NMM - Navios Maritime Partners Has Corporate Governance Issues But One Of The Best Values Available

Summary

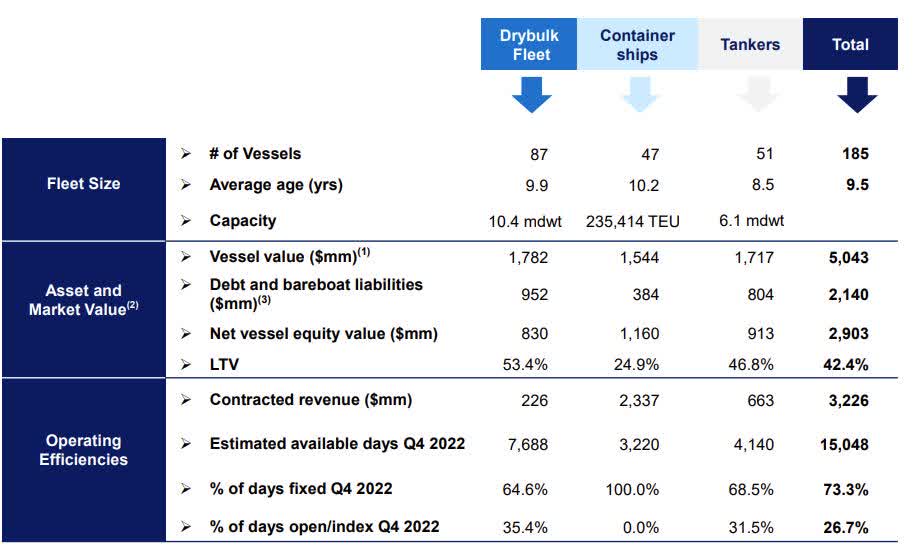

- NMM is a diversified shipping company controlling 185 vessels with a gross fleet value exceeding $5 Billion and Debt/Bareboat Liabilities of $2.1 Billion.

- NMM is highly profitable and has a 2023 forward P/E ratio of only 1.32.

- The stock is trading at about 25% of NAV.

- Recent tax changes have caused some non-US investors to sell NMM which partially explains the low valuation.

- NMM has had some serious corporate governance issues in the past, but I believe CEO Angeliki Frangou may be turning over a new leaf.

Written by George Spritzer, co-produced by Alpha Gen Capital

Author’s note: This article was released to Yield Hunting members on Jan. 16 , 2022. Please check latest data before investing.

Overview of the Company

Navios Maritime Partners LP ( NMM ) is a publicly traded limited partnership that is headquartered in Monaco. It owns and operates one of the world's largest fleet of dry bulk and container vessels. The vessels are chartered out to a diverse customer base which includes major mining companies, trading houses and steel producers.

I believe that NMM should be an attractive investment over the long run. As global trade continues to grow over time, the need for transportation of goods by sea also increases which drives demand for NMM's vessels. Their diverse customer base and variety of different vessel types should help to mitigate risk.

Another positive aspect of NMM's business is the company's strong financial position. NMM has a solid track record of generating consistent earnings and cash flow. NMM has a low level of debt which gives the company financial flexibility.

While NMM's business should be solid over the long term, it is important to point out that the shipping industry is highly cyclical and is subject to a number of risks, including fluctuations in demand for shipping, changes in charter rates, and changes in fuel costs. It is also affected by the global economy and the strength of the US dollar.

In the last year or so, there have been unprecedented macro events with a big impact on NMM:

- Central banks have been reducing liquidity in the financial system as they normalize balances. At the same time, interest rates are rising to combat inflation.

- China is the largest consumer of raw materials and produce. Their focus on zero COVID policies has caused slower economic growth and reduced their appetite for goods.

- The conflict in Ukraine has disturbed normal trading patterns for oil and gas. It has also created a scarcity of grains and mineral commodities.

NMM Fleet Description

Dry Bulk Vessels: 185 vessels with a carrying capacity of 16.5 million DWT. The average age is 9.5 years. Some of the vessel types are:

- Capesize: Largest dry bulk marine option with a carrying capacity between 170,000 and 190,000 DWT. They are too large to use the Suez Canal or the Panama Canal. Capesize vessels are mainly used to transport coal, iron ore and commodity raw materials between Australia and China or between Brazil and China.

- Panamax: Vessels with size limits 75,000 to 93,000 DWT which allows them to use the Panama Canal. Primarily used to transport products in the Caribbean and Latin America.

- Ultra-Handymax: Medium sized vessels with a carrying capacity of 58,000 to 65,000 DWT.

- Handymax: Can carry between 35,000 and 48,000 DWT. They have five cargo holds and four on-deck cranes which make them popular for unloading cargo in ports that do not have sophisticated infrastructure.

{kind=link}

Corporate Governance Issues

NMM has been the subject of corporate governance concerns in the past. One of the main issues is related to the ownership structure of the company.

About 10% of NMM's shares is owned by Navios Maritime Holdings Inc ( NM ) which is controlled by Angeliki N. Frangou also known as AF. This has led to concerns about potential conflicts of interest between NMM and NM.

Another governance issue is related to the composition of the board of directors. Shareholders have complained about the lack of independent directors on the board and the potential for the board to be dominated by individuals with close ties to Ms. Frangou. Another issue is that the company has had a history of late filings of financial reports.

Most shareholders understood why AF slashed the NMM quarterly dividend from $0.30 to $0.05 back in August, 2020 because of Covid19. But then the company became highly profitable, and the dividend was not restored.

Instead of this, AF did some dilutive equity raises for acquisitions to bail out her other near bankrupt companies- NNA and NMCI. These consolidation acquisitions may work out over the long term, but have annoyed many shareholders that are still unhappy about the large distribution cut in 2020.

With the more recent $835 Million NM deal, there was no share dilution, but NMM had to assume $441.6 Million of bank liabilities, bareboat obligations and leasing obligations. The 36 new vessels should help the company longer term, but the need to "repair" the balance sheet will delay share buybacks or potential dividend increases.

But to be fair, it is worth pointing out that NMM has also taken some steps to address governance issues. They have adopted a corporate governance framework to promote transparency, accountability, and ethical behavior. They also have a code of conduct and a policy on related-party transactions which are designed to minimize the potential for conflicts of interest.

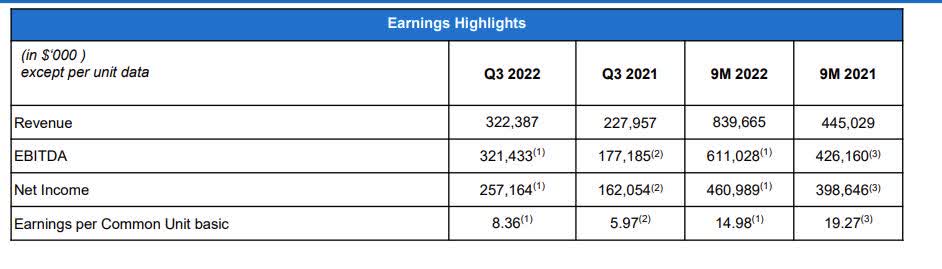

NMM- Recent Earnings

{kind=link}

{kind=link}

NMM Trades at a Huge Discount to NAV

In their last earnings presentation in November, NMM reported a gross fleet value of $5.04 Billion and a net fleet equity of $2.9 Billion which is equivalent to an NAV of about $100 a share. NMM currently trades near $25 which is about a 75% discount to NAV.

The average analyst EPS estimate for 2023 is $19.60 a share which implies a forward P/E ratio of only 1.32.

NMM is likely one of the cheapest deep value stocks available in the stock market today. There are a number of reasons for this, which include:

- Corporate governance issues

- Volatility of shipping industry

- Recent selling caused by potential tax changes for non-US investors

- Low dividend yield of 0.78%. Investors are concerned they will never get the dividend restored back to pre-Covid levels.

- Significant debt

NMM Tax Treatment

Even though NMM is a limited partnership, it has elected to be treated as a 'C' corporation for US tax purposes. Investors receive a Form1099-DIV and not a Schedule K-1. Because of this, it is not subject to section 1146 as that section only applies to entities that are characterized as partnerships for US federal income tax purposes.

The IRS recently introduced new regulations under Section 1446(f) regarding publicly traded partnerships (or PTPs) held by foreign persons. The withholding requirements under the new regulations went into effect on January 1, 2023 and has impacted these non-US investors in the following ways:

- Starting Jan. 1, 2023, brokers will withhold 10% of gross proceeds from sales of PTP securities and certain distributions by PTPs.

- Transactions and the related tax will be reported on Form 1042-S.

- The new PTP withholding tax is separate from the existing 37% withholding for individuals and 30% withholding for entity accounts on payments of US source dividends and income related to PTP securities.

US investors are unaffected by this legislation. I do not believe the legislation should apply to NMM, since it is treated as a "C" corp for tax purposes. But it has had an impact on some non-US investors in NMM who may have been forced to sell their shares. Some brokers in Europe may have over-reacted to the legislation and wanted to play it safe for compliance reasons. For example, Citibank recommended that all non-USA clients sell out of PTP securities like NMM, even though it is a "C" corp for tax purposes. Here is the letter sent to non-US clients who own NMM:

Impacts to non-US residents from changes to Publicly Traded Partnership regulations

We have recently been advised by Citi that the U.S. Treasury Department, and the Internal Revenue Service ((IRS)) released final regulations relating to Publicly Traded Partnerships ((PTP)).

The rules apply to sales, exchanges, or other transfers (for consideration) occurring on or after 1 January 2023. These new PTP regulations introduce significant withholding tax consequences for non-U.S. residents, in addition to expanded withholding and reporting burdens for withholding agents and intermediaries.

In essence, we understand this will result in an additional 10% withholding tax on income and a straight 10% withholding tax on any sales proceeds.

You are currently a holder of Navios Maritime Partners LP ((NMM)) which, according to Citi, is deemed a PTP security, which from 1 January 2023 will be subject to the regulations and associated additional withholding.

I believe that a lot of the weakness in the NMM stock price has been caused by selling from foreign investors who own NMM. I even heard that some smaller brokers in Europe actually forced people to sell stocks like NMM because they may have wrongfully added it to a US MLP list.

A Share Buyback of $100 Million Has Been Authorized

In July, 2022, NMM bailed out debt-laden former parent NM in a $835 million deal to buy 36 dry bulk carriers. Some NMM investors were unhappy about this transaction. MRMP Managers LLC had previously sent a letter to NMM sharing their concerns regarding the management of the company:

"While we are only holders of LP interests in NMM, we have serious concerns regarding Angeliki’s decisions that seem designed to benefit other entities in the Navios group. We believe these decisions run counter to her duty as Chairman & CEO of NMM."

But there was also some good news for shareholders. The company announced a $100 million common unit buyback program. But they said that near-term utilization of the program is likely to remain limited since cash would have to be replenished first.

In the last earnings call on November 10, an analyst asked if management would be using any free cash flow for the buyback program. Angeliki Frangou responded:

"We adopted the buyback because we wanted to have the flexibility. Yes, of course, because of macro certainties that we saw and the balance sheet consideration – that balance sheet considerations, we have not put it in that yet, but it’s something that we are looking. This is about Navios concentrating on total returns. This is a very important thing and the decision of how we return to our shareholders, it depends on the value. But we are – this is something that we adopted because we wanted the flexibility to use it."

Will The Big Discount Ever Be Reduced?

There are a number of ways the company can use its ample free cash flows to decrease the large discount to NAV:

1) Aggressively buy back the NMM common shares

This is probably the best outcome for investors since it would be highly accretive to NAV, and ease concerns about corporate governance. By reducing shares outstanding, it would also decrease the cost of large dividend increases in the future.

2) Increase the quarterly distribution

A large dividend increase would likely cause a "pop" in the stock price and could bring back many yield oriented investors. But as a total return investor, I prefer the buyback route because reducing share count has longer term benefits. In a taxable account, you have taxes to pay on any distributions.

3) Change the ship management operations from external to in-house

There have been some concerns that NMM management may be charging above average management fees, although I believe the fees are more or less in line with the industry averages. A move to internal management could reduce fees somewhat and alleviate some of the corporate governance concerns.

4) Pay off debt, especially the floating rate debt

This is probably the place where much of the free cash flow will go in the short term. Angeliki spoke about balance sheet considerations in the last conference call. Reducing debt does have the benefit of reducing the risk profile of the company, and could help to bring in more institutional money. Paying off some of the higher cost floating rate debt is probably the most beneficial.

I believe that Angeliki Frangou will try to improve her reputation with shareholders over the next few years. She will never be viewed like Warren Buffett. But I think she is trying to improve the image of NMM and get a new shareholder base that is oriented more toward total returns. She has recently sold off some older ships which will reduce her management fees. This is shareholder friendly since selling older ships at or above NAV can be highly accretive.

With the passage of time, and some share buybacks and more debt repayments, I think the stock can easily go from 25% NAV to 70% NAV. If earnings also do well, there is room for significant stock appreciation. I don't expect a dividend increase right way, but that is certainly possible in 2024.

Ways to Invest in NMM

Income oriented investors may not be attracted to NMM right now, because its dividend yield of 0.78% is quite low. But there are option contracts available on NMM which allow you to earn a significantly higher yield.

One approach is to sell a cash-covered put. The NMM $25 put maturing on March 17 traded at $1.51 on Friday. You need $2500 cash to cover 100 shares of NMM or 1 put. You receive the $1.51 right way, so your cost basis if you get assigned on the put is $25.00 - $1.51= $23.49.

If you are not assigned on the put because NMM stayed above $25 on the expiration date, you get to keep the $1.51 put premium. So your rate of return would be $1.51/$23.49 or 6.42% in two months.

Another approach is to buy NMM and to sell a covered call at $30 or $35 against the shares. This provides extra income and some downside protection. But you lose the stock, if NMM rises above the call exercise price at expiration. The options are not very liquid, but it doesn't hurt to enter limit orders to sell the call options at attractive prices.

For further details see:

Navios Maritime Partners Has Corporate Governance Issues, But One Of The Best Values Available