the vessels constituted about 15% of its earnings days.

According to the EIA, the start of December 2022 has seen ethane prices fall 10% while natural gas prices declined 21% (at the Houston Ship Channel). Ethylene spot prices on their part dropped 9% with propane registering a 10% decline. However, Europe has seen a surge in energy costs, which is threatening chemical production.

We are likely to see derivative margins for feedstocks in the petrochemical industry including ethylene coming under threat in 2023 due to recession and inflation. Still, the US is putting pressure by offering competitive products despite supply chain disruptions.

{kind=link}

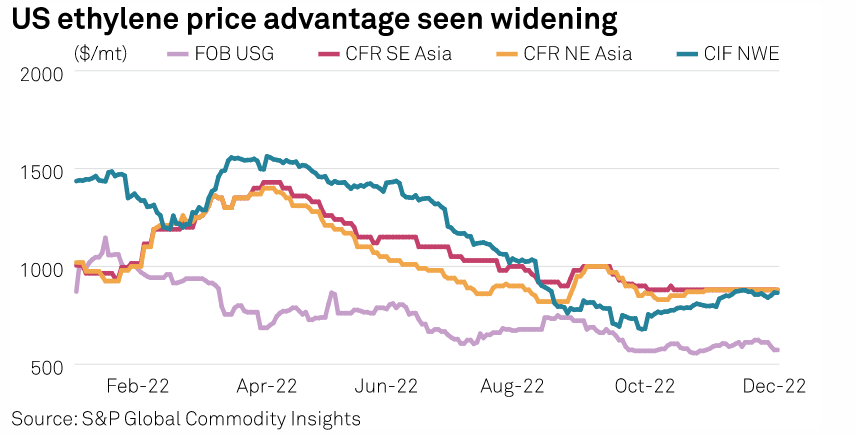

Since February 2022, US ethylene prices have declined below $1000/mt due to lower downstream demand. This situation has made more ethylene available for export.

In the other venture, Navigator has a 50% ownership with Enterprise Products Partners ( EPD ). For most of 2022, EPP operated the export terminal JV at 1 million mt/year of its capacity. With its collaboration with Navigator, the JV will expand its capacity by 50% by 2H 2023 and up to 2 million mt per year in 2025. These are realistic goals, considering ethylene margins may improve in 2023 despite an oversupply downstream. In its Q3 2022 earnings call, Navigator explained that about 80% of US ethylene exports went to Europe, with Asia also serving as a key destination.

Higher Operating Revenues

Navigator’s operating revenues for Q3 2022 rose 7.9% (YoY) with its adjusted EBITDA at $41.5 million against $40.5 million recorded in 2021. The first two quarters of 2022 had seen this metric hit a total of $55 million, but the company is optimistic about exceeding this guidance in Q4 2022. The 4% (YoY) growth in operating revenue at $106.8 million in Q3 2022 was partly attributed to the Ultragas transaction conducted in August 2021. It not only saw an increase in handy-size vessels being added to the company's fleet, but also an income generation of $9.6 million from nine vessels operating within the Unigas and Luna Pool collaborations.

{kind=link}

Revenues from Luna and Unigas Pool rose 17.9% (YoY) in the three months ending on September 30, 2022, as compared to the same period in 2021. It also gained 323.15% (YoY) in the nine months ending on September 30, 2022, as compared to the same period in 2021.

Navigator noted that vessel utilization rates for the quarter rose 84.9% (QoQ) as compared to 84% noted in Q3 2021. This improvement represented an additional income of $800,000 with improved charter rates raking in an additional $0.5 million. Having met the 85% utilization rate guidance for the quarter, Navigator will be looking to drive it north of 90% into 2023. I expect the company to increase its volumes of ethylene exports into Europe and Asia by H1 2023. This increase is possible since it confirmed the employment of 10 ships in the Asia-Pacific time charters, as well as an increase in ammonia exports.

Risks to consider

Navigator Holdings hit a utilization rate of 85% in Q3 2022 when adjusted for vessels found on time charter rates. With the company planning to increase the number of vessels, the utilization rates may likely decline below the 80% threshold. Investors will have to consider the number of vessels on varying time charters such as ammonia, LPG, and other petrochemical products. Additionally, if ammonia fails to grow as Navigator believes, especially in Europe, then it will reduce the company’s intended revenue sources and lower the utilization rates altogether.

Another risk is contained in the LNG business. In the past number of years and especially in Q2 2022, reports surfaced that due to the ongoing war in Ukraine as well as tougher emission standards some shipbuilders had decided to convert their old LNG carriers into floating storage and regasification units (FSRUs). Navigator is yet to declare if it will explore this strategic business, considering its voyage expenses increased 20.5% to $3.4 million and its vessel operating expenses gained 10.6% (YoY) to $38.7 million.

Further, in the execution of the joint ventures, Navigator stated that it would not use debt to finance its expansion strategies. The term loan secured at the beginning of December 2022, is set to be used to repay an existing loan facility of $33.3 million (from January 2015) and $78.5 million for corporate purposes. It appears Navigator lacks sufficient funds to repay long-term loans yet it is planning an expansion project with two joint ventures. Also, it is unclear if the debt from 2015 also includes the current debt, which stands at $881.4 million.

Bottom Line

Navigator Holdings is looking at the recovery of the petrochemical industry, ethylene, ethane, and ammonia at the beginning of 2023 to increase its voyage levels and add revenue. The company's two joint ventures are also expected to increase export capacity into the year. Still, it is unclear how the company will fund this capital expenditure program considering it will not use debt. However, there are still considerable amounts of cash to cover general expenses as well as maintain continual revenue generation from the Luna and Unigas Pools. However, any delay to the expansion projects will affect the share price. For these reasons, we propose a hold rating on the stock.

For further details see:

Navigator Holdings: Pegging Recovery On Expansion And Higher Exports