XIACY - Navitas: Investors Are Overlooking This Significant Risk

2023-06-29 09:37:07 ET

Summary

- The Navitas stock is trading near its all-time high, benefitting from investors' optimism over its growth prospects, alongside the incremental boost from AI momentum across the broader semiconductor peer group.

- The stock now trades at about 21x estimated sales, joining only a handful of peers, including industry leader Nvidia, with such an elevated premium.

- Yet, there is one immediate significant risk that could alter optimism over Navitas' fundamental outlook, which market might have underappreciated.

Navitas ( NVTS ) represents one of the biggest gainers amid this year’s broader market rally, more than doubling its value in the last six months (+143% YTD). It is also currently one of the most expensive stocks in the semiconductor sector and broader tech industry, trading at close to 21x estimated sales (putting into perspective, Navitas is one of a handful of other semiconductor stocks that trades at the 20x range, including Nvidia / NVDA ).

Specifically, the fabless power semiconductor company has been a key beneficiary of both longer-term secular demand trends, as well as easing supply chain bottlenecks this year across core verticals, which have together helped offset its exposure to persistent headwinds from the extended slump in the PC and other consumer electronics end markets. Solar and energy storage, as well as EVs have been Navitas’ strongest growth verticals this year, especially as the transition to electric in the transportation industry remains resilient despite impending recessionary headwinds.

Specifically, Navitas’ core power hardware offerings – namely, gallium nitride- (“GaN”) and silicon carbide-based (“SiC”) power devices – represent about $300 of content per EV. And as EV adoption continues to gain momentum, Navitas faces favourable long-term growth trends in the vertical – EV sales are expected to jump 35% this year, while total new car sales worldwide are expected to expand in the lower single-digit range over the same period given a “downbeat outlook for the global economy”. Meanwhile, management is also expressing cautious optimism over the pace of recovery in its core mobile end market through the remainder of the year, buoying market confidence in the stock.

The mobile market seems to be bottoming and starting to recover in Q2. And, in general, our overall customer engagement and activity continues to expand.

Yet, while investors remain confident in Navitas’ growth prospects, the stock’s elevated valuation likely represents the market’s mispricing of risks pertaining to the company’s China-concentrated operations, especially amid escalating geopolitical tensions and a slow post-pandemic recovery in the region. Paired with persistent losses, stemming primarily from elevated R&D spend as Navitas remains in the process of scaling operations, both the stock’s lofty valuation premium at current levels and outsized market optimism over the underlying business’ growth prospects lack durability, especially amid persistent deterioration of macroeconomic conditions.

Navitas’ China Exposure

Navitas is most notably known for their proprietary design and provision of power semiconductor systems (i.e. GaN- / SiC-based hardware) for solar / energy storage, mobile / consumer electronics, EVs, home appliances / industrials and data center applications. China sales currently represent Navitas’ biggest source of revenue, accounting for close to 40% of the company’s full year 2022’s consolidated mix, and close to 60% of the first quarter’s consolidated mix, in line with historical trends. Key customers include Lenovo ( LNVGY / LNVGF ) and Xiaomi ( XIACF / XIACY ) – both of which are China-headquartered companies, with upcoming product launches incorporating Navitas’ technology.

In addition to sales, the fabless chipmaker also relies on contract manufacturers located across Asia – primarily TSMC ( TSM ), Navitas’ core wafer fab partner for GaN-based power devices. While TSMC has been looking to diversify its global manufacturing footprint beyond its base in Taiwan amid escalating Washington-Beijing geopolitical tensions, related investments have been focused on process technologies for advanced high-performance computing chips rather than power semiconductor productions. Specifically, the diversification of GaN production capacity beyond Taiwan is unlikely to be a priority for TSMC within the foreseeable future given the vertical remains a nominal contributor to the foundry’s consolidated sales mix. This is further corroborated by the importance of Navitas’ volumes to TSMC as disclosed in the company’s latest 10K filing, albeit likely immaterial to the foundry’s broader business exposure in chip manufacturing considering Navitas’ annual revenues in the millions:

Although we have no volume-contacted commitments with TSMC, and work on the basis of purchase orders, our volumes of GaN products in TSMC wafer fabs are critical to the utilization and efficiency of TSMC’s GaN-specific infrastructure.

Source: Navitas 2022 10K Filing

Shaky Macroeconomic Backdrop

One of the most prominent China risks facing Navitas is its exposure to the region’s faltering post-pandemic recovery trajectory. Recall that Navitas is expecting to double its current year revenue from prior year levels. With 1H22 sales expected to forge sub-100% y/y growth (1Q23A: +98% y/y; 2Q23E: +86% y/y to +97% y/y), Navitas’ guidance implies acceleration in the second half.

However, the demand environment in its core China market is becoming increasingly uncertain as recent economic data points to a post-pandemic recovery that is rapidly losing steam amid “weak business and consumer confidence , a faltering property market , and slowing global demand for exports”. And cautious investors’ sentiment over the situation can be corroborated by tepid valuation gains across U.S.-listed Chinese stocks in recent months, as previous optimism over the reopening trade ends in disappointment . China’s economic weakness amid stringent COVID-Zero restrictions enforced through 2022 had already been an acute challenge to Navitas’ mobile end market, and persistent deterioration to the demand environment ahead risks a repeat of the slowdown that could temper management’s optimism for a 2H recovery.

Back to your other question on the mobile handset market, I still think we lost a bit of time in the last year with the slowdown, namely in China, but even more broadly in mobile.

Specifically, management’s cautious optimism that weakness in the mobile end market has bottomed and is poised for a consistent pace of recovery through the remainder of the year, driven primarily by observations of backlog growth during the first quarter, might have been premature. Smartphone shipments across China remain well below prior year and pre-pandemic levels. Volumes declined 12% y/y during the first quarter. And despite a recent 23% jump observed in May, total smartphone shipments in the region since January remain close to 3% down from the same period last year amid country-wide lockdowns and nominal economic activity. The bleak outlook is further corroborated by other smartphone component suppliers, such as Sony ( SONY ), which recently warned of persistently elevated handset inventory levels through the remainder of the year.

And regarding [the] smartphone market situation. Regarding China, we are not optimistic. If we look at the logistical inventory levels in the fourth quarter at around February, it went down slightly but in March it went up again. So we believe that we should not be optimistic.

Similar concerns were present based on Xiaomi’s – one of Navitas’ key mobile / consumer electronics customers – first quarter results, which were accompanied by a 19% y/y revenue decline “in a reflection of crumbling demand for electronics and internet services in a sputtering Chinese economy”. Industry research estimates a “23.5% drop in Xiaomi handset shipments during the first quarter”, with the company likely boasting the highest inventory levels amongst smartphone vendors worldwide. While Navitas’ power technologies were incorporated in Xiaomi’s recent launch of its namesake 13 Pro and Ultra smartphones earlier this year, weak take-rates suggest continued headwinds to Navitas’ near-term demand environment.

Meanwhile, on the PC side, shipments in China remain in a slump, dropping by almost a third y/y during the first quarter. Weak business and consumer sentiment, as shown in recent economic data discussed in the earlier section, has driven a 27% y/y decline in commercial PC take-rates and 21% y/y decline in consumer PC take-rates, with related outlays likely to stay on hold for a while given “evolving macroeconomic uncertainties”.

The weak outlook is consistent with weak first quarter results at Lenovo – another key customer for Navitas – which is grappling with its third consecutive quarter of revenue declines, dragged primarily by soft PC demand. Although the broader PC supply chain – spanning chipmakers to workstation OEMs – have been expecting a 2H recovery, ongoing uncertainties in the Chinese demand environment risks thwarting such optimism. With economic uncertainties in Navitas’ China market still running at large, the timeline for realizing such backlogs into revenue is now potentially pushed further out into the future, which also risks derailing the company’s near- and longer-term fundamental targets, such as expanding gross margins to the mid-40% range by year-end, and achieving operating breakeven on quarterly revenue of $50 million by late 2024 / early 2025.

Uncertain Geopolitical and Regulatory Environment

In addition to macroeconomic headwinds, Navitas’ China-concentrated operations also exposes the company to greater geopolitical and regulatory risks, in line with considerations outlined in its latest 10K filing:

Further, our sales may be adversely affected by the current and future political environment in China and the policies of the China Central Government. China’s Central government has exercised and continues to exercise substantial control over nearly all sectors of the Chinese economy through regulation and state ownership. Our ability to ship products to China may be adversely affected by changes in Chinese laws and regulations, including those relating to taxation, import and export tariffs, raw materials, environment regulations, land use rights, property, and other matters…Any changes in United States and China relations, including through changes in policies by the Chinese government could adversely affect our financial condition and results of operations…”

Source: Navitas 2022 10K Filing

The semiconductor sector has faced the brunt of geopolitical tension-driven regulatory changes this year. Related impacts started off with Washington’s curbs on exports of advanced semiconductor technologies to China late last year. And in the latest development, Beijing has responded with a cybersecurity probe in Micron Technology ( MU ), with unspecified findings related to “ serious cybersecurity risks ” identified in the memory chipmaker’s products now affecting as much as 13% of its revenue.

While the latest regulatory changes for the sector impacts primarily advanced technologies used in critical computing infrastructure and less so on broadly used components like power semiconductors, reflecting the governments’ means to protect their respective national security interests amid escalating geopolitical tensions, Navitas remains exposed to ensuing secondary implications to its business. For instance, Micron is currently a key supplier of memory chips for Lenovo workstations, and the recent regulatory changes could impact the PC maker’s output volumes and, hence, orders from Navitas. Lenovo is also championed by China’s state agencies and is a key vendor for government workstations and equipment; hence, its potential exposure to cybersecurity risks identified in certain Micron components, for instance, could also impact sell-through volumes and, inadvertently, demand for Navitas’ power components.

Meanwhile, recently observed regulatory impacts on advanced semiconductor technologies also do not preclude further tightening of rules surrounding the broader sector, which means Navitas’ concentrated sales in China remain directly exposed to related risks as well – especially as the company looks to deepen its reach into data center opportunities amid rising interest in AI and ensuing power requirements. Specifically, Navitas is currently in the process of preparing to ship its “new high powered GaN ICs” for data center application in the fourth quarter, as well as continued R&D on the recently announced “ Gen-5 SiC diodes ”. The developments will be critical to expanding its volume of development projects for the data center end market, and growing the vertical’s revenue pipeline beyond $60 million. Navitas estimates a $1 billion TAM for GaN ICs in the data center end market, stemming from the transition away from incumbent silicon-based data centers that are less energy efficient, especially as increasingly complex workloads become more power demanding.

Nearly 50% of the total cost of ownership of a data center is related to power, which includes the cost of power supplies as well as the cost of electricity for data processing, cooling, lighting and other power needs…a silicon-based data center today is about 75% efficiency, implying 25% of the energy used by a data center is wasted as heat. A GaN-based data center can improve efficiency to about 84%...representing benefits in reduced cost of electricity and the cost of cooling. Based on our analysis, approximately $1.9 billion in electricity could be saved each year if all data centers moved to GaN.

Source: Navitas 2022 10K Filing

And Navitas is likely well-positioned for accelerated market share gains in the vertical given its lower total cost of ownership (“TCO”) advantage via the provision of GaN ICs optimized for data center application, as well as an “overall bill of materials cost lower than legacy silicon”. However, with much of its sales concentrated in the Chinese market, and stiffening regulatory and geopolitical headwinds over the data center end-market (e.g. cloud, AI, internet of things, data, high-performance computing, etc.), Navitas’ aspirations to expand its market share in the related vertical faces budding execution risks in our opinion.

Valuation Considerations

Navitas currently trades at approximately 21x estimated sales, with much optimism priced into the stock for the underlying business’ growth prospects as it continues to scale.

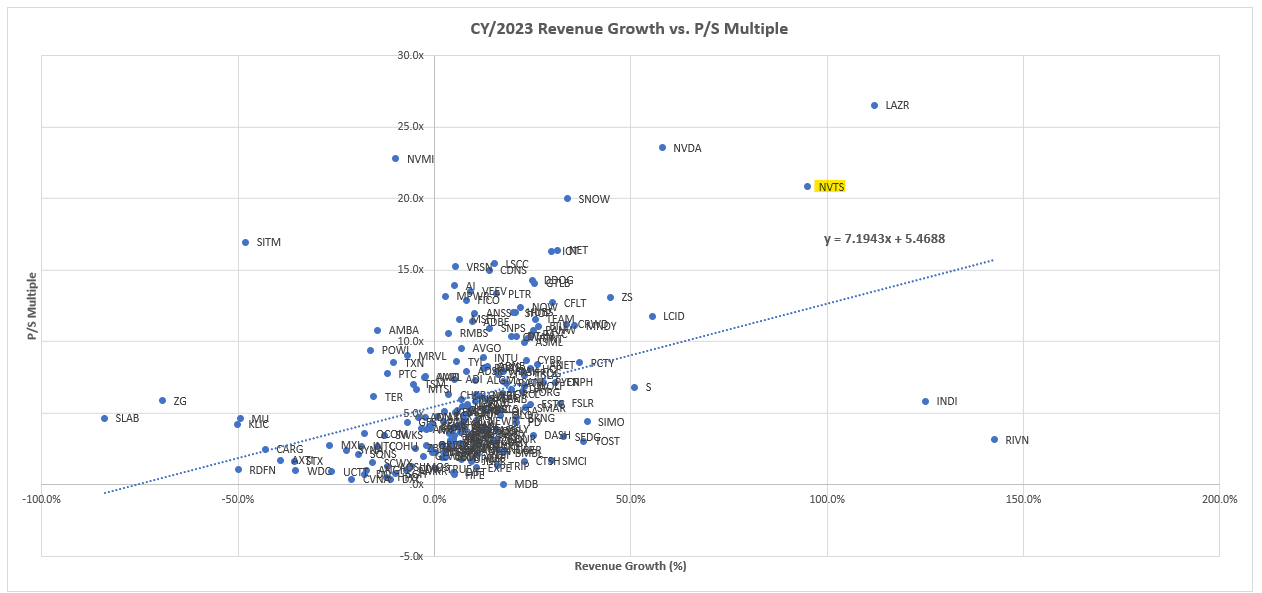

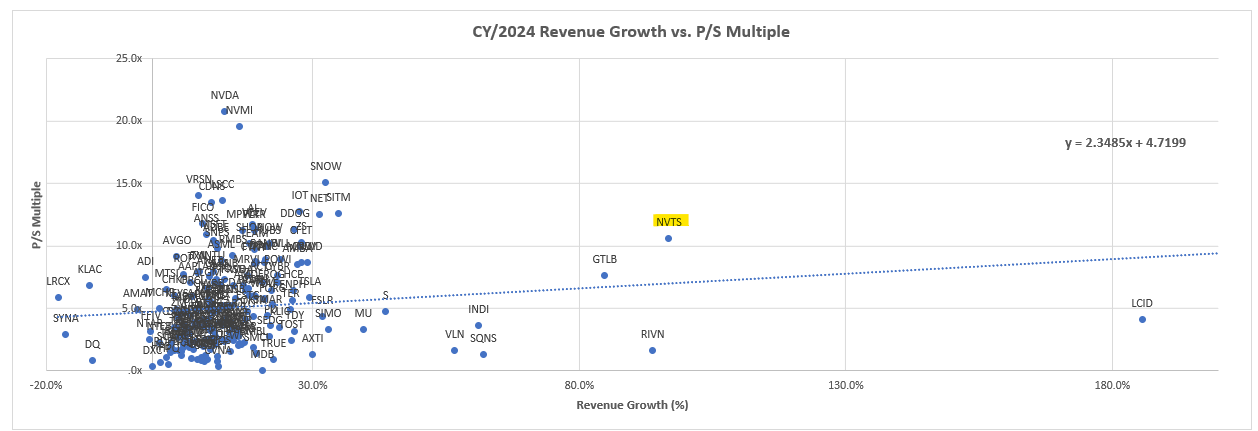

i. Sales Growth vs. P/S Multiple – Technology

Author, with data from Seeking Alpha Author, with data from Seeking Alpha

{kind=link}

{kind=link}

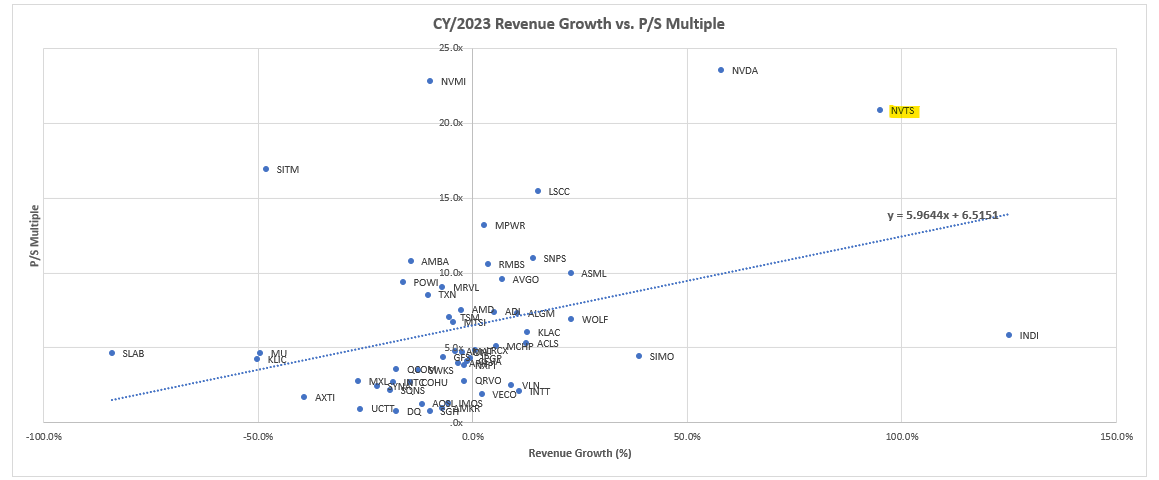

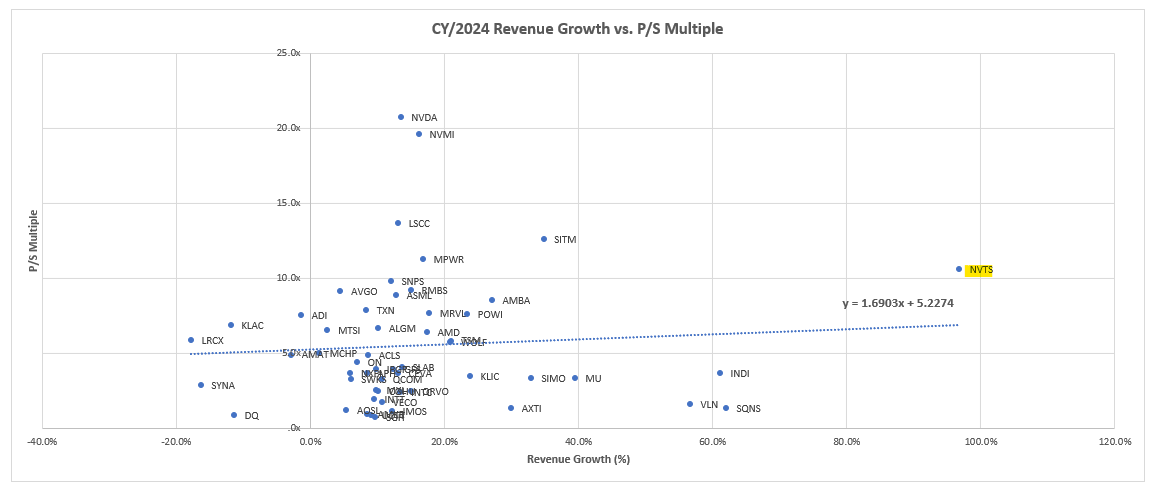

ii. Sales Growth vs. P/S Multiple - Semiconductors

Author, with data from Seeking Alpha

{kind=link}

Author, with data from Seeking Alpha

{kind=link}

The Navitas stock has likely benefited from burgeoning market interest in AI this year as well, riding on the coat-tails of related market tailwinds that have largely overshadowed the underlying business’ exposure to China-related risks (cue Nvidia, whose AI prospects have defied concerns over near-term regulatory and geopolitical concerns). While Navitas remains optimistic about the incremental demand for power chips stemming from the rapid adoption of AI technologies, the company has yet to see an immediate impact on its P&L from interest in the emerging field unlike peers engaged in accelerated computing solutions like Nvidia and AMD ( AMD ).

I also think this [data center] pipeline is not really reflecting what’s going on in the market today around generative AI. I think, we’re just scratching the surface on the potential applications and market implications of that technology and the massive data consumption that’s going to go with it, which leads to a massive power consumption, which we’re going to see in coming quarters, I believe, certainly coming years, to create a big power problem, which is a big power opportunity for Navitas. So that’s a bit on the medium to long term.

Essentially, the company expects AI-related tailwinds to materialize for its business over the medium- to longer-term, leaving room for significant uncertainties and execution risks, which effectively draws concerns over the durability of immediate valuation gains observed in the stock at current levels. This is further corroborated by Navitas’ nominal backlog (< 8%) from the data center vertical relative to the broader business’ $760 million revenue pipeline acquired to date:

In electric vehicle…we have strong momentum in shipments, backlogs and pipeline with over 25 customer projects either shipping with silicon carbide or in development with GaN and silicon carbide, and a total revenue pipeline of over $300 million…In solar and energy storage, we have strong momentum in shipments, backlog and pipeline with over 35 customers in production or in development, and a total revenue pipeline of over $150 million…In home appliance and industrial, we have over 45 customers in production or development and a revenue pipeline of over $150 million…In data centers…[we] have increased our customer development projects to 15, representing a revenue pipeline of over $60 million…In mobile, we have over 150 customer projects in development with a revenue pipeline of over $100 million.

More importantly, we believe Navitas’ valuation premium reflects market’s mispricing of immediate China risks facing the underlying business, which could potentially offset some of the near-term growth tailwinds that investors had been (potentially overly) optimistic about. Take for instance Micron – the stock’s battered valuation over the past year due to persistent cyclical headwinds was further exacerbated by its exposure to incremental geopolitical and regulatory risks earlier this month. As such, we remain incrementally cautious about similar China headwinds – spanning macroeconomic, geopolitical, and regulatory uncertainties – facing Navitas’ fundamental and valuation prospects ahead, as they represent multiple compression risks to the stock.

The Bottom Line

Admittedly, markets could have overlooked China-related risks facing Navitas, given the company’s technology is not yet widely exposed to critical infrastructure applications prone to national security risks. Yet, the company remains exposed to the indirect impact of related risks within the immediate-term as discussed in the foregoing analysis, which could have adverse implications on its longer-term growth and profitability roadmap – including barriers to Navitas’ ambitions in deepening its reach in the emerging AI and data center growth frontiers.

Meanwhile, on the fundamental front, we also remain incrementally cautious over the implied 2H reacceleration based on management’s full year guidance of doubling sales growth at Navitas, given a faltering post-pandemic economic recovery in China, the company’s biggest revenue driver. Taken together, we remain skeptical over the durability of the stock’s lofty valuation premium at current levels, with this year’s eyewatering rally likely prone to impending downside risks in the near-term to adjust for anticipated demand deterioration – especially in Navitas’ core China market – amid persistent global macroeconomic uncertainties.

For further details see:

Navitas: Investors Are Overlooking This Significant Risk