NCNO - nCino: A Takeover Might Be At A Not-So-Generous Valuation

2023-07-12 01:59:43 ET

Summary

- Cloud provider nCino, which offers a Bank Operating System to manage key functions within banks, is reportedly up for sale or seeking a transaction, causing a 30% jump in share price.

- Despite strong revenue growth, concerns about nCino's bottom line and changing market conditions could result in a disappointing payout per share for common shareholders in any takeover deal.

- The company's ownership structure, with Insight Venture controlling 35% of the company, could also influence the terms of any deal, with a potential price range between $22 to $35 per share predicted.

Introduction - takeover on the horizon

nCino ( NCNO ) is a cloud provider to banks and financial institutions. It offers a vertically integrated solution called Bank Operating System that manages virtually all the key functions within a bank. From loan origination to credit analysis, to customer management, this suit is able to drive the main tasks and support employees of any level with their responsibilities.

Around 3 weeks ago, on June 16, it was reported that nCino was basically up for sale or looking for a transaction. This news caused a 30% jump in the share price with expectations that an eventual takeover could happen at a generous multiple. We believe that various points suggest that any transaction would not benefit common shareholders much and that it would likely close at mediocre multiples. We think that even though nCino has a very valuable asset and suit, it also has very good reasons for a buyer to pay a relatively cheap price. Find below an in-depth analysis of the setup.

The big question: what is the multiple?

This is the big question mark every time the market deals with transactions, and most importantly takeovers. That small number defines the equity value after paying down all the creditors, and thus the payout per share that everyone is getting at closing. With respect to the case of nCino, we believe it is gonna be at least disappointing if not tremendously low.

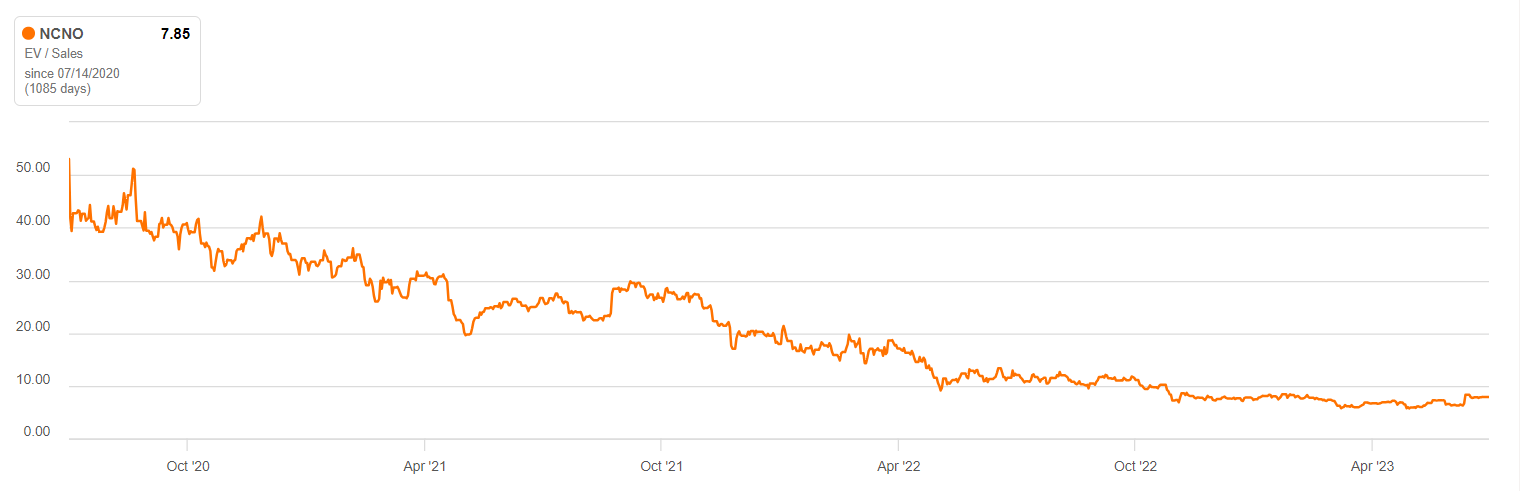

First of all, market conditions changed a lot since its IPO, and we noticed that even in the share price.

{kind=link}

nCino - EV/Sales (Seeking Alpha)

This is the great re-rate that nCino suffered. From an EV/Sales close to 50 to a sub-8 multiple. This is clearly the result of strong revenue growth in the referenced period, but also a net change in overall market conditions. The higher interest rates environment prohibits virtually any company, no matter the MOAT, to be acquired at 50 times(!) sales.

If we look at the actual multiples that the market for cloud companies experienced in the last 3 years, we actually notice some roller coasters. The pre-pandemic norm was around 8 to 9 times . Then the 2021 period changed everything, including these metrics. Some deals closed as high as 15 times sales , prompting a massive re-rate in public peers. Today, these valuations dropped below pre-covid levels at around 5.8x . This is of course a massive change that needs to be taken into consideration as a systematic change that will affect any transaction for nCino.

The real issues come from the bottom line

There is absolutely no concern about the growth path of nCino as its revenues grew consistently over the last few years. This highlights one of the most important strengths of the company: its resilience to acquire more market share, and thus eventually its MOAT. Revenue growth for this company means also a co-validation of the unique nature of its cloud platform, and its ability to keep away competition.

nCino - Revenues (Seeking Alpha)

Revenue grew almost 10 times in just 6 years and is now close to $450 million per year.

However, we are strongly concerned about the price at which this growth came. We believe that any potential acquirer, in a period of high and rising rates, would put more weight on the bottom line compared to the top line. And this is where nCino was not really able to perform.

nCino - Net Income (Seeking Alpha)

This is the development of Net Income over the same comparable period. The losses have been driven by Opex (SG&A expenses) that are apparently vital to sustain growth (given the direct correlation). And while cash losses might seem way better in theory, the reality is that they have been offset by a growing about of stock-based compensation.

nCino - SBC (Seeking Alpha)

As can be seen, SBC has been massively used since the start of the pandemic. We think that the company took advantage of the generous valuation that the market was giving to nCino, to cash in on this strength to make the losses less negative.

Takeaway on a possible transaction - what price should we expect

There is one last (but not least) consideration to make. The ownership structure of nCino.

nCino - Ownership ( Simply Wall St )

Insight Venture controls close to 35% of the company, meaning that they are the key negotiators in every kind of deal that might emerge. And so the point is, how hungry for exists are they? Which terms would they accept? This is what a recent article from June 2023 states: “ Insight Partners Slows Dealmaking Amid Tech Funding ‘Bloodbath ’”. They slashed the target for their last fund “Insight Partners has reportedly lowered the $20 billion goal for its latest fund as tech valuations continue slumping” and they just raised $2 billion. So we believe that a stake valued at $1.2 billion stuck at nCino could be an interesting source of liquidity for a struggling Insight Partners.

We provide below our own estimates of the ranges at which a deal would be possible in our opinion. We try to include the considerations for the bottom line issues, and thus a possible restructuring by the acquirer, along with the overall market conditions.

| Scenario |

| Multiple (EV/Sales) |

| Fair price per share |

| Worst case |

| 6.0 |

| $22 |

| Medium case |

| 8.0 |

| $29 |

| Best case |

| 9.5 |

| $35 |

We based these scenarios on various assumptions. For example, the best case is taking into consideration a premium multiple (almost 40% higher than the market median multiple) because of the strong MOAT. On the other hand, the worst case would be an acquirer more focused on the bottom line and the issues that affect the business - such as reliance on SBC, which is not possible as a private company. We derive a range between $22 and $35 target per share. A downside of 24% and an upside of 20%, respectively.

Conclusion

nCino is definitely a high-quality asset that has been incredibly successful i n growing its business while building a strong MOAT against competitors. Their products are essentially vital for their customers and can hardly be replaced by cheaper options. However, also in light of recent speculation over a takeover, we believe that the company is very expensive and any transaction will likely disappoint investors. We assign a hold rating and see the downside as low as 24% while the upside is capped at around 20% from the current prices.

For further details see:

nCino: A Takeover Might Be At A Not-So-Generous Valuation