NCNO - nCino: Challenged Outlook And Fully Valued

2023-07-03 14:20:40 ET

Summary

- Growth to decline from historical 30%-50% to 16%-17% in FY 2024 as NCNO faces slowdown across larger enterprise deals.

- Fundamentals are not exceptional but decent and improving.

- Downside risk remains moderate today, while the stock appears fully valued in my opinion. I rate the stock neutral.

nCino ( NCNO ) is a cloud-based platform that offers financial institutions/FIs a comprehensive platform (nCino Bank Operating System) for managing their banking operations. The platform provides functionality for various banking processes, including consumer lending, client onboarding, deposit account opening, analytics, and AI/ML.

NCNO went public in July 2020, when its share price surged from $31 at open to over $80 on the first day of trading. Since then, the share price has continued its gradual decline. It traded between the $60-$80 range in 2021 and the $20-$40 range for most of 2022. Most recently, it is trading at ~$30 per share, pretty much revisiting its opening IPO price.

I give NCNO a neutral rating. My target price model indicates that NCNO may see some small upside if it tops the highest end of its revenue guidance range. However, at $30-$31 per share today, the stock appears fully valued, in my opinion.

Risk

While NCNO appears to be a decent business with 30%-50% revenue growth and demonstrated path to profitability, growth will potentially slow down to 16%-17% in FY 2024 due to some headwinds such as project delays and churns.

I believe that there are two key headwinds for NCNO that will create uncertainties and potential downside risks this year - the first one is the lengthened sales cycle within the larger enterprise U.S. accounts. The second one is the ongoing lower mortgage activities due to the high-interest rate environment, which may continue to reduce demand for NCNO's recently-acquired digital mortgage solution SimpleNexus.

{kind=link}

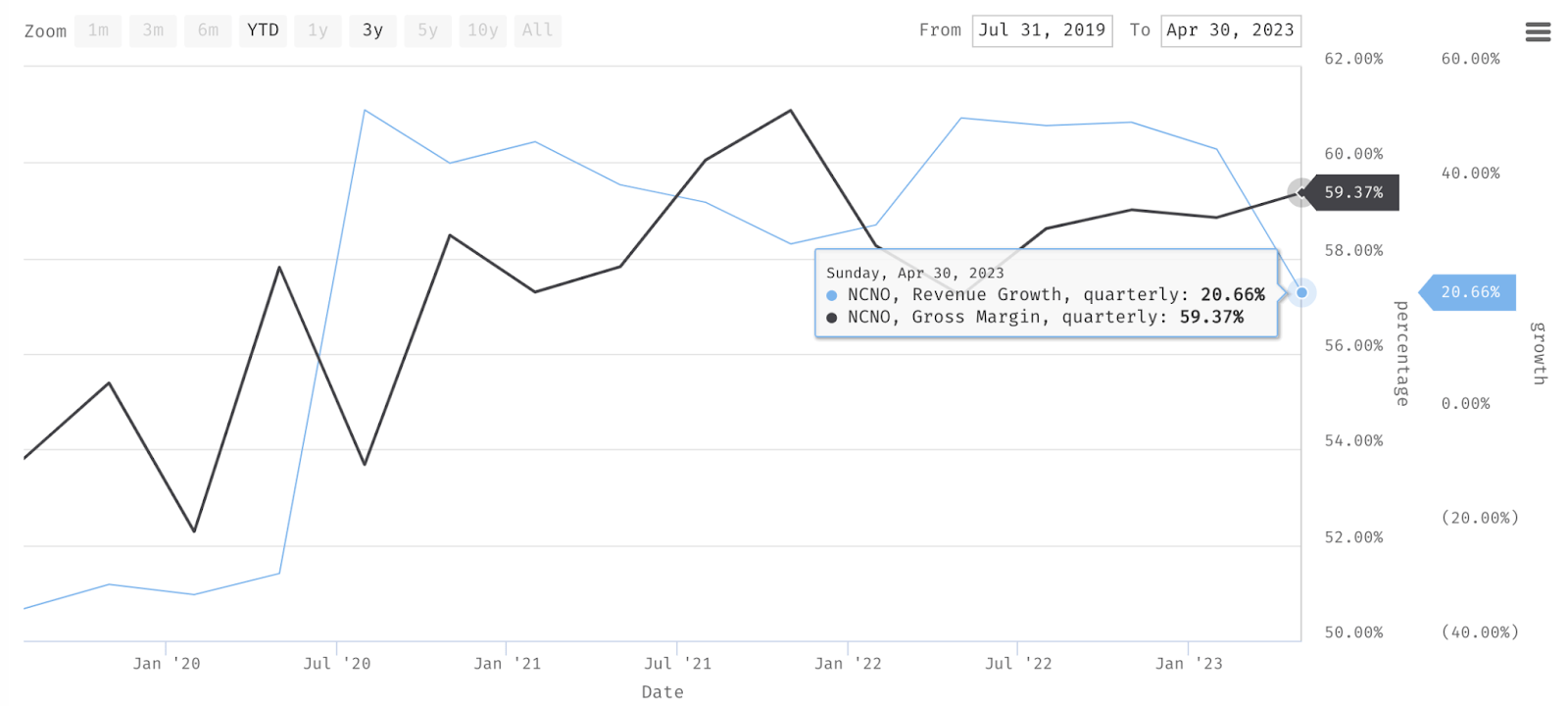

In Q1, growth decelerated to ~21%, primarily driven by the lengthened sales cycle in the U.S. enterprise customer segment with above $100 billion of assets. I feel that some of the key reasons for the current slowdown are the after-effects of the 2023 U.S. banking crisis and also the high-interest rate environment.

I can see how these two situations come together to pressure banks to tighten spending. As the management suggested in Q1, for instance, some banks have faced downward pressure on net interest margins as the competition among banks to offer more attractive deposit rates has intensified due to the high-interest rate environment. With profitability under pressure, it is sensible for banks to delay investments in large projects, such as cloud-banking transformation.

{kind=link}

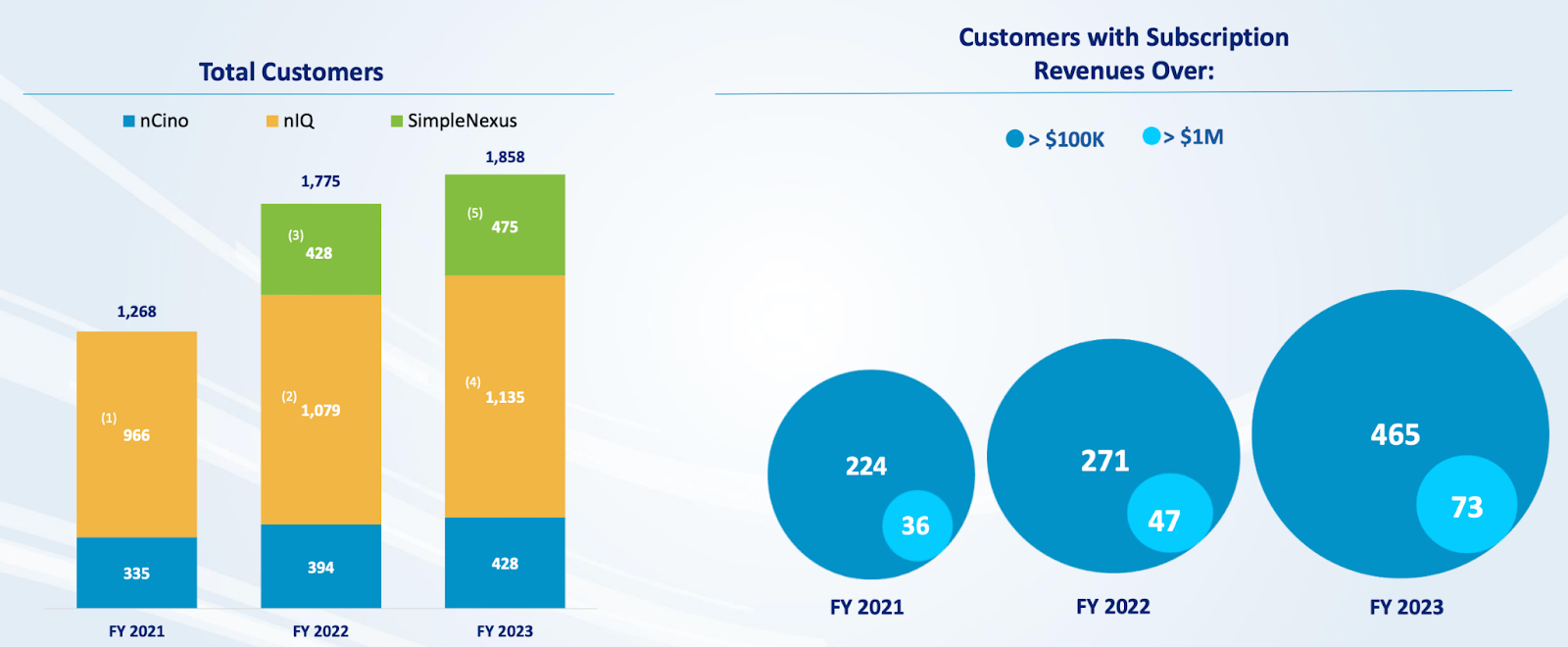

While smaller banks might have faced a less severe impact as of Q1 , enterprise banks appear to have been playing a much more critical role in driving NCNO's growth due to the larger deal sizes. Since the IPO, an increase in the number of enterprise customers has positively correlated with the overall revenue growth.

{kind=link}

In FY 2023, for instance, growth accelerated to ~49% from ~34% in FY 2022 as the number of customers with >$1 million in subscription value increased by over 50% to 73. Conversely, as the same group of customers saw a slower 30% growth YoY in FY 2022, revenue growth actually decelerated to ~34% from ~48% in the previous FY.

Considering that interest rates will remain elevated at least until the end of the year not only in the U.S. but also Europe, I feel that NCNO may face delayed and sluggish recovery. In a worse-case scenario, I would probably also expect that a rebound may only happen sometime mid-next year.

Another area where NCNO may continue to see weakness is in the U.S. mortgage business, where it already saw some churn due to some brokers downsizing and going out of business . In general, home borrowers may delay purchase decisions due to the high-interest rate environment today , effectively pressuring the overall mortgage brokerage business.

Freddie Mac

A survey conducted by Freddie Mac as recently as last month in June also suggested below-average confidence in the housing market today, despite the overall improvement since Q4 last year.

Catalyst

Despite the near-term challenges, I believe that NCNO may remain well-positioned to capture the global opportunities in cloud banking transformation longer term, given its relationship with Salesforce ( CRM ), and may see growth reacceleration as the temporary macro headwind subsides.

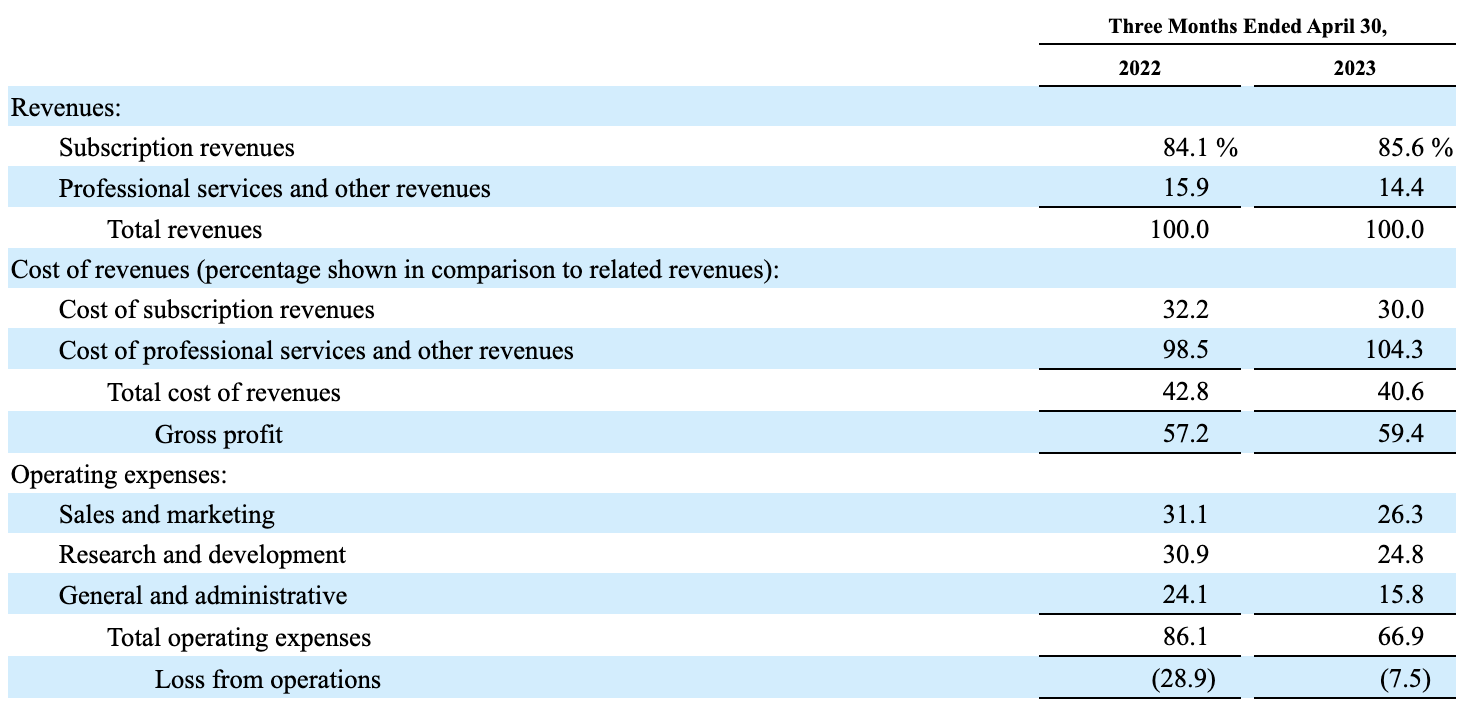

Fundamentals are not exceptional but have been decent and improving as of Q1, as highlighted by the positive OCF/operating cash flow and significantly-narrowed operating loss. Cash balance also improved to ~$98 million in Q1, while NCNO virtually has no debt. Its debt-to-equity ratio stood at 0.07x as of Q1.

{kind=link}

In Q1, NCNO reiterated its shift towards profitable growth , and things have looked better. Operating margin expanded as NCNO significantly reduced all operating expenses as % of revenue by 500-800 bps. On a non-GAAP basis, NCNO also had a positive operating margin of 10% . NCNO will also expect to maintain the same operating spend outlook throughout FY 2024 with forecasted 16%-17% revenue growth.

I think that it will be important to monitor NCNO's progress in maintaining such a profitable growth outlook beyond FY 2024, especially once headwinds subside and when it potentially needs to increase spending to reaccelerate growth.

Growth acceleration with operating profitability may not be an unrealistic expectation. There are two possible reasons. First, SimpleNexus' integration may provide room for more growth opportunities once the mortgage market recovers. In Q1, we learned how NCNO continued to win new logos with SimpleNexus despite the tough macro situation:

So we're pleased with where we sit. As of now, we see a total of 16 cross-sales of SimpleNexus that we've done into the nCino customer base. When I look at the growth of pipeline of large financial institutions with SimpleNexus, it shows that that market coverage is helping.

Source: Q1 2024 earnings call

Secondly, NCNO does not need to sacrifice its bottom line to drive market share growth for SimpleNexus, since it appears that the newly-acquired offering already contributes positively to profitability and cash flow generation:

Additionally, although we are no longer breaking out SimpleNexus, we have received questions about their impact on our bottom line and wanted to note that we expect Simple Nexus, which you will increasingly hear us refer to as our U.S. mortgage business, to generate non-GAAP operating income and contribute positive free cash flow for fiscal '24.

Source: Q1 2024 earnings call

Valuation/Pricing

To estimate the target price for NCNO in FY 2024, I assume the following bull vs bear scenario:

-

Bull scenario (50%) - NCNO to finish FY 2024 with revenue of $478.5 million, meeting the high-end of its 17% revenue growth guidance. I would assume that the non-GAAP operating margin remains at the same level at 10%, also in line with the guidance. I assign NCNO a P/S of ~8x, where it is currently trading at.

-

Bear scenario (50%) - NCNO to finish FY 2024 with revenue of $469.6 million, missing its revenue growth guidance slightly with 15% growth. I expect NCNO's P/S to contract to ~6x, revisiting its May figure.

Author's Own Analysis

Consolidating all the information above into my model, I arrived at an FY 2024 weighted target price of ~$30 per share. Since NCNO has been trading between $30-$31 most recently, it appears fully valued.

As such, I rate the stock neutral. My target price model also suggests that even a minor execution error resulting in a slight guidance miss may cause NCNO to see a potential correction, as reflected in the 15% revenue growth projection under the bear scenario.

Conclusion

As a business providing cloud-based banking software to global FIs, NCNO may continue to see challenges from the weak macro environment despite its strong positioning to capture future growth opportunities. Revenue growth had been strong between 30%-50% with a clear path to profitability. However, project delays and churns will lead to a slower growth rate of 16%-17% in FY 2024.

NCNO also appears fully valued, and as such, I give the stock a neutral rating. Additionally, my target price model indicates that even a small execution error and slight guidance miss could result in a potential correction, as seen in the 15% revenue growth projection under a bear scenario.

For further details see:

nCino: Challenged Outlook And Fully Valued