NBXG - NBXG: Discount Deepens Further

Summary

- NBXG's discount has widened since our last update, presenting an even more interesting time to consider the fund.

- While there are significant headwinds and tech-tilted funds might not be completely out of the woods yet, there have been some signs of stability.

- At the same time, the fund relies on capital gains to fund its distribution; with those lacking, the outlook for maintaining the current distribution would be cloudy.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on January 26th, 2023.

Neuberger Berman Next Generation Connectivity Fund ( NBXG ) is a fairly unique fund with a heavy tech emphasis. They aren't solely dedicated to the tech sector, but it consumes an overweight portion of their portfolio. With the fund coming to market in mid-2021, it came in just in time for the tech/growth collapse that we've experienced in the last year and a half or so.

However, the fund presents several attractive points that an investor could consider. The fund isn't your usual closed-end fund holding a lot of familiar names. In that way, they can provide investors with added diversification. Of course, that's if you are interested in the type of underlying portfolio that NBXG offers. Diversifying for the sake of diversifying isn't a good strategy on its own.

The other reason one might consider this fund is due to the massive discount that has opened up in this fund. We are near the lowest of the low points in terms of discount as it breaches the 20% level. At the same time, we've seen the declines stop, and there appears to have been some stability since we hit the lows in October. If this stability continues, and most of the tech wreck is behind us, NBXG offers an interesting opportunity.

Since our last coverage near the beginning of September, we can see that stability playing out. I've also included the S&P 500 SPDR ( SPY ) for some context, although that isn't an appropriate benchmark.

Ycharts

The Basics

- 1-Year Z-score: -1.09

- Discount: -20.32%

- Distribution Yield: 12.20%

- Expense Ratio: 1.30%

- Leverage: N/A

- Managed Assets: $972 million

- Structure: Term (anticipated liquidation date of May 26th, 2033)

NBXG is a "non-diversified, limited-term closed-end management investment company focused on next-generation mobile network connectivity and technology." They have no focus on U.S. or non-U.S. companies - instead, they are investing where they see fit. This also includes any market cap and private holdings.

Although, they do limit themselves to mostly equity investments. Given the volatility of equity positions in the field that they are investing in, it makes sense that they also don't intend to utilize any leverage. When interest rates rise, that is one less thing to worry about with this fund.

With other CEFs that are leveraged, the borrowing costs on these funds have been exploding to 5%+. We could see that move even higher with at least a couple more interest rate increases from the Fed. So, considering funds that aren't leveraged in this environment isn't necessarily bad.

Performance - Deep Discount

One of the things I noted in our prior update was that the fund's discount was near the end of the bottom range. Although this fund doesn't have a long history, getting a good sense of where this fund will trade is more difficult. That being said, NBXG proved to me that despite the discount stabilizing, the market was ready to discount the fund even further.

We have made a new all-time wide discount level. The fund bounced off of that relatively quickly but has then once again been trending to a wider level.

Ycharts

I still believe this represents a fairly attractive time to consider the fund. In fact, an even more attractive time, considering I believed a ~16.5% discount was attractive previously.

NBXG isn't alone in its poor performance. As a reminder, CEFs are only merely a wrapper for other assets and not an asset themselves. To provide some more context on how the fund has done since its launch, I've added several different 'benchmarks.'

That includes comparing with BlackRock Science and Technology Trust II ( BSTZ ) and ARK Innovation ETF ( ARKK ). These two are particularly relevant because, along with NBXG, they invest in some of the newest tech names that worked incredibly well in 2020/early 2021. However, it is the names that came down spectacularly in 2022. BSTZ is also almost entirely focused on tech, whereas NBXG carries exposure to other sectors as well.

Along with those, I've also included SPY again and Technology Select Sector SPDR ( XLK ). I've included XLK because it represents the more traditional larger and mega-cap tech names. It can highlight the big performance difference between old tech and new tech.

Ycharts

Distribution - A Cut Is Possible

NBXG has maintained the same $0.10 monthly distribution that it has had since its launch. However, closed-end funds can essentially pay out whatever they'd like until NAV reaches $0. This is because a fund can pay distributions classified as income, gains or return of capital.

Not all return of capital is bad; there can be reasons why ROC is present in a distribution for good reasons. It can also be beneficial for taxable accounts. However, in this case, with no embedded gains built up previously, it would be considered destructive ROC.

There simply wasn't time in this fund's life when material gains were possible due to the timing of the launch. That resulted in the entire distribution being classified as ROC in 2022 - with a significant portion of ROC classified in 2021 as well.

NBXG Distribution Tax Classification (Neuberger Berman)

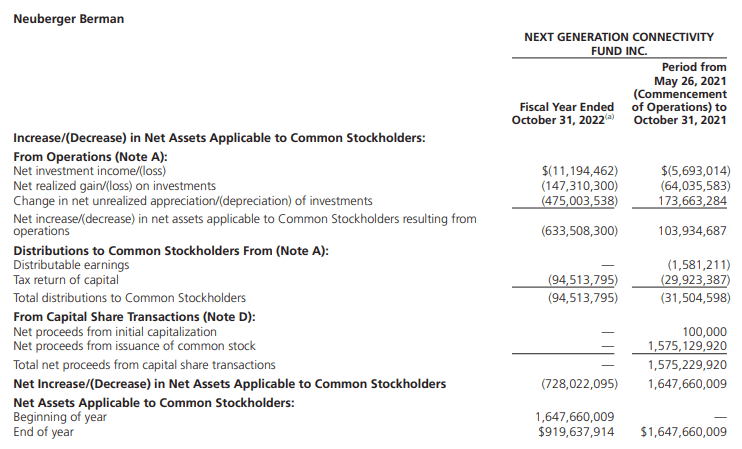

As we can see from their last annual report, the fund generated no net investment income. That isn't uncommon since most of their underlying holdings don't pay dividends. On top of this, we can see the significant unrealized and realized losses the fund accumulated.

{kind=link}

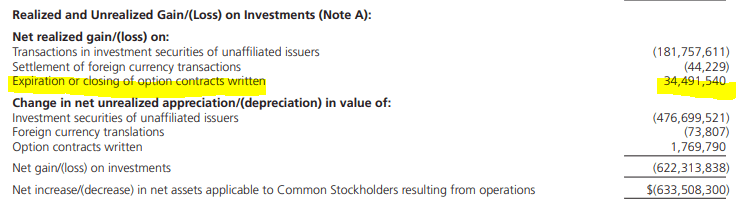

There is one silver lining here in this fund, though. The fund employs an options writing strategy. Their efforts produced nearly $34.5 million in realized gains. While it wasn't nearly enough to cover the distribution or turn the realized losses into realized gains, if those profits wouldn't have been there, it would have been an even worse outcome.

NBXG Option Writing (Neuberger Berman (highlights from author))

{kind=link}

For these reasons, I wouldn't be overly surprised if they announced a distribution cut. So while the distribution yield comes to 12.20% and a NAV rate of 9.72%, I wouldn't bank on that distribution being maintained in perpetuity.

NBXG's Portfolio

These are some busy managers, as the portfolio turnover rate for the 2022 fiscal year came to 103%. For the partial fiscal year of 2021, it was an elevated 81%. They're clearly moving around underlying holdings quite frequently. Unfortunately, with the focus on growth investments, there really wasn't anywhere to hide. Thus, the weak performance we experienced with the fund.

Since our last update, tech exposure has come down some but still remains a massive part of their portfolio relative to any other exposure. It had previously been a 63.7% allocation. Interestingly, they break out private/restricted into their own sector. That part of the pie has ticked up some from the prior 15.6% weighting listed.

NBXG Sector Breakdown (Neuberger Berman)

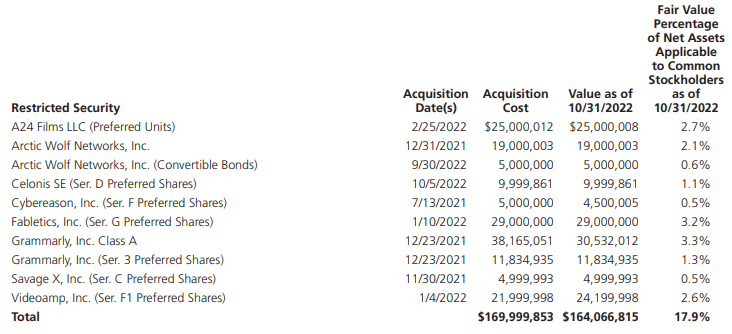

With private investments, there is always a bit of uncertainty as to their valuations. That's why there will likely always be some sort of discount running on this fund. One of the problems is when it gets valued and how often, and if they are valued accurately. Here is a list of the private securities the fund was carrying at the end of the fiscal year and their valuation.

{kind=link}

Grammarly is particularly noteworthy because it is the fund's largest position, and it has been for quite some time. It appears they have taken down the valuation of the equity stake, but the preferred valuation hasn't changed a cent. In fact, you'll notice that the majority of these positions haven't had a valuation change from the acquisition cost besides Grammarly equity and Cybereason Series F Preferred.

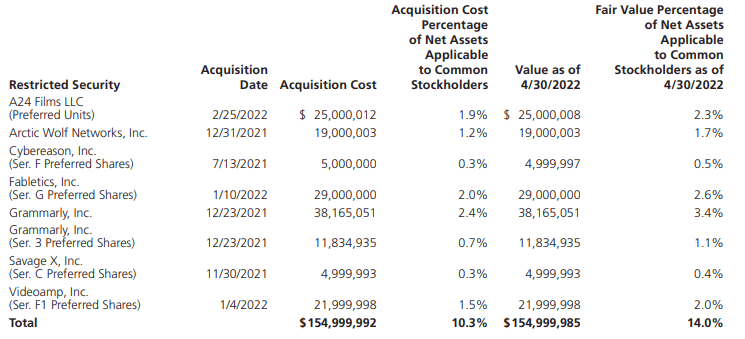

This is a recurring theme. They actually hadn't changed the Grammarly equity stake until this latest fiscal reporting in the annual report. In the previous semi-annual report, it was marked at the same exact valuation as the acquisition cost. That was despite seeing well enough evidence that the valuations of publicly traded growth/tech names were falling quite dramatically.

I would also point out the acquisition date, the acquisition cost and the value as of April 30th, 2022. Cybereason, Inc.'s position has a $3 reduction in its value, and A24 Films had a $4 reduction. The rest carry the value as the exact same for each of these investments from acquisition to the value on April 30th. That is despite the sizeable sell-off in the market between the acquisition date on most of these to the reporting period. Hence, why that "private exposure discount" seems to make a lot of sense.

{kind=link}

An investment is only as valuable as someone is willing to pay for it. So I would just say that if the NB team tried to sell me some of these restricted positions, knowing what we've seen publicly, I wouldn't be paying them the amounts they value their positions at.

Fortunately, this is a smaller portion of their portfolio, albeit not an insignificant portion though. With the excessive discount already represented, that's why I'd still find NBXG fairly attractive, as this discount should reflect some of this risk.

They also provide the market cap allocation of the underlying portfolio. While large caps are a significant portion of the portfolio, this was a significantly larger portion previously .

Instead of changing their portfolio though, I believe a good portion of the adjustments here were simply mid, and small-cap tech plays that jumped so massively in 2021 that they jumped into a new market cap category. With significant depreciation experienced in some of these names, it would have simply been some of these names falling out of the large-cap category.

NBXG Portfolio Weighting By Market Cap (Neuberger Berman)

Looking at the top ten positions, they break this down into public holdings and private holdings. As mentioned already, Grammarly remains in a significant position and retains the top spot once again.

NBXG Top Holdings (Neuberger Berman)

Looking at the portfolio more broadly, they provide helpful stats. In particular, it might be noteworthy to see the 64 public holdings and 8 total private exposure holdings. For the most part, that means it's a fairly narrowly invested portfolio.

NBXG Portfolio Stats (Neuberger Berman)

The stats presented here also show us that despite valuations coming down significantly, they are still weighted significantly toward higher-valued positions. With a forward P/E of 28.2x, that's actually climbed from the 25.7x ratio previously. In Q3,2021, this came in at a lofty 35.9x, which reflects the severity of the declines in valuations we saw in the last year.

The estimated long-term EPS growth has actually inched higher with their new mix of portfolio names, too. It had been at 24.93%. Finally, on a P/S, we also saw the portfolio inch up from 4.7x.

This still suggests that valuations in growth are commanding some quite elevated valuations, and that means we still have to see things go mostly right. With a potential recession, I wouldn't necessarily predict a quick recovery in the underlying portfolio. For a longer-term investor, it could still be an interesting time to consider this fund.

The fund starting to stabilize along with the broader market since October is also encouraging. The latest earnings we see, while not overly rosy, also show that things might not be as bad as feared. Q4 GDP beating expectations with the latest announcement is more evidence that the economy, at this point, isn't doing too terribly either. However, it was a bit of a slowdown from the Q3 GDP.

Conclusion

The fund might not experience a quick recovery, but the discount is quite attractive. I believe the discount reflects the added risk of having a meaningful sleeve of their portfolio in private investments whose valuations don't seem to change for the most part. The publicly traded names they hold are still pretty richly valued. So despite the damage done this far, we certainly aren't looking at cheap valuations necessarily in the growth space.

The significant discount is also a sign of expected headwinds. This could be especially true, with 2023 being a year we may see a recession. That would prolong the potential recovery, which means this fund is more for a long-term investor. One that is more patient could get an even better deal should economic damage start going further than originally thought.

For further details see:

NBXG: Discount Deepens Further